FDP - Fresh Del Monte Produce: Moderately Attractive And Trading Cheap

2023-12-21 02:02:57 ET

Summary

- Fresh Del Monte Produce's revenue has grown at a CAGR of 2%, which is expected to continue, owing to the highly competitive, commoditized nature of the fresh produce industry.

- Although its margins have experienced volatility during the last decade, we suspect the company can normalize at an elevated level.

- Long-term success appears achievable, owing to its scale and strong brand. This should support a continuation of its 2-3% growth rate with population and economic growth.

- FDP is underperforming its peers but is trading at a ~53% discount to these companies. We believe this sufficiently accounts for its financial weakness.

- The company appears undervalued with a FCF yield of ~15%. This illustrates a reasonable opportunity although we struggle to see a significant long-term upside.

Investment thesis

Our current investment thesis is:

- FDP is a moderately attractive investment, even if we are hesitant to recommend foodservice businesses due to their mild growth. The company has a highly competitive value proposition, underpinned by its scale and brand.

- The key is that the stock is quite considerably undervalued, particularly against its historical average level. Its near-term results and relative performance leave some cause for concern, but this is compensated for in its valuation.

Company description

Fresh Del Monte Produce ( FDP ) is a global producer, marketer, and distributor of high-quality, fresh, and value-added food products. The company primarily focuses on fresh fruits, vegetables, and prepared foods. With operations spanning North America, Europe, Asia, and the Middle East, Fresh Del Monte is a prominent player in the global fresh produce industry.

Share price

FDP's share price performance has been poor, losing over 15% of its value during the last decade and broadly heading in a downward trajectory. This is a reflection of the difficulties operating within this industry and its valuation evolution.

Financial analysis

{kind=link}

Presented above are FDP's financial results.

Revenue & Commercial Factors

FDP's revenue has grown mildly during the last decade, with a CAGR of +2% into the LTM period. Growth has been consistently low, with only a single period of double-digit gains and 3 fiscal years of negative growth.

Business Model

FDP controls every step of the production process, from farming and processing to packaging and distribution. This vertical integration allows it to maintain quality standards and respond to changing levels of demand globally.

The company offers a wide range of products, including fresh fruits (pineapples, bananas, melons, etc.), vegetables, prepared foods, and beverages. Diversification helps mitigate risks associated with fluctuations in specific product markets and supply. The nature of these products limits FDP's scope for significant value enhancement, impacting profitability (EBITDA-M of ~6% and limited improvement) and growth (+2% CAGR). This said the business sells consumer food staples, allowing for consistent demand for goods in line with population growth and economic development.

FDP is branching out where possible, such as with its partnership with Kraft Heinz ( KHC ), but such actions do not move the needle compared to its core fresh produce offering.

Kraft partnership (FDP)

{kind=link}

FDP's key selling point is its well-known and trusted brand. Its ability to deliver fresh and high-quality products at scale has built strong brand recognition. Consumers know they are getting high-quality products and businesses can trust FDP to source flexibly. This has allowed the company to broadly maintain its upward growth trajectory despite scale.

The fresh food market, especially fruits and vegetables, is saturated. With many competitors offering similar products, which are "commoditized" in nature, differentiation becomes challenging, leading to price wars and reduced profit margins. This fundamentally makes the industry quite unattractive and is a primary reason why we have been critical of foodservice businesses in the past as investments.

