FNLPF - Fresnillo: Expect Moderate Growth In 2024

2023-09-06 04:46:32 ET

Summary

- Fresnillo plc has underperformed its benchmark ETF, Global X Silver Miners ETF, in terms of price performance over the past year.

- Despite the H1 2023 results deteriorating on a YoY basis, FNLPF is well-positioned to achieve suitable long-term share price growth without compromising its dividends.

- The Juanicipio mine is firing on all cylinders and will be an important growth catalyst.

- With the gold/silver ratio on the rise, FNLPF's strategy to expand its gold footprint might bear fruit.

Thesis

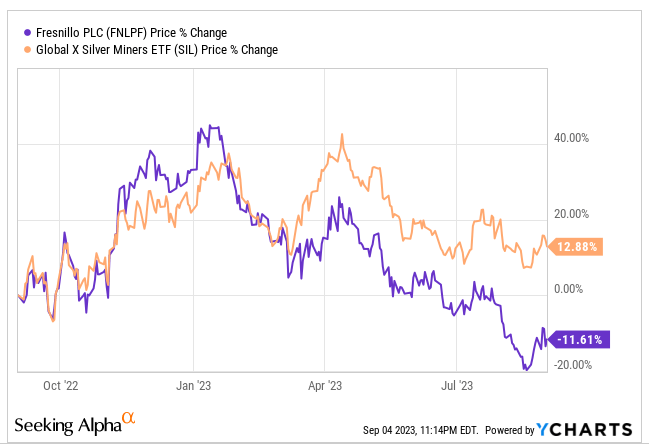

Fresnillo plc ( OTCPK:FNLPF ) is a mining giant exploring, developing, and operating PM (precious metals) mining assets in Mexico. FNLPF is among the top 10 Global X Silver Miners ETF ( SIL ) holdings, constituting 3.68% of SIL's portfolio. However, the stock has lagged behind its benchmark ETF regarding price performance during the past 12 months. FNLPF has declined by ~12%, whereas SIL has recorded gains of ~13% over the same period (spread of ~25%).

{kind=link}

Fresnillo Plc.-1 Year price change v/s Benchmark ETF - Source: YCharts

In my view, the following catalysts are responsible for FNLPF's lackluster price performance compared with SIL:

- The impact of an unimpressive H1 2023 (on a YoY basis), particularly in cost performance.

- Price adjustment due to regular dividend payouts in April and August each year.

- A balanced portfolio comprising large-scale 'producing' mines and promising 'future' projects. Generally, miners whose portfolios contain only future mining projects are more reactive to metal price changes than those operating a mixed portfolio of producing assets and future projects.

This article analyzes FNLPF's H1 2023 results, which deteriorated (on a YoY basis) despite a notable improvement in revenues and metal prices. We also consider the growth catalysts that can support share price growth in the medium-to-long term.

As we will discuss in our analysis, FNLPF's increased production volume for gold/silver supported by near-to-medium-term pipeline projects, portfolio optimization initiatives with a focus on cost performance, strong balance sheet highlighting robust liquidity, and an attractive dividend policy all add to the company's appeal as a promising 'long' investment. We also highlight the challenges impacting an investment case in the company. Let's get into the details .

H1 2023 Review - Results and Expectations

Let's start with the headline numbers. Look at the table below.

{kind=link}

Fresnillo's H1 2023 Headline Numbers - Source: Author

During H1 2023, FNLPF improved its gold (up 5.4%) and silver production (up 1.4%) on a YoY basis, and this favorable volume variance was augmented by an improvement in both gold (up 4.1%) and silver prices (up 2.4%). Notably, the gold segment outperformed silver in terms of both production volume and price growth. This enabled FNLPF to deliver a marginal ~6% improvement in YoY revenues.

In contrast, FNLPF's cost profile reveals a more significant problem: rising costs that offset the impact of a YoY improvement in PM prices and production volumes. This single aspect has reflected heavily on FNLPF's overall financial performance during H1 and impacted the operating cash flows, EBITDA (and margins), earnings, and dividends. I believe the following catalysts were mainly responsible for FNLPF's substandard cost performance during H1, 2023, on a YoY basis:

1) Rising MXN/USD will continue to haunt cost performance

A significant catalyst behind rising costs during H1, 2023, was the revaluation of the Mexican Peso against the US Dollar. This is because a strengthening Peso directly impacts the labor, materials, supplies, etc., and other direct costs paid for in the Peso and accounted for in the dollar. The following chart shows that the MXN (Mexican Peso) has gained approximately 20% against the USD during the past two years.

