FDP - Fresh Del Monte Produce Is Still Attractive Despite Its Pullback

2023-05-30 14:33:48 ET

Summary

- Fresh Del Monte Produce has experienced mixed financial performance, with some weakness on the topline but largely positive bottom line results year over year.

- Shares of the company are slightly cheap compared to similar firms and look appealing on an absolute basis.

- Despite recent downside, I believe there is potential for upside and rate the company a soft 'buy'.

In an ideal world, every investment that we make would be in a company that experiences consistent improvement on both its top and bottom lines. But this is not always the case. Sadly, some companies post mixed results or even worsening ones year after year. In instances where this becomes a trend, the downside for shareholders could be as much as all of the capital that they put in. But in cases where it is temporary, the pain could offer an attractive opportunity for investors to buy in on the cheap. That seems to be the case, in my opinion, when it comes to food producer Fresh Del Monte Produce ( FDP ).

The company has its hands in multiple types of operations. But for the most part, it focuses on the production of bananas, pineapples, and avocados. Recent financial performance has been mixed, with a bit of weakness on the top line, but bottom line results coming in largely positive year over year. Relative to similar firms, shares of the company tilt slightly toward the cheap end of the spectrum. But on an absolute basis, they definitely look appealing. So even though the company has seen a bit of downside in recent months, I would argue that some upside exists from here.

The market doesn't like this taste

I typically don't find myself drawn toward companies that are engaged in the production and sale of food. This is especially true when it comes to grown produce as opposed to branded items of a unique nature. This is because the commoditized nature of the products, combined with conditions outside of the company's control, can have a big impact on the operations of said firm. But every so often, I find myself a prospect that I think might offer some decent upside. One example of this that I can point to is Fresh Del Monte Produce.

Back in November of last year, I revisited my prior investment thesis on Fresh Del Monte Produce. Leading up to that point, shares of the company were outperforming the broader market. But although the 2022 fiscal year was looking to be rather mixed in nature, I felt as though the financial performance of the company was strong enough and that shares were cheap enough to justify a bit of upside. This caused me to reiterate my 'buy' rating on the company. But since then, things have not gone exactly as I would have hoped. While the S&P 500 is up a rather impressive 5.1%, shares of Fresh Del Monte Produce have pulled back by 2.6%.

