FSNUF - Fresenius: The Company Is Climbing And I'm At 'Buy'

Summary

- I've been unfailingly bullish in the long-term on Fresenius - both the medical care, but also the main company headquartered in Germany.

- Fresenius has had an extremely tricky set of years, due to company challenges and what could be characterized as mismanagement (without being wrong).

- Still, the foundational case for Fresenius remains solid - and the company is now slowly climbing back up from trough levels.

Dear readers/followers,

It's not been that long since my latest update on Fresenius - however, the company has seen some pretty major movements in share price, which has seen my own position climb back into the green. While we're nowhere near a full recovery to historical levels yet, it might be time to see how attractive the company is beyond its lowest trough given the volatility of the stock.

That is why I'm updating my thesis for Fresenius ( FMS ) here, both ways of investing in the company, but the dialysis arm above the other in this particular piece.

Updating on Fresenius

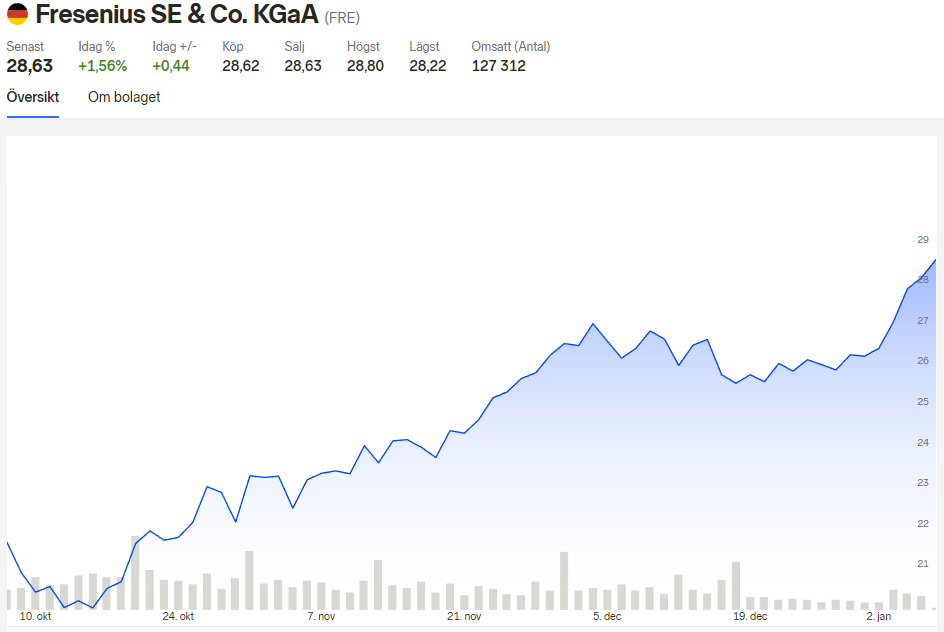

Fresenius has, for the native side of the share, seen a 31.6% climb in share price over a course of 3 months at this time.

{kind=link}

I didn't buy most of my position at the trough you see there - but I did load up, as I pointed out in my latest articles on the more general shares of the company, not just FMS, but all of Fresenius ( FSNUF ) ( FSNUY ).

Fresenius and its Medical Care arm have been a very interesting story to follow over 2 years' time. At times, there seemed the stock could find no bottom, and now it's one of my best performers relative to my own investments since October.

If you recall, the company is a large German healthcare company out of Bad Homburg in Hesse. The Medical care arm with FMS as a symbol is its own thing, but it's also a subsidiary of the main business, with a global presence in over 100 countries, €37.5B worth of sales in FY20, and over 300,000 employees across the world. In many of its areas, Fresenius holds a #1 market position, allowing the company a decent moat for its products and services. This includes the dialysis arm in its main geography, the USA.

Now, as most of my readers undoubtedly know, I have long been a proponent of investments in the main company as opposed to the dialysis arm. This is due to the advantage of diversification, as I view that you're missing out on some of the company's best segments if you only go for the dialysis business, FMS.

But I understand the logic, given the FMS ticker and the NYSE liquidity of said ticker, and you're certainly getting a good and undervalued business.

However, you are missing out on 3/4ths of this excellent "pie".

{kind=link}

You're also investing in the arm that's seen the most organic sales growth decline at a relative pace compared to any other of the segments, which explains some of the disconnects between the FMS valuation and the FRE valuation (native).

