FRO - Frontline: Industrial Demand Confirms The Potential Upside

2023-12-06 05:43:38 ET

Summary

- Frontline reported a revenue of $377.08 million, down 1.33% YoY and 26% QoQ compared to $382.18 million in Q3FY22 and $512.8 million in Q2FY23, respectively.

- The company has recently expanded its fleet by acquiring 24 VLCCs, positioning it to cater to the growing demand in the crude oil industry.

- FRO’s forward P/E ratio of 7.12x is 26.4% lower than its sector median P/E ratio of 9.70x, which indicates the company is undervalued.

- FRO stock is undervalued and has the potential for a 34.19% growth from current price levels.

Investment Thesis

Frontline plc ( FRO ) is an international shipping company that ships refined products and crude oil. The company's performance is negatively affected in the third quarter due to the macroeconomic pressures and geopolitical issues. I believe it can improve its performance in the coming quarters as it has recently expanded its fleet.

About FRO

FRO is an international shipping company that owns and manages oil and product tankers. The company offers seaborne transportation of refined products and crude oil. It mainly serves major oil trading businesses and large oil firms. The company conducts its business in one reportable segment: tankers. Crude oil and product vessels are included in this category. FRO provides time & bareboat and voyage charter contracts under which the company performs transportation services. The company generates 94.1% of its revenue from voyage charter contracts while time charter contracts represent 5.02% of the company’s annual revenue. The remaining 0.88% revenue of the company is administrative income which it earns from fees charged for new building supervision and technical & commercial management of vessels. The firm’s fleet comprised 70 vessels with an aggregate capacity of 13.1 million DWT.

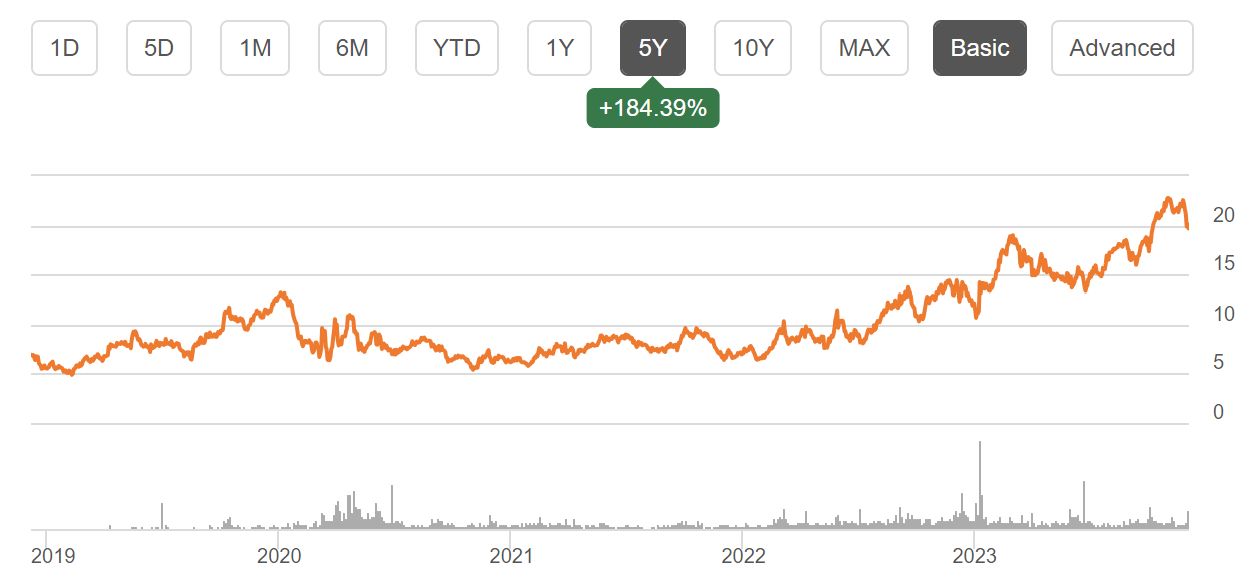

FRO's Share Price History (Seeking Alpha)

{kind=link}

The company’s share price has experienced 184.39% growth in the last 5 years. The share price increase in last two years is a significant portion of the company's 5-year share price growth. I will discuss the reasons behind this humongous growth in last 2 years in the next section.