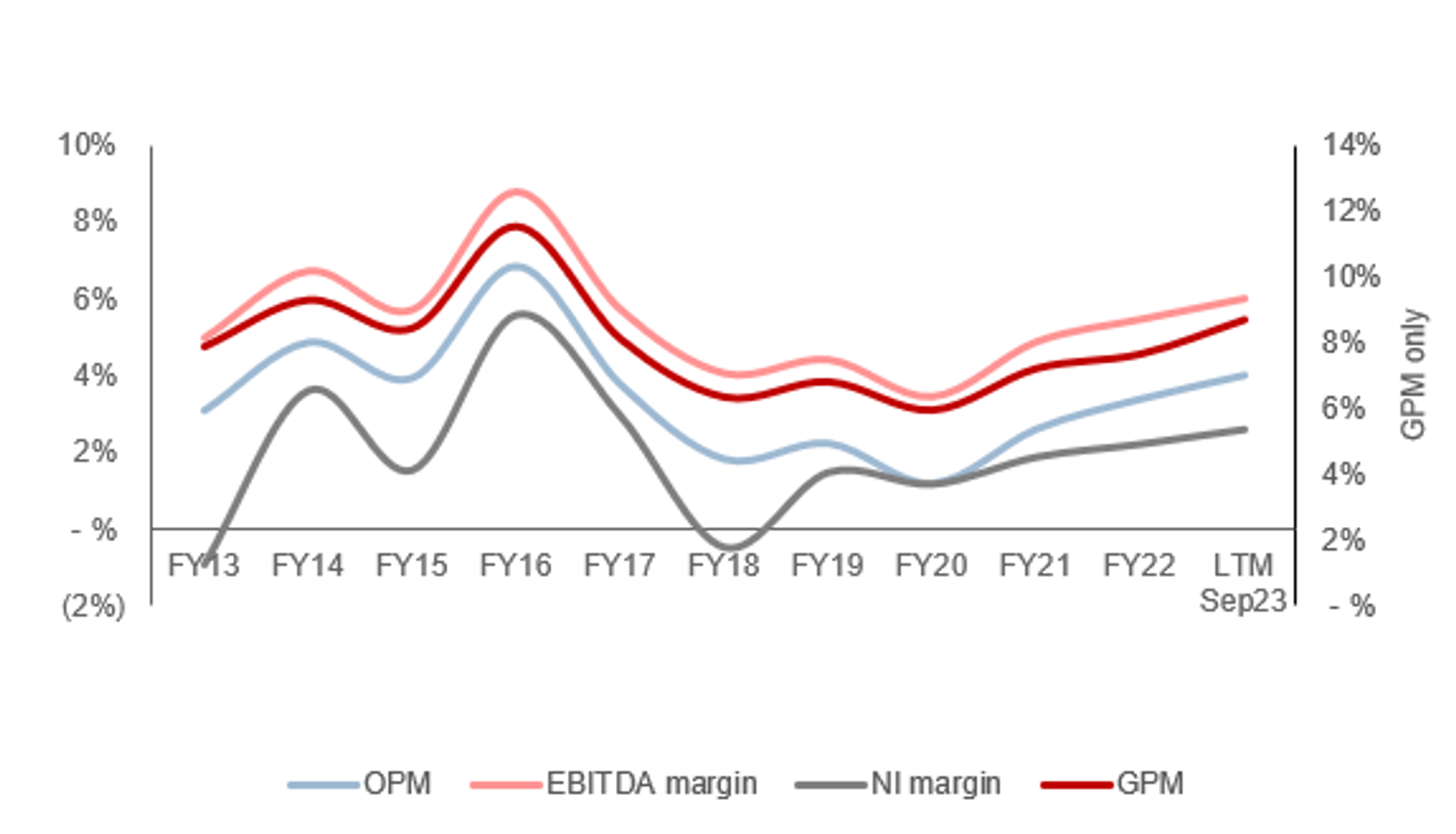

Margins

{kind=link}

FDP's margins have seen some volatility over the last decade, driven by industry development from globalization and increased competition (EBITDA-M peaked at 9% and had a low of 3%). Execution of operational improvements has been minimal, which is relatively disappointing given the technological developments we have seen in supply chains across a number of industries. It is likely much of this is offset by competition.

The company has seen an upward trajectory in recent years through pricing power, which we suspect will begin to subside ( discussed further next ). This said, we do believe the business can normalize at its existing level, which is slightly ahead of its historical average.

