FTDR - Frontdoor: Improving Renewal Base With Upside From The New Frontdoor Brand

2023-06-02 14:44:20 ET

Summary

- Frontdoor is the leading home service plan provider in the US, operating primarily under the American Home Shield brand.

- I am initiating coverage on the name with a Buy rating and a price target of $36.6, with an implied upside of 16.7% (as of May 24, 2023).

- I believe Frontdoor will continue to lead the home service industry with its scale, efforts on digitalization, and recurring revenue model with healthy margins.

Introduction

Frontdoor (FTDR) is the leading home service plan provider in the US, operating primarily under the American Home Shield brand. With inflation easing and the macro-environment acting more in favor for FTDR, I believe the FTDR stock presents an interesting investment opportunity at current valuations. The company's established scale, bolstered by its commitment to digitalization and offerings expansion, coupled with its ability to generate recurring cash flow, not only protects against downside risks but also lays the groundwork for future growth. Read below for more.

Company Overview

FTDR's value proposition involves providing customizable subscription-based service plans that protect and handle unexpected breakdowns of home systems and appliances through its network of 15,000 contractors. Contractors benefit from the significant work volume and stable demand from FTDR by being part of the network. As of December 31, 2022, FTDR had 2.1 million active home service plans across the US.

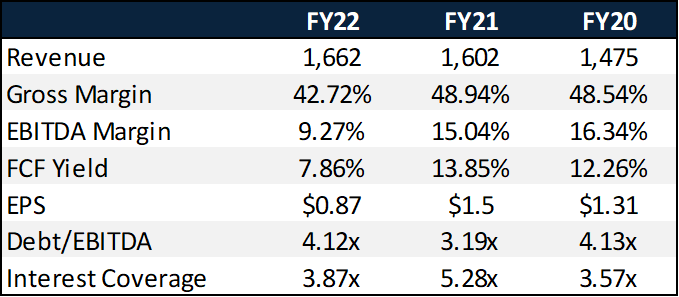

Financial Snapshot

FTDR experienced margin compression in FY22 due to inflation in raw material and labor costs. The real estate segment suffered a 37% year-over-year decline due to interest rate hikes. Still, the renewal and DTC segments demonstrated resilience with high single-digit growths and improved renewal rates.

{kind=link}

Frontdoor 10k, Created by Author

Industry Overview

FTDR operates within the broader US home service category, which generates approximately $500 billion in revenue, as stated in the company 10k . The current FTDR verticals target the $100 billion repair and maintenance sectors within the broader TAM, indicating opportunities for further penetration.

