FRO - Frontline: Aggressively Buying Cash Flow In A Tight Tanker Market

2023-11-01 16:29:03 ET

Summary

- Frontline plc recently acquired 24 VLCCs from Euronav in a complex deal, increasing its fleet capacity by 57%.

- The acquired vessels are young and eco-friendly, with 9 out of 24 equipped with scrubbers.

- Frontline's earnings and free cash flow per share are expected to be highly accretive, but the company's success is dependent on VLCC rates and market conditions.

Frontline plc ( FRO ) recently acquired 24 VLCCs (very large crude carriers) from Euronav ( EURN ) in a complex deal with Compagnie Maritime Belge that also buys Frontline's 26% stake in Euronav at $18.43/share. CMB will then bid for the Euronav shares at the same price (a mandatory result from the stake sale). Frontline has said the deal should be highly accretive to earnings and free cash flow ("FCF") per share.

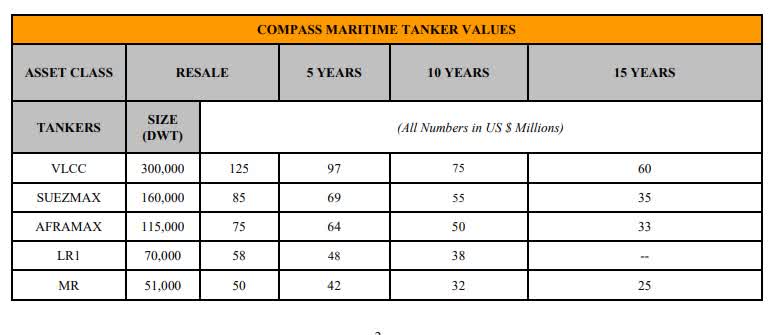

That's easy enough to believe (if VLCC rates hold up reasonably well) as Frontline is financing most of it with debt. It is taking its total fleet from 65 vessels to 89. However, in terms of deadweight tonnage, the company increases its capacity by 57%. In addition, most of the vessels are fairly young, with an average age of 5.3 years. They are all eco vessels, and 9 out of 24 are outfitted with scrubbers. What scrubbers are worth differs from time to time. I think the premium vessels earned with these are relatively muted this year. But from time to time, these vessels earn a significant premium. Europe introduces new environmental regulations in '24, which may or may not give the scrubber spread a boost. At a high level, the transaction appears to be executed roughly at fair value if I go by recent Compass Maritime VLCC values :

{kind=link}

But Frontline seems to have acquired slightly higher quality vessels that are worth more than the baseline value. Offshore energy also just wrote:

The very large crude carrier ((VLCC)) sector is in a unique position with a large portion of its fleet, around 30%, expected to struggle to meet energy efficiency regulations, particularly the Energy Efficiency Existing Ship Index ((EEXI)) and the Carbon Intensity Indicator ((CII)).

What is more, 14% of the VLCC ships are older than 20 years, and 30% of the VLCC fleet is older than 15 years, the highest fleet age since 2001. These ships are likely to become recycling candidates in the upcoming period due to their inefficiency.

The tanker industry is a boom-and-bust one. Especially VLCC's can earn enormous amounts in good times but go through scary slumps when the market is bad. Last quarter, the company earned ~$1 per share, and that's before this latest expansion significantly expanded its fleet.