{kind=link}

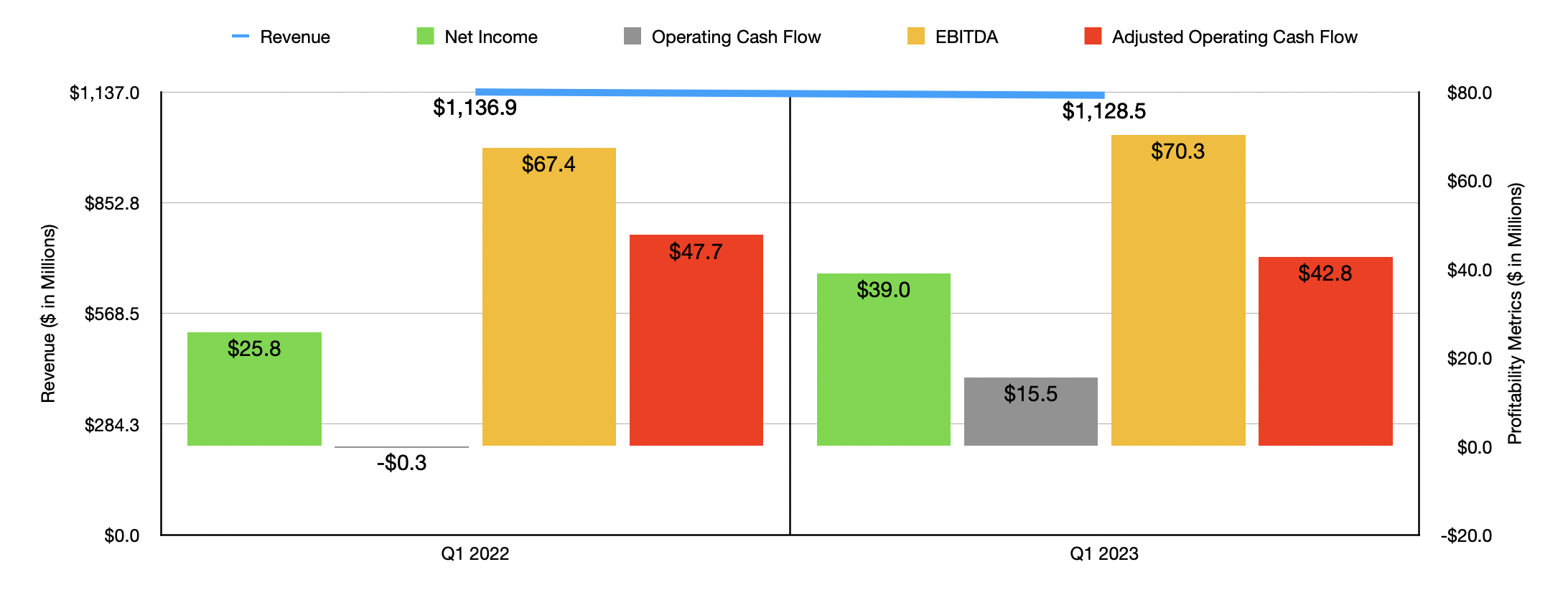

Some of this return disparity is very likely because of recent financial performance reported by management. Consider the first quarter of the 2023 fiscal year compared to the first quarter of 2022. Revenue during that time came in at $1.13 billion. That was down slightly from the $1.14 billion reported one year earlier. Interestingly, when you dig deeper, you can see that the sales figures for the firm varied meaningfully depending on what the individual source of revenue was that you might look at.

Consider revenue associated with banana sales. It actually rose nicely year over year, climbing 4.7% from $406 million to $425.1 million. This increase, management said, was largely driven by higher per unit selling prices in most of the regions in which it operates, as well as higher volumes shipped in both North America and Europe. On the other hand, revenue associated with the company's fresh and value-added products took a tumble, dropping 4.4% from $672.7 million to $643.4 million. This decline, according to the company, was largely thanks to lower per unit selling prices of avocados and a reduction in product volumes shipped because of a fall in fresh-cut vegetables, prepared foods, fresh-cut fruit, and other items. Interestingly, management said that the drop in volume was actually intentional, driven by the company's desire to try and improve its profitability.

Looking at the bottom line, we can say that profitability did, in fact, improve. Net income of $39 million dwarfed the $25.8 million reported one year earlier. However, it's important to note that a sizable chunk of this improvement was the result of a one-time event. You see, in the first quarter of 2022, the company generated a loss on the disposal of property, plant, and equipment. That loss was $3.8 million. But in the same time this year, that number came in positive to the tune of $27.5 million. The largest chunk of this gain was associated with the sale of two distribution centers and related assets that were unloaded for the joint venture that the company has in Saudi Arabia. The business brought in $66.1 million for its 60% stake in the firm. That allowed it to book a $20.5 million gain.