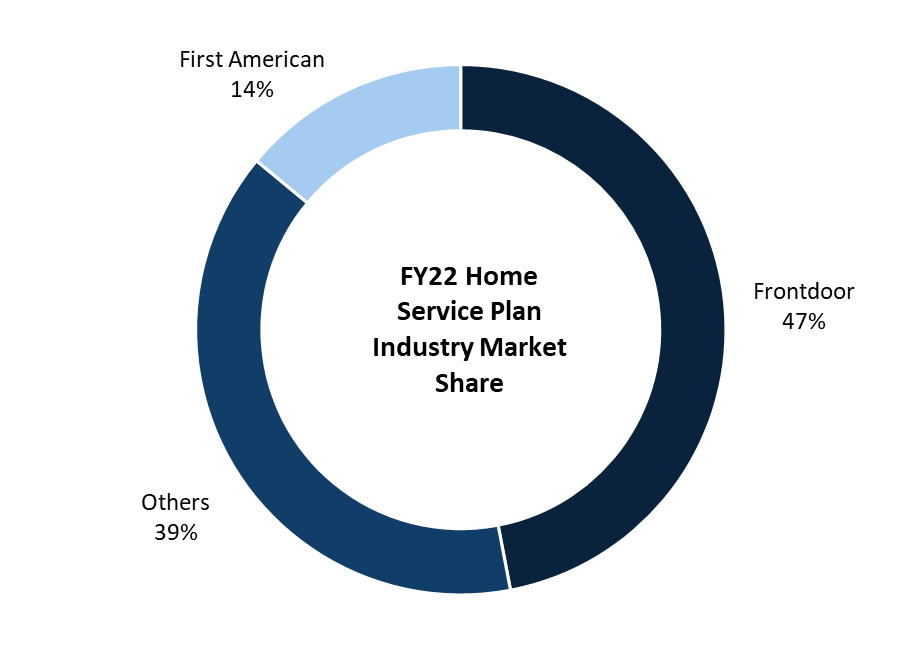

Competition

The competition in the home service plan industry is at a medium level, with a few major players such as FTDR, First American Financial (FAF), and Old Republic International (ORI). According to IBIS World , as of 2020, FTDR held the largest market share in the industry at 47.9%, First American accounted for 14%, and other companies made up the remaining 38.1%.

{kind=link}

IBIS World, Created by Author

Internal competition within the industry is typically based on two factors: 1) pricing structure and 2) service coverage. The average monthly payments range from $22 to $76, with additional one-time service fees ranging from $60 to $125. I am also seeing companies expanding their offerings to offer personalized coverage for specialty appliances, on-demand service, and DIY guidance to differentiate from competitors.

Thesis Explainers

Well-Positioned in the Growing Market with Incomparable Scale

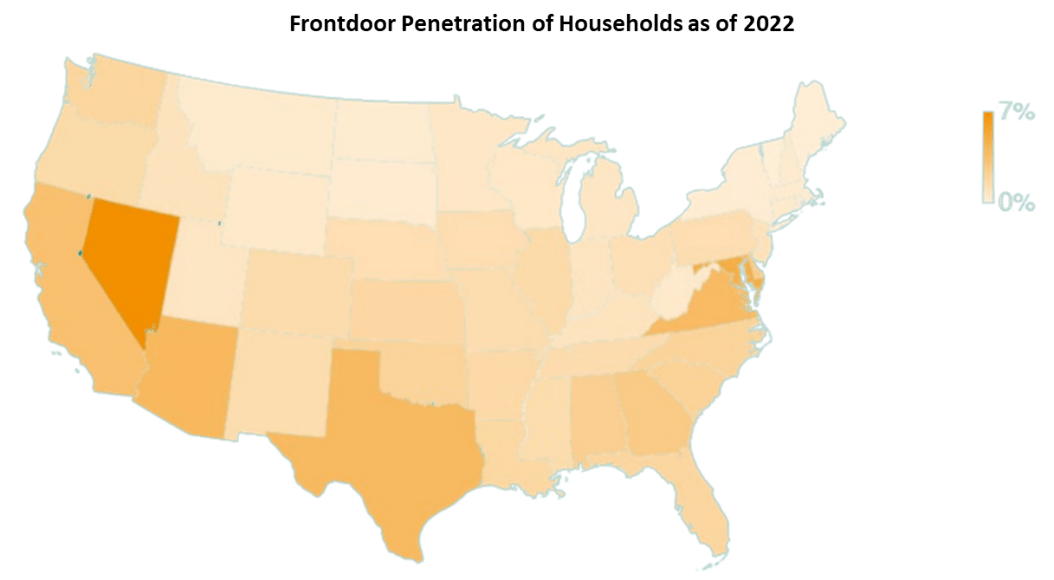

FTDR has three times the size of its closest competitor in the US. The overall industry penetration remains low, with only 6 million out of 128 million US households or approximately 4% subscribe to a home service plan, indicating a healthy runway for growth. Although some might argue that similar products like AppleCare failed to appeal to a larger customer base, I believe the home service plan has the potential to penetrate further as houses have longer useful lives and high switching costs. I will argue that the industry's historically low penetration rate should be attributed to companies' customer acquisition strategies rather than the product itself.

In the past, the industry relied heavily on a real estate go-to-market strategy to acquire new customers, leading to a limited TAM centered around existing home sales. I believe this agent-driven sales approach failed to educate consumers on the values of home service plans, hindering consumer brand awareness and engagement. Therefore, I favor FTDR's shift towards DTC, where the sales process is more interactive and engaging, leading to more loyal customers. The result speaks for itself, as FTDR grew its DTC channel at a CAGR of 7.02% over the past five years, with a renewal rate above 70% compared with the mid-20% in real estate, as stated in the company presentation.