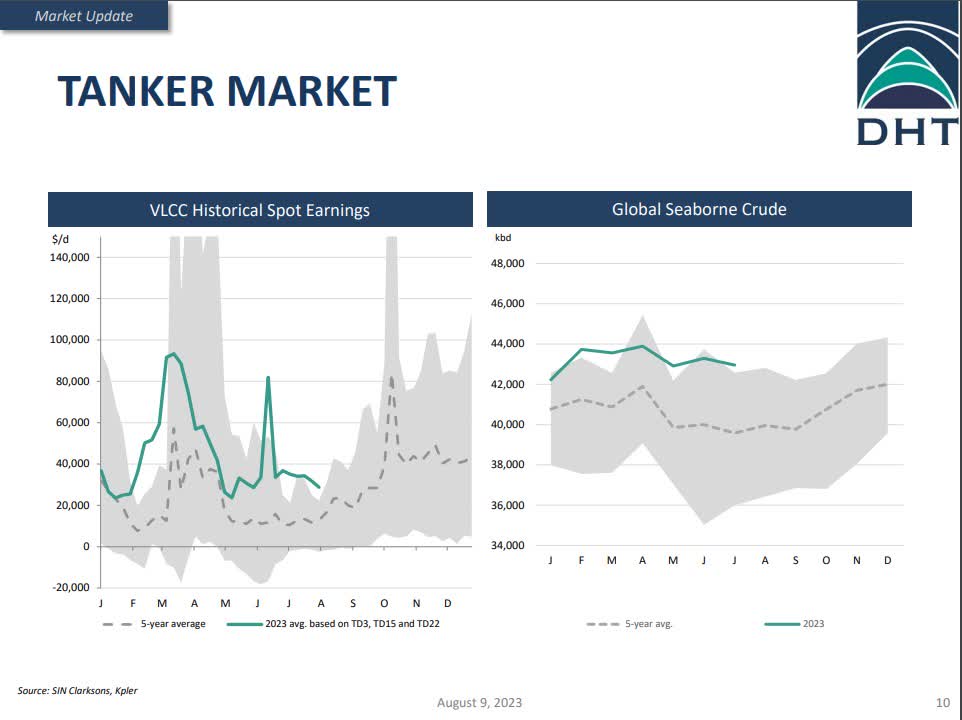

This is exactly when I want to be careful owning a tanker company, because annualized this looks like $4 per share. Indicating the company trades at 5x earnings. The forward yield looks like it is nearly 15% at this rate. All before the latest accretive deal. But earnings are exceptionally strong compared to a 5-year average (per a competitor's presentation ):

{kind=link}

When rates go down, due to operating leverage, the earnings are strongly affected.

Here's what the CEO Barstadt said on the recent earnings call :

In the second quarter, we had a very untypical spike for VLCC and Suezmax towards the end. And this puts us in a position to make some extra cash and also to carry some value into the third quarter. Most interestingly, this spike was caused by minor weather delays, telling a tail of how narrowly balanced our market is. The macroeconomical headwinds seem to have a very-muted impact on our little part of the global macro puzzle, and we'll get to that later in the presentation.