Financials

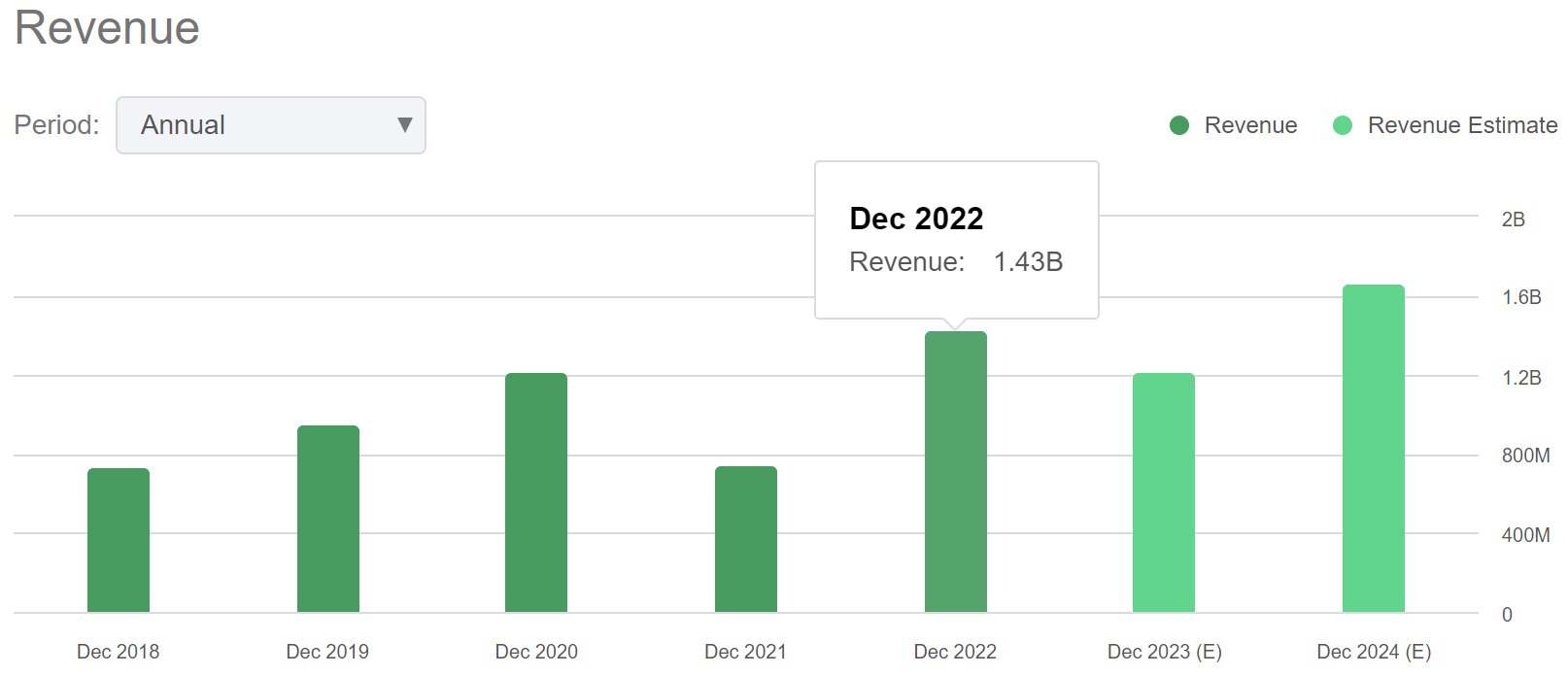

Revenue Trend of FRO (Seeking Alpha)

{kind=link}

FRO has experienced significant revenue growth in FY2022. The company’s revenue in FY2022 was $1.43 billion which is 90.82% YoY growth compared to $749.38 million in FY2021. This revenue growth was mainly influenced by the rise in domestic demand and time charter equivalent earnings as a result of higher TCE rates. The company maintained a similar level of time charter earnings and experienced all time high imports from China in Q1FY23. It has also experienced higher weighted average market earnings which has helped the company to achieve revenue of $497.3 million (6.2% QoQ decline) in Q1FY23. The company continued to experience higher TCEs and supportive demand from Asia which has helped FRO to achieve revenue of $512.8 million (3.12% QoQ increase) in Q2FY23. The revenue growth in Q2FY23 was partly offset by rising supply from new competitors.