{kind=link}

Frontdoor Presentation

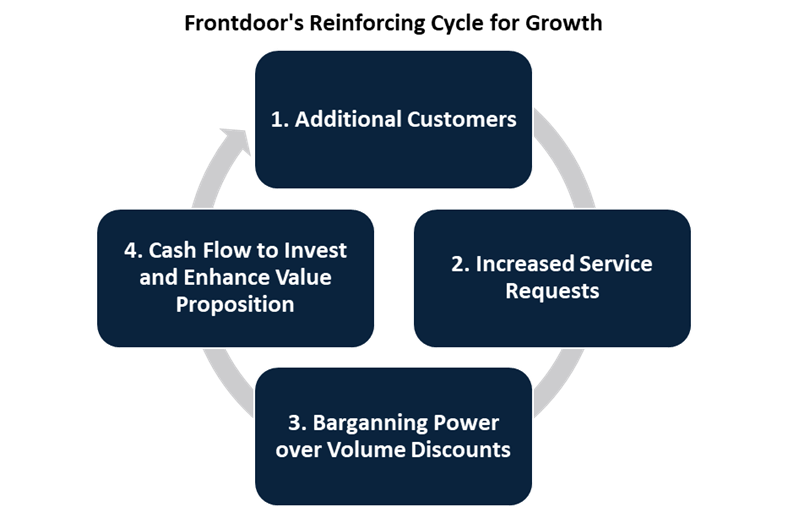

I believe FTDR is well positioned to further cultivated the market through its established scale that form a flywheel for continuous growth. Currently, FTDR serves 2 million customers by collaborating with 15 thousand contractors that handle 4 million job requests annually across 50 states. The company leverage on its preferred contractors who meet FTDR's stringent quality criteria for 82% of the service requests. These preferred contractors benefit from the high volume of work and typically see FTDR account for approximately 40% of their total business. In return, these contractors offer labor rates that are approximately 45% lower than other contractors. Moreover, FTDR can secure volume discounts with OEM suppliers for replacement parts, further enhancing its margins and pricing flexibility. Based on my analysis, FTDR's scale creates a self-reinforcing cycle in which an increasing number of customers generate higher demand for services, leading to volume discounts on labor and parts, ultimately resulting in higher margins and cash flows.

{kind=link}

Frontdoor Presentation, Created by Author

Value Prop Enhancement Through Digitalization and Expanded Offerings

I believe FTDR's efforts on digitalization and on-demand services separate itself apart from the old-fashioned and low-tech competitors that still rely on website forms or calls to request services. In 2019, FTDR acquired Streem , a tech start-up utilizing enhanced augmented reality, computer vision, and machine learning to expedite accurate diagnoses of breakdowns and facilitate repairs for home services professionals. This technology reduces repair time and, in some cases, eliminates the need for an in-home technician by providing simple DIY solutions. In 2022, FTDR launched ProConnect , which tackles specific customer requests leveraging its extensive contractor network and solves critical pain points for customers, such as finding qualified professionals and transparency over costs.

