FMCQF - Fresenius Medical Care: What Can We Expect For 2024E

2023-12-28 08:16:55 ET

Summary

- Fresenius Medical Care has seen a recovery in its share price after a dip in October 2023, presenting an attractive upside potential.

- The company's 3Q23 results showed continued organic growth, successful execution of its turnaround plan, and raised earnings outlook.

- While FMS still has average margins and profitability compared to its peers, it remains undervalued and offers a compelling investment opportunity.

Dear readers/followers,

Fresenius Medical Care (FMCQF) (FMS) is a company that I've been covering for years, and investing in for years. For certain parts of my position, I'm actually at a very impressive overall RoR. That is not the case for the entirety of my current position in Fresenius - and as before, my investment into the company is done using the larger Fresenius company, not the Fresenius Medical Care Arm.

Still, Fresenius owns a large part of the Medical Care company, so this is still a relevant approach and one that I believe will eventually result in outperformance. I would be lying if I said that I wasn't disappointed at the amount of time that it's taken for the company to see even some extent of normalization here.

In this article, I'll update my thesis for the next year and see what we may expect for 2024-2026 from the Medical Care company.

Also, I've had some short-term success with the recommendation to my last article - though in the larger context, the company still needs to recover far more.

Seeking Alpha Fresenius Medical Care (Seeking Alpha)

Fresenius Medical Care - A lot to like, assuming the company eventually reverses

The market has already spoken as to what is too cheap, and what isn't. Back in October of 2023, the company dove for a month or two, before recovering firmly back to a $20/share level for the FMS ticker. The yield here is not attractive - we're talking less than 3% in an environment with 4%+ risk-free - so the upside for the company has to be significantly attractive for this to make any sort of sense.

Thankfully, that's actually the case here.

My last article on this company coincided with the crash, which in itself was an overreaction to the Danish company Novo Nordisk (NVO) and its weight-loss drug Ozempic. I spent the article showing why this was an overreaction, and why even if Ozempic caused everything that its proponents hoped, this still wouldn't mean any sort of fundamental decline for Fresenius.

Ozempic is Novo's GLP-1 drug, and Novo has been pinning a fair bit of hope on the drug for the future. As a result of this, dialysis companies that worked on the other side of this area dropped double digits back in mid-October when the efficacy of this drug became clearly indicated. I don't just mean FMS, because I also invest in other companies. Businesses like Baxter (BAX), and Outset Medical (OM), dropped double-digits, with onset dropping the most at 21% in a single day, being the most exposed in this context.

The reasons why the impact of Ozempic isn't as bad as many seemed to fear are clear - or in this case, actually unclear. From the lack of clarity in healthcare savings costs, the fact that it's in no way a cure for Kidney failure, but simply a delay in the progression of kidney disease, seems to imply to me that the market didn't understand that this was potentially only a revenue hit - not a fundamental business threat.

We have 3Q23 results to look at, which came out in November about 2 months ago.

The company's current heavy focus is on unlocking its value as a leading kidney care company. It's cut down segments to two, simplified the company's financial reporting, and overall optimized its capital allocation and how it works with its segment with its FME25 targets, in both Care Delivery and Care Enablement, it's now two segments.

The company itself addressed in the beginning, the expectation of the impact of GLP medications.

{kind=link}

3Q23 saw the company confirm its upward trajectory. We're talking about continued organic growth by both segments, continued treatment growth, and successful execution of the company's turnaround plan.

This has resulted in the 2025E savings and optimization targets being fully on track here. The company also raised its earnings outlook. These trends also fully reflect the trends going on in my investment, Fresenius, which at last may see some above-market returns that I have been expecting for a long time.