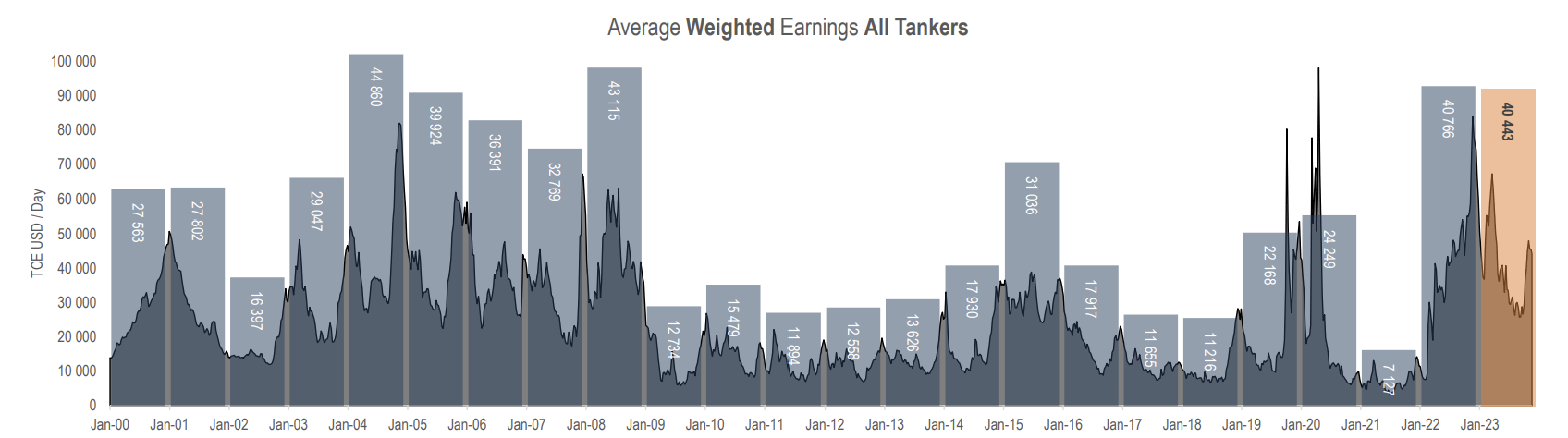

Average Weighted Earnings All Tankers (Investor Presentation: Slide No.14)

{kind=link}

The crude oil market experienced high volatility as a result of geopolitical tensions. The shift in prices and demand led to a disruption in the industry. However, the current as well as the long-term growth factors are highly positive. As per the World Oil Outlook 2023, the global energy demand is anticipated to rise by 23% up to 2045, out of which global oil demand can soar by 17%. Iran, Russia, and Venezuela are the growing and resilient exporters of crude oil. Venezuela projects a 300kpd short-term boost in exports to reach around ~6-700kbd yearly. The US exports are also on the rise and reaching historic highs. In addition, the refinery investments by 2045 are expected to significantly rise especially in Asia-Pacific and China which can help the industry to grow and increase the need for transportation for crude oil and refinery products. After considering above factors, I believe these positive industry dynamics have created high opportunities for the shipping industry participants. Identifying these scenarios, the company has signed an agreement with Euronav to acquire 24 VLCCs for transaction cost of $2.35 billion. Most of the vessels are anticipated to be delivered in 2023's fourth quarter, with the remaining vessels coming by in 2024's first quarter. These VLCCs will have average age of up to 5.3 years. As per my analysis, this acquisition can act as catalyst to boost the company’s growth as it can help it cater to rapidly growing industry demand by enabling it to transport increased quantities of refined products and crude oil. The continued growth of the company despite the adverse macroeconomic conditions is reflected in its Q3FY23 financial results.

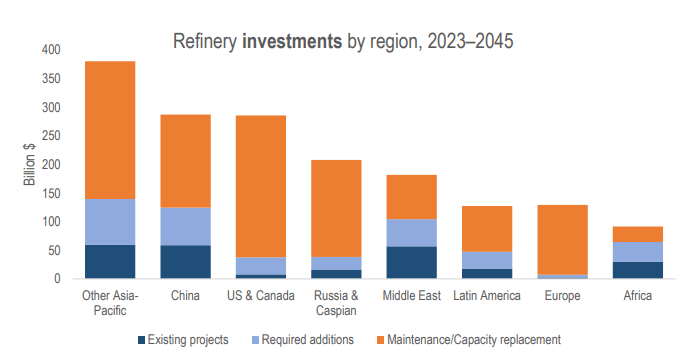

Refinery Investments by Region (Investor Presentation: Slide No: 11)

{kind=link}

The company has reported its quarterly results . It reported a revenue of $377.08 million, down 1.33% YoY and 26% QoQ compared to $382.18 million in Q3FY22 and $512.8 million in Q2FY23, respectively. This growth was mainly resisted due to adverse macroeconomic conditions, low TCEs, and geopolitical issues. The company has missed the market’s revenue consensus by $16.76 million or 6.74%. The total operating expenses stood at $262.73 million.