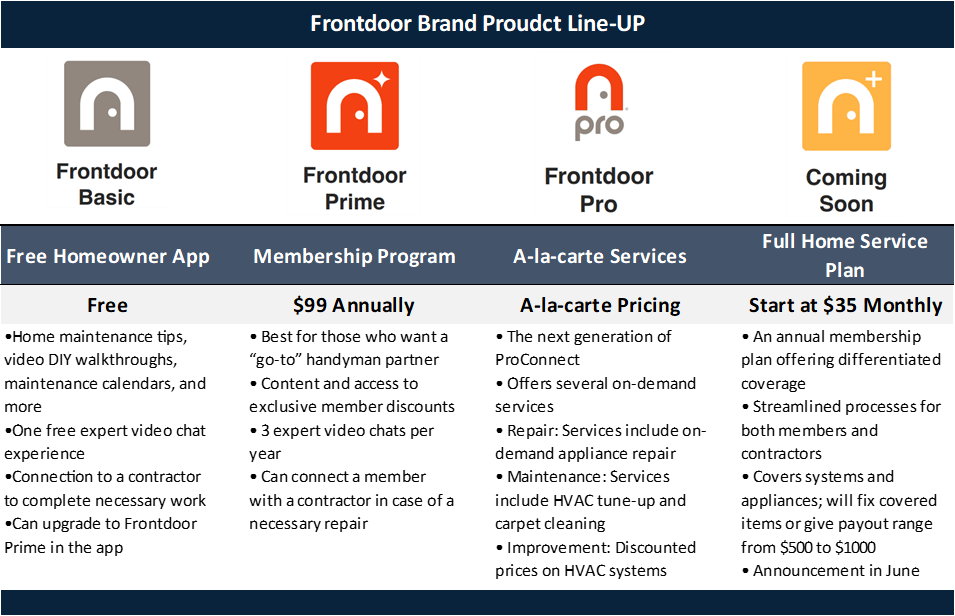

Upon the recent investor day , FTDR announced a plan to launch the new Frontdoor branding that combines the capabilities of Streem and ProConnect into a digital home service membership. According to the company presentation, the new brand is set to capture another 42 million potential customers outside of the traditional home service plan through its differentiated offerings on FTDR Basic, Prime, and Pro. I believe the apps further solidify FTDR's brand name as the one-stop home services solution. Within the first month of launch, the apps already surpassed 225k downloads , with customers utilizing and sharing positive feedback on the free expert calls. It is important to note that the project is still in its early stage and subject to management execution. Nonetheless, I believe a successful roll-out has the potential to enhance the value proposition for customers and generate additional revenue for contractors. This, in turn, further reinforces FTDR's growth cycle.

{kind=link}

Frontdoor Presentation

Sustainable Subscription-Model with Recurring Free Cash Flow

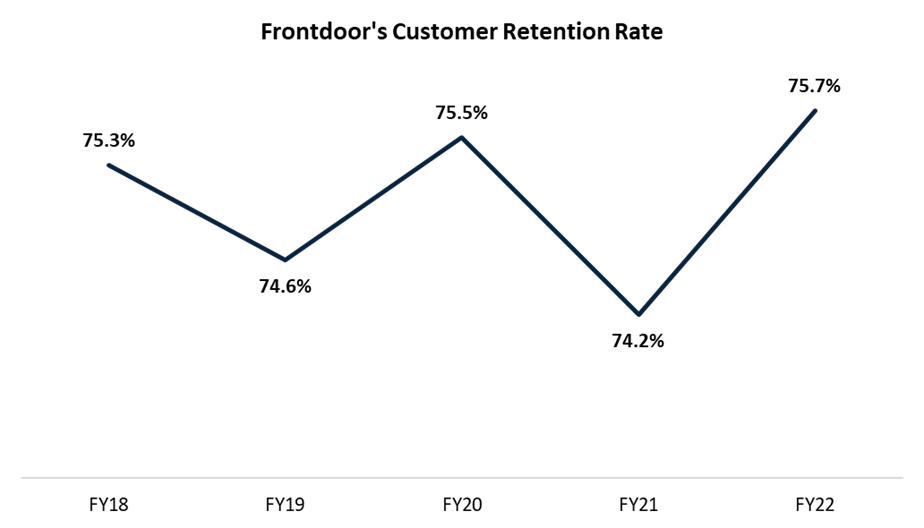

FTDR’s subscription-based business model provides certainty and visibility over revenue and free cash flow generation. The company's customer retention rate is a crucial metric for assessing its performance, as FTDR estimates a 1% increase in retention rate translating to $20 million in annualized revenue. Over the past five years, FTDR has maintained an average retention rate of 75.1% and reached a peak of 75.7% in the latest fiscal year.

The renewal period begins after customers initially join through the real estate or DTC channel. Customers acquired through real estate typically receive the plan as a purchased gift, paid upfront by the broker or seller. The real estate renewal rate is only around 30%. In the DTC channel, 18% of customers pay upfront, while 82% have monthly autopay arrangements. The flexibility of payment options and increased awareness among DTC customers contributed to a 74% renewal rate after the first contract in FY22. The substantial renewal base ensures revenue stability, with the renewal channel accounting for 72.4% of FTDR's total revenue in FY22.

