MAG - Fresnillo plc: Do Not Expect Anything Particular In The Nearest Future

2023-03-09 18:53:48 ET

Summary

- The new Fresnillo plc Juanicipio mine should have a positive impact on silver and base metals production. However, its impact on gold production will be marginal.

- Over the last two years, we have seen a significant increase in costs of production; in my opinion, this problem will stay at Fresnillo plc.

- Lower throughput at nearly all mines is another negative factor.

- Despite strong metal prices, last year Fresnillo plc burnt cash.

- As a result, I still think that it is a good idea to avoid Fresnillo plc.

Introduction

With annual silver production of over 50 million ounces, Fresnillo plc ( FNLPF ) is one of the world’s largest primary silver producers. Today, the company operates eight mines, all located in Mexico. One of them, Juanicipio, is shared with MAG Silver Corp. ( MAG ), with Fresnillo plc holding a 56% stake (the remaining 44% belongs to Mag).

A few days ago, Fresnillo plc released an annual report for 2022 . Let me discuss this document and identify a few major problems this big miner is facing.

Production

Last year, Fresnillo plc produced 51.1 million ounces of silver, a bit more than in 2021 (50.0 million). However, gold production dropped from 751.2 thousand ounces in 2021 to 635.9 thousand in 2022 (a decrease of 15.3%). As for base metals:

- Lead production dropped by 6.4%

- Zinc production was flat compared to 2021.

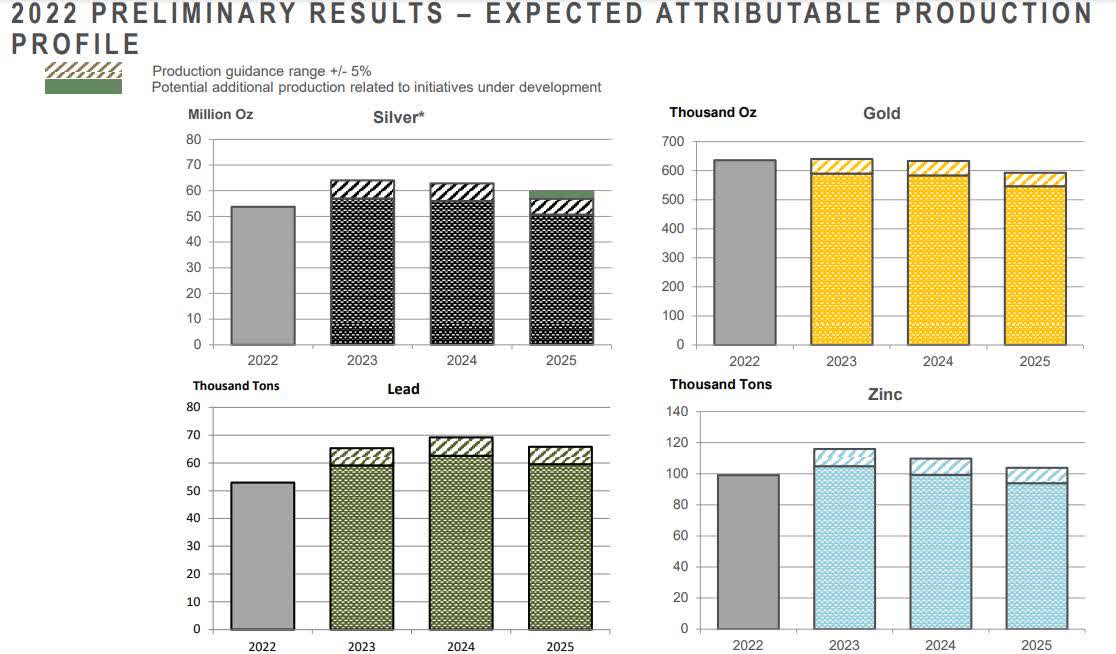

All right, it was a bit of history, so now let me show what likely is going to happen between 2023 and 2025:

{kind=link}

It is easy to spot that this year the silver, lead, and zinc production is going to increase a bit. The reason is obvious – at some point of this year, we should see the Juanicipio mine operating at full capacity. As a result, the total silver production (silver is the main metal produced by Juanicipio) should go up from 51.1 million ounces in 2022 to 53.0 (midpoint) this year. Due to the fact that Juanicipio is also a base metals producer, Fresnillo plc expects to deliver more zinc and lead this year. However, the Juanicipio’s positive impact on gold production will be marginal. Although this mine is expected to deliver between 21 and 28 thousand ounces of gold a year over the next five years (attributable to Fresnillo plc), this additional production will be overshadowed by lower production at Noche Buena (in fact, this mine should cease its operations soon). As a result, this year the consolidated gold production will be flat or even lower than in 2022.

Summarizing – due to Juanicipio, silver and base metals production should be higher in the coming years. However, I do not expect a spectacular increase. On the other hand, I expect no growth in the Fresnillo plc gold segment. And, as the chart below shows, the gold segment is crucial for Fresnillo plc :

{kind=link}

For example, last year the gold segment produced 54.2 million ounces of silver equivalent while the silver segment delivered 51.1 million ounces.