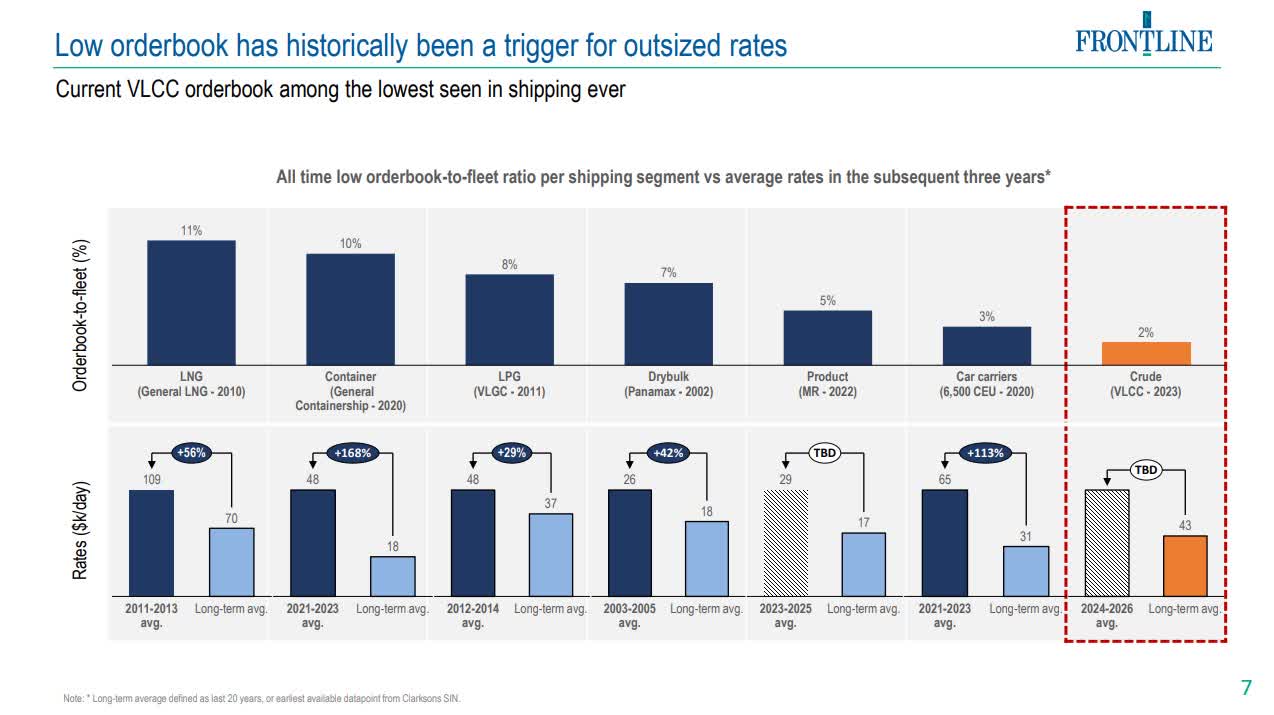

He's basically saying they were overearning indicating this kind of yield isn't sustainable. At the same time, I'll get into this, the fact that the market is so tight could indicate there's more to come. In the deal presentation Frontline highlighted the VLCC orderbook. It's very low:

{kind=link}

I checked what other VLCC operators are saying and they're basically mirroring the idea that very few VLCC's are entering the market until 26', the current fleet is old and a large slice isn't so eco-friendly .

Operators seem a bit perplexed at the low order book given the current demand for VLCC's and outlook. I've noticed a trend across industries that operators seem to underestimate (in my humble outside opinion) the effect of higher interest costs on the desirability to invest in machinery, inventory or in this case carrying capacity. Even if it is still economically feasible, the risk/reward doesn't always make as much sense anymore. Especially with shipping and large projects that could be a concern for financiers. The yield on a 20-year treasury is 5.209%. I'd want to make quite a lot more lending out money to finance a newbuild.

The Ukraine-Russia conflict doesn't look like it will end this year. Winter is coming, which will shut down fighting and there will be at least another 9 months of capacity disruptions.

Even if rates go down quickly (and the near-term prospects don't seem to indicate that) the firm has quite a few ships that are under longer-term contracts:

We have secured quite firm numbers as we progress into Q3, with 74% of our VLCC days booked at $53,200 per day; 67% of our Suezmax days fixed at $48,800 per day; and 57% of our LR2/Afra days at $40,500 per day. And again, to remind you, all these numbers are on a load-to-discharge basis, and they will be affected by the amount of ballast days that we end up having towards the end of Q3.

Here's what they said on the call about forward free cash flow:

If we assume VLCC TCE rates of $75,000 per day at 5.5 year historic spread to VLCC for Suezmax and LR2 tankers, the annual free cash flow potential is $1.4 billion or $6.34 per share, which translates into a free cash flow yield of 36%.

Again, that's before acquiring another 24 tankers. The company would be very lucky to hit it big like that. It's not my expectation. But then again, TradeWinds reported rates jumped to $64.600 per day. Note they could go either way, and rates are notoriously volatile.

