BLCO - From Euphoria To Reality: Viatris' Tale Of Market Whirlwind

2024-01-12 12:54:48 ET

Summary

- Viatris is an American pharmaceutical company formed as a result of the merger of Mylan and Upjohn.

- Over the past two and a half months, Viatris' share price has risen by more than 38%.

- Viatris' dividend yield is 3.97%, which is attractive because it is well above the sector median.

- On the other hand, the company's revenue and margins continue to decline year-over-year due partly to the sale of its biosimilar business to Biocon Biologics.

- I am initiating coverage of Viatris with a "hold" rating.

Viatris Inc. ( VTRS ) is an American pharmaceutical company formed as a result of the merger of Mylan and Upjohn. The company is one of the leaders in the generics industry.

Thesis

Over the past two and a half months, Viatris' share price has risen more than 38%, reflecting increasing sales of its branded drugs in recent quarters, stock market euphoria about the expected Fed interest-rate cuts in 2024, and statements from its management, which anticipates the company to generate free cash flow of at least $2.3 billion annually over the next five years.

{kind=link}

However, in light of the fall in its margins and revenue after the sale of its biosimilar business to Biocon Biologics, the overbuying of its shares based on the RSI and MACD indicators, and sluggish sales of its generic products and Tyrvaya, developed by Oyster Point Pharma, I believe that the current share price does not reflect these risks.

I'm initiating coverage of Viatris with a "hold" rating.

Viatris' relatively high dividend yield and strong balance sheet

The company has a return on equity of about 8.9%, which decreased slightly compared to 2022.

{kind=link}

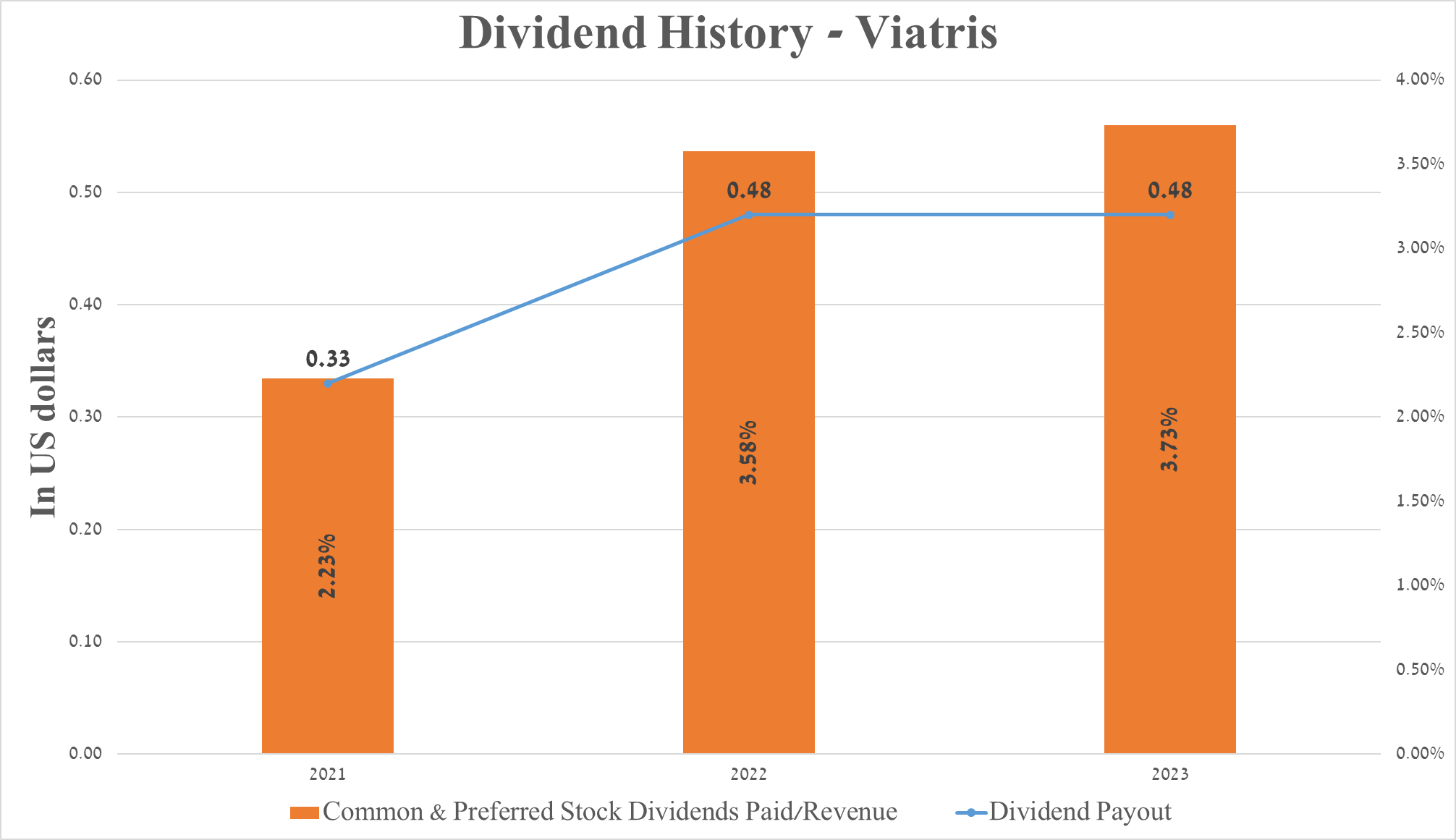

Over the past two years, the company's management has not increased dividend payments, and I expect this trend to continue, partly due to the fall in its revenue and the need to continue to reduce its debt burden in the current economic situation.