Still, Fresenius medical care is the global market leader in Dialysis. It has almost half the company's annual sales revenues, and most of that is attractive services, as opposed to products (like in the other fields. When Medical care works, it grows faster than the whole company, not slower.

The reason it's been underperforming has been headwinds that for months, and years since the pandemic began, have been hammering the company's trends and P&Ls.

But FMS manages 345,000 patients in 4,100 clinics across the world. 70% of that is NA, with the rest split something like this.

FMS IR (FMS IR)

From a global and NA-focused macro perspective for the company's services and products, there is nothing wrong here. The company and the overall market see a massive increase in the treatment area of dialysis because over 1,600,000 patients will need continual renal replacement therapy in 8 years. That's about 4-5x the company's current patients, and a massive market increase.

The company has also been heavily tilting towards home dialysis expansion, and 25% of all treatments are expected to be home-based by 2025. Digitization and modernization are driving the business. As with all changes, the current effects on the company due to this are chaotic - how could it be different?

Add to this the stress of the pandemic - again, it's not strange that we're seeing the troubles we're seeing if we exclude the company's mismanagement (because there are no good excuses for that).

Recent company trends in the quarterly report show the continued, challenging business environment. being service-oriented, the FMS segment is more impacted , not less by wage and labor cost inflation, and the pandemic has also delayed substantial improvement plans in American healthcare, the company's largest market.

The company revised its 2022 guidance. Revenue for 3Q22 still came in higher than YoY, with a 15% revenue growth, but operating income dropped by 7%, showcasing the company's failure to turn sales dollars into positive earnings. Net income was even heavier impacted, dropping 17% excluding special items.

FMS IR (FMS IR)

There are both significant tailwinds and headwinds for the company as things currently stand. The biggest headwind is inflation and SCM followed by excess mortality from COVID-19. These, and other headwinds, are as of yet completely unable to be weighed up by cost savings, PPE cost reductions, and growth - and it will be some time before this normalizes. The reason here is that the math is clear - FMS is one of the more heavily impacted by inflation and SCM, with COVID-19 still being " a thing", and where other companies (and segments of Fresenius) have managed to push sales revenue to where operating income trends are flat, the cost structures and contracts that govern their dialysis operations don't fall under services that have the ability to do this.

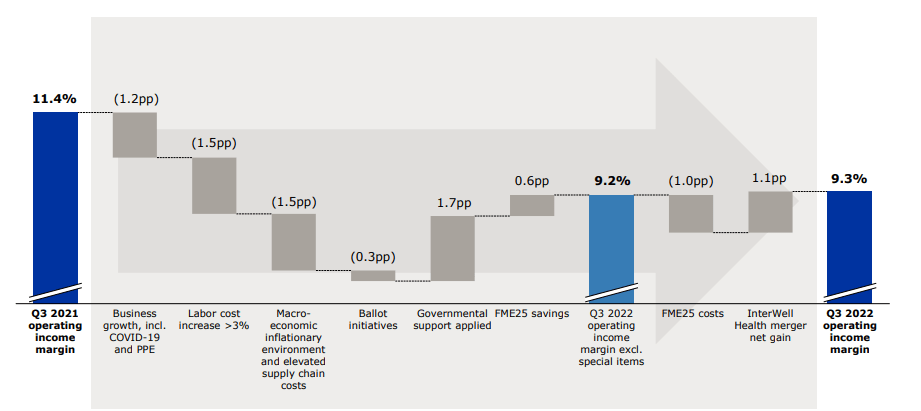

So the climb back up will be steeper - and it's worth mentioning that the company even had positive FX, but this is still where 3Q22 is. Here are some of the specifics from the company's operating income bridge.

{kind=link}

On the positive side, the company's debt is still within the corridor levels of 3.5x at most, and CapEx is actually down around €30M for the quarter. The company also doesn't really have any worrying sort of maturities in the near term, or before 2026. It's also still BBB rated by all agencies, indicating investment grade despite what's been happening.

On every level, FMS hasn't done the best job in any of this - preparing, fundamentals - but it's done well enough considering its circumstances. Remember, 90%+ of the things we're discussing are things that the company really can't do anything about or change in any way. It's macro, outside of FMS control.