{kind=link}

2-Years' MXN v/s USD - Source: XE

Notably, the USD has weakened despite multiple rate hikes by the Fed during the past two years to combat inflation, pushing the funds rate from near 0% to 5.5%.

{kind=link}

Fed funds hike history (2022-23) - Source: Forbes

Comments: Generally, the Fed's decision to hike the funds' rate is based on low unemployment rates that demonstrate demand growth and result in inflation. However, recent data shows that the economy is cooling, raising hopes of a pause in the Fed's current hawkish trend in the funds rate. This implies that the Peso will continue to increase against the USD (probably at a greater pace), especially since it maintained its rally (in the last two years) despite persistent rate hikes by the Fed.

Imagine a scenario when the Fed drops the rate in the future (note that I expect a pause in the successive rate hikes in the upcoming meeting of the FOMC in September 2023). The dollar theoretically becomes less attractive due to a decline in demand. In that case, the Peso will likely accelerate its flight against the dollar.

Either way (rate hike paused or rate reduced), the costs incurred in Mexico (as reported in the USD) will increase. The Fed's next rate decision will decide the magnitude of the potential impact on the MXN/USD. Given that all the producing mines of FNLPF are situated in Mexico, I believe the 'One Country' approach will amplify the impact of a cost increase emanating from the Peso's revaluation. For reference, the revaluation of Peso led to a YoY increase of $45 MM in 'adjusted production costs' during H1 2023.

2) Cost Inflation - Expect Improvement

The impact of cost inflation (excluding currency revaluation) led to a YoY cost increase of $41.6 MM during H1, 2023. Recently, the inflation in Mexico has been easing for good, thanks to a high interest rate implemented by the Mexican Central Bank (Banxico). For FNLPF, I expect cost inflation to reduce (mainly the cost inflation for local inputs paid for in the Mexican Peso).

3) Expenses relating to the start-up of the Juanicipio beneficiation plant and mine ramp-up

FNLPF's 56% directly (and ~60% indirectly) owned Juanicipio mine is nearing the completion of its processing plant, has reached ~85% of its nameplate capacity of ~4,000 tpd, and FNLPF expects to reach full nameplate capacity by the end of Q3 2023. The impact of such start-up/ramp-up expenses during H1 2023 was ~$19.6 MM. I expect these expenses to reduce during H2 2023 since only a tiny portion of the nameplate capacity expansion remains to be achieved on the Juanicipio processing plant (less than 15%).

Besides the above, the following catalysts also impacted FNLPF's cost performance during H1, 2023, on a YoY basis:

- Recognition of Herradura's higher stripping costs as an expense rather than capitalization

- Increased maintenance, contractors, materials, and diesel consumption due to longer haulage distances, deeper mines, and advanced development work

- Higher ore processing volumes

Portfolio Review

Let's analyze FNLPF's mine-wise performance during H1 2023 from different aspects.

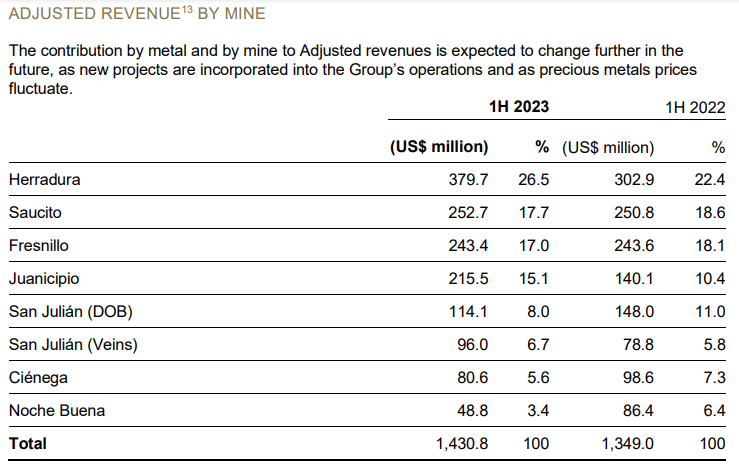

1. Contribution to Group Revenues: The following table highlights mine-wise contribution to FNLPF's H1 2023 revenues.

{kind=link}

Mine-wise Revenue Contribution - Source: Interim Report 1H23

Here are my notings from the tabulated information above:

- The Herradura and Juanicipio mines saw a remarkable YoY improvement in revenues and proportionate revenue share.