{kind=link}

On the other hand, its payout ratio [non-GAAP] of about 16.06% indicates no risks associated with a reduction in dividend payments.

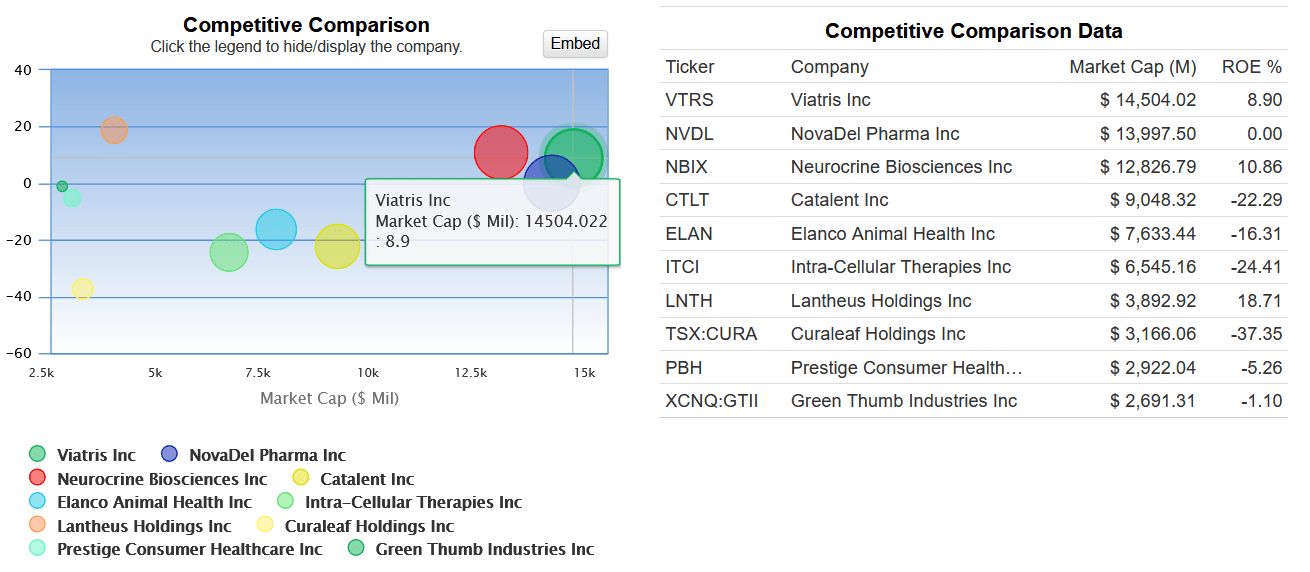

Viatris' dividend yield is 3.97%, which is attractive because it is well above the sector median. However, this figure is lower than that of many of its key competitors, including Organon & Co. (OGN), Takeda Pharmaceutical Company Limited (TAK), and Bristol Myers Squibb Company (BMY).

