PARXF - Frontera Remains A Buy After Strong Results And Improved Outlook

2023-04-17 05:06:00 ET

Summary

- Heightened perception of risk associated with operating in Colombia weighing heavily on market value.

- Strong growth prospects including a transformational opportunity in offshore Guyana.

- Frontera remains heavily undervalued despite record 2022 results, growing production, and higher oil prices.

Canadian intermediate oil producer Frontera Energy (FECFF) (FEC:CA) remains unpopular with investors despite petroleum prices firming and the company's prime position in offshore Guyana. Frontera announced strong 2022 results including record fourth quarter 2022 net income and solid annual EBITDA growth. Despite that impressive performance Frontera's stock lost 3% over the last year. Recent geopolitical events in Colombia, where the driller's core producing assets are located, including tax hikes, the oil industry's deteriorating social license and heightened security risks are weighing on Frontera's market value. That negative impact is magnified by Frontera's disappointing 2023 guidance where earnings are expected to soften because of higher taxes in Colombia. Despite the gloomy 2023 forecast Frontera remains heavily undervalued, although the price target has been revised downward to reflect the negative fallout associated with those events.

Latest developments

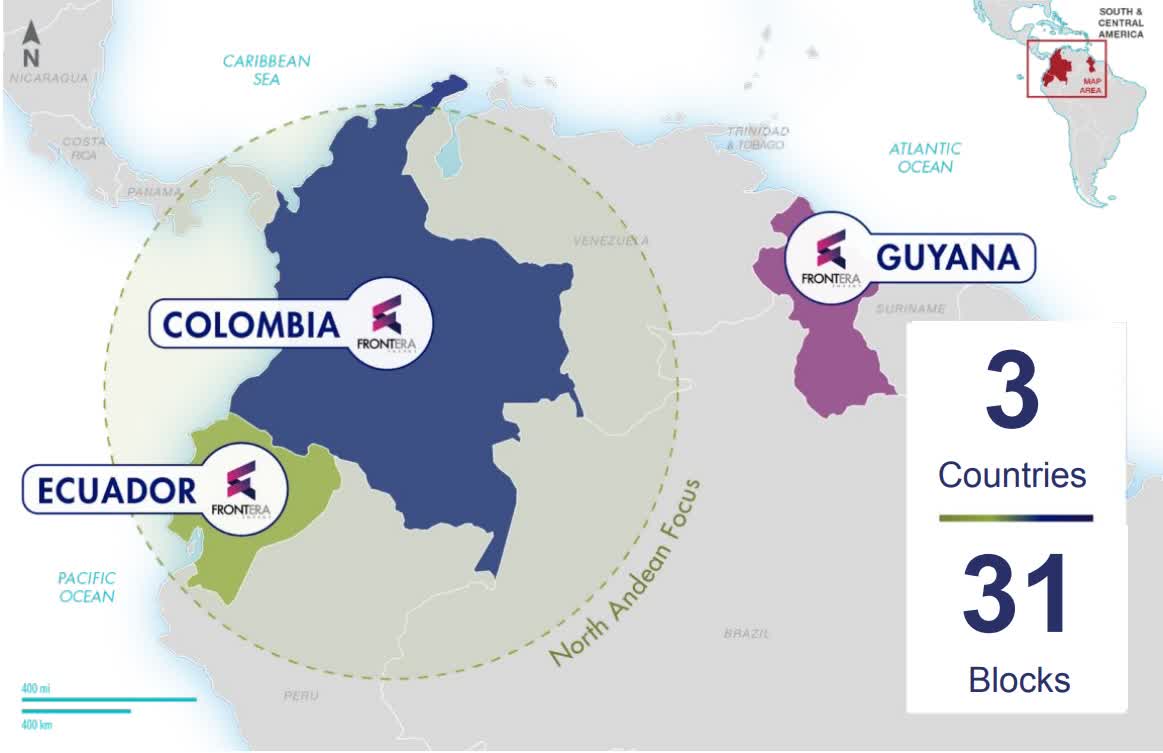

Frontera is Colombia's third largest oil producer after national oil company Ecopetrol ( EC ) and fellow Canadian driller Parex Resources (PARXF) (PXT:CA). The intermediate oil producer offers investors exposure to upstream assets in three South American countries; Colombia, Ecuador and Guyana.

