FTDR - Frontdoor: Overvalued With Poor Financials

2023-03-06 08:56:33 ET

Summary

- FTDR recently posted FY22 and Q4 FY22 results. Their income declined significantly, and revenue growth was flat.

- They are overvalued compared to industry standards.

- The stock is showing bearish signals.

- I assign a hold rating on FTDR stock.

Frontdoor ( FTDR ) offers home service plans in the U.S. their home services cover the replacement and repair of approximately 20 home systems and appliances like plumbing, refrigerators, ovens, spas and pumps, and air conditioning systems. They also provide pro-connect on-demand home services and Streem. It is a technological platform that aids home service professionals in correctly diagnosing problems and completing repairs by utilizing computer vision and augmented reality. They recently announced FY22 and Q4 FY22 results. In this thesis, I'll talk about its valuation and analyze its financial performance. In FY22, their income fell considerably while revenue growth remained flat. The revenue forecast also indicates that FY23's revenue increase will be flat. Therefore, I have rated FTDR as a hold because it might not provide returns to its investors.

Financial Analysis

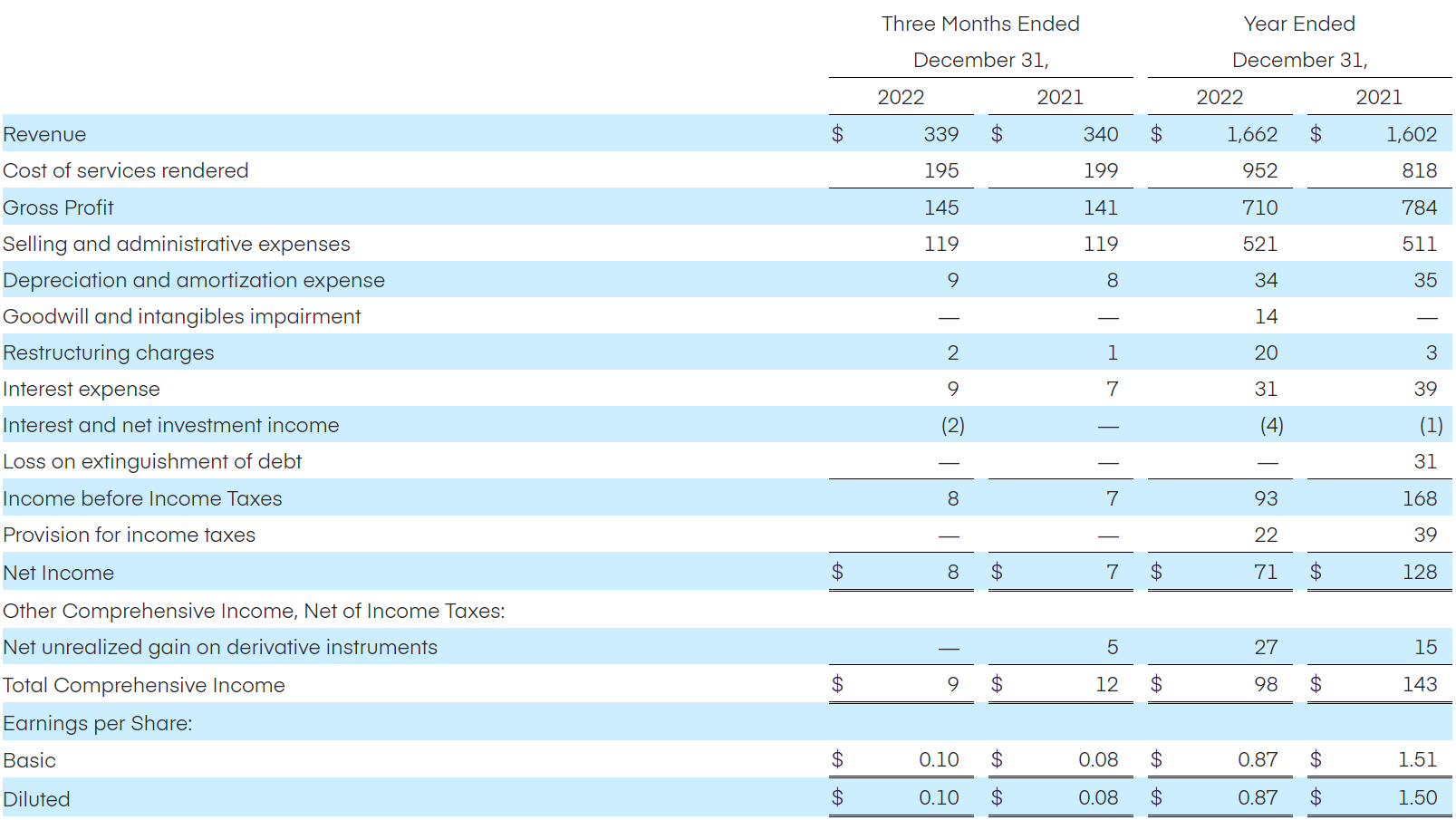

FTDR recently posted its FY22 and Q4 FY22 results . The revenue for FY22 was $1.6 billion, a slight increase of 3.7% compared to FY21. The net income for FY22 was $71 million, a decline of 44.5 % compared to FY21. I think there were a number of factors that contributed to the declining income and stagnant revenue growth. Their revenues and net income were significantly affected by high inflation, a drop in sales through their real estate channels, and challenging market conditions.