{kind=link}

Viatris' financial results and outlook

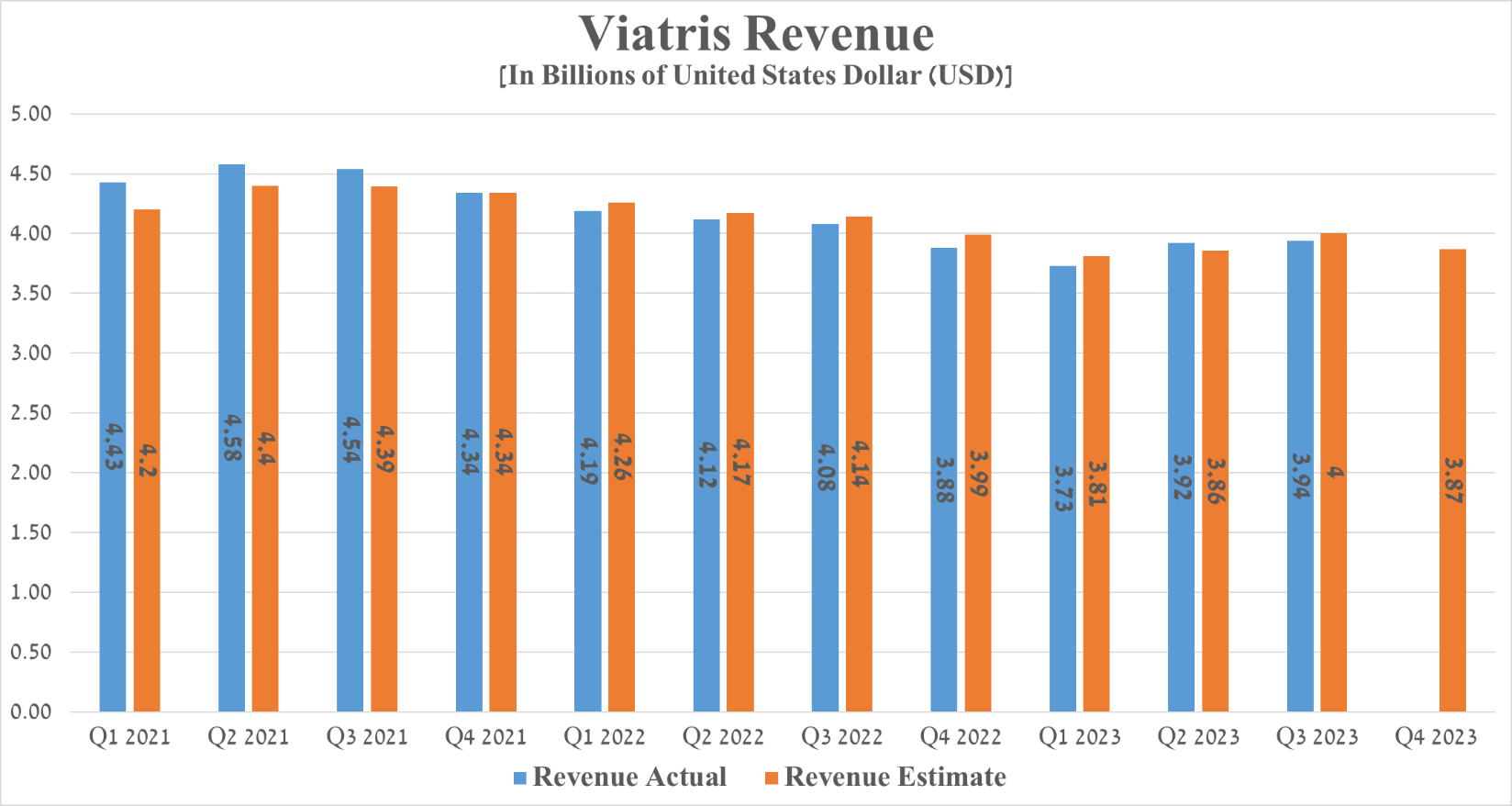

Viatris' revenue for the three months ended September 30, 2023, reaching $3.94 billion, down 3.4% from the previous year and, just as importantly, missing analysts' expectations by $60 million.