- The Saucito and Fresnillo mines' revenue contribution remained unchanged from last year.

- San Julian (DOB - Disseminated Ore Body) and San Julian (Veins) saw a moderate decline in YoY revenues and proportionate revenue share.

- Both Cienaga and Nochebuena mines saw a significant drop in YoY revenues and proportionate revenue shares.

2. Mine-wise metal sales volume: On a group level, H1 gold revenues accounted for 43.7%, up from 41.2% from the SPLY(read: Same Period Last Year). Silver revenues accounted for 44.2%, up from 42.8% from the SPLY. On the flip side, revenues attributable to zinc sales declined sharply from 12% to ~8% due to falling YoY zinc prices. Given the significance of gold and silver metal sales to FNLPF's total revenues, let's look at the mine-wise sales volume in the table below.

Mine-wise Gold/Silver Sales Volume - Source: Interim Report 1H23

Here are my notings from the tabulated information above:

- Both gold and silver saw a YoY increase in production volumes, with Herradura leading in gold production and Juanicipio leading in silver production.

- Herradura and Juanicipio production recorded a 5%+ YoY increase in favorable volume variance.

- Fresnillo mine's silver production remained flat YoY but declined in proportionate silver volumes (down from 25.4% to 22.3%).

- Silver production from Saucito declined YoY, as did the proportionate silver production volume. However, Saucito's gold output and proportional gold production volume saw a remarkable YoY improvement.

- San Julian (Veins) saw a healthy increase in silver/gold production and a marginal overall increase in proportionate production volumes. San Julian (Disseminated Ore Body) witnessed a drop in production.

- The Pyrites Plant at Saucito looks promising regarding YoY silver and gold production growth.

- Cienaga and Noche Buena both witnessed a drop in YoY gold/silver production.

3. Cost Profile: Now, let's look at the table below, which shows the mine-wise AISC (All-In-Sustaining-Costs) for payable gold and silver ounces produced (during H1 2023) and my notings that follow:

Mine-wise AISC - Source: Interim Report 1H23

- Except for Herradura, all mines reported higher AISC on a YoY basis.

- Cienaga's AISC of ~$3,073/oz was way ahead of average realized gold prices of ~$1,950/oz, implying that Cienaga's production resulted in a cash burn of ~$1,123/oz. However, due to a lack of availability of information, we cannot say whether stopping Cienaga production and putting the mine on 'care and maintenance' status would have been a better option.

- Noche Buena's AISC went significantly up by ~36% YoY, primarily due to the mine coming to the end of its life.

- Fresnillo and Saucito witnessed a 3-4% YoY increase in AISC/silver oz, implying a significant reduction in operating margins.

- AISC information for the Juanicipio mine is unavailable, possibly due to the mine being in the ramp-up phase. However, I'd note that despite processing low-grade stockpiles during Q2 2023, Juanicipio's H1 silver grades far exceeded those of any other mine. This implies that Juanicipio's AISC per silver ounce may be better than FNLPF's other silver mines. For reference, note that H1 silver grades were 448 g/t for Juanicipio , compared with 177 g/t for the Fresnillo mine, 197 g/t for Saucito, 192 g/t for the Pyrites Plant at Saucito, 144 g/t for Cienaga, 152 g/t for San Julian (Veins), 156 g/t for San Julian DOB, besides negligible silver ore grades for both Herradura and Noche Buena.

Section Conclusion - Where's the beef?

