FSNUF - Fresenius: Still Struggling Still Undervalued

2023-04-23 07:22:20 ET

Summary

- Fresenius reported solid results for fiscal 2022, but keeps missing its own growth target - at least for the bottom line.

- The company is also losing its status as dividend aristocrat and is keeping the dividend only stable after a streak of 29 consecutive years of dividend increases.

- Management also announced a new strategy with the Fresenius Medical Care deconsolidation being a major part of this strategy.

- In my opinion, the stock remains undervalued.

Among the investments I made in the last few years, Fresenius SE ( FSNUF ) is certainly a candidate for the biggest disappointment. Of course, I could collect dividend payments in the last few years, but the stock is trading almost 40% below the price I purchased the stock. And I bought the stock after it declined already 50% from its all-time high, but the stock kept declining.

In case of Fresenius my investment thesis did not work out so far, which is reason enough to take a close look again and again at the company and the stock (at least as long as I keep holding the stock).

When to Quit?

Fresenius SE is a disappointment since 2017 when the stock started to decline and when I purchased the stock in early 2020 after it had already declined 50% from its previous all-time high, I was pretty sure I had a bargain on my hands. But not only did I barely see a day when the investment was in the green, the stock has been cut in half again and is still trading more than 70% below its previous all-time high.

I remained bullish all the time and still see Fresenius as clearly undervalued but we must also ask the question if it shouldn’t be time to admit defeat and sell the stock and acknowledge that I was wrong about Fresenius.

In the spirit of these thoughts let’s ask the question when it is time to quit on an investment. The answer is actually simple: When the fundamentals of a company are not matching the investment thesis anymore. And there are several possibilities when fundamentals are not matching the investment thesis:

- Fundamentals about a business may change over time due to new trends or unforeseen events (COVID-19 for example) and the original valid investment thesis might become inadequate. This could make it necessary to alter an investment thesis a little bit or in some cases just admit that we were completely wrong.

- It is also possible that an investment thesis about a company was wrong from the beginning and did not match the presented fundamental picture. While there are some hard facts about a business (reported numbers on income statement or balance sheet for example) there is a lot of room for interpretation and different analyst might draw different conclusions from the same income statement. Hence, we should always entertain the possibility that an investment thesis was wrong from the start.

However, there is at least one reason that should not make us quit on an investment – a stock price that remains deeply undervalued. As long as we a convinced that a business should trade for a much higher share price as the fundamentals imply a higher share price, we should hold to the stock. Similarly, we should not give in and buy a stock we are convinced is overvalued just because the stock keeps trading for extremely high valuation multiples.

As I have written several times, the stock market is a complex system and making precise assumptions is very difficult or almost impossible. And the possibility for making a huge mistake is rather high. And in that spirit, we should look at all investments again and again and ask ourselves if our thesis is still valid. It is possible that we made a mistake, but it also happens quite frequently that the stock market is getting it wrong, and Mr. Market is offering absurd prices for several years in a row (both overvaluation as well as undervaluation being possible).