{kind=link}

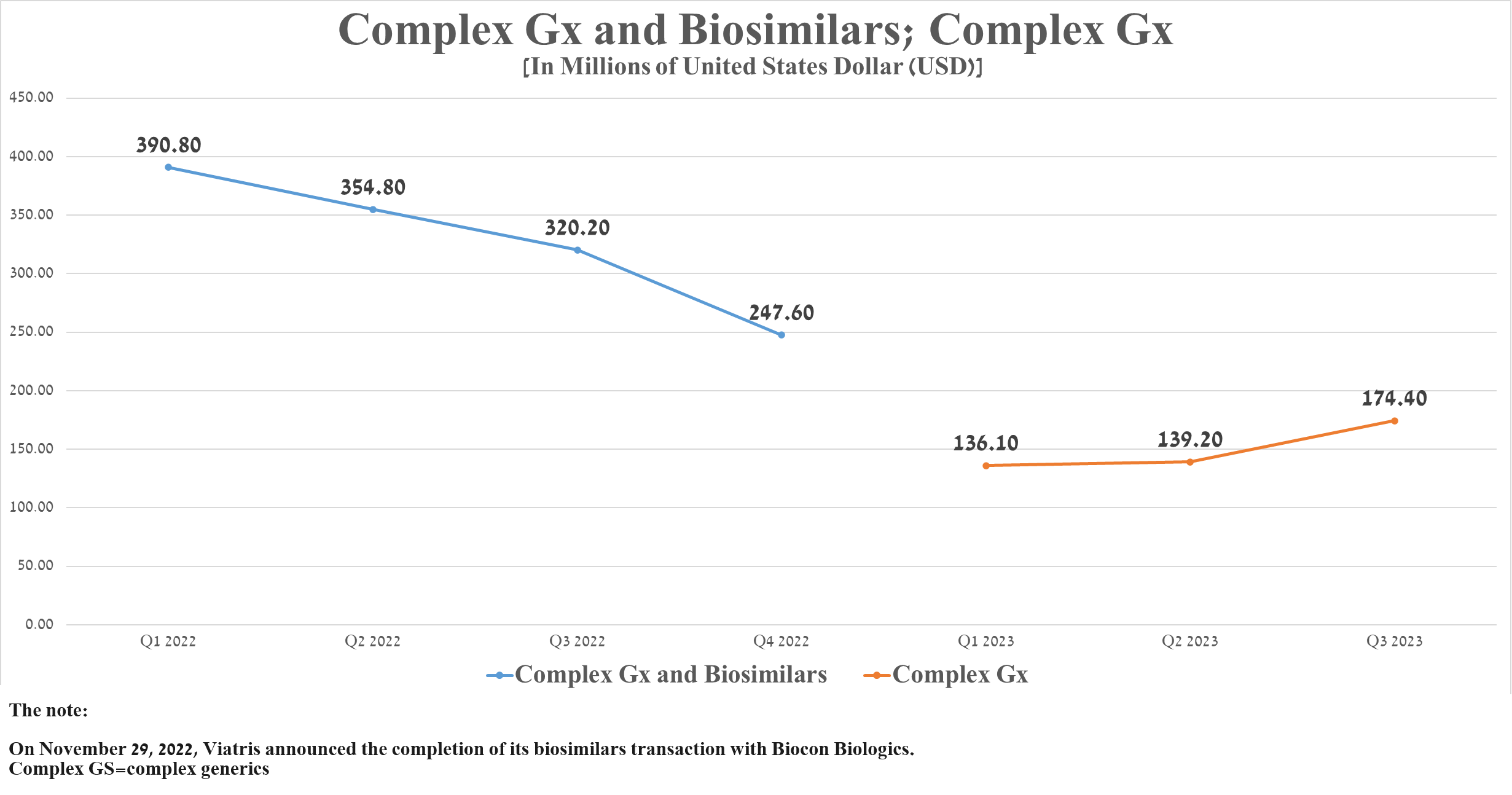

The year-on-year decline in this financial indicator was primarily caused by the sale of Viatris' biosimilar business for up to $3.335 billion. According to the deal, which closed on November 29, 2022 , Viatris received $3 billion. Of this amount, 2 billion was paid in cash, with another $1 billion representing convertible preferred shares in Biocon Biologics. Furthermore, Viatris could receive an additional $335 million in 2024.

{kind=link}

On the other hand, what pleasantly surprised me is the increase in sales of Viatris' branded drugs, whose exclusivity ended a couple of years ago. Sales of these products totaled approximately $2.53 billion in the third quarter of 2023, up 3.6% quarter-over-quarter, primarily due to increased demand for Lyrica, Zoloft, Creon, EpiPen, and Lipitor despite increased competition with its generic versions, as well as the launch of more innovative medications.

{kind=link}

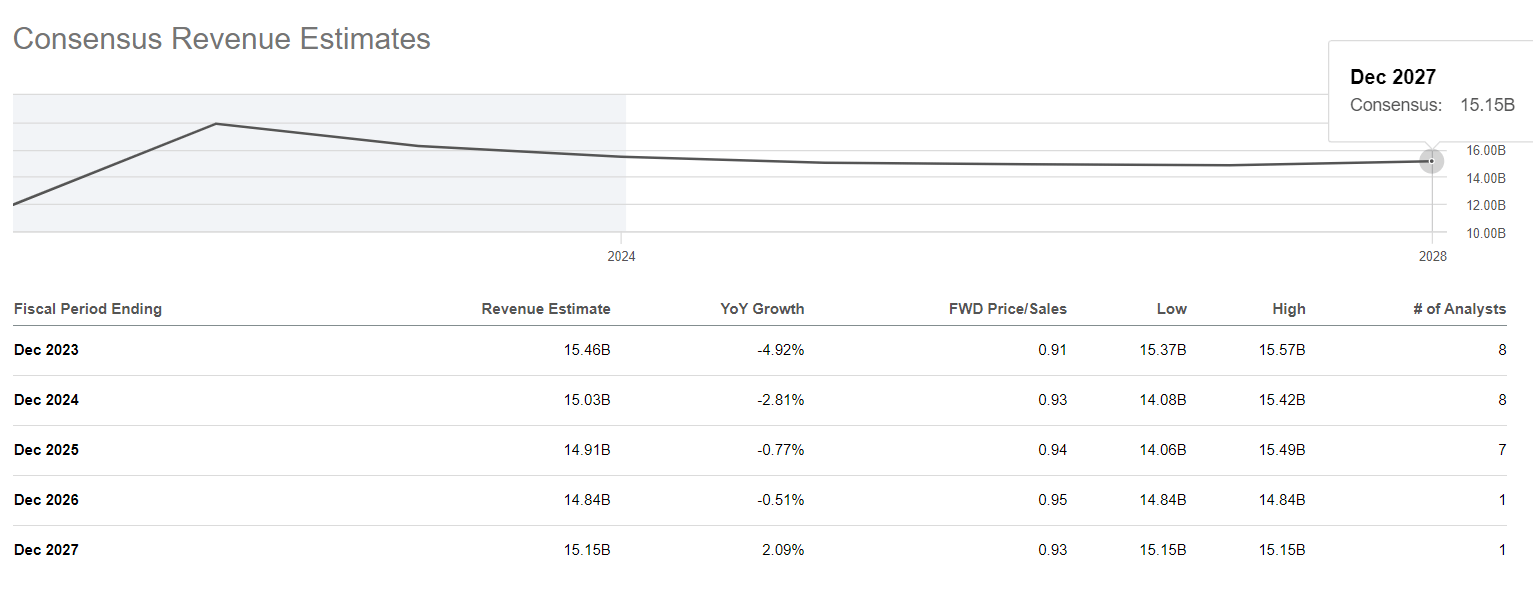

Seeking Alpha offers financial data on Wall Street analysts' expectations for the coming quarters. So, Viatris' revenue for the fourth quarter of 2023 is anticipated to be in the range of $13.87 billion to $14.34 billion, which is 8.8% less than the previous year.