From the above discussion, it becomes clear that Juanicipio is the most promising asset in FNLPF's portfolio. FNLPF owns ~60% of the Juanicipio mine (56% directly and ~4% indirectly through MAG Silver). The Juanicipio mine significantly outperformed the other mines on multiple metrics, including silver grades, production volumes, YoY growth in proportionate revenues, etc. Besides, I believe that Juanicipio has promising near-term growth prospects. On that note, FNLPF expects the Juanicipio processing plant to achieve the nameplate capacity of ~4,000 tpd in Q3 2023. The plant operates at 85% of its nameplate capacity (as last reported).

In the future, I anticipate increased ore processing volumes at the Juanicipio mine, improvement in ore grades (H1 2023 grades declined YoY due to processing low-grade stockpiles at Juanicipio), and low-cost operations since Juanicipio's ore will be processed at the mine processing plant rather than being shipped to the processing plants of Fresnillo and Saucito mines. This will reflect positively on Juanicipio's cost performance in the future.

Interestingly, the Juanicipio business segment had the best profit margins (at 56.2%) compared with other mines (41% for Fresnillo, 21.68% for Herradura, 6.7% for Cienaga, 29.87% for Saucito, 10.42% for Noche Buena, and 44.24% for San Julian). The table below highlights the segment-wise revenues and profits for FNLPF's mining segments during H1 2023.

{kind=link}

Segment-wise Revenues and Profits - Source: Interim Results 1H23

4) Other initiatives for portfolio optimization: FNLPF's following planned measures target cost reduction at other key mines (Fresnillo, Herradura, and Saucito):

- Besides implementing remote/autonomous drilling methods at the Fresnillo mine, FNLPF is deepening the San Carlos shaft to reduce haulage costs.

- Optimization of slopes at the Herradura mine to lower stripping and haulage costs.

- Weight tracking of haulage truck fleets at Saucito to ensure optimal load and consequently improve the mine's cost profile.

Notably, the H1 capital expenditure of ~$228 MM witnessed a YoY decline of 23.8%. It mainly comprised mine development (at Saucito, Fresnillo, and Juanicipio mines), acquisition of in-mine equipment to contribute to the normalization of the mining cycle, increasing the depth of Jarillas shaft, leach pad construction at Herradura, and investment in tailings dam (at Saucito, Fresnillo, and San Julian Veins/DOB).

Pipeline projects - Extending the gold footprint

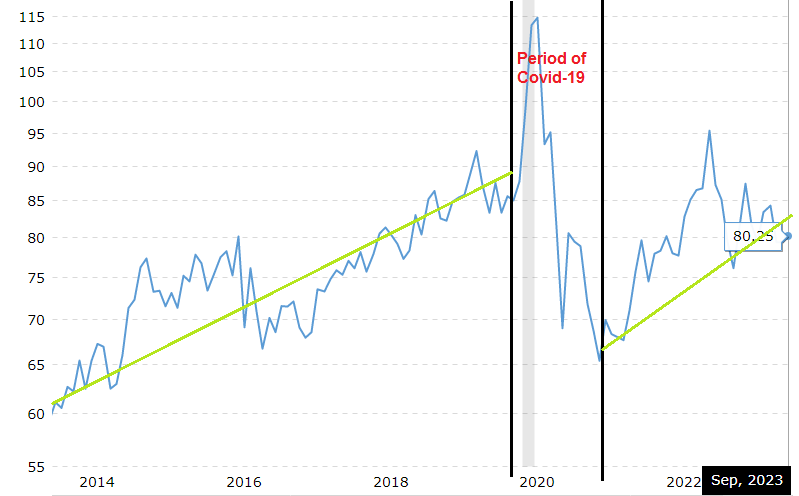

In a previous section, we saw that Herradura led in gold production (followed by Saucito and Noche Buena). Noche Buena has met the end of its mine life, and mine closure activities commenced in May 2023. Note that gold accounted for ~44% of H1 revenues. Interestingly, the gold/silver ratio has been on an uptrend during the last five decades, which means that one ounce of gold is increasingly becoming more valuable than one ounce of silver. The following chart highlights an overall increasing gold/silver ratio during the past ten years, except for the post-COVID period of economic restoration, which saw a massive (albeit temporary) drop in gold prices. Presently, the gold/silver ratio is at 80+ points. If we take any lessons from history, I believe it would be safe to assume that this ratio will vary within the range of 80-100 points in the long run, regardless of silver's role in the green economy.