Frontera Asset Map (Frontera Energy)

{kind=link}

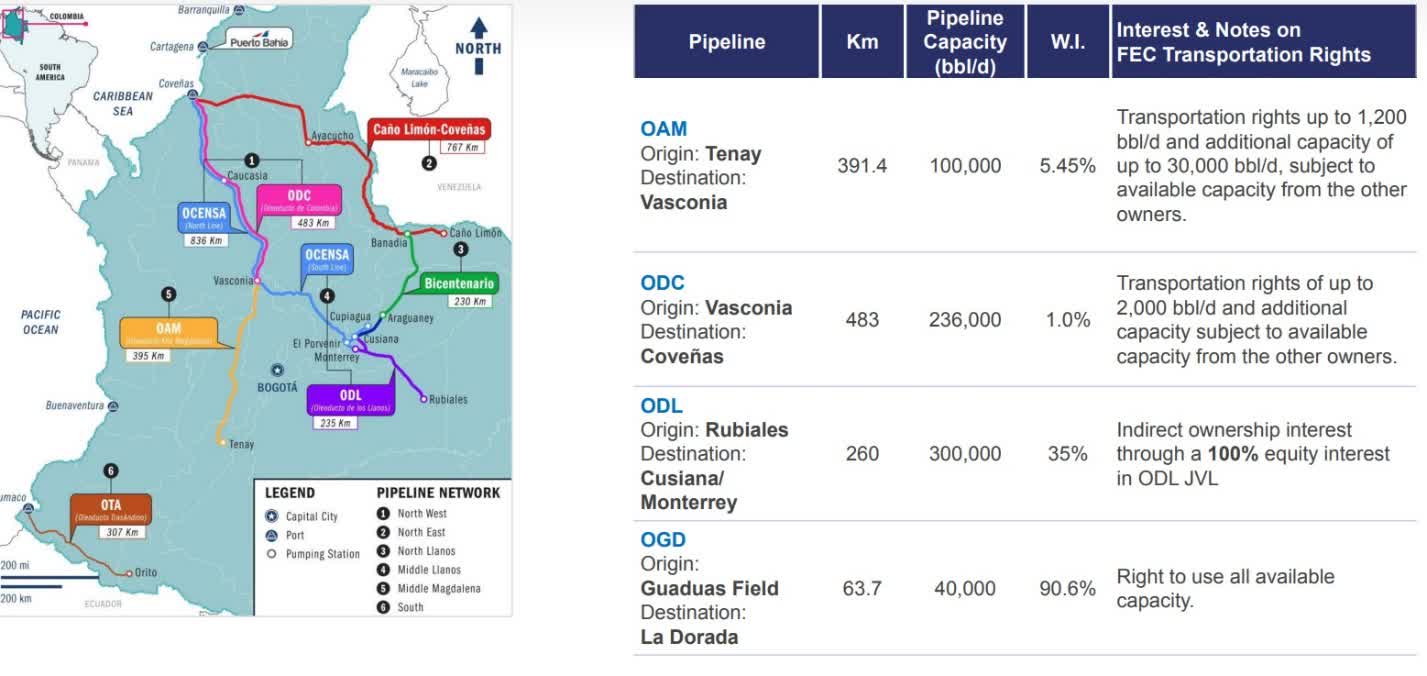

Aside from its upstream assets Frontera also owns interests in a range of industry infrastructure. During 2022, Frontera's Colombian midstream assets delivered segment income of $54.3 million, representing 8% of the driller's gross income for that year, compared to $77.8 million for the year prior. That year over year decline be blamed on weaker 2022 revenue combined with higher operating costs.

The key Colombian industry infrastructure assets owned by Frontera include four pipelines, which are the only cost effective means of transporting oil in the Andean country's rugged terrain.

Frontera Colombia Pipeline Assets (Frontera Energy)

{kind=link}

The most important pipeline asset being Frontera's 35% interest in the 300,000 barrel per day Oleoducto de los Llanos Orientales, or ODL for short, with the remaining 65% owned by state-controlled Ecopetrol. The 162-mile-long pipeline is a crucial transportation asset for Colombia's oil industry. It connects the Rubiales and Quifa oilfields in Meta Department to the Monterrey and Cuisana collection and storage facilities in Casanare Department from where the petroleum can be transported to the Caribbean port of Coveñas for shipment to international markets.

According to Colombia's oil industry regulator the National Hydrocarbon Agency , known by its Spanish initials ANH, the Rubiales field is Colombia's largest oilfield having pumped 37 million barrels of oil during 2022, while Quifa is the sixth largest producing 9.2 million barrels that year. The importance of those fields to Colombia's energy patch indicates that demand for utilization of the ODL pipeline remains strong ensuring consistent revenues for the pipeline's owners.