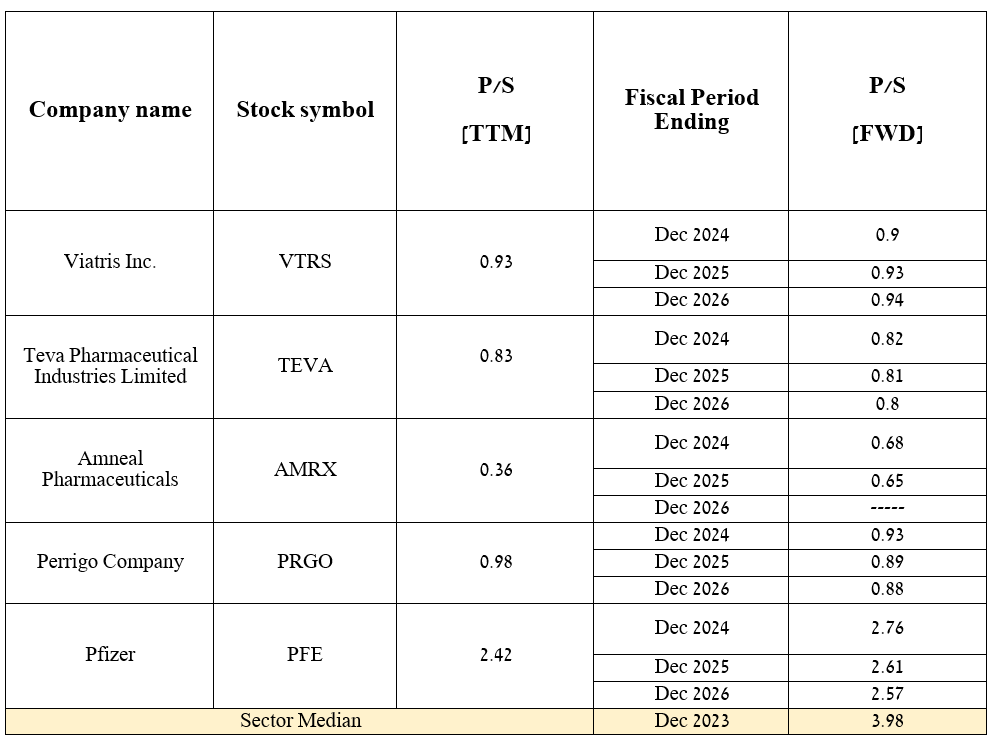

In addition to the company's year-on-year decline in revenue, its price/sales [FWD] is 0.94x, which at first glance may indicate that Viatris is trading at a discount to most pharmaceutical companies, but in my opinion, this is not the case. This is because its P/S stays comparable to many other major generic drugmakers, which in the eyes of investors are the less preferred choice to Big Pharma, including Pfizer Inc. ( PFE ), due to their slow revenue growth and relatively low gross margins.

{kind=link}

At a more global level, Viatris' revenue is projected to decline steadily over the coming years, and as a result, its P/S ratio will drop to 0.93x by 2027, remaining unchanged from its current value.

As a result, this makes Viatris less attractive to long-term investors looking for healthcare assets. Especially compared to companies with higher dividend yields and whose portfolios consist of blockbusters and experimental drugs aimed at treating cancer and autoimmune diseases.

{kind=link}

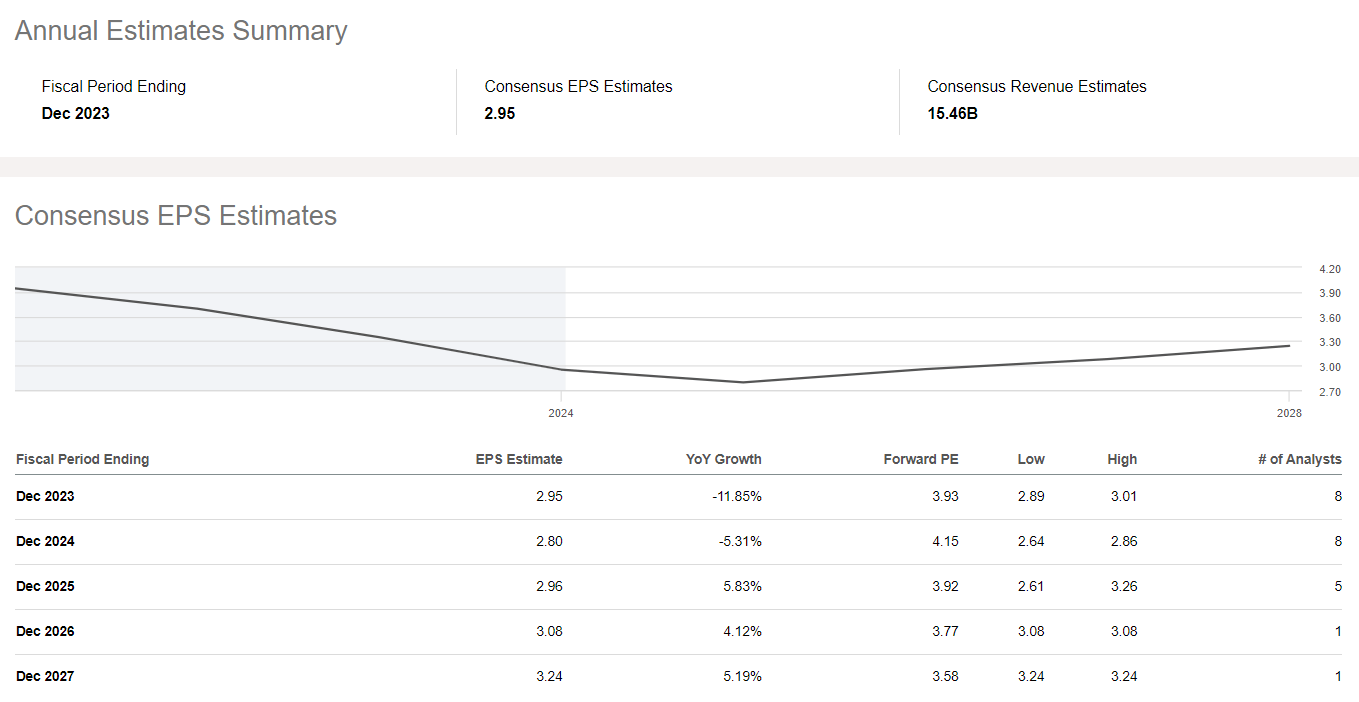

Viatris' Q3 Non-GAAP EPS was $0.79, beating analysts' consensus estimates by $0.05. However, its EPS is expected to be in the range of $0.57 to $0.7 in the fourth quarter of 2023, which is 3.64% relative to the fourth quarter of 2022.

