FSNUF - Fresenius: One-Off Special Situation Opportunity To Buy

Summary

- Over the last six months, Fresenius has seen the exit of its CEO, increasing activist exposure, and is reviewing the deconsolidation of its largest subsidiary Fresenius Medical Care.

- We view this deconsolidation as a positive special situation that will result in significant deleveraging.

- Our simple scenario analysis values the shares on PBR 0.7x post-deconsolidation, with our fair value estimate being PBR 1.0x. We have a buy rating.

Investment thesis

Fresenius ( OTCPK:FSNUF ) is expected to deconsolidate its subsidiary Fresenius Medical Care (FMS). We believe this special situation is a positive as a deleverage play and rate the shares as a buy.

Quick primer

Fresenius is a German healthcare group with four core business segments. Fresenius Medical Care ((FMS)) (a separately listed company where Fresenius has a 34% stake) (key peer is DaVita ( DVA )) runs the world's largest network of dialysis clinics, providing treatment for patients with chronic kidney failure. Kabi specializes in intravenously administered generic intravenous drugs, clinical nutrition, and infusion therapies. Helios is a private hospital operator, as well as approximately 300 Occupational Risk Prevention Centers in Spain. VAMED manages projects and provides services for healthcare facilities worldwide.

The company will report FY12/2022 results on February 22, 2023 .

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

Our objectives

In March 2021 we reiterated our sell rating on Fresenius, citing deterioration in free cash flow generation and management's odd call to review its group structure in order for capital markets to fully appreciate its company value.

Nearly two years on, management announced on February 9th, 2023 that it was considering deconsolidating the subsidiary Fresenius Medical Care (to be called FMC from now on in this piece), the dialysis unit that is currently undergoing difficulties managing cost inflation and staffing shortages, as well as former CEO Carla Kriwet stepping down at her own request and by mutual agreement with Fresenius over strategic differences. Activist fund Elliott Investment Management has taken a stake in the company in October 2022, following the resignation of former long-standing Chief Executive Stephan Sturm in August 2022.

With Sturm now gone and potential changes ahead to the group, we want to ascertain whether the shares now present a buying opportunity.