{kind=link}

Frontdoor 10k

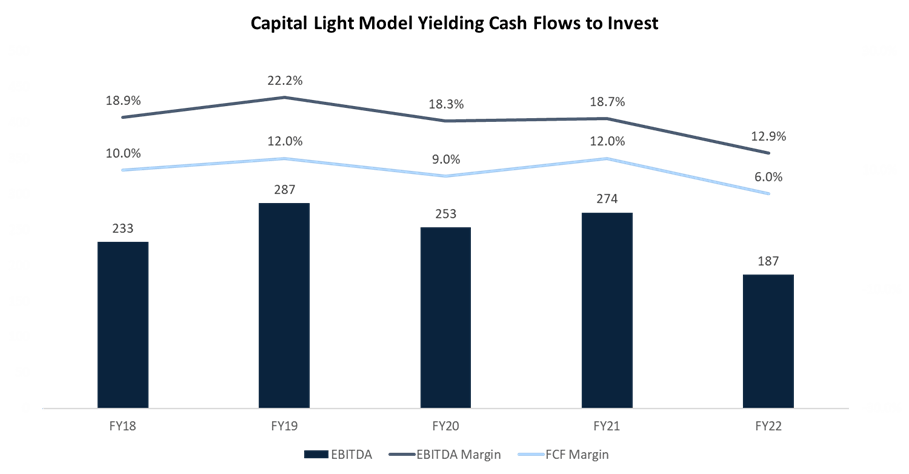

Walking down the income statement, FTDR has maintained consistent margins over the years and has generated meaningful cash flow. Excluding the potential impacts from the inflationary period in FY22, the average EBITDA margin stands at 19.5% and the FCF margin at 10.8% for FY17-FY21. In 2022, FTDR faced several macro headwinds that impacted its margins, including a decline in home sales, raw material inflation, and new investments in rebranding. However, I believe FTDR's margins are still relatively safe and expect to rebound as these headwinds subside.

Looking ahead, I believe FTDR's subscription-based model provides flexibility to allocate resources towards 1) core business investments, 2) selective mergers and acquisitions, and 3) debt repayment. Specifically, FTDR can use its available resources to invest in on-demand services and further expand the DTC channel, strengthening its already defensive competitive position.

{kind=link}

company 10k

Catalysts

Easing Inflation and Improved Supply Chain Bottlenecks

In the coming months, FTDR expects to benefit from easing inflation and improved supply chain conditions , leading to a decline in raw material costs. I believe impacts will be direct and significant to FTDR, as its Q1 result immediately improved as inflation moderates. Investors should continue monitor the related macro indicators to further assess FTDR's recovery.

Roll-Out of Full Home Service Plan App in June

In June, FTDR will launch the FTDR Premium App, offering comprehensive coverage that has the flexibility to fix or payout to customers. FTDR anticipates that the app will provide an enhanced user experience through digitalization and the ability to predict costs accurately. I look favorably to the launch since most competitors do not have this kind digital capability, which position FTDR well in the digital transformation trend.