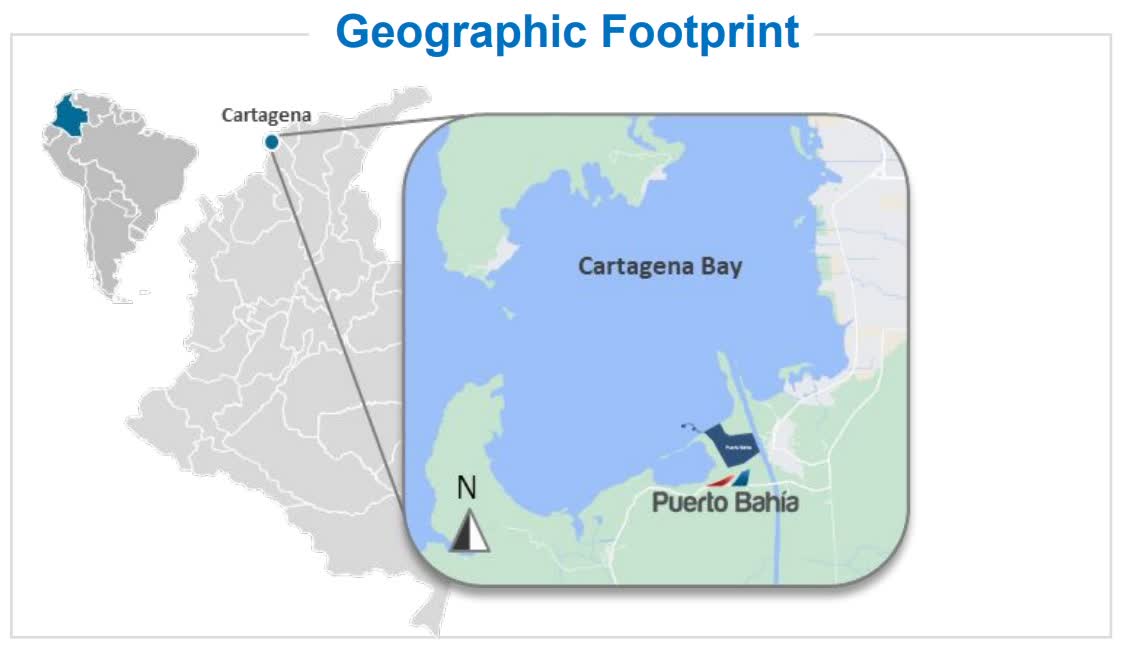

Frontera also owns 96.55% of the issued and outstanding shares for the Puerto Bahia port in Cartagena Colombia. It forms part of the complex that comprises the port of Cartagena de Indias, which is ranked as Colombia's busiest seaport and the country's main oil exporting facility.

Map of the port of Cartagena de Indias (Frontera Energy)

{kind=link}

Puerto Bahia is one of the few deep draft ports in Colombia with oil loading facilities making it a crucial piece of transportation infrastructure for Colombia's economically crucial oil industry. Those attributes will ensure that demand for utilization of Puerto Bahia remains high which coupled with Colombia's expanding oil production and manufacturing capabilities will drive higher revenues.

Solid 2022 performance

For the full year 2022, Frontera announced some impressive results including record fourth quarter net income of $197.8 million, although annual net income of $286.6 million was less than half of the $628 million reported a year earlier. It was a significant increase in taxes payable, $249.3 million compared to $1 million a year earlier, that was responsible for 2022 net income being significantly lower than 2021. Nonetheless, full year 2022 operating EBITDA rose significantly by 70% year over year to $641.9 million on the back of stronger production and higher oil prices.

Frontera's full year 2022 average daily production of 41,382 barrels of oil equivalent per day represented a 9% increase over 2021. Total hydrocarbon output was 94% weighted to oil with 52% comprised of heavy crude and 42% light oil. Frontera delivered an impressive netback of $59.78 per barrel, a solid 60% increase over the $37.26 per barrel netback reported for 2021. This is a solid netback for an intermediate upstream driller generating most of its revenue from sour light and heavy oil assets in Colombia.

Those solid numbers highlight that Frontera has recovered from the impact of the COVID-19 pandemic, is capable of growing production from its portfolio of quality onshore Colombian assets and is positioned to take advantage of higher oil prices.