Quarterly results

FDP's recent performance has materially slowed relative to its 3Y level, with top-line revenue growth of +2.2%, (0.7)%, (2.6)%, and (4.8)% in its last four quarters (Source: Capital IQ) . In conjunction with this, margins have slightly stepped up, although appear to be normalizing.

The company's declining growth is a reflection of the wider macroeconomic environment. With elevated inflation and interest rates, businesses have initiated consistent price increases to offset supply chain issues, allowing for an accelerated top-line trajectory. This is unsustainable, however. With consumers significantly squeezed from a cost-of-living perspective, demand is beginning to waver. This has initially impacted discretionary industries but is not spreading to areas of inelastic demand, with volume beginning to wholly offset price gains.

Looking ahead, we believe there is more pain coming. Inflation is remaining stubborn and so a return to expansionary policy continues to be pushed back. It was always going to be extremely difficult to balance economic growth and disinflation. Offsetting benefits will come from easing inflationary pressures allowing for near-term margin improvements.

Key takeaways from its most recent quarter (Q3) are:

- The net sales decline was primarily driven by the fresh and value-added products segment, namely lower unit pricing on avocados due to market conditions and lower sales volume of non-tropical fruit. This reflects a cooling in the industry.

- This was partially offset by higher net sales in its banana segment, driven by both per-unit pricing and volume.

- The company has benefited from lower product and distribution costs in the fresh and value-added products segment, owing to easing inflationary pressures.

Balance sheet & Cash Flows

FDP is conservatively financed, with a ND/EBITDA ratio of 1.6x. Interest only comprises 1% of revenue yet Management seems committed to deleveraging. This careful approach has meant underwhelming distributions, with limited dividend growth and sporadic buybacks. We would like to see cash flows redirected to distributions, with a commitment to grow dividends.

FCF generation has been historically limited, although limited by its profitability profile in conjunction with its Capex requirements. Management has significantly reduced Capex spending in recent quarters, potentially due to softening demand and the desire to protect FCF. The concern here is that FDP is underinvesting its capabilities.