Struggling Business

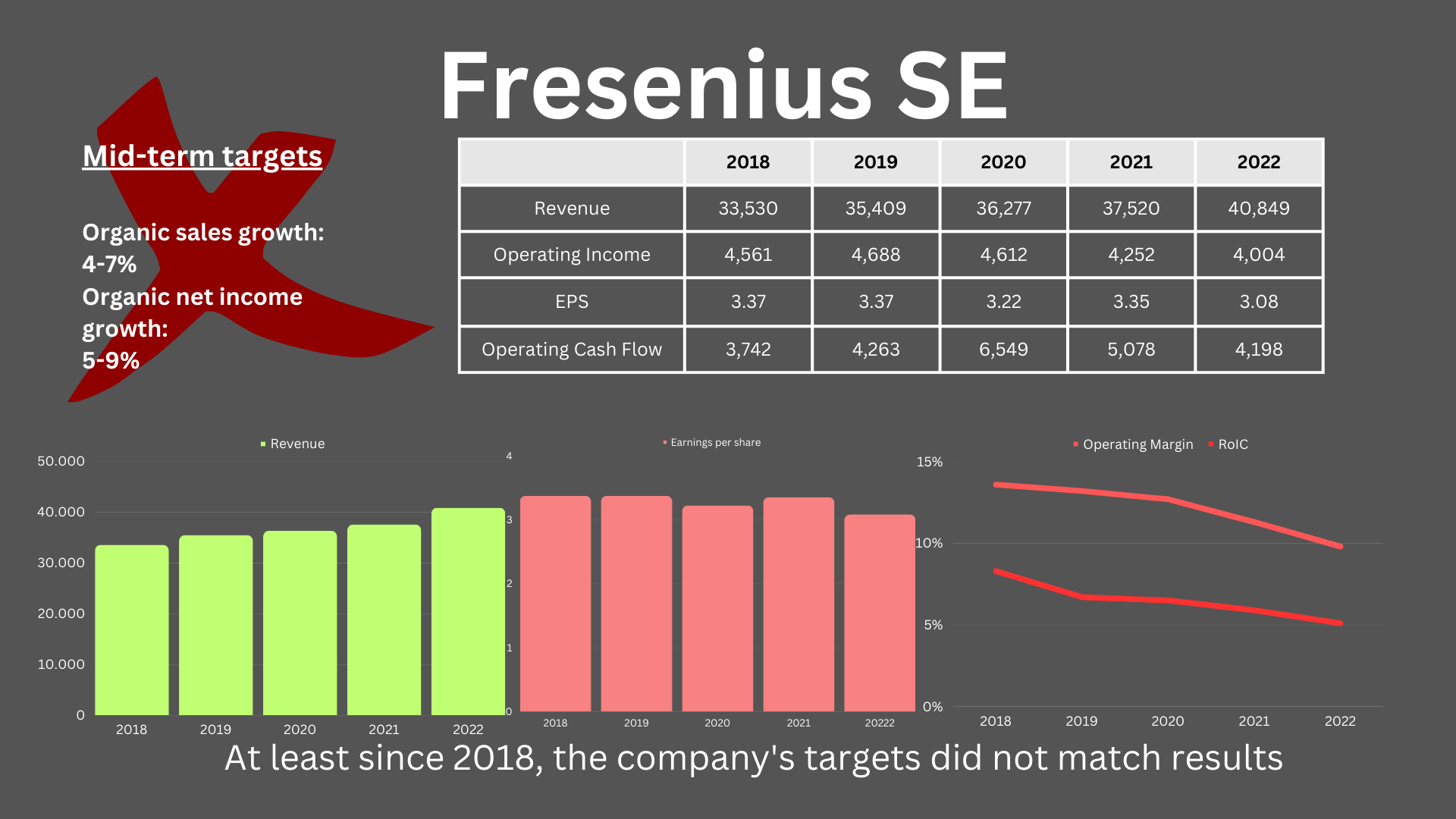

And when asking ourselves why Fresenius is struggling and the stock is caught in a bear market since 2017, the results of the last few years might provide some answers. Fresenius had mid-term growth targets for the years until 2023. Organic sales growth was expected to be between 4% and 7% and organic net income growth was expected to be between 5% and 9%.

{kind=link}

And especially the results for fiscal 2022 were a disappointment once again. Or to put it a little more moderate: were not reflecting the growth targets of Fresenius. In fiscal 2022, Fresenius SE generated €40,840 million in revenue and compared to €37,520 million in revenue in the previous year the top line grew 8.8% year-over-year. Growth in constant currency was at least 4% year-over-year. And while the top line could still grow, operating income declined from €4,158 million in fiscal 2021 to €3,321 million in fiscal 2022 – resulting in 20.1% YoY decline. And finally, diluted earnings per share declined 8.1% year-over-year from €3.35 in fiscal 2021 to €3.08 in fiscal 2022.