Valuation

DCF Model Analysis

{kind=link}

Created by Author

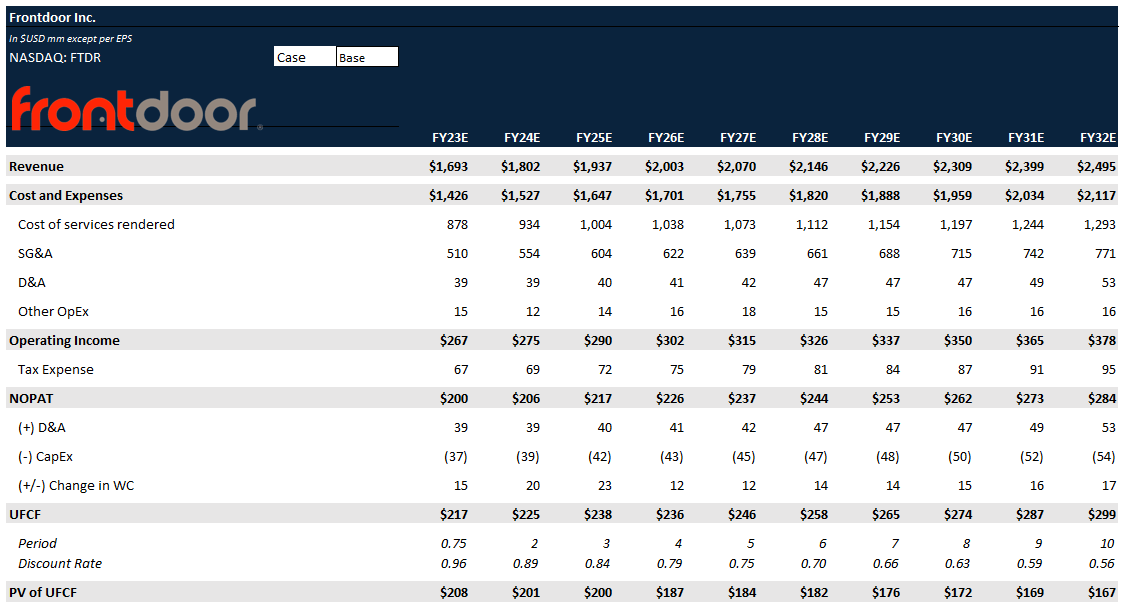

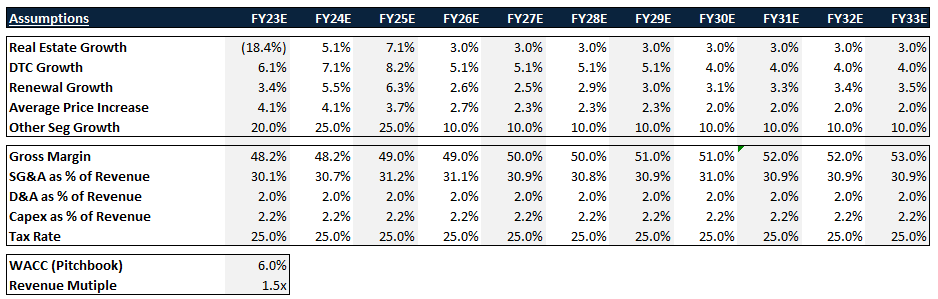

I anticipate that the real estate market will continue to experience a decline in the short to medium term due to elevated interest rates and a pessimistic economic outlook. Even if the real estate channel recovers, I believe the long-term growth will stay around a low single-digit rate due to limited TAM correlating with existing home sales. With the DTC channel's proven track record, FTDR poises to maintain its momentum and establish the channel as the key driver for attracting new customers. I project the segment to grow at a mid single-digit rate during the forecasted period, similar to the historical figures. I expect FTDR's digitalization efforts and on-demand service to improve customer stickiness across channels and result in mid single-digit growth in the long term. Furthermore, I expect the new Frontdoor brand to generate approximately $100 million in FY25, with momentum driven by recent download data and positive feedback across app stores.

I expect FTDR to gradually improve its gross margin as inflation moderates and leveraging on its growing economies of scale. The SG&A should relatively be fixed around a similar level, as I see the home service market needs to continue educating customers to achieve higher penetration. I believe the Capex and D&A should be flat as FTDR operates on a capital-light business model. Finally, the WACC is 0.0601 based on Pitchbook , and the terminal value is calculated based on a revenue exit multiple of 1.5x in FY33E.