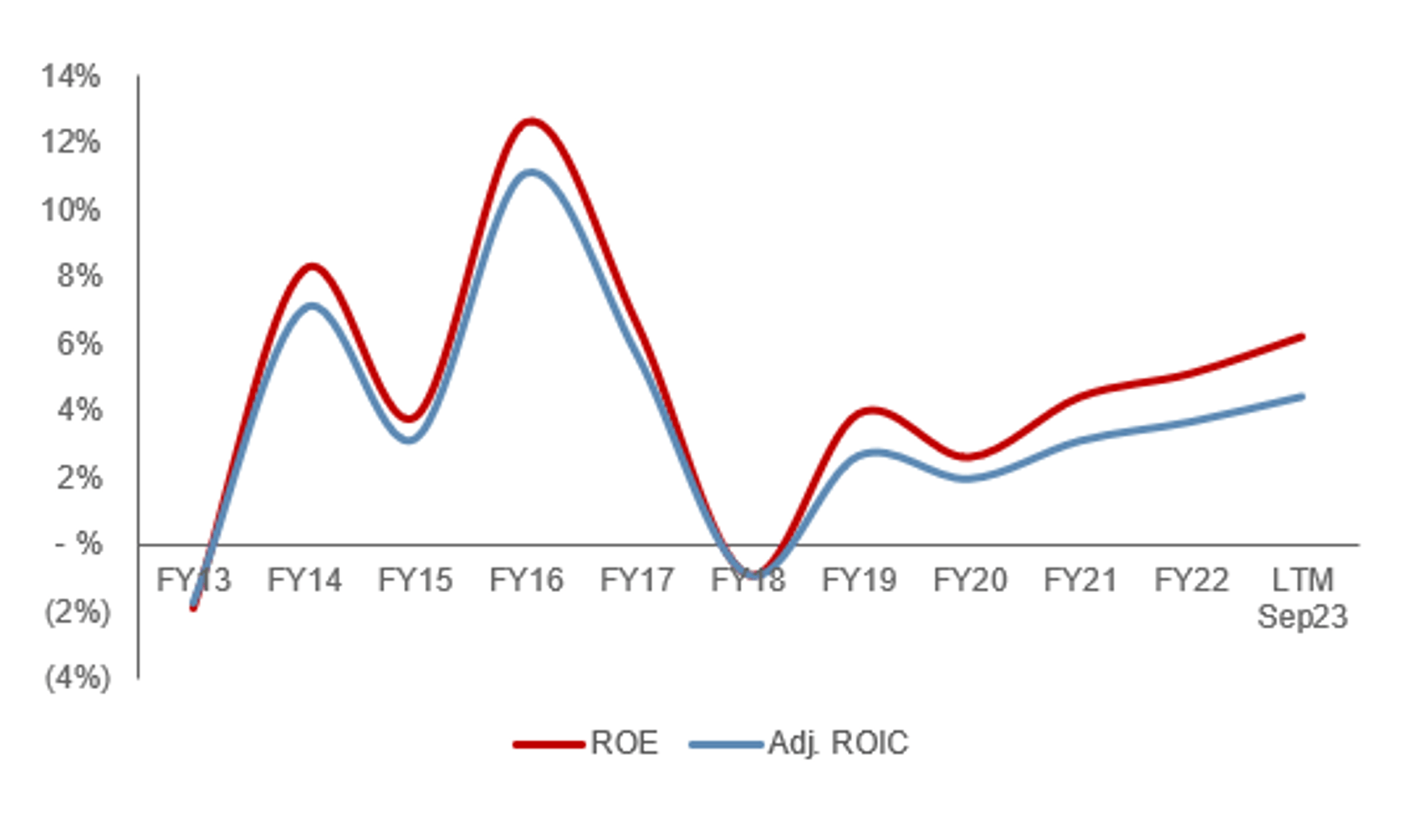

FDP's ROE has been broadly mild, generally fluctuating between 3-8%. This is a reflection of the industry and its commoditized nature, limiting the scope for generating substantial returns. Excluding FY13 and FY18 (due to large below-EBITDA non-recurring accounting charges), FDP's average is ~6%.

{kind=link}

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its mild growth, with a CAGR of +2% into FY24F. In conjunction with this, margins are expected to broadly flatline at the current level.

These assumptions appear reasonable in our view. We suspect FDP has limited scope to outperform on growth given the industry, as it is highly mature and commoditized in nature. The key question for us is whether FDP can sufficiently protect its position and incrementally improve with small gains, which appears to be the case. Offsetting demand will soften the scope for margin improvement.