{kind=link}

10-Year Gold/Silver Ratio - Source: Macrotrends

For FNLPF, it indicates substituting a more significant proportion of its future revenues from silver to gold. With Noche Bueno's operations discontinued, FNLPF's near-term hopes are pinned on the gold production growth from Herradura, Saucito, San Julian Veins, and Juanicipio.

What I like the most is the presence of the following promising pipeline projects (mostly gold-based) in FNLPF's portfolio that could significantly add to the company's gold production in the future.

- Orisyvo - a high-sulfidation gold deposit in Mexico with an expected resource of 9.6 million ounces of gold and 13 million ounces of silver. This project is in the advanced PFS (pre-feasibility study) stage.

- Rodeo - an open-pit, heap leach gold deposit in Mexico with an expected resource of 1.3 million ounces of gold and 14 million ounces of silver. This project is in the advanced PEA (preliminary economic assessment) stage. The chart below highlights that the Rodeo and Orisyvo projects will likely begin commercial production within the next five years (assuming things run smoothly on the exploration and permitting fronts).

- Tajitos - an open-pit, heap leach gold deposit in Mexico with an expected resource of 1.1 million ounces of gold. FNLPF expects to issue a new PEA in 2024.

- Guanajuato - an epithermal gold/silver deposit in Mexico with an expected resource of 2.2 million ounces of gold and 152 million ounces of silver. This is also a PEA stage project with an updated resource estimate expected to be released by the end of FY 2023.

- Juanicipio - The Juanicipio mine, which appears to be firing on all cylinders, has a combined (Indicated and Inferred) resource of 267 million ounces of silver, 1.429 million ounces of gold, 1.256 billion pounds of lead, 2.293 billion pounds of zinc, and 109 million pounds of copper (on a 100% basis). The fact that this resource estimate is based on the exploration results of only 5% of the property indicates significant exploration potential at the Juanicipio mine, which may lead to considerable resource growth in the future.

{kind=link}

Orisyvo / Rodeo Development Timeline - Source: H1 Presentation

It's pertinent to mention that FNLPF has front-loaded the 2023 exploration spend during H1. For reference, note that out of the total planned exploration expenditure of $175 MM, the company has already spent ~$97 MM (or 55%) during H1. Given the revaluation of the Peso against the USD and the fact that FNLPF has to issue PEA/PFS on some of these exploration projects (in the near term), I consider it a wise move.

Balance Sheet

As of June 30, 2023, the company's balance sheet totaled $5.9 BB, including 'cash and investments' worth ~$890 MM. Cash and investments declined 8.2% during the past six months (December 31, 2022=$969 MM). Compared with outstanding Senior Notes to the tune of ~$1,159 MM, FNLPF's net debt amounted to ~$269 MM at the end of H1, up from $198.7 on December 31, 2022. Note that ~$317.9 million Senior Notes are due in 2023, with the remaining $850 MM due in 2050.

The current cash position is sufficient to cover that part of the LTD, which is maturing within the next 12 months. Hence, I'm not worried about the company's liquidity profile. Moreover, due to the ramp-up of Juanicipio's processing plant to full capacity, together with an overall improvement in PM prices during H2 (check the charts below), I anticipate the net debt position to improve going forward. Besides, a strong liquidity position will enable FNLPF to continue its healthy dividend payouts in the future, in line with its policy to distribute 33-50% of after-tax profits to the shareholders.

Gold & Silver Technical Price Chart - Source: Finviz

The inventories declined from $587.4 MM on December 31, 2022, to $543.6 MM on June 30, 2023 (or 7.4%). The decline is explained by the consumption of low-grade stockpiles that were processed at the Juanicipio beneficiation plant and the inventories consumed at the Noche Buena mine that approached the end of its mine life. I view this positively since the low-grade stockpiles previously processed at Juanicipio will be replaced by relatively better-grade concentrates as Juanicipio production ramps up.

Investor Takeaway

In the preceding discussion, we have analyzed an investment case in FNLPF from multiple angles. The company maintains a strong balance sheet with a 'Net Debt to EBITDA' position of 0.42x (based on TTM results). The company's cash position adequately covers the debt maturing within the next 12 months, indicating a robust liquidity profile and the ability to continue dividend payouts in the future, in line with company policy. Meanwhile, generally improving PM prices during H2 (compared with H1 2023) indicates the possibility of improving cash inflows, HoH.