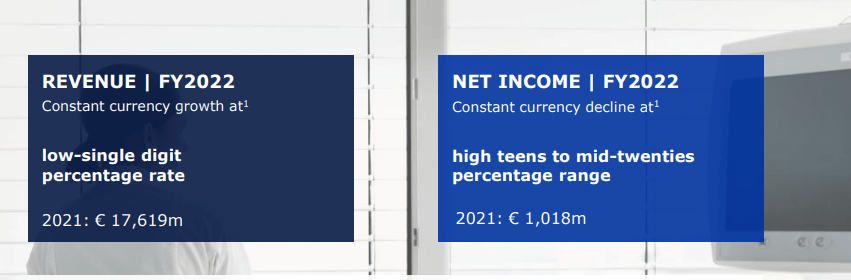

The company revised 2022E in the following way.

{kind=link}

Still positive, of course. The company isn't going negative in terms of net any time soon, but the environment remains pressured and it's not going away any time soon.

Because FMS lacks the buffer of organic growth and better P&L fundamentals from its other 3 operating segments, it's likely that Fresenius will return to normal faster than FMS. That is by the way also what we're seeing in the quarterlies.

Kabi has mostly stabilized its sales growth, Vamed is actually back to pre-pandemic organic sales growth, and Helios is above pre-pandemic levels. These are the reasons I own FSNUY instead of FRE (or rather, the common share).

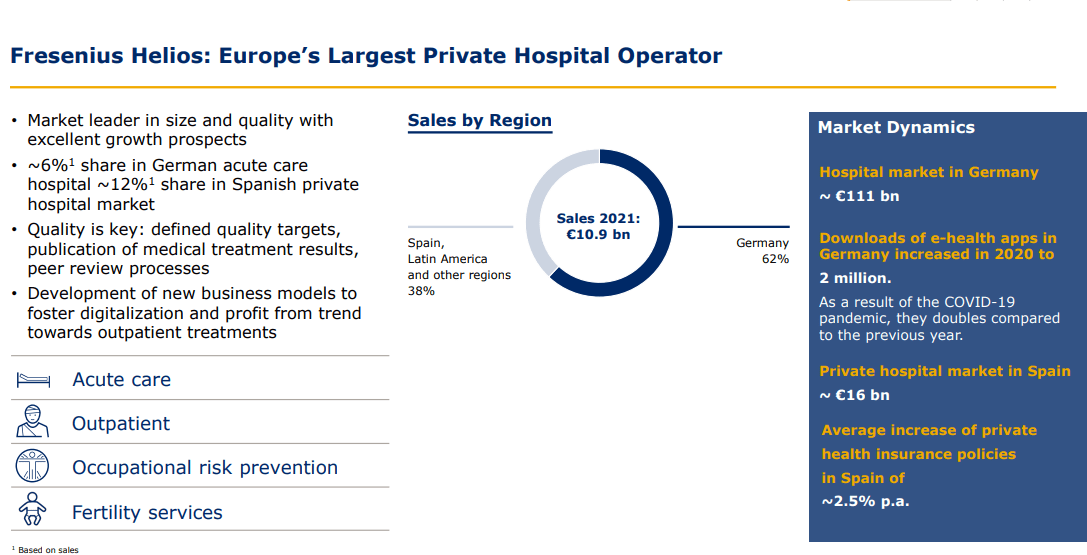

Take Helios for example.

{kind=link}

Germany and Europe is a huge Hospital markets - a hundred billion and above in Germany alone - and Fresenius owns parts of it. This is complemented by both hospital services and supplies, which are the other operations Fresenius has. Completely complementary and accreditive.

To me, owning FMS instead of Fresenius is like owning an energy company, but going strictly for the midstream business when there is a business that has distribution and upstream as well.