Industry analysis

{kind=link}

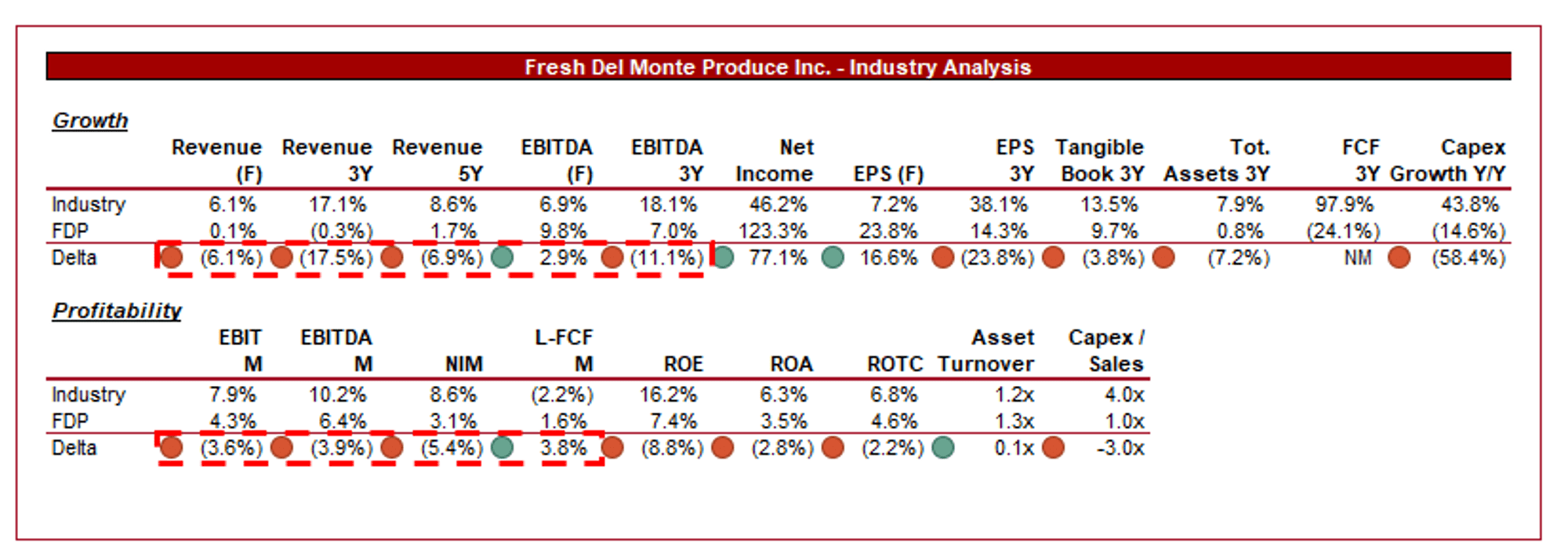

Presented above is a comparison of FDP's growth and profitability to the average of its industry, as defined by Seeking Alpha (6 companies).

FDP's performance is disappointing relative to its peers, much of which is directly attributable to the specific segment it serves. Its commoditized nature and limited scope for value-add beyond scale and distribution capabilities have limited its ability to improve margins.

Further, its lower profitability limits FDP's ability to conduct inorganic growth through acquisitions, another key factor that makes its overall growth potential limited.