Costs of production

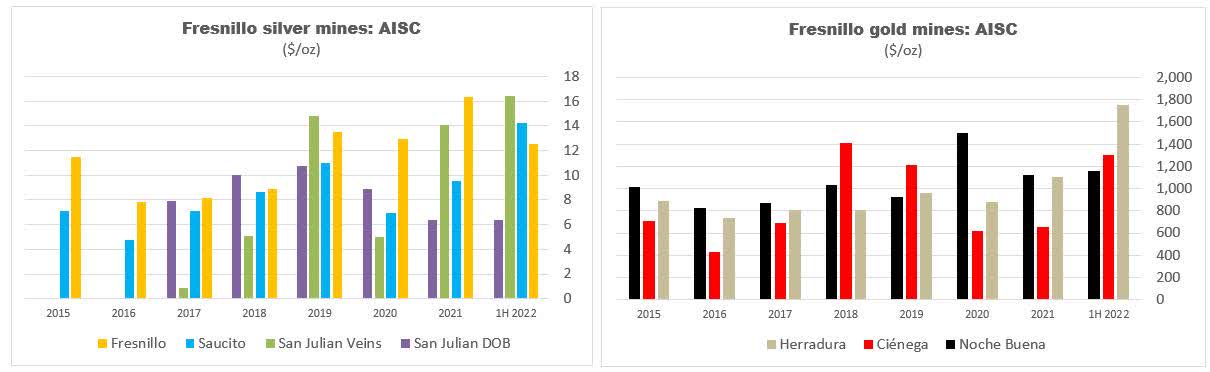

In my opinion, here is the largest problem Fresnillo plc is facing. Let me take the gold segment. Here the highest-cost producer is Cienega – last year this mine produced its gold at AISC (all-in sustaining cost of production) of $2,011 per ounce of gold. Keeping in mind that last year the average price of gold was $1,799 per ounce, each ounce of gold produced by Cienega burnt $212. Fortunately, Cienega is a mid-size mine (it accounted for 8.4% of the 2022 total production), so its high cost of production had a marginal impact on the overall results.

Herradura – big problem

On the other hand, the largest gold miner, Herradura, reported the AISC of $1,360 per ounce. In my opinion, it was a bad surprise because this mine used to be a low-cost producer in the past. For example, between 2015 and 2020 it was delivering its gold at the AISC standing below $1,000 per ounce. Then, in 2021 this cost jumped to $1,100 per ounce and last year to $1,360 per ounce!

As a result, a gross margin (defined as revenue less direct costs of production – look at the red arrow below) delivered by Herradura dropped from $281M in 2021 to a mere $147M in 2022. Interestingly, the average gold prices in 2022 and 2021 were comparable. In addition, the margin delivered by Herradura was comparable to the margins generated by much smaller mines as Juanicipio or Fresnillo:

Gross margins by mine (in millions of $):

{kind=link}

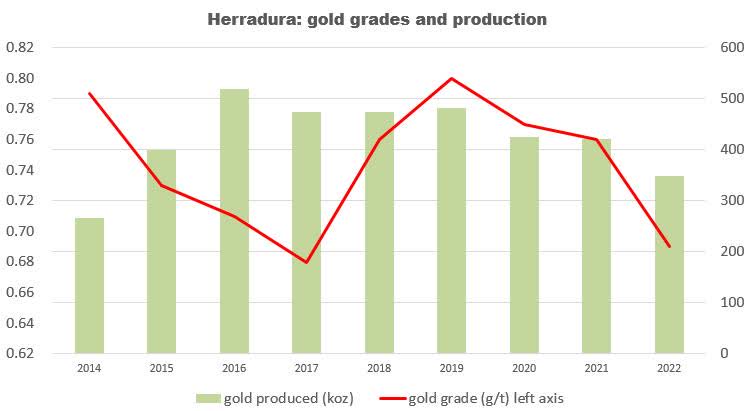

Summarizing – due to significantly higher costs of production at most of the mines (Cienega, Herradura, Noche Buena, Saucito and San Julian veins) last year the Fresnillo plc profitability dropped significantly. What is more, due to weakening metal grades I expect that costs of production will stay at last year’s levels or even go up further. The chart below illustrates this thesis – note that the main factors behind a significant production drop at Herradura were falling gold grades (the red line):