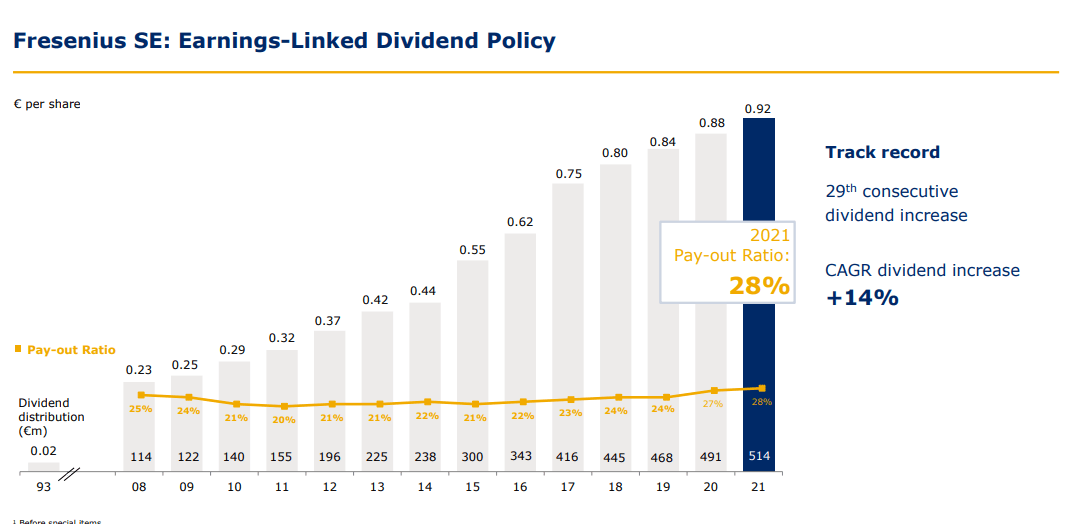

And remember, the company is a dividend grower - not a shower.

{kind=link}

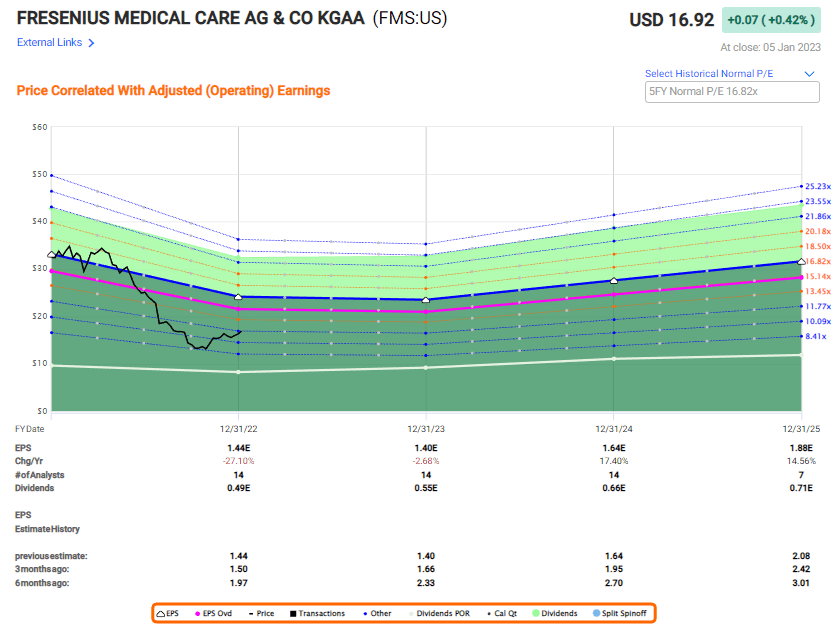

Let's look, as things stand, at the FMS valuation and where we could see ourselves investing here.

Fresenius Medical Care Valuation

FMS, like FSNUY, has recovered from the worst sort of its trough, and is back up to double-digit normalized P/E-ratios at this time. Remember, despite its FMS ticker, it's actually a 0.5x ADR of the native share, traded on the German stock market.

{kind=link}

Much in line with what I said, the company isn't expected to see the tide turning in 2023E either. I would agree with that. The combination of a recession, which I believe will be coming in both EU and the US, if a mild one, coupled with current other headwinds will see FMS's earnings flat at best - declining at worst. There will come a turnaround, but I'm not so sure 2024E is it.

Revenue and sales volume growth will do their part to stabilize the company. The volume growth expectations due to higher numbers of patients are real, and how these end up influencing profits, we'll see. But the company won't see, as I believe it, a full normalization before we see better profits return to the board here.

I believe that to be at least 1-2 years off when we'll see trends shifting.

The company is still undervalued - as it has been for a long time. Even assuming only 11-12x P/E your annualized rates of return for this company could be as high as 13%, and that's based on current estimates with a slow climb back. If we normalize at 15-16x, that RoR goes up to 25%, or nearly triple-digits until 2025E.