On the flip side, a detailed look at the company's financial and operational profiles reveals that despite increased production volumes and improved gold/silver prices during H1 (on a YoY basis), the company's bottom-line profitability suffered from higher production costs. While FNLPF is undertaking certain cost-improvement initiatives for portfolio optimization, there's still a long way to go. We have a ray of hope with Juanicipio ramping up to full-scale production in the near term. Nonetheless, we also have cash-burning mines like Cienaga, which incur an operating loss of ~$1,000+/oz of gold production.

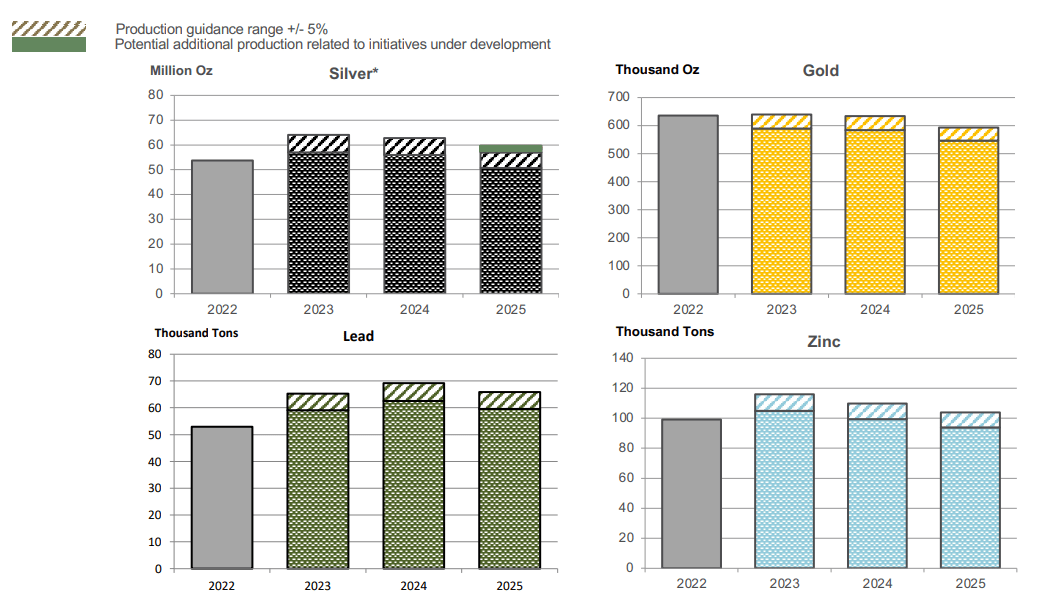

Having said that, I believe a lot will depend on the operational performance of key mining assets like Juanicipio, Herradura, Saucito, Fresnillo, and San Julian Veins (in the future). Besides, we should not ignore the possibility of PM prices moving significantly south from here and the impact it could have on the share price. I say so because FNLPF expects metal production to marginally decline from 2023 onward (check the charts below).

{kind=link}

Medium-Term Metal Production Outlook - Source: H1 Presentation

One might wonder whether the gradual decline in expected metal production over the medium term could impact the company's free cash flows and, consequently, its dividends. I doubt that because FNLPF plans to gradually reduce its CAPEX (check the chart below) over the medium term. Assuming precious metal prices will remain stable over the near-to-medium term, I believe FNLPF will have ample cash to pay dividends in the future.

2023-25 CAPEX Guidance - Source: H1 Presentation

Finally, given an improving gold/silver ratio, FNLPF must strengthen its gold portfolio. The company is actively conducting exploration studies on pipeline gold projects like Rodeo and Orisyvo and expects to ramp up these projects to the production phase over the next five years (subject to regulatory approvals).

Considering the above factors, I believe FNLPF can deliver suitable share price growth in the long run; however, the growth trajectory is more likely to build over time (due to the presence of multiple challenges, as discussed above).

For further details see:

Fresnillo: Expect Moderate Growth In 2024