{kind=link}

Created by Author

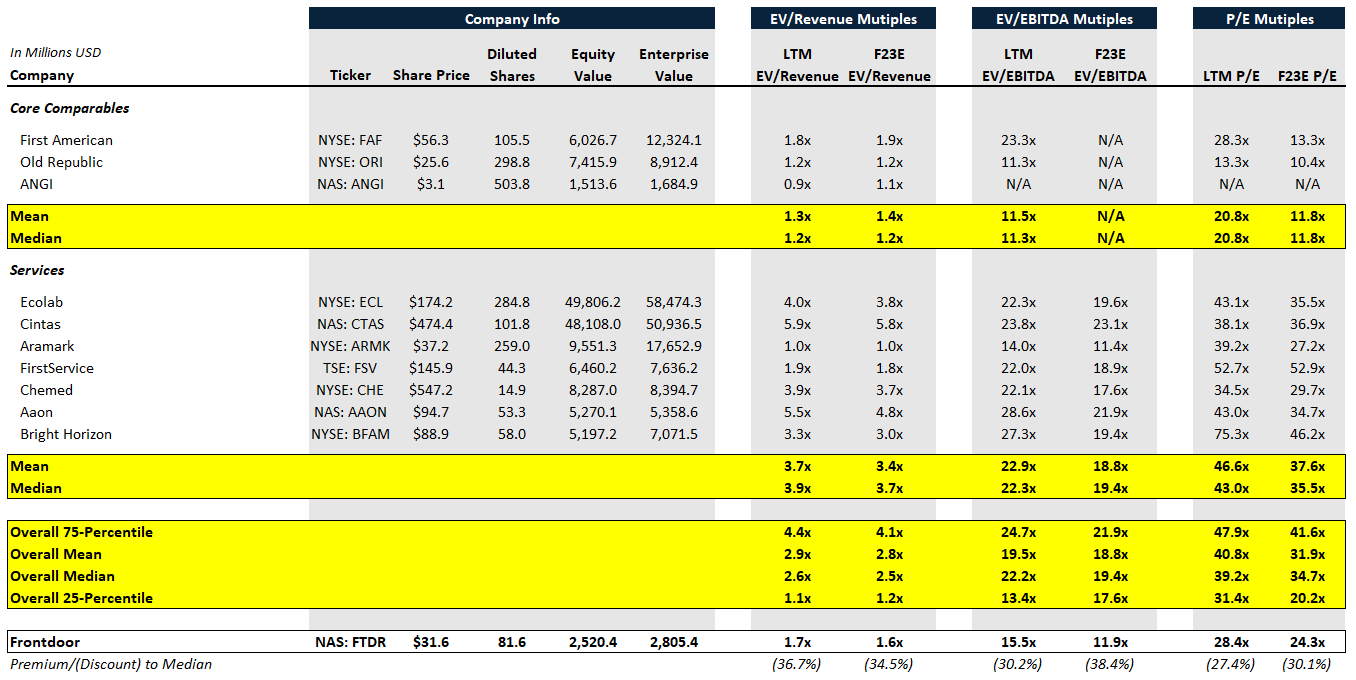

Public Comps Analysis

{kind=link}

Created by Author

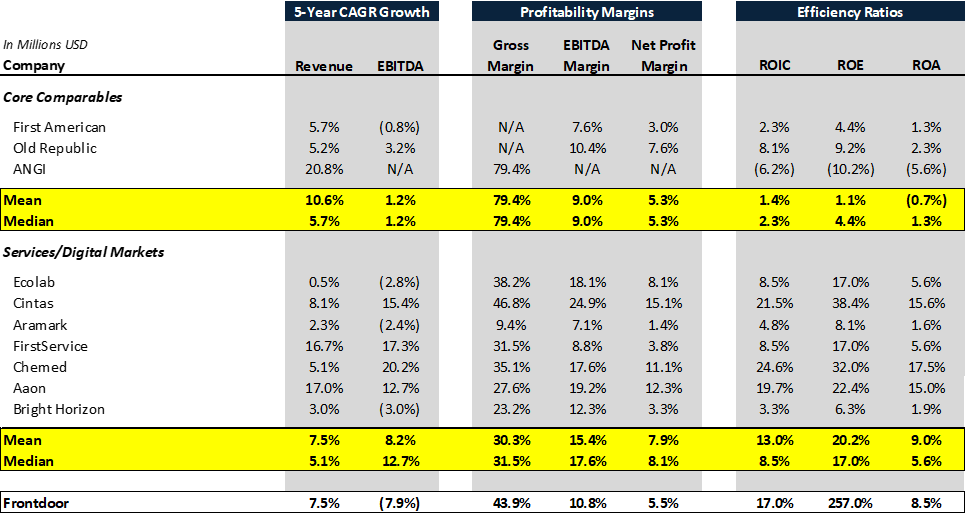

FTDR's business model stands out due to its uniqueness, as many of its public comps align with only one of FTDR's businesses, either the core home service plan or the on-demand service. Among these comps, First American and Old Republic are the most similar, as they rank as the second and third largest providers of home service plans in the US. However, it's worth noting that home service plans constitute only a small portion of their overall business. Angi ( ANGI ) is a well-matched comparison with FTDR's growing on-demand offering, as the firm is a leading online home service marketplace with extensive operations in the US and Europe. In addition to these specific comparable, broader services companies with similar financial profiles and service natures have also been taken into consideration. Currently, FTDR is trading at a premium benchmarking to the core comps but at a hefty discount to the overall median. Looking into the ratios, FTDR has promising performance compared to the comps, except for EBITDA growth and margin. I believe the dip in EBITDA should only be temporary and will recover once inflation cools. In addition, FTDR also gained some traction with its dynamic pricing strategy, where it realized 11% price increase , which may also act as a tailwind for EBITDA growth.

{kind=link}

Created by Author

Valuation Summary & Target Price

Created by Author

I calculated the price target based on 1.45x F23E EV/Revenue and 11.5x F23E EV/EBITDA multiple. I believe FTDR should trade at a premium to the core comps with its compelling ratios and discount to the service comps considering the macro headwinds and the high execution risk of the Frontdoor apps. Therefore, I am initiating a price target of $36.6 based on the conservative public comp analysis.

However, I anticipate that a higher multiple will be assigned to FTDR once it demonstrates concrete signs of recovery in its real estate segment and gains momentum from the new Frontdoor apps. The DCF analysis incorporated these variables and resulted in a forecasted share price of $48.2.

Risks

Operational Risk