{kind=link}

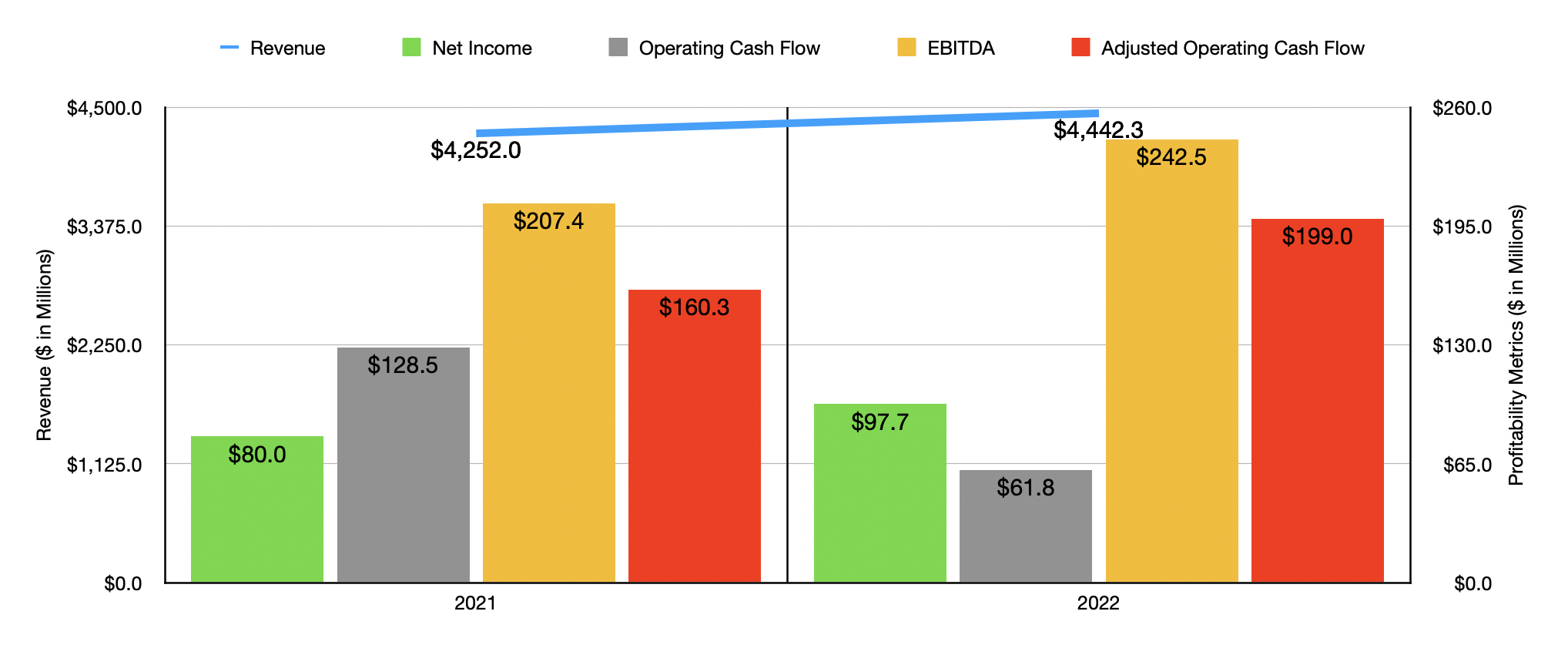

When it comes to other profitability metrics, the picture was not too much different. During that period, operating cash flow came in at $15.5 million. That compares to the $0.3 million loss generated one year earlier. On the other hand, when we dig a bit deeper, the picture doesn't look quite as positive. If we adjust for changes in working capital, we would actually have seen the metric dip from $47.7 million to $42.8 million. Meanwhile, however, EBITDA for the company expanded slightly from $67.4 million to $70.3 million. To be clear, this is not the first quarter in which the company has seen some mixed results. In the chart above, for instance, you can see financial results for 2022 relative to 2021. While it is true that almost every metric increased during this time, actual operating cash flow more than halved from $128.5 million to $61.8 million.