Considerable growth ahead

A key reason for investing in Frontera is that the company, aside from holding a quality portfolio of onshore oil producing assets, possesses considerable growth potential which will boost reserves and production.

Offshore Guyana

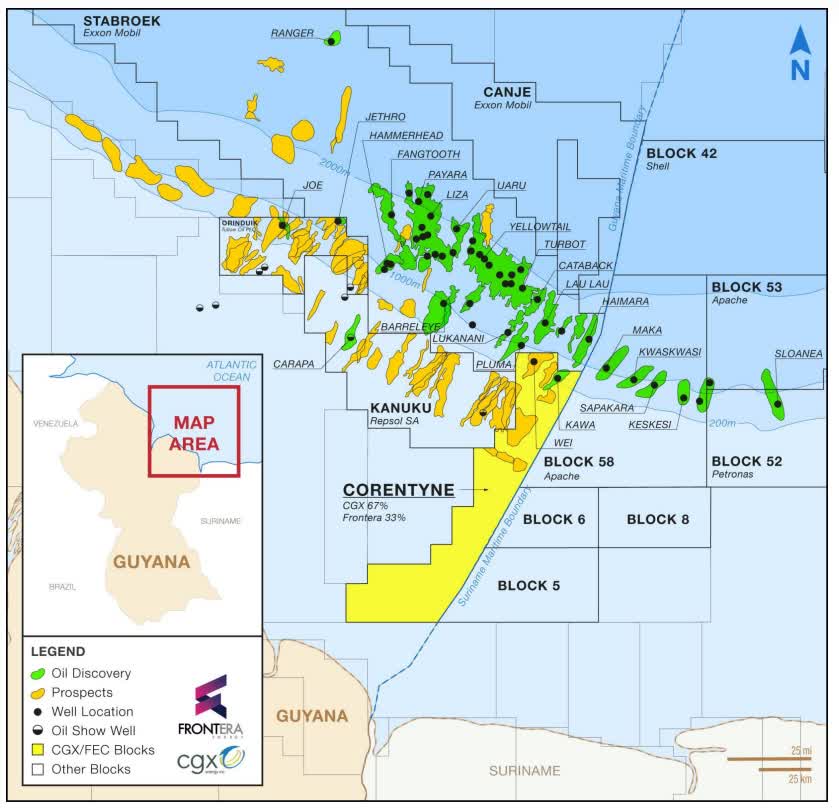

The main growth asset is Frontera's 68% working interest in the Corentyne Block offshore Guyana, where it owns nearly 77% of the operator CGX Energy ( CGXEF ) OYL:CA giving the company a consolidated interest of 92.63%. Frontera and CGX have already made one discovery in the northern area of the Corentyne Block with the Kawa-1 well which found 177 feet of hydrocarbon bearing reservoirs. According to CGX the geological characteristics are similar to discoveries made in the neighboring Stabroek Block in offshore Guyana and Block 58 offshore Suriname.

Offshore Guyana Map (Frontera Energy)

{kind=link}

The partners started drilling the Wei-1 wildcat well in January 2023 with it anticipated it will take up to five months to reach the target depth of 20,500 feet.

There is still considerable work to be completed on the Kawa-1 well to determine whether the discovery is commercially viable but that likely will not occur until further exploration wells are drilled to determine the Corentyne Block's oil potential. If CGX and Frontera choose to proceed with developing the Corentyne Block it could cost anywhere from $6 billion to $10 billion to bring it to first oil. Such an extensive capital investment will require a farm in agreement with a larger offshore oil company.

While the Corentyne Block on offshore Guyana provides a transformational opportunity for Frontera, it is the company's onshore Colombian and Ecuadorean assets which will drive future reserve and production growth.

Colombia and Ecuador exploration assets

Frontera has three exploration blocks in the Lower Magdalena Valley Basin VIM-1 with a 50% working interest, VIM-22 and VIM-46 all undergoing various levels of work. The most advanced is VIM-22 here Frontera is in the process of drilling three exploration wells Winer-1, Chimi-1 and Subara South-1. There are civil works underway on the VIM-1 Block and a seismic assessment needs to be undertaken on the VIM-46 Block. The VIM-1 Block, where fellow Canadian driller Parex holds the other 50% and is the operator, is currently pumping 1,280 barrels per day and will become a major contributor to Frontera's production as development work is completed.