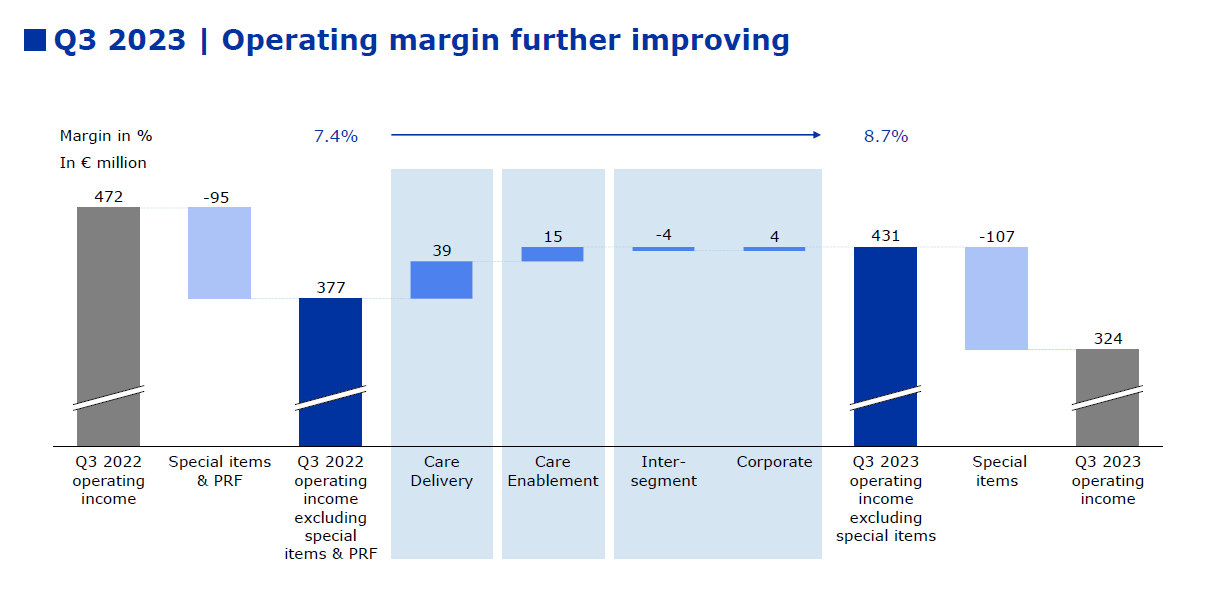

Organic growth for the company was enabled by growth in both of the segments, driven by both volume and price - and the company's operating income improved based on better performance, and expense management while managing the negative continued impacts from inflation and a non-recurring payment item. Here is a bridge for the operating margin improvement.