Valuation

{kind=link}

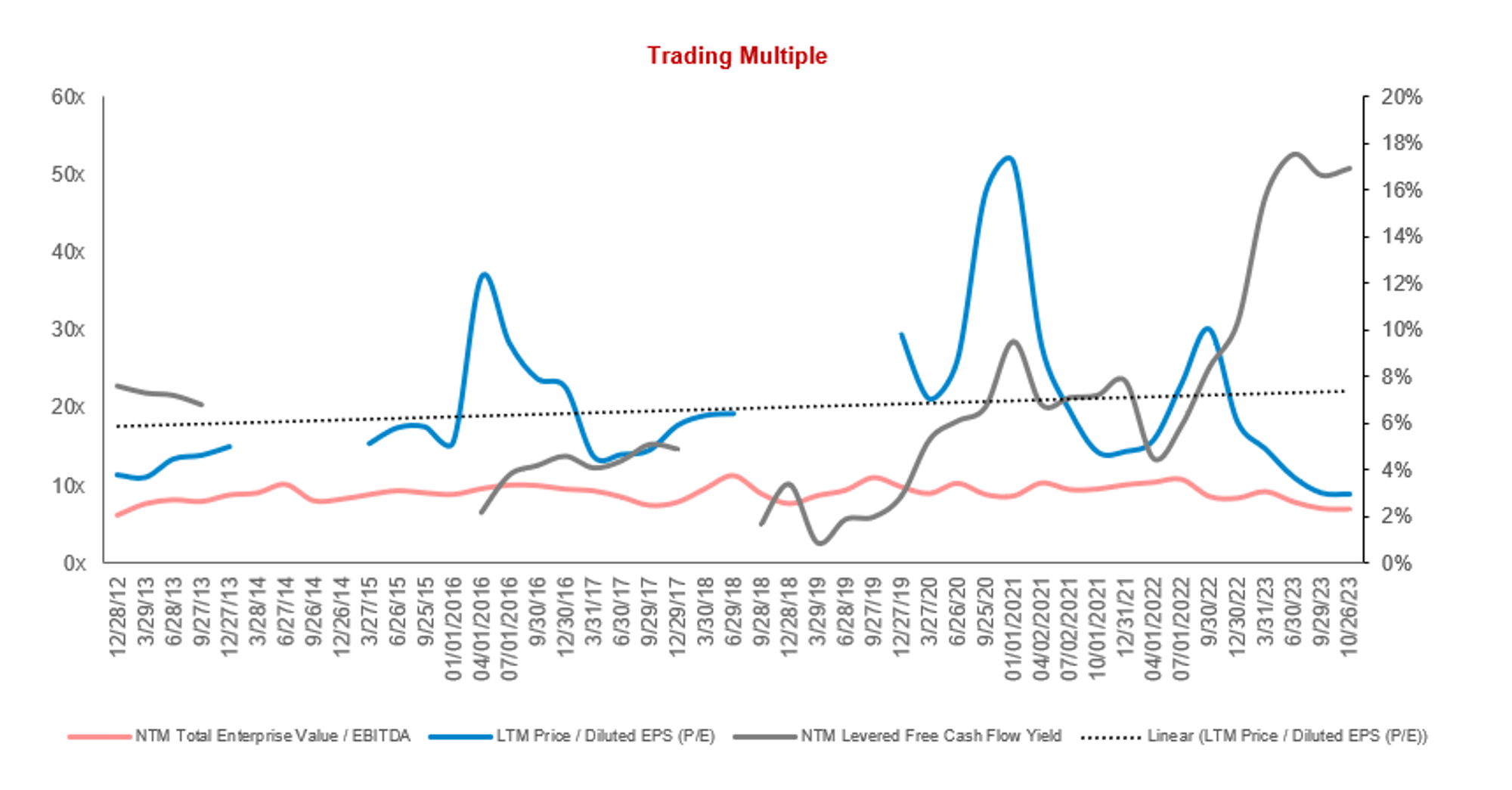

FDP is currently trading at 7x LTM EBITDA and 7x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, although not to a substantial extent. The company has seen margin erosion and faces near-term risks due to market uncertainty. This said, as a food business, inelasticity will work in its favor and limit its downside risk. At a 30-47% discount on an LTM EV/EBITDA basis, we consider the stock undervalued ( Valuation sources: Capital IQ ).

Further, FDP is trading at a 53% discount to its peers on an LTM EV/EBITDA basis. A discount again appears reasonable, owing to its lower growth and profitability. The size of the discount appears slightly larger than we would suggest (~35%), which again implies upside.

Based on this, FDP is undervalued. Our target upside at this valuation is ~18%, reflecting its relative valuation to its peers and a conservative discount of 35%.

Seeking Alpha's Quant concurs with this, rating the stock a "STRONG BUY". Its financial profile in conjunction with its valuation is fairly compelling. This is illustrated in its NTM FCF yield, which is ~16%.

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- [UPSIDE] Expansion into emerging markets.

- [UPSIDE] Product diversification to improve scale.

- [DOWNSIDE] Market saturation contributes to further competition and pricing pressure.

- [DOWNSIDE] Climate-related disruptions. by.

- [DOWNSIDE] Supply chain challenges with yield.

Final thoughts

FDP is a solid business. The company is positioned to grow at its mild rate in the long term, driven by economic development and population growth. beyond this level, we struggle to see any scope for outperformance. The business does not generate enough cash to revolutionize itself, and so is ring-fenced within its current sphere.

We are highly critical of foodservice businesses for this reason, they provide limited scope to outperforming the market. This said, FDP is in a unique position. The company appears incredibly cheap and is trading at an impressive FCF yield.

For more risk-conscious investors looking to exploit the dip in valuations, FDP could be an attractive choice.

For further details see:

Fresh Del Monte Produce: Moderately Attractive And Trading Cheap