Frontera also holds 100% interests and is the operator for two exploration blocks in the Llanos Basin; LLA-99, where seismic and environmental impact assessments need to be undertaken, and LLA-119 where civil works are being developed. Frontera estimates those Colombian properties offer prospective resources of 252 million to 503 million barrels of oil equivalent. The company continues to develop its core Colombian assets which are the Quifa, Guatiquia and CPE-6 Blocks

The driller owns interests in two exploration assets in Ecuador the Perico and Espejo Blocks. Three successful exploration wells were drilled on the Perico Block where Frontera is the operator and owns a 50% working interest with the remainder held by GeoPark ( GPRK ) where medium oil was discovered. There are two remaining exploration targets to be drilled with Frontera planning to drill a production well on the block during 2023. The Espejo Block, where Frontera owns a 50% interest and the remainder is held by the operator GeoPark, has three pending exploration targets to be drilled. Frontera estimates those two blocks contain prospective resources of at least 43 million barrels of oil equivalent.

In total, the company estimates its exploration activities across its Colombian and Ecuadorean blocks will add 59 million to 111 million barrels of oil equivalent to its proven and probable reserves. The exploration and development plans will lift production to over 50,000 barrels of oil equivalent daily by the end of 2024 and potentially nearly 80,000 barrels during 2026, giving earnings a solid lift.

Robust financial position

Frontera has a strong balance sheet with a well-laddered debt profile. The driller finished 2022 with $290 million in cash and equivalents with a further $88 million in accounts receivable and $75 million inventory, coming to a total of $453 million. This indicates Frontera has adequate cash to fund its 2023 capital expenditures and meet current debt repayments. There are no significant long-term debt payments due until December 2027 when the newly negotiated $120 million loan with Macquarie Group for the Puerto Bahia facility falls due. The strength of Frontera's balance sheet and ability to internally fund annual capital expenditures including those directed to exploration and development drilling mitigates the risk associated with investing in an intermediate upstream oil producer.

Finding what the company is worth

In my December 2022 article , I calculated that Frontera has an indicative fair-value of $16.78 to $23.59 per share using the after-tax net present value, or NPV, of the driller's proven and probable reserves. Since that article Frontera has revised its oil reserves causing the after-tax NPV of the reserves and the company's after-tax net asset value, or NAV, to change. According to Frontera's January 2023 announcement, net proved reserves of at the end of 2022 were 98.6 million barrels a 10% decrease compared to 2021, while combined net proved and probable reserves of 156.8 million barrels were 6% lower.

Lower 1P and 2P reserves will typically, that will impact the after-tax NPV causing the company's after-tax NAV per share to fall. In the case of Frontera's 2022 reserves assessment the after-tax NPV rose because a higher 13-year forecast Brent price of $87.38 per barrel, compared to $76.46 for the 2021 reserves assessment, was used to calculate the after-tax NPV. Using Frontera's 2022 1P after-tax NPV-10 of $1.66 billion, which includes a 10% discount, the company has an indicative fair-value of $17.34 per share as per the chart below.

Financial table (Author and company filings)

That amount is 70% higher than the value of Frontera's U.S. pink sheets stock indicating there is considerable upside available to investors with a solid margin of safety.

Frontera's indicative value per share is even higher when the after-tax 2P NPV-10 of $2.42 billion is used to calculate its after-tax 2P NAV per share in accordance with industry methodology. This gives the driller a NAV of $26.15 per share as per the chart below.

Financial table (Author)

That is 11% greater than the 2P after-tax NAV that I calculated in my December 2022 article and 2.5 times greater than Frontera's U.S. pink sheets value at the time of writing. This number further confirms that the driller is heavily undervalued offering significant upside and a margin of safety for investors.

Company specific risks

Aside from the standard risks associated with investing in a small-cap intermediate oil producer, notably commodity price risk, there are specific hazards that can impact Frontera's operations and market value. These are associated with the company's core producing assets located in Colombia which has a long history of violence perpetrated by illegal armed groups and instability. Those risks have not changed significantly since my December 2022 article so you can review them through the link to that article , although I have provided an updated summary below.

Regulatory risk and tax hikes

Colombia's first left-wing president Gustavo Petro committed to cease awarding new hydrocarbon exploration licenses . While there are some indications that he may not proceed with that plan Minister of Mines and Energy Irene Velez at the Davos Economic Forum committed Colombia to ending exploration contracts and the energy transition. While that will have an outsized impact on Colombia's oil dependent economy it will likely have little to no negative effect on Frontera and the company's peers. The Petro Administration has publicly committed to honoring all existing hydrocarbon sector contracts.