{kind=link}

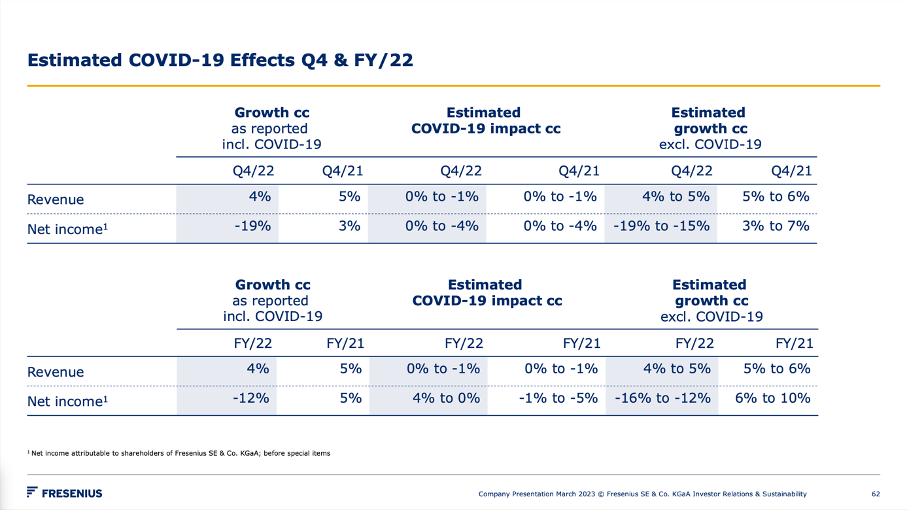

Of course, we should not ignore that the last few years were rather difficult for Fresenius and COVID-19 had a huge impact. However, for fiscal 2022, Fresenius is not seeing a huge negative impact on results due to COVID-19 anymore and results were still rather disappointing.

{kind=link}

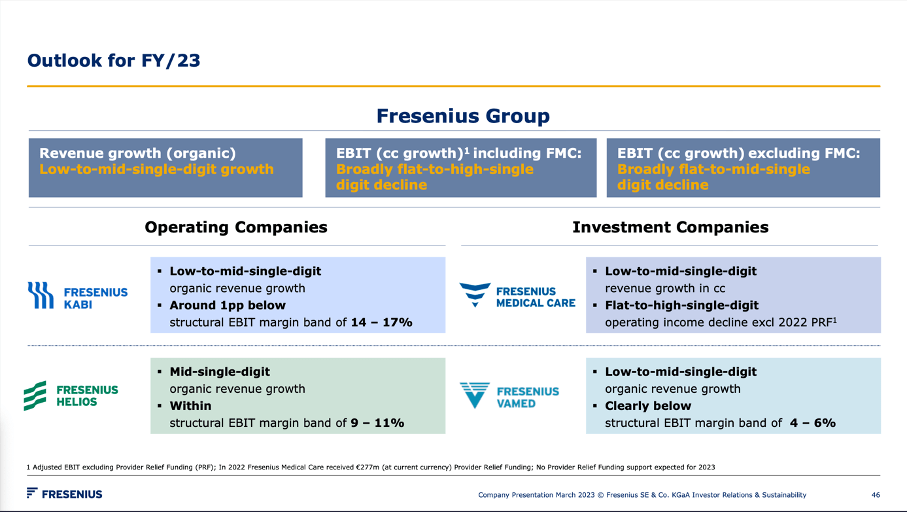

When looking at the outlook for fiscal 2023, the target for revenue is low-to-mid single digit organic revenue growth. However, EBIT is expected to be flat in the best case but could also decline in the high single digits and therefore Fresenius will keep struggling. Hence, the picture for Fresenius is still not great and we still can claim that in theory there is growth potential, but management is struggling to actually report growing earnings per share.

{kind=link}

And when looking at the results in the last few years one should certainly be allowed to ask the question if Fresenius can grow again. It doesn’t help much when the long-term outlook is favorable, and management has ambitious financial targets but fails to deliver. But to be fair, revenue growth is visible in the last few years – Fresenius only fails to generate bottom line growth.