{kind=link}

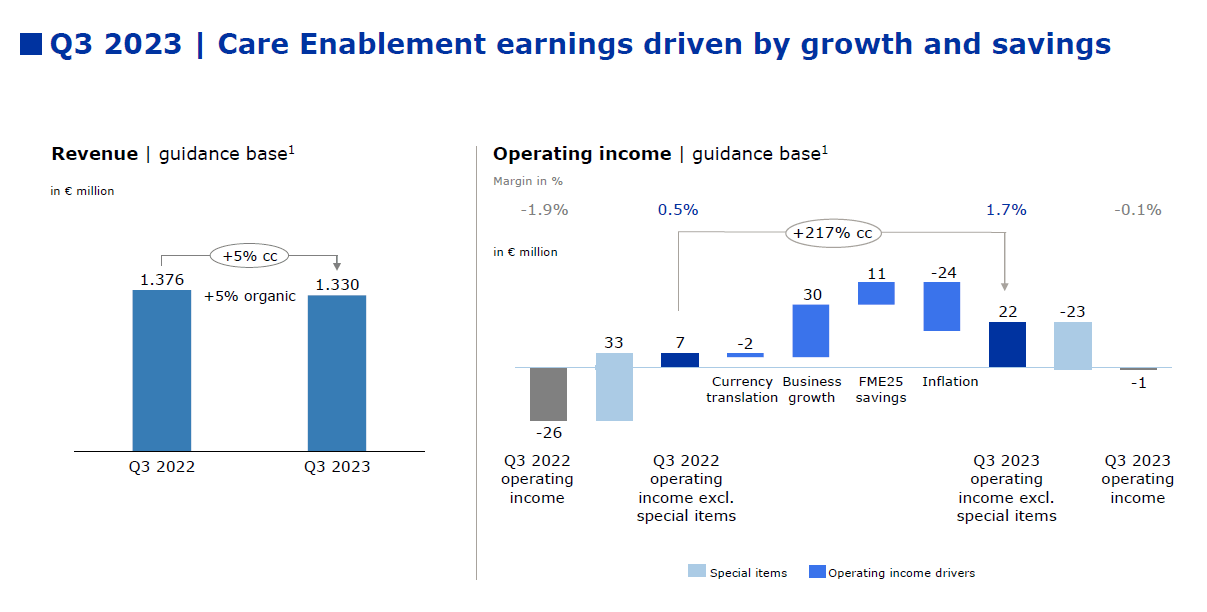

The underlying trends are what interest me here. We're talking solid organic revenue growth in the care delivery segment, with positive U.S. same market treatment growth when adjusted for exits from less profitable contracts. The company has managed to combine business savings and finally optimize its mix. Care enablement, the other sector, saw better sales of in-center disposables, machines, and home products as well, with positive continued impacts from good pricing measures. The bridge here is even more impressive in its improvement.

{kind=link}

The company still isn't above average in anything. When looking at the sector of Healthcare companies, the problem we find here is that FMS still is fairly average, in both gross, operating, net margins, and most of the fundamental KPIs when looking at profitability. The same is true for fundamentals. Debt to EBITDA is still at around 4x, with an interest coverage of sub-3x. Not the greatest trend.

At the same time, we have good signs for the company. The company's top-line indicators are growing sequentially, which implies that the company needs to improve its operating margins to really bring about some change here - and that's exactly what FMS is now reporting.

Also, and important to remember, that no matter how you slice it, this company is still quite cheap.

Price is the single most important factor once we determine that a company is worth investing in based on the foundations of its business model - which I believe Fresenius Medical Care is.

{kind=link}

Again, not the most efficient or attractive business model - at least not yet - but definitely where I believe it to be "good enough".

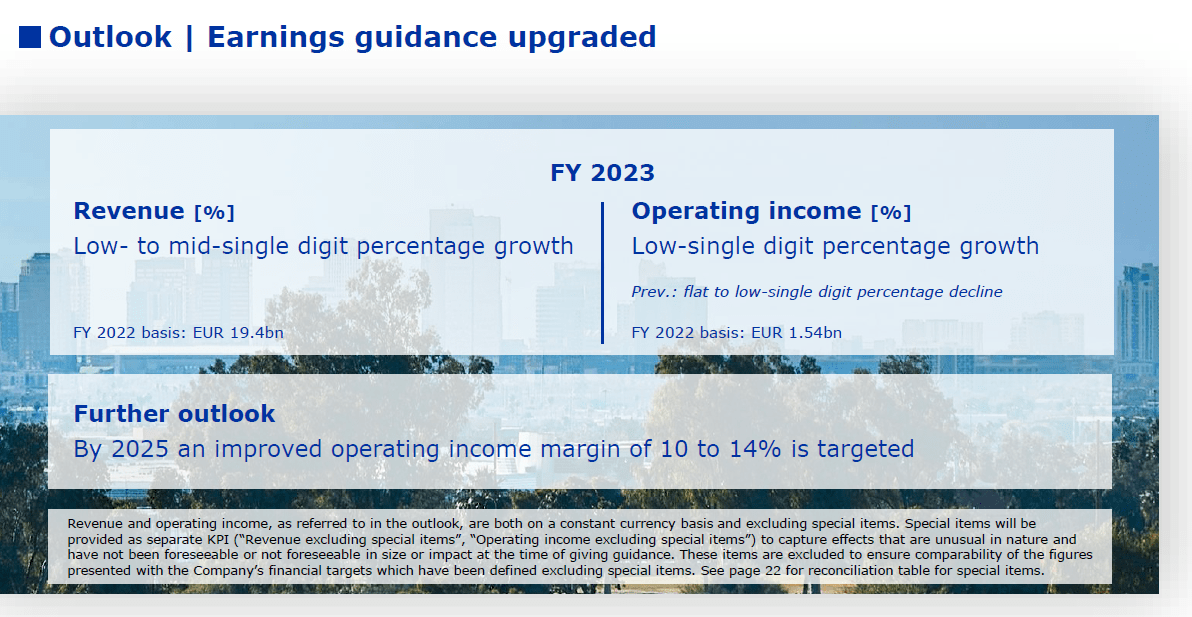

FMS had a good 2023 3Q - good enough to where the company raised its earnings guidance for the year, which should provide some support for the share price and valuation going forward.