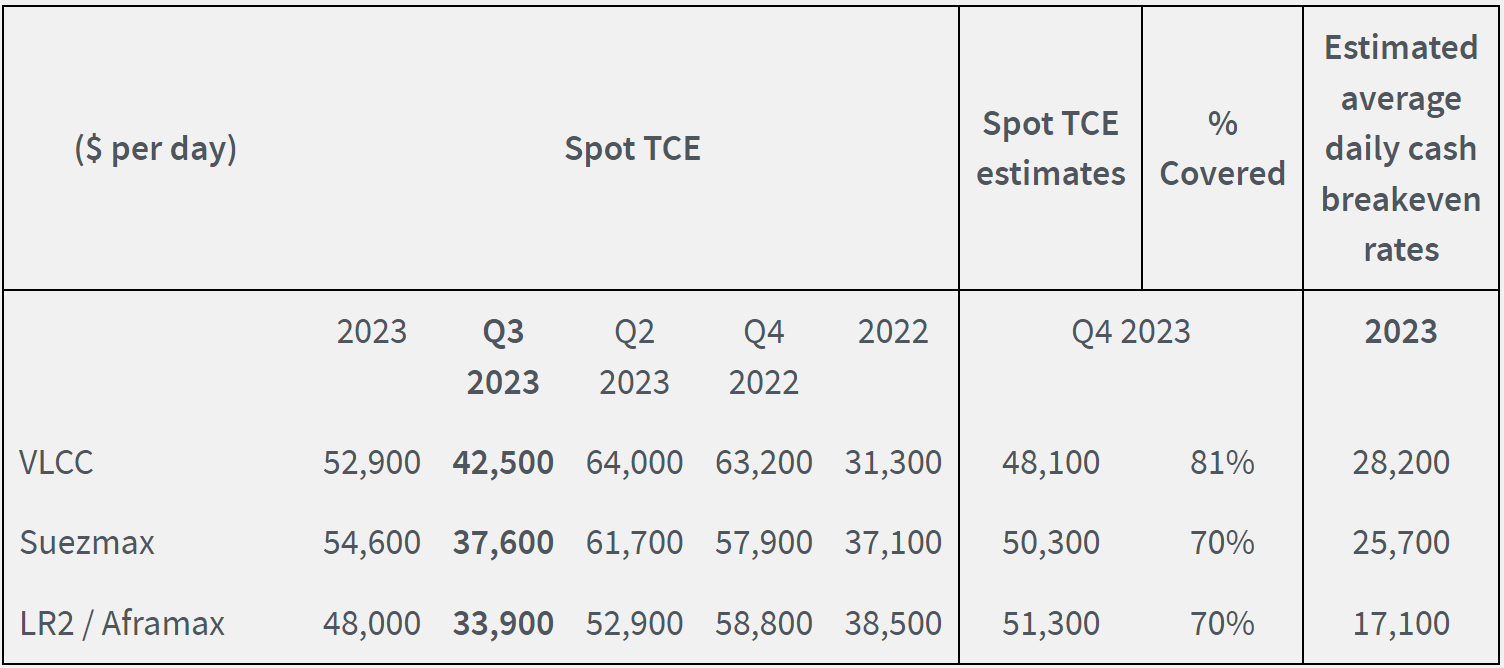

Spot TCE Rates of FRO (Press Release of FRO)

{kind=link}

Net income declined by 31.01% YoY from $156.44 million to $107.74 million. The primary driver of this decline is lower TCE rates which is partly offset by variations in other sources of income and outlays. The decline in net income has resulted in a diluted EPS of $0.48 which is $0.02 or 4% below the market’s EPS expectations. FRO reported $285.38 million in liquidity and adjusted EBITDA stood at $173.03 million. The loan facility with an approximate value of $91 million that was originally scheduled to mature in Q1–24 was refinanced in November 2023. The senior unsecured revolving credit facility, with an approximate value of $75.3 million, was extended to Q1–26 in October 2023.

For the company, the third quarter of the year turned out to be a shoulder quarter. Owners withdrew from the deal when the Russian benchmark crude price solidified its position above the price cap, increasing the non-Russian fleet's capacity. However, recently the demand picked up in the northern hemisphere, resulting from normal seasonality return. It is returning to a fairly normalized market where VLCCs lead in profitability thanks to robust US exports and continued strong Asian imports. The firm’s long-term growth appears to be positive as it has increased fleet capacity which can help it capture the growing demand in the long term and increase its profit margins.