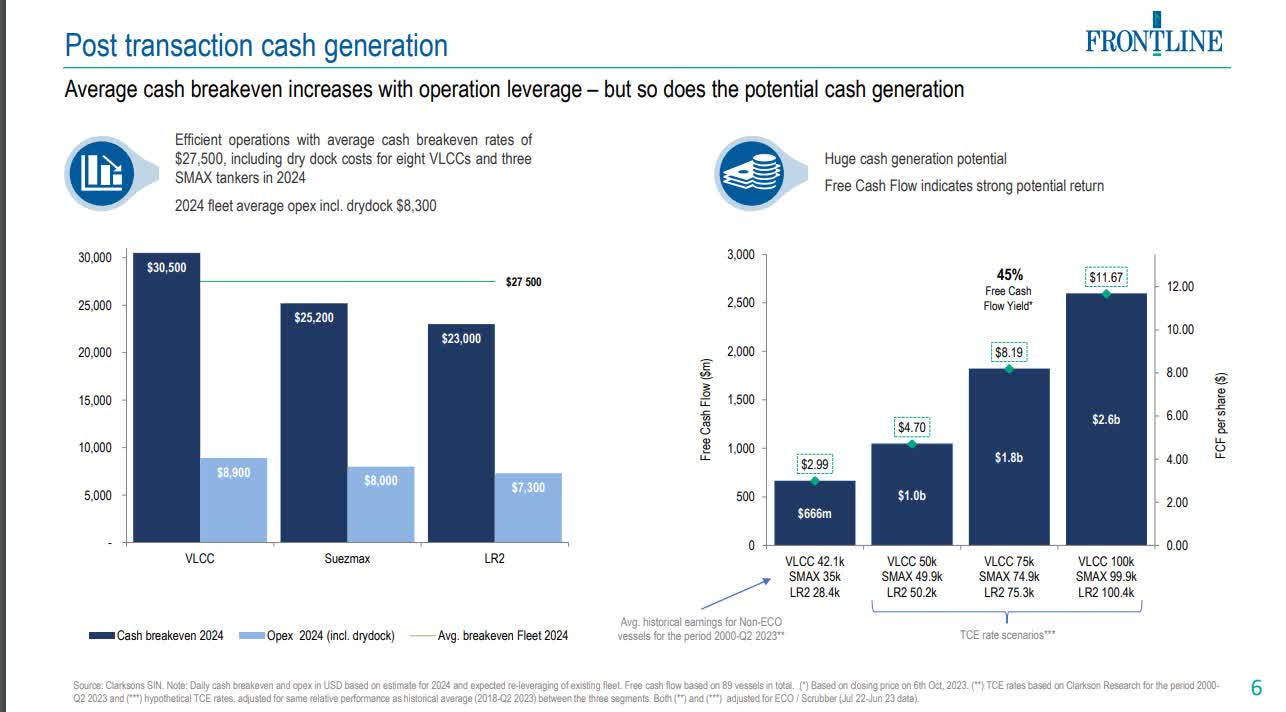

The deal presentation had a slide where the company modeled the free cash flow capacity post-deal. It is losing Euronav dividends but didn't dilute equity and found reasonable financing. At current rates of around $60k the company would generate somewhere in the $5.8-$6.5 of FCF per share. With rates at $40, the company would still be generating $3 in FCF per share.

{kind=link}

I pulled the Seeking Alpha valuation metrics, and Frontline trades very much in line with other tanker companies. Maybe slightly rich based on pre-deal numbers:

Valuation metrics tanker sector (Seeking Alpha)

If the deal closes and tanker rates are still $50k+, I can easily see Frontline trade towards $30 per share while paying out royal dividends. The caveat is that this deal will take total debt to around $4 billion. An amount that seems very manageable as long as rates are $50k+ which translates into a $1 billion+ of FCF. If rates start dropping below $50k things look increasingly uncomfortable. Especially, as contracts would roll off.

Given where rates are now, the risk decreases substantially with every quarter as Frontline plc rebuilds a cash hoard and/or pays down debt to make the transaction more manageable. Everything taken together, it seems like it's a great time to be long Frontline. If the VLCC market turns quickly the share price could take a spectacular dive though.

For further details see:

Frontline: Aggressively Buying Cash Flow In A Tight Tanker Market