Additionally, their gross profit margin dropped from 49% in FY21 to 42.7% in FY22. Their financial performance in FY22 was, in my opinion, quite underwhelming. Both their net income and gross profit margins experienced significant declines, which is cause for worry.

{kind=link}

In comparison to Q4 FY21, there was no increase in revenue in Q4 FY22. The revenues matched Q4 FY21. The net income for Q4 FY22 was $8 million, which was $7 million in FY21. I think the decline in real estate revenue—which fell by 32% in Q4 FY22 compared to Q4 FY21—was the primary cause of the stagnant revenue and income. The drop-in home service plans, which resulted in a decrease in real estate revenue, was, in my opinion, caused by the challenging real estate sellers' market. In my opinion, the financial success of FTDR in FY22 was below average because of how much inflation affected its operations. Their sales barely increased, and their income fell sharply.

Technical Analysis

{kind=link}

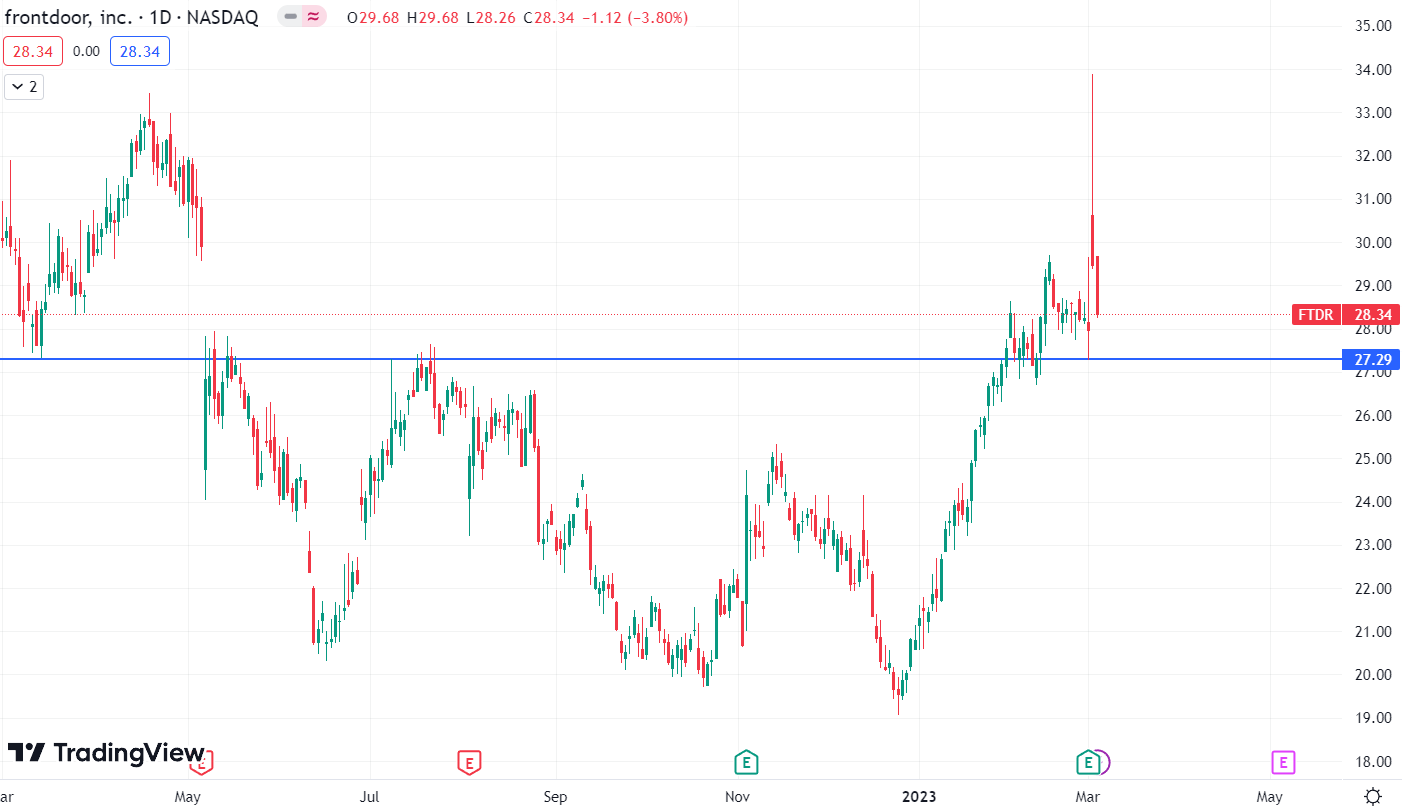

FTDR is trading at the level of $28. The stock has been attempting to break through the $27 level since May 2022, as can be seen, if we look at the daily time period. It made three attempts to break it but was unsuccessful. Finally, after ten months of consolidation, it broke the $27 record. But after bursting through the level, it produced two enormous red candles, suggesting that it might be a bull trap. I believe one should steer clear of this company because I believe a trend reversal from current levels may be imminent. It could enter a consolidation period once more and fall to a level of $23.

Should One Invest In FTDR?

{kind=link}

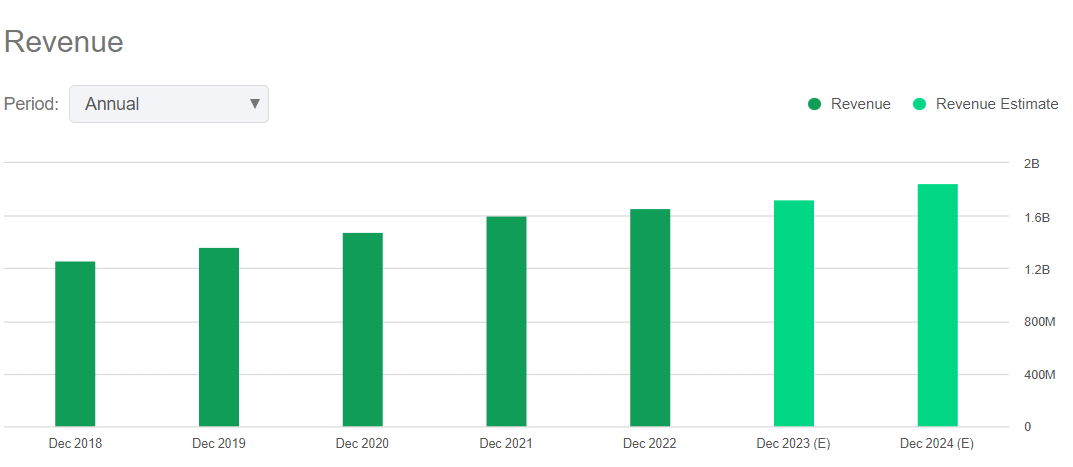

They had a terrible financial year, with almost no revenue increase and a sharp decline in income. Regarding FY23, the projected revenue is around $1.72 billion, a small increase of 3.6% from FY22. The management anticipates a slight revenue increase in FY23, and I believe they may have trouble hitting their revenue goals. I say this because I anticipate pressure on the real estate channel segment throughout FY23, and the management anticipates a 20% decline in real estate channel revenues as well as a decrease in home service