Highly Indebted Business

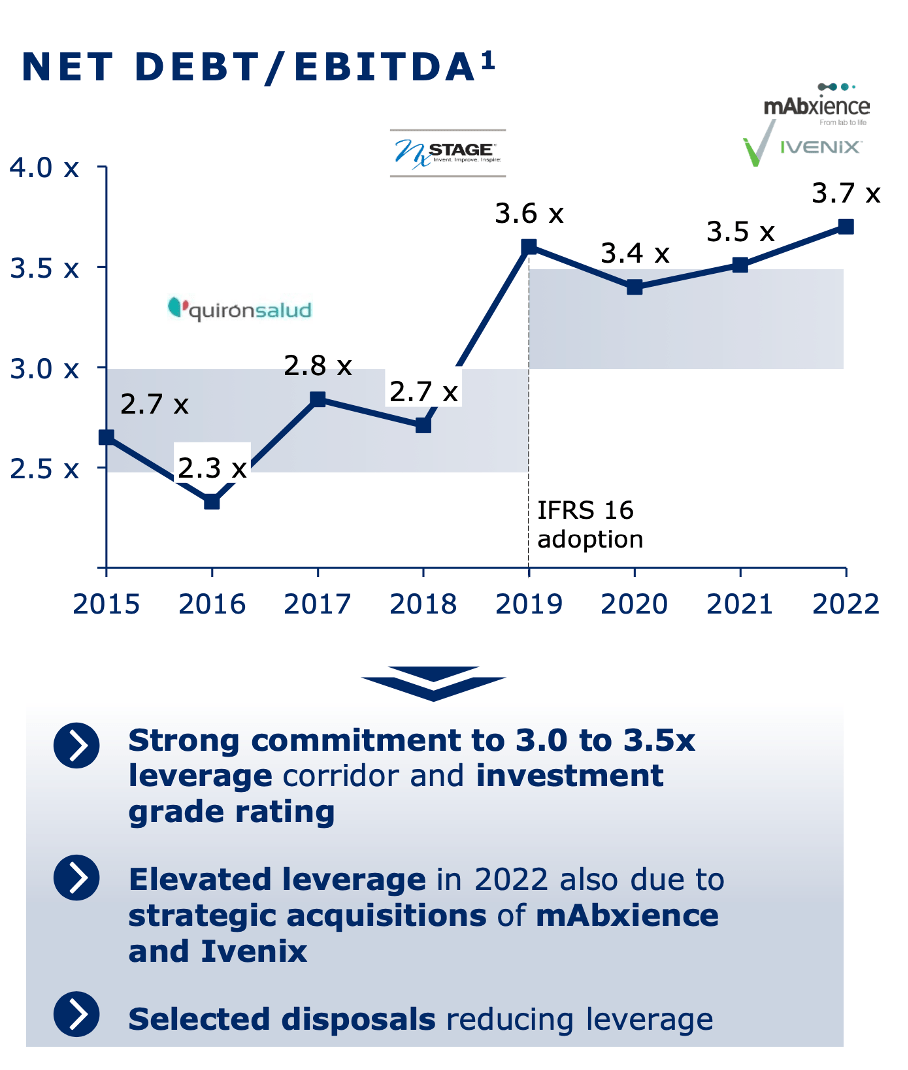

The second major problem is one, I have also mentioned several times in the past – Fresenius has extremely high debt levels. Due to several acquisitions, it is trading for 3.7 times net debt (compared to EBITDA). And although Fresenius is committed to a target range of 3.0 to 3.5 leverage, I would still see these numbers as rather high and not the most ambitious target a company can have.

{kind=link}

On December 31, 2022, the company had €27,763 million in debt on its balance sheet. Compared to a shareholder’s equity of €32,218 million this is resulting in an acceptable debt-equity ratio of 0.86. However, when comparing the total debt to the operating income of €4.0 billion to €4.5 billion, it would take between 6 and 7 years to repay the outstanding debt – and such a long time is not acceptable. And €2,749 million in cash and cash equivalents are only enough to repay a fraction of outstanding debt.

And Fresenius has not only rather high debt levels, but also €31,444 million in goodwill on its balance sheet and when subtracting these (more or less) worthless assets from the balance sheet, the shareholder’s equity would decline close to zero.