The November 2022 tax hikes will have a marked impact on oil producers in Colombia. The two key changes which affect oil companies are firstly the removal of royalty payments as an income tax deduction and secondly an additional tax levy is payable when the international Brent price exceeds a certain level. An additional 5% tax is payable when the Brent price ranges from $67.30 to $75 per barrel, which rises to 10% at $75 to $82.20 per barrel and then an additional 15% is payable when prices exceed $82.20 a barrel. That additional levy forms a crucial part of the tax package aimed at generating an additional $4 billion in fiscal revenue which will bring a spiraling budget deficit under control.

Heightened security risk

Colombia's oil industry has been grappling with a deteriorating security environment and social license for some years. Pipeline bombings, oil theft and attacks on oilfields and related facilities impact production while causing operational costs to rise, especially with damaged pipelines forces to shutter for repairs. The security risks are further exacerbated by a deteriorating social license which is responsible for regular anti-oil industry protests and community blockades of facilities.

The latest attack was on the 220,000 barrel per day Caño Limon Coveñas pipeline which connects the Caño Limon oilfield in the Department of Arauca to the port city of Coveñas on the Caribbean coast. The pipeline has long been a target for frequent acts of sabotage, bombings and petroleum theft by leftist guerillas. The latest event was blamed on the National Liberation Army (ELN - Spanish initials) and saw the pipeline ruptured by explosives. This is the seventh such attack since the start of 2023. The 190,000 barrel per day TransAndino pipeline (OTA - Spanish initials) connecting the Putumayo Basin to the Pacific port of Tumaco is also frequently sabotaged and suffers from the regular application of illicit valve to steal petroleum.

Due to harsh terrain and a lack of other transportation infrastructure pipelines are the only reliable and cost effective means of transporting large volumes of petroleum in Colombia. When pipelines are attacked the operator CENIT, a subsidiary of Ecopetrol, is forced to shutter operations while repairs are made meaning drillers are forced to store the petroleum produced on site and/or use more costly road transportation to ship it to market. That causes production outages and operating costs to rise impacting revenues and profitability.

Growing dissent among communities in the municipalities where Colombia's oil industry operates is also impacting industry operations. Violent protests in the department of Caqueta against Emerald Energy a subsidiary of China state controlled Sinochem left one civilian and a police officer dead. At least 79 police officers and nine oil workers were detained by the protestors only to be later released. Protests erupted over allegations Emerald failed to meet the terms agreed with local communities over the construction of road infrastructure and financial restitution. There are various claims, which are difficult to substantiate, that the local community was not appropriately consulted when the project was approved in 2012, as is their legal right, and that Emerald failed to honor its promises. Those types of complaints from communities in the regions where Colombia's oil industry operates are becoming commonplace.

There is also growing community dissatisfaction with the growing amount of environmental damage caused by frequent oil spills and other emissions from industry operations. Colombian petroleum industry thinktank Crudo Transparente claims that there were 71 oil spills and other environmentally damaging incidents between 2017 and 2022. The worst event occurred in 2018 threatening waterways near Barrancabermeia, the city at the heart of Colombia's energy patch. Local communities claim the spill was inadequately cleaned-up and that petroleum is still present in river sediment. This is a common theme in the Putumayo Basin, Colombia's second most important sedimentary basin, which is situated in the Andean country's ecologically sensitive Amazon region.

Conclusion

Frontera is well-positioned to continue unlocking value for shareholders. The driller's working interest in the Corentyne Block offshore Guyana offers a high-risk transformational opportunity. Frontera also has a solid drilling inventory across a range of onshore blocks in Colombia in Ecuador which will drive 2P reserve expansion and higher production. Those opportunities and the potential for considerable success are significant positive catalysts that will, if successful, give Frontera's market value a substantial boost. A considerable portion of the risk associated with investing in a small-cap intermediate oil producer is mitigated by Frontera's solid balance sheet. It is an overblown perceived degree of risk associated with Colombia, and to a lesser extent Ecuador, which is weighing on Frontera's market value. The after-tax NAV for Frontera's 2P reserves of $26.15 is 2.5 times its market price indicating that not only is there substantial upside available but a large margin of safety. When that is combined with the improved outlook for oil, which rallied strongly on the back of OPEC Plus' surprise production cut, Frontera's share price is poised to pop.

NB: Frontera is a U.S. pink sheets stock with its primary listing on the TSX where it has an average daily trading volume of 81,135 shares.

For further details see:

Frontera Remains A Buy After Strong Results And Improved Outlook