The risk of inflation poses significant challenges to FTDR's margins and operations, as observed by the decline in margins over the past two years. Inflationary pressures drive up the cost of raw materials and labor, impacting FTDR's cost structure. Higher input costs, such as those related to OEM parts used in repairs, can squeeze FTDR's profit margins. Additionally, increased labor costs and rising OPEX further strain margins. Inflation can also influence consumer behavior, potentially reducing demand for discretionary services like home warranties. To mitigate these risks, FTDR may need to negotiate favorable pricing agreements, optimize operations, and adjust pricing strategies accordingly.

Strategic Risk

FTDR is heavily investing in the development and marketing of the new Frontdoor brands. However, there is a level of uncertainty surrounding the success of this initiative, considering the challenging performance experienced by on-demand service providers like Angi in recent years. Despite FTDR's advantage of owning an extensive contractor network that can potentially achieve synergies with the new offering, the project remains exposed to high execution risk. However, it is worth noting that FTDR's core home service business provides a measure of downside protection to valuation in the event that the new initiative faces significant challenges or setbacks.

Conclusion

I am initiating a price target of $36.6 with a buy rating. Although the street consensus appears neutral on the name, I believe FTDR is showing signs of recovering with its renewal rate growth and three consecutive EPS beats despite the challenging macro environment. In addition, the stock was already penalized heavily, nearly halved from its 2021 high, which exhibited a compelling valuation for potential investors to consider. I believe the street price target of $30 might be underwhelming for FTDR as I am already seeing inflation cooling and some signs of resiliency in the real estate market. The street price target implied an FY23E EV/Revenue multiple of 1.4x and F23E EV/EBITDA multiple of 10.4x, which is even a discount to some comps with worse top-line growth prospects. I believe FTDR should at least be valued in-line with its core comps. Looking near-term ahead, I am seeing further upsides on the stock with the company eyeing more price increases in the Q1 presentation and launching the Frontdoor Premium app in June. In conclusion, FTDR remains a solid company with substantial competitive advantages built around its extensive scale and large base of renewals, which provide downside protection and potential for future upside growth.

For further details see:

Frontdoor: Improving Renewal Base With Upside From The New Frontdoor Brand