plans. Additionally, I believe that the business will face pressure from a number of factors, including inflation, recessionary fears, and weak market conditions, and we could see its effects on the share price. Because of the many uncertainties and risks that this business may encounter in FY23, I think it is best to avoid purchasing its stock for now.

Now looking at the valuation part, I will use two valuation metrics to judge its valuation. The first is the P/E ratio. The P/E ratio is a method of determining a company's worth by dividing its stock price by its profits. They have a P/E ((FWD)) ratio of 21.74x compared to the sector ratio of 15.03x. This shows that they are overvalued. The second ratio is the Price / Sales ratio which demonstrates the price investors are ready to pay per dollar of stock sales. They have a Price / Sales ((FWD)) ratio of 1.34x compared to the sector ratio of 0.93x. After looking at both valuation metrics, I believe they are overvalued and have limited growth potential.

Risk

Tariff policies are constantly being evaluated and could alter. For instance, rising parts costs associated with the repair and replacement of home systems and appliances could increase as a result of blanket tariffs on imported steel and aluminum. This could adversely affect their business, financial position, results of operations, and cash flows. Additionally, new taxes and adjustments to American trade policy might provoke retaliation from the impacted nations, which might result in the imposition of tariffs on American products. The demand for its services could be materially and adversely affected, which would have a negative effect on its financial position.

Bottom Line

After analyzing all the parameters, I believe they are overvalued with limited growth potential. Their annual results were disappointing, showing a sharp drop in net income and stagnant revenue growth. The management’s FY23 revenue guidance also suggests stagnant revenue growth in FY23. In addition, the stock is also showing bearish signals. After considering all the factors, I suggest one should refrain from buying this stock for now. Hence I give FTDR a hold rating.

For further details see:

Frontdoor: Overvalued With Poor Financials