Dividend

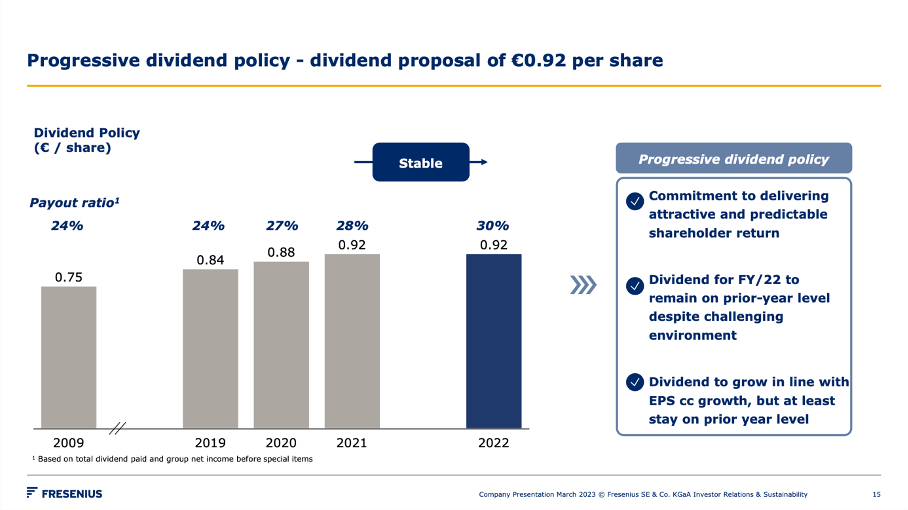

A third problem right now is the dividend of Fresenius. Or to put it a bit mildly: the dividend is also underlining that Fresenius is struggling. While Fresenius is describing its dividend policy as progressive, the truth is that the proposed dividend of €0.92 must be seen as a disappointment. It is the same annual dividend as last year and therefore a streak of 29 consecutive years of dividend increases ended for Fresenius. The company was one of the few German dividend aristocrats, but in Germany management and investors don’t pay much attention to the status “dividend aristocrat” (in contrast to the United States). In the United States, companies are sometimes desperately trying to increase the dividend in very small steps to keep the status “dividend aristocrat” or “dividend king” – 3M Company ( MMM ) or Walgreens Boots Alliance ( WBA ) would be two examples right now. In Germany (or Europe) however, keeping the dividend only stable is much more accepted.

{kind=link}

Although the dividend was kept only stable, it is still resulting in a dividend yield of 3.6% which can be seen as solid dividend yield. When using earnings per share of fiscal 2022, we get a payout ratio of 30%. This is still a rather low payout ratio, but clearly above Fresenius’ target range of 20% to 25% and the decision to keep the dividend only stable is therefore not surprising.

New Strategy

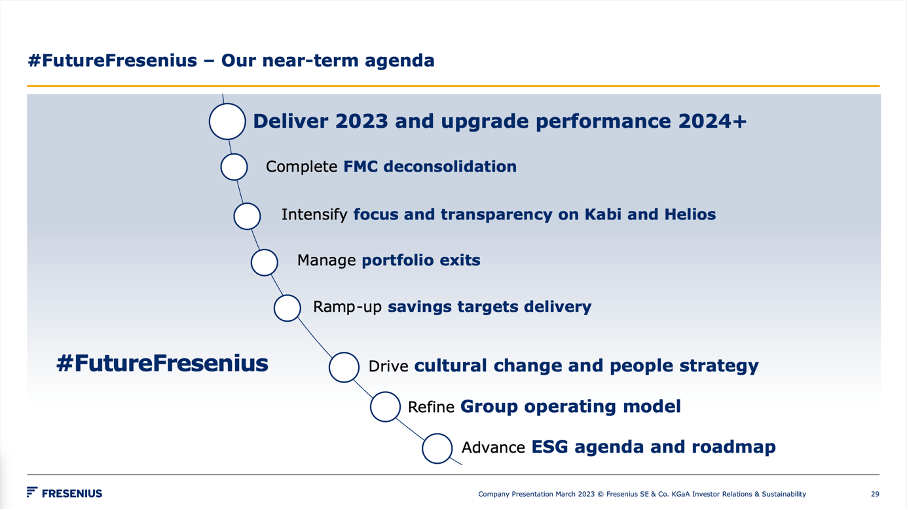

To countervail these negative developments, Fresenius announced a new strategy, which is marketed using the hashtag #FutureFresenius. One of the major news from this new strategy is the Fresenius Medical Care (FMS) deconsolidation. The legal from of Fresenius Medical Care will be changed to a German Stock Corporation (“Aktiengesellschaft”). The goal is to simplify the governance and group structure. Management is expecting the conversion to become effective by the end of 2023. Fresenius will focus on therapy to advance patient care across three platforms – Biopharma, MedTech and Care Provision. Management is expecting annual structural productivity improvement to approximately €1 billion by 2025.

{kind=link}

And while implementing a new strategy sounds great and should make us confident, we also must question how good such strategies are and if they really will have an impact. Fresenius would not be the first business announcing a new major strategy that is not working and won’t really have an impact.