Deconsolidation of Fresenius Medical Care - a deleverage play

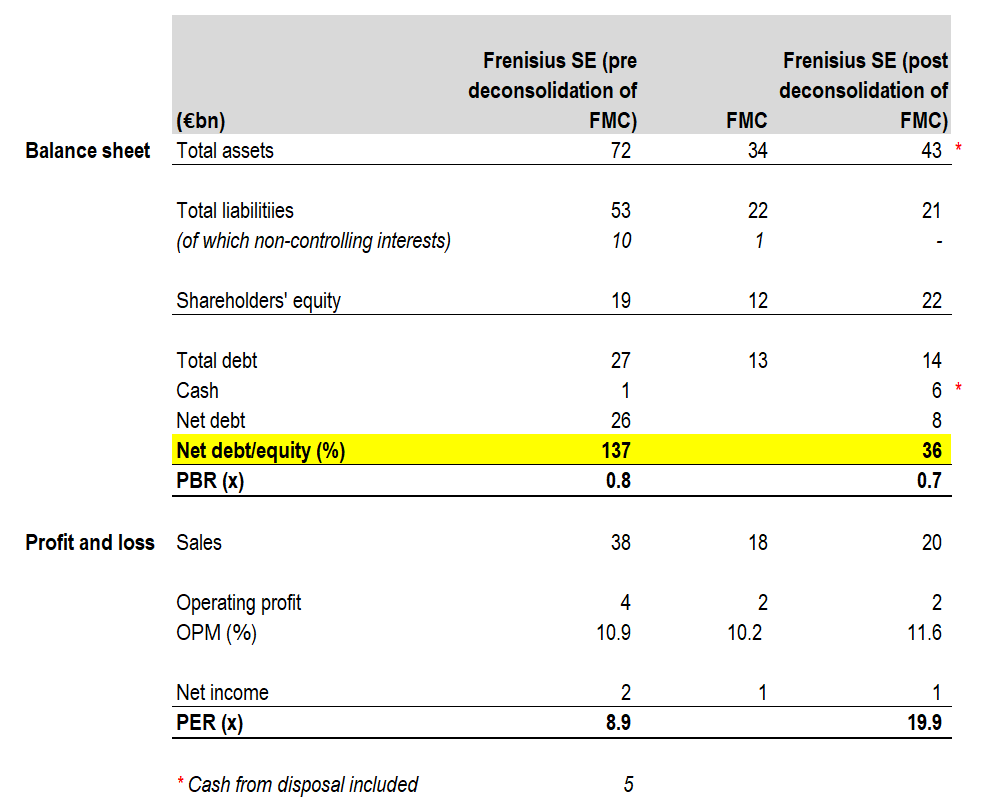

It seemed only fair to illustrate what an actual deconsolidation of FMC would look like for Fresenius. There are multiple scenarios based on the size of the stake sale as well as inter-group transfers of assets and liabilities. We will keep it simple, and have assumed the following:

- Fresenius disposes of all of its current 32.17% stake.

- There are no inter-group transfers of items on the balance sheet.

- Fresenius' non-controlling interests are 100% from FMC (in reality more like 90%)

- FMC's shares are sold at a 40% premium to the current share price - a generous but not unusual yardstick for takeout (roughly EUR5bn ). We ignore any impact of capital gains.

We have then modeled a simplified balance sheet and profit and loss account to show how Fresenius will transform. We have taken numbers from the FY12/2021 accounts.

Simplified scenario analysis of FMC deconsolidation

Simplified scenario analysis of FMC deconsolidation (Company, Bloomberg)

{kind=link}

The key changes to the balance sheet are as follows:

- There is significant deleveraging, with FMC's debt disappearing from the group and an additional EUR5 billion cash generated from the stake disposal.

- The resultant net debt-to-equity ratio drops from 137% to 36%, which is far more prudent. Deleveraging can be a positive catalyst for valuation multiple to expand, particularly for PBR.

From a P&L perspective, we note that there is potential for some margin enhancement, but the PER multiple rises significantly. Unfortunately, ROE will drop notably from 10% to around 5%.

This scenario places Fresenius' shares in a positive light. The key attraction is the strengthened balance sheet via an asset sale, lowering leverage significantly which in turn makes the business more attractive as a going concern.

What could go wrong?

We have taken a very simplified approach to this special situation event, and consequently, there are many variables that could lower any positive impact. The obvious one is that the stake sale is a small token gesture, meaning that although deconsolidation takes place, there is virtually no cash generated - but net debt to equity will still notably improve.

If the offer price for FMC's shares has a low premium or below market price, there could be an outcry resulting in a delay in a deal taking place. FMC will also have to either find adequate financing to buy back its shares or find a willing partner who would be happy to invest at a higher price.

Valuation

For a mature ex-growth company (Type 2 diabetes is a bigger global health concern than Type 1 and does not need dialysis treatment), valuation multiples such as price to sales will be low. The bright spot is the strengthening balance sheet via asset sale and deleveraging, and if the company reaches a net debt-to-equity ratio of sub 50% this should result in a PBR multiple being closer to 1.0x, denoting 40% upside. We believe the shares are currently undervalued.

Risks

Upside risk comes from the company announcing a formal group restructuring plan involving the divestment of FMC on February 22nd, 2023. This should act as a positive catalyst for the stock.

Downside risk comes from company management delivering a plan that has no concrete details about the size of the stake sale, timeline, or any definitive guidance on how the capital structure of the company will change.

The largest negative event would be management stating that the deconsolidation of FMC is off the table. However, with activist pressure mounting and former CEO Sturm now gone, we believe this is unlikely.

Conclusion

Fresenius has been a value trap with the share price in decline since 2017. There appears to be an upside opportunity now, although under new management and with a potentially huge shake-up in the business, the outlook for the longer term looks neutral to challenging. We recommend buying the shares for this special situation.

For further details see:

Fresenius: One-Off Special Situation Opportunity To Buy