{kind=link}

Wall Street forecasts that Viatris' net income will continue to decline through 2026, and even after that period, its EPS growth rate is expected to be subdued, reaching $3.24 in 2027, despite an anticipated improvement in global economic conditions.

In my assessment, one of the possible reasons for this trend is the low growth rate of Tyrvaya, as well as the lack of promising product candidates with an innovative mechanism of action that can change the approach to the treatment of common diseases.

{kind=link}

It is equally important to discuss Viatris' debt, which, in my assessment, is not a significant risk to its financial position. So, its net debt amounted to about $17.23 billion at the end of the 3rd quarter of 2023, and at the same time, it decreased by 31.6% relative to 2020 due to the repayment of senior notes. Also, on the earnings call , Chief Financial Officer Sanjeev Narula said the company paid off $500 million in debt in the fourth quarter of 2023.

Over the last 11 quarters, we have generated over $7.2 billion of free cash flow, and as a result, we have been able to pay down approximately $6.1 billion of debt during the same period, and we will pay down the $500 million maturity in Q4 from cash on hand.

However, due to the company's continued decline in EBITDA in recent years, driven both by the sale of its biosimilars franchise and falling sales of its branded drugs, its net debt/EBITDA ratio has remained almost unchanged over the past three years and stays around 3.5x.

As a result, on August 10, 2023 , S&P Global Ratings left the company's long-term credit rating unchanged at "BBB-" but at the same time revised the outlook from stable to negative.

{kind=link}

Key risks to consider

In addition to the expected technical correction, I will highlight two potential risks that financial market participants need to consider minimizing potential losses.

Viatris' acquisitions continue to disappoint

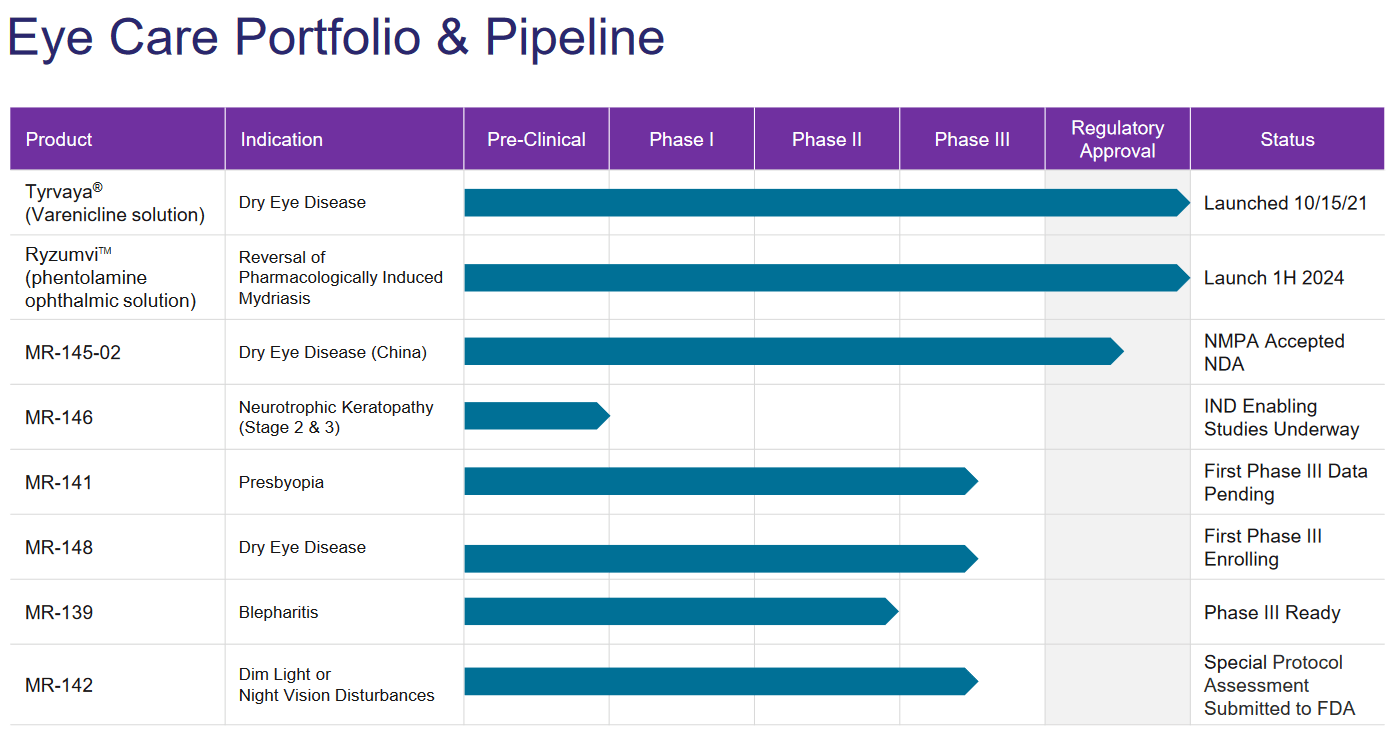

On November 7, 2022 , Viatris announced the acquisition of Oyster Point Pharma for approximately $415 million upfront. As a result of the deal, the company acquired several product candidates and Tyrvaya , an FDA-approved drug for the treatment of patients with dry eye disease.