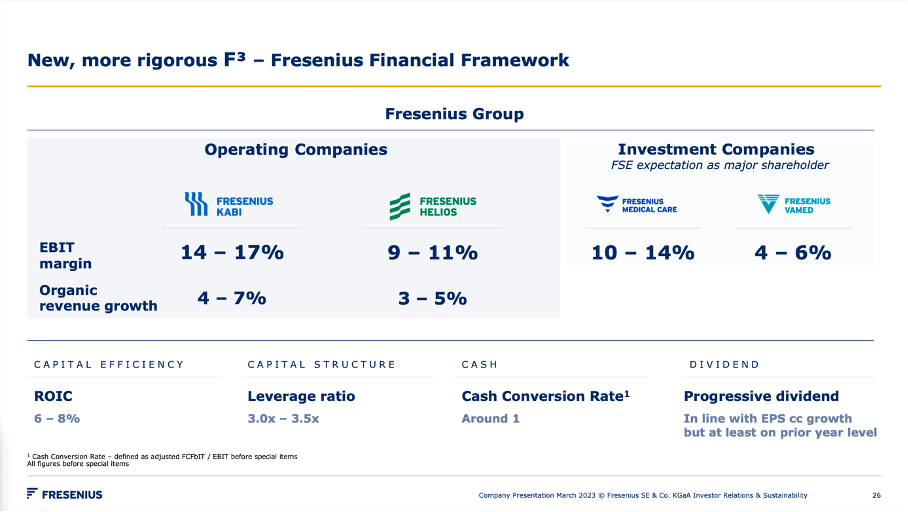

Fresenius is also providing a new outlook it is calling the Fresenius Financial Framework (or F3 in short). While the company is providing organic revenue growth targets for Fresenius Kabi and Fresenius Helios it is not offering mid-to-long-term targets for the Fresenius Group.

{kind=link}

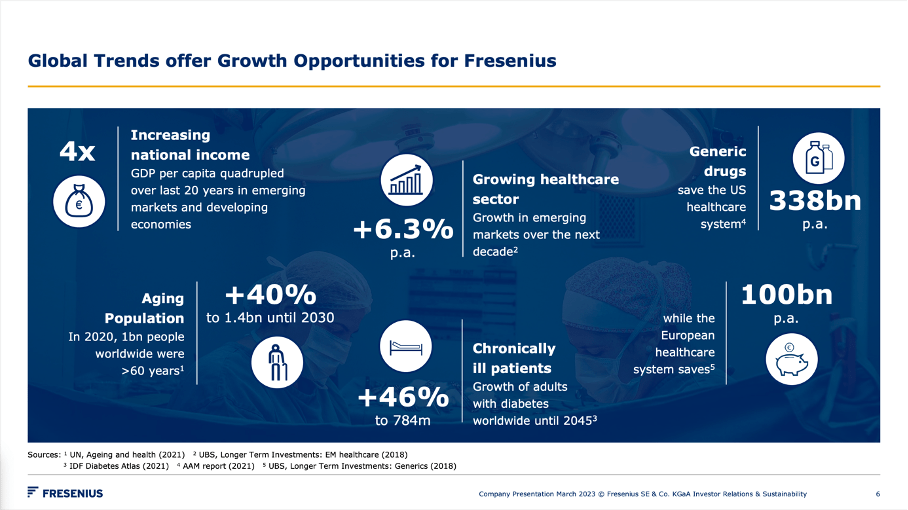

Although Fresenius was struggling in the last few years, the growth rates according to the bigger picture are still quite good and should make us optimistic. As I have mentioned several times in the past, Fresenius will profit from the aging population which will increase the demand for healthcare. Population above 60 years will improve 40% until 2030 to about 1.4 billion people. The number of chronically ill patients will also increase about 46% to 784 million until 2045.

{kind=link}

And we should especially be optimistic as there are several long-term tailwinds driving top line growth for Fresenius. We can also remain confident that management will be able to transform the top line growth to bottom line growth again and margins will also improve.

Intrinsic Value Calculation

In my opinion, Fresenius is still undervalued. When using the results from fiscal 2022, Fresenius SE is trading for only 8 times earnings and for a profitable and stable business (even if the business is struggling to grow the bottom line) such a valuation multiple is not justified. A single digit valuation multiple is only justified for businesses in constant decline.

However, we can remain optimistic that Fresenius will be able to grow its bottom line again – like it has grown its top line in the last few years. In my last article , I calculated an intrinsic value of $50 for Fresenius SE and I would still see this calculation as a realistic. And we are still calculating with rather cautious assumptions – 3% growth and a free cash flow in line with numbers of the last few years.

Despite the company keeps struggling, I remain confident Fresenius can return on its path of growth, and we should not price the stock as if Fresenius was a declining business or headed for bankruptcy. And while Fresenius SE is not priced as if it is heading for bankruptcy, a P/E ratio of 8 is indicating a declining and clearly struggling business.

Conclusion

When looking at Fresenius we have a company which is struggling to grow the bottom line and saw even declining earnings per share in some years. And while the company was struggling in the last few years, we have a company that has performed well for decades but is struggling a bit in the last five years. However, we are also looking at a company that is still profitable in every single year and trading for an extremely low valuation multiple.

Fresenius is already undervalued if the company is only able to keep its revenue and earnings per share stable. And if Fresenius is able to return on the path of at least modest growth – as the company is expecting – and management being able to reduce debt, we are looking at a real bargain.

For further details see:

Fresenius: Still Struggling, Still Undervalued