{kind=link}

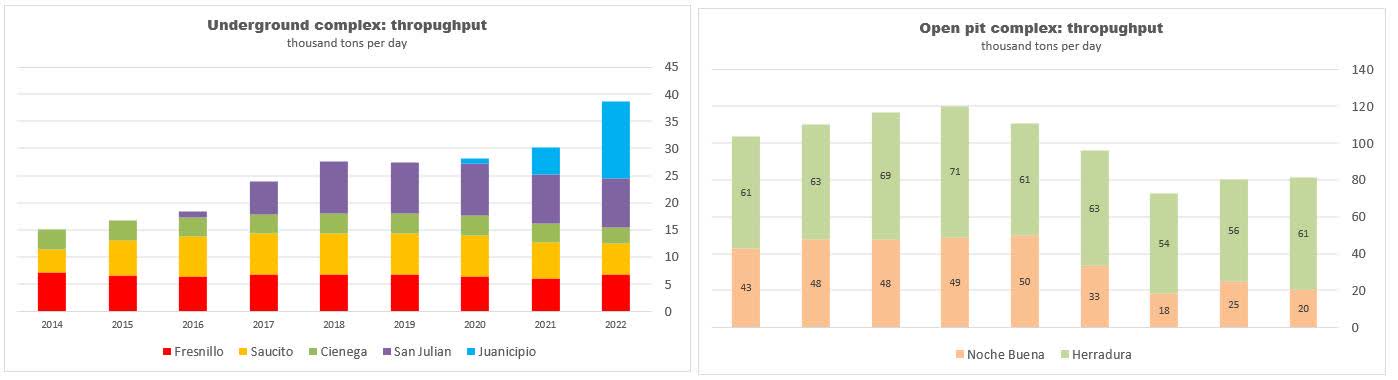

Throughput goes down across the board

Generally, if over the years a mine processes less and less ore, it means that there is not enough ore at such a mine. Of course, it is not a healthy sign for any mine. And in the case of Fresnillo plc, it is a common phenomenon.

Let me take, once again, the largest mine, Herradura. At its peak production, in 2017, Herradura was processing 71.3 thousand tons of ore a day. However, in 2022, this mine was processing only 60.8 thousand tons of ore a day, which means a decrease of 14.7%.

The same happened to each mine, excluding the newest one, Juanicipio. And here are the two charts illustrating this problem:

{kind=link}

For those interested in costs of production at the remaining mines, please, look at the chart below:

{kind=link}

Now let me discuss a few financial measures.

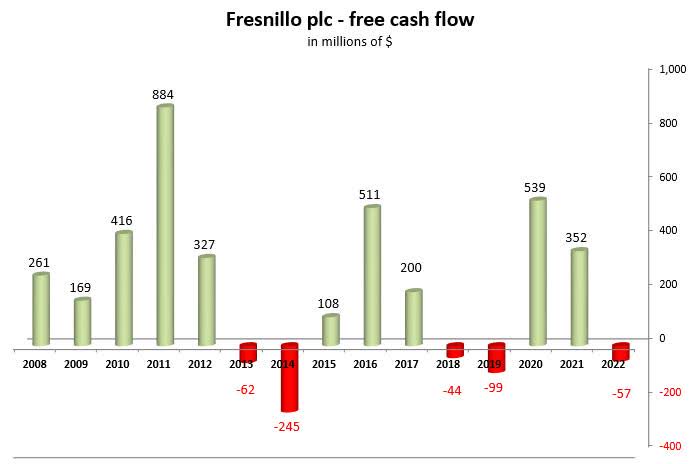

Cash flow

The chart below shows free cash flow delivered by Fresnillo plc since 2008.

Note: free cash flow is defined as cash flow operating activities less capex plus cash delivered by silver stream contract

{kind=link}

Interestingly, there were only five years when the company burnt cash: 2013, 2014, 2018, 2019 and 2022. The explanation for the first four years is easy – low prices of gold and silver (e.g., between $1,217 and $1,418 for gold). However, last year the prices were pretty strong: $21.7 per ounce for silver and $1,799 per ounce for gold. And despite higher metal prices the company also burnt cash. Definitely, higher AISC was the main factor behind this phenomenon.

Investment thesis

In my opinion, the negatives discussed above will stay at Fresnillo plc in the nearest future. Apart from Juanicipio and San Julian, the remaining mines are pretty old, and it will not be easy (or even impossible) to see a significant improvement there. What is more, even San Julian does not look that well as before. For example, last year this mine produced 22.1 million ounces of silver equivalent while in 2021 it delivered 25.4 million ounces (a decrease of 13.0% compared to 2021). The main factor behind was a lower silver grade at the DOB (Disseminated Ore Body) segment of this mine (168 g/t in 2022 vs. 221 g/t in 2021). This year the company expects another drop of the average silver grade (to 130 – 140 g/t) so I do not expect anything spectacular there.

As for the Juanicipio mine – this year it should be fully operational, so we will see whether my doubts about this mine were justified or not (those interested in details, please, refer to my last article on Fresnillo plc).

As a result, I still recommend avoiding Fresnillo plc shares . In my opinion, there are better precious metals plays to invest.

Strikingly, Mr. Market seems to share my opinion. For example, since my last article on Fresnillo (published on November 8, 2022), these shares have outperformed against GDX, a precious metals benchmark:

{kind=link}

For further details see:

Fresnillo plc: Do Not Expect Anything Particular In The Nearest Future