{kind=link}

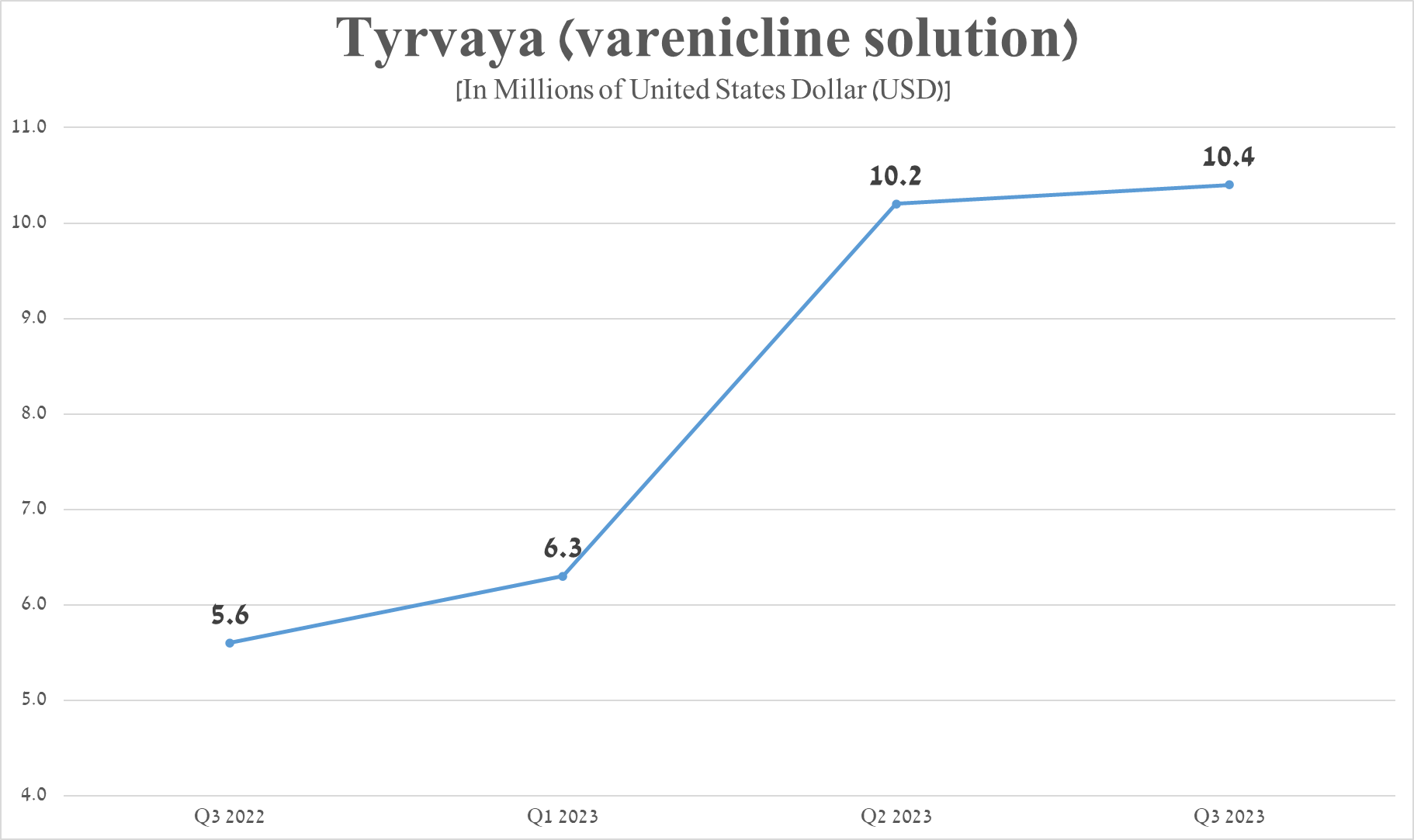

However, its sales were $10.4 million in the third quarter of 2023, up slightly from the previous quarter due to intense competition with other drugs, including AbbVie Inc.'s Restasis ( ABBV ), Kala Pharmaceuticals' Eysuvis, Bausch + Lomb Corporation's Xiidra ( BLCO ).

{kind=link}

On the Q4 2022 earnings call , President Rajiv Malik said revenue from Tyrvaya will be $56 million in 2023, but it's already clear that this figure will be significantly less as its sales totaled $26.9 million over three quarters.

We expect to deliver approximately $500 million in new launches, plus $56 million in revenue from Tyrvaya, which more than offsets 2.9% erosion of our base business.

As a result, I am inclined to believe that it is unlikely that Michael Goettler's forecast of achieving $1 billion in Viatris Eye Care revenue by 2028 will be realized.

In January, we completed the acquisitions of Oyster Point Pharma and Famy Life Sciences to establish our new Viatris Eye Care division. And as we said, we anticipate the combined assets of these acquisitions to add to the top line immediately and grow strong double-digits from there, reaching at least $1 billion in sales by 2028.