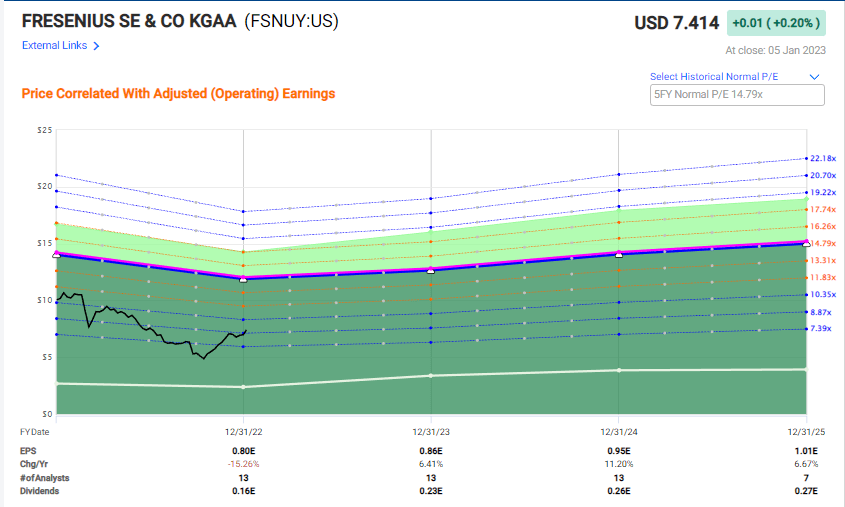

I believe that to be more likely for FSNUY than for FMS though. This isn't an article on the base company, but let me just show you the comparative charts so that you can see what I am talking about.

{kind=link}

Not only did the company trade at lower normalized P/Es, it drops aren't expected to be as deep, and recovery is expected in 2023E, which I consider likely due to the 4-segment mix. Full normalization to discount P/E of 14.8x, as opposed to 16.5x means a 30% annualized RoR here or 115% in less than 3 years.

Again, I view Fresenius as being better in every single way.

The company does have risks - and one of the more significant ones are the C-suite issues because management has really been making the wrong choices for the past couple of years. Combine this with a somewhat dubious (in terms of shareholder-friendliness, interest, and innovation) largest shareholder in the form of the Else Kröner-Fresenius foundation, and you do need to keep an eye on this business.

Regardless if you invested in FMS or FSNUY, the company still has a long way back to climb. This is a multi-year investment that I view likely to garner triple-digit returns, but again, one that's going to take time.

Street targets for FMS are as follows. S&P Global give the company a $20/share average target, implying an upside of 24% at current share prices. That's down from a $35/share average back in late -21. Again, analysts show their tendency towards exuberance here.

For the native FSNUY ticker FRE, we see similar trends. 16 analysts give the German company an average target of €36/share, down from nearly €50/share in -21, also a 27% upside to today's share price.

My previous PT for the native FRE ticker was €45. I'm sticking to that. My PT for FMS was around $30/share - and I'm sticking to that one as well, though noting clearly that these targets are for the long-term.

Here is how I view the current thesis for the common share/s.

Thesis for the common share

- Fresenius and Fresenius Medical Care are solid companies that both have fundamental upside and attractive operations. For FMS, I see a massive upside to a normalized valuation based on current repressed valuations owing to macro headwinds that the company has no control over. For Fresenius itself, the recovery is faster, but likely to be long as well. I give them respective PT's of $30/share and €45/share.

- I view the native FSNUY/FRE as the company to invest in for the sake of diversification.

- Both Fresenius and Fresenius Medical Care are "Buy" to me here, and I stand by my stance.

Remember, I'm all about: 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The companies both fulfill all of my investment criteria.

Thesis for Options

However, options for the company may be a more interesting play at this time. Take a look at the native EU options for FRE.

Fresenius Option (Author's Data)

That's 16.71% annualized waiting for Fresenius native ticker to drop 8% in 42 days, which in today's environment it might, but also probably won't (as I see it). Even if it did, that's a price I would "Buy" at.

So for the companies, I see this as the play to make. €2,600 isn't much in the way of capital exposure either.

For further details see:

Fresenius: The Company Is Climbing, And I'm At 'Buy'