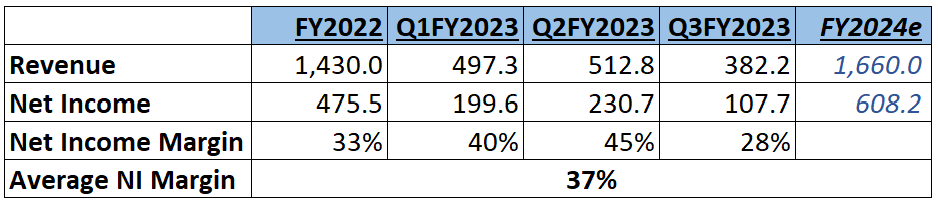

The company's VLCC capacity has almost doubled with latest acquisition. According to McQuilling Services , due to development on supply-side and rising demand in Asia can help the tankers company to experience a higher TCE almost on same level of FY2022 and FY2023. It is safer to say that the rising fleet capacity and higher TCEs can help FRO to exceed the FY2022 revenue in FY2024. Therefore, I am predicting it to be $1.66 billion . Looking at the Q3FY23 result, increasing demand, and the company's double VLCC fleet capacity (compared to before acquisition VLCC capacity), the company can easily exceed FY2022 revenue in FY2024. Since the economic environment and industry demand may be comparable to those of FY2022 and the previous three quarters, I am only taking into account the net income margin of these periods. The average net income margin is 37%. The company can maintain a net income margin of 37% in FY2024 with help of rising industry demand and capacity. The rising demand can also push TCE upwards which can help FRO to maintain the net income margin in the coming period. FRO has proven itself as most energy efficient fleets with 91% ECO vessels and 64% scrubber installed. Therefore, I am predicting FRO can maintain net income margin of 37% in FY2024’s which gives the EPS estimate of $2.73.

Calculation of Average Net Income Margin (Value Quest)

{kind=link}

What is the Main Risk Faced by FRO?

In the shipping industry, charter rates are extremely volatile and prone to cyclical fluctuations. Shifts in the demand for crude oil and refined products transported globally by water, as well as variations in the supply and demand of vessel capabilities, all influence changes in charter pricing. The company is unable to control the nature, pace, direction, and severity of changes in industrial conditions, and it is difficult for it to regulate every aspect that impacts vessel supply and demand. Most of its vessels are chartered on the spot market and time charter, which is cyclical. If the charter rates decrease it could negatively impact the asset values of the company and can further reduce its profitability and cash flows.

Valuation

The global oil industry is anticipated to grow by significant levels. I believe the firm is strongly positioned to capture the growing demand in the market as it has recently acquired 24 VLCCs which can help it to increase its market share and transport more quantities of crude oil by utilizing its increased fleet. Considering all these factors and the EPS estimate calculation in finance section of this report, I am predicting an EPS of $2.73 for FY2024 which gives the forward P/E ratio of 7.12x. FRO’s forward P/E ratio of 7.12x is 26.4% lower than its sector median P/E ratio of 9.70x, which indicates the company is undervalued. The company's primary competitors are Equitrans Midstream ( ETRN ), Plains GP Holdings ( PAGP ), DHT Holdings ( DHT ), International Seaways ( INSW ), and Scorpio Tankers ( STNG ).

{kind=link}

We can observe in the above chart that the company trading at discount compared to its peers despite the efficient fleet and latest acquisition additional fleets. Because of favorable industry demand and FRO’s alignment with fleet expansion, I think it has the potential to grow in the upcoming quarters and trade at its industry average P/E ratio. Therefore, I estimate the company may trade at a P/E ratio of 9.56x in coming period, resulting in target price of $26.1, a potential upside of 34.19% from the present share price of $19.45.

Conclusion

The company’s recent financials were impacted by macroeconomic pressures and geopolitical tensions, however, the environment is improving steadily. The crude oil industry has a positive long-term prospect and I believe the company is strongly positioned to cater to the additional demand as it has recently acquired 24 VLCCs which can facilitate it to transport additional crude oil and increase its profitability. Cyclicity can impact its profit margins. The stock is currently undervalued and we can expect a healthy 34.19% growth from the current price levels as a result of rising industry demand. Considering all these factors, I assign a buy rating to FRO stock.

For further details see:

Frontline: Industrial Demand Confirms The Potential Upside