In addition to the low growth rate of Tyrvaya sales, other pharmaceutical companies are actively working to develop medications that are more effective than Viatris' product candidates. Financial market participants should also consider that more generic versions of blockbusters approved for the treatment of various eye diseases are on the market, which will eventually have a negative effect on the sales trajectory of the company's ophthalmology franchise.

Lack of growth in sales of Viatris' generics

Despite expanding the company's portfolio of generic products, including lenalidomide, total sales have not shown clear growth in recent years.

{kind=link}

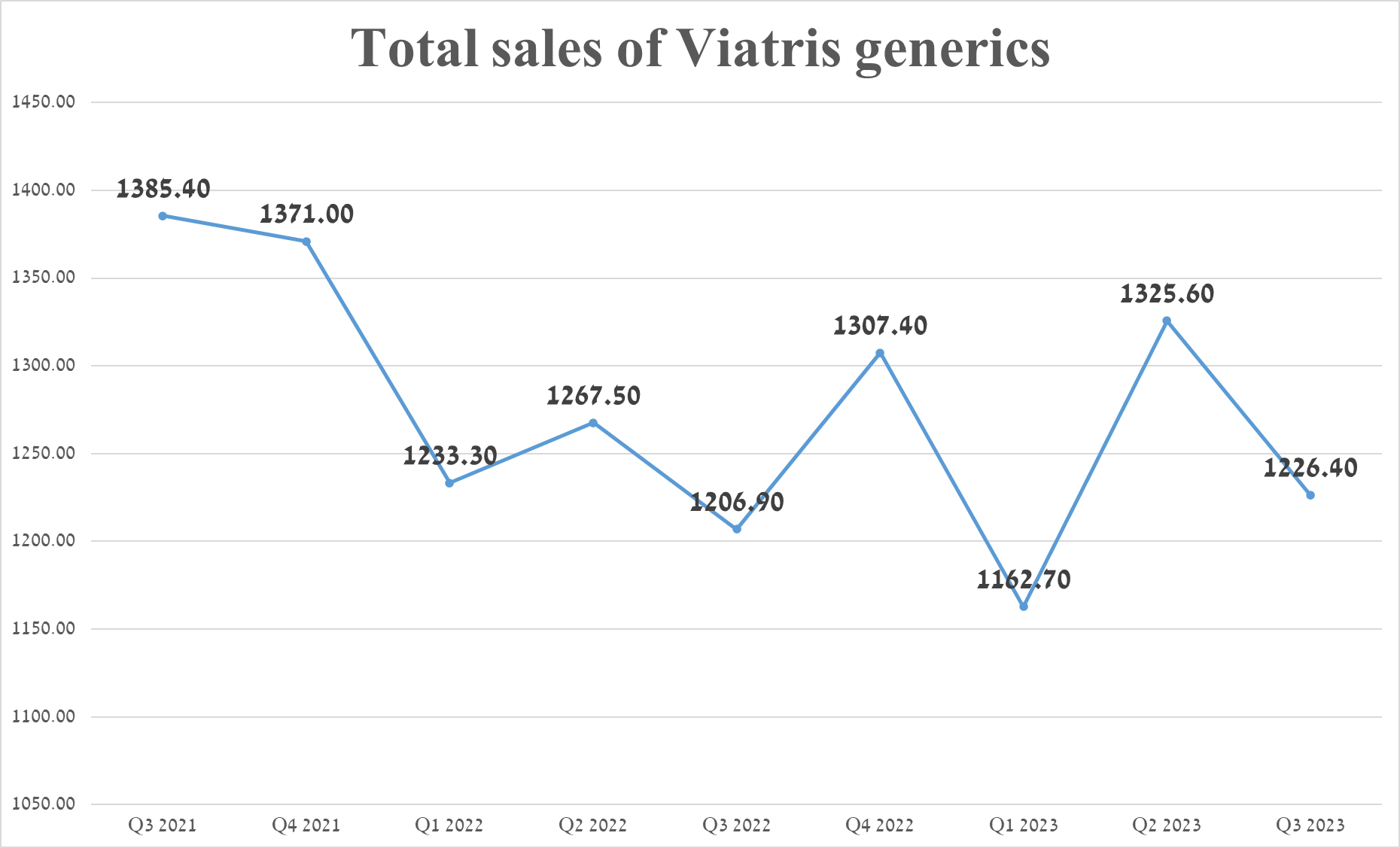

So, Viatris' generic drug revenue was about $1.23 billion for the third quarter of 2023, down $99.2 million from the previous quarter. This negative trend is explained by a decrease in sales volumes of existing medicines caused by increased competition with other generic manufacturers, including Teva Pharmaceutical Industries Limited ( TEVA ), Sandoz, and Dr. Reddy's Laboratories Limited ( RDY ), as well as a decrease in their prices in the US market.

Takeaway

In recent months, Viatris' share price has risen significantly, reaching a strong resistance zone between $12 and $12.2, which the bulls were unable to break through after several attempts. Additionally, given that Viatris' revenue and gross margin continue to decline, and the company is trading in line with its historical 5-year average P/E and P/S ratios, I believe it is not an attractive asset for long-term investors looking for undervalued healthcare assets ahead of the anticipated Fed interest-rate cuts in 2024.

For further details see:

From Euphoria To Reality: Viatris' Tale Of Market Whirlwind