{kind=link}

Let's look at what amounts to the company's risks and overall upside here.

Risks & opsides for Fresenius Medical Care

I consider this company to have a no-nonsense upside here for the long term, and have been undervalued - albeit for a good reason - for a very long time. Risks to the company do exist, and some of them are operational, not related to macro. The company's profit mix is something to be aware of because almost all of the company's earnings come from commercial insurance policies. If the landscape for these policies or how these are handled on a political scale changes, the potential impact on Fresenius's profits is not insignificant. I don't see this as dire as some analysts do - I believe insurers can affect these factors, but a fundamental downturn over a long time is unlikely - but the risk exists. We have some proof that pricing pressure is coming - just look at the relatively recent Supreme Court ruling against DaVita.

On the upside, the company is heavily diversified both in geography and business mix, its home-treatment rates which are increasing are going to lead to better margins (conceivably at least), and the company has a working venture capital arm and is investing in ways to treat ESRD aside from traditional tools. More importantly, though, the company is without a doubt and without argument, at a very cheap level given that its earnings have troughed.

Let's look at the updated valuation upside for the company.

Valuation for Fresenius Medical Care

This company has been troughing for years. We've seen earnings decline since 2021, but the earnings growth had slowed down to near-zero in 2019. Shareholders of this company have essentially been losing money since 2018 when the company was overvalued at almost 18-20x P/E.

It's currently trading at 16x normalized, but closer to 10-12x if we account for a future earnings growth.

Is Fresenius Medical Care the best company that you can invest in here?

I do not believe that to be the case, no - but it's a solid business with a good upside, and deserves highlighting for this fact.

You can heavily impair the company's earnings to only look at the last 5 years, normalize under P/E 15x at 14x, and still see a market-beating RoR and upside.

If the company's forecasts materialize, which they do over 50% of the time for the past decade, you're looking at almost 20% annualized RoR with a 42%+ RoR in 3 years for this business. If you're willing to normalize the multiple at closer to its 20-year average, which is 18.5x, that RoR goes up to 33.5% per year or almost 80% in total.

I still believe that Fresenius, with native ticker FRE, offers you a more compelling mix and upside because the estimates for the company are better growth, a better mix, and not as concentrated revenues. Furthermore, the decline in Fresenius SE & Co KGaA wasn't as deep as it was in the medical care segment, FRE has better fundamentals with a full BBB, and a yield of 3.3%, rather than sub-3%.

So, overall, Fresenius is still the better pick here, according to me - but FMS with medical care still constitutes a "BUY" here.

I'm not changing my target for the company, and my updated thesis for 2024E is as follows.

Thesis

- I view FMS as a company to buy. It's a leader in the kidney care sector and owns large parts of the dialysis operations in the US market as well as on an international basis. It's BBB-rated, has an acceptable yield, and has a near-72% upside going forward to the next few years.

- However, due to the corporate structure, governance, and the appeal of its "parent", I consider Fresenius to be the superior investment if comparing the two. FMS is a "BUY", and it has upside - but FSNUY/FRE has a better thesis. I still view this as being the case.

- However, the company is a very solid "BUY" here - and the recent decline due to the Ozempic trial results does not faze me in the least. I show you two reasons why this company is actually unlikely to see any sort of impact as of this, at worst we'll see some delays in treatments.

- The recent company quarterly earnings report means that I am sticking to my price target for the company, as well as my stance - and I still consider it "cheap" despite not being as cheap as it was back in October.

- I give FMS a PT of $34/share for the long term and rate it a "BUY".

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Because the company fulfills every single one of my criteria, it is a "BUY" to me here. I'm talking about both FMS and FRE here, but this article is on FMS.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Fresenius Medical Care: What Can We Expect For 2024E