{kind=link}

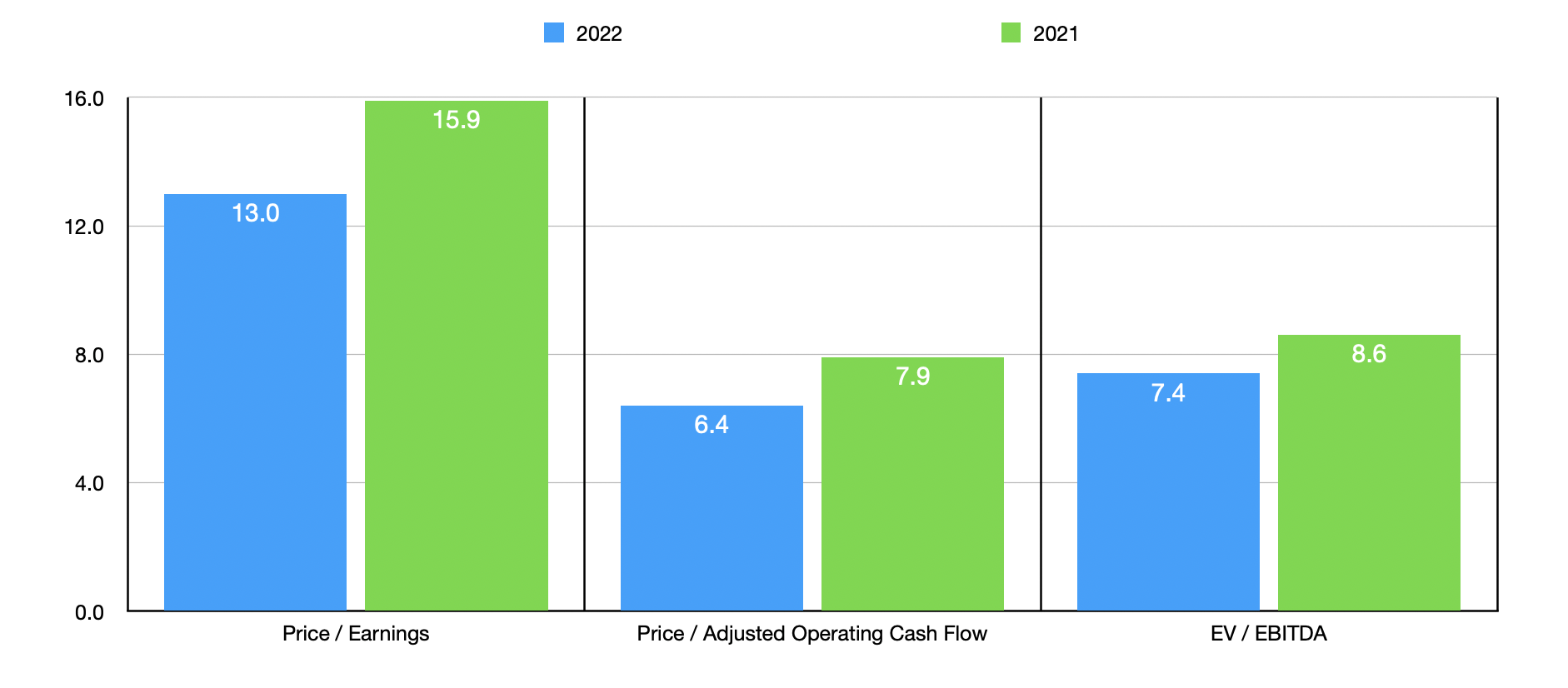

Management has not provided any guidance for the current fiscal year. But between how volatile this space can be, as well as the uncertainty associated with the broader economy and how early we are in the 2023 fiscal year, it might be best to focus instead on pricing the firm using data from 2022. This, combined with pricing using data from 2021, can be seen in the chart above. The price to earnings multiple for the company is 13. This on its own is not all that cheap. But if looking at it through the lens of the price to adjusted operating cash flow multiple, we end up with a reading of about 6.4. Meanwhile, the EV to EBITDA multiple for the company is 7.4. In the table below, you can see how shares are priced compared to similar firms. On a price to earnings basis, only two of the five companies were cheaper than Fresh Del Monte Produce while another was tied with it. Using the EV to EBITDA approach, we end up with two of the companies being cheaper than our prospect. Meanwhile, using the price to operating cash flow approach, all four of the companies that have positive multiples ended up being cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Fresh Del Monte Produce |

| 13.0 |

| 6.4 |

| 7.4 |

| Alico ( ALCO ) |

| 14.5 |

| 28.2 |

| 15.0 |

| Archer-Daniels-Midland ( ADM ) |

| 9.1 |

| 13.2 |

| 7.2 |

| Darling Ingredients ( DAR ) |

| 14.1 |

| 12.2 |

| 9.9 |

| Ingredion ( INGR ) |

| 13.0 |

| 47.0 |

| 9.0 |

| Bunge Limited ( BG ) |

| 9.3 |

| N/A |

| 6.0 |

Takeaway

From what I can see, the market is a bit frustrated by inconsistent financial results. While I can understand where market participants are coming from, I also believe that shares of the company look quite cheap on an absolute basis while looking slightly cheap compared to similar firms. I'm not going to say that Fresh Del Monte Produce is some fantastic prospect with tremendous upside. Because I don't think that's the case. But on the whole, I would say that some additional upside likely exists from here. Because of this, I have decided to keep the company rated a soft 'buy' for now.

For further details see:

Fresh Del Monte Produce Is Still Attractive Despite Its Pullback