FRO - Frontline Is A Solid Buy Despite Canceled Merger With Euronav

2024-01-18 23:56:26 ET

Summary

- Frontline plc is a global leader in seaborne transportation of crude oil and refined products, demonstrating adaptability and resilience in a volatile sector.

- The company has a solid financial base, with $715 million in cash reserves, and has shown prudence in not fully hedging its positions, allowing for potential market recoveries.

- The recent acquisition of Euronav tankers and the sale of old tankers demonstrate Frontline's strategic vision and position the company for long-term growth.

Introduction

Frontline plc (FRO) is a global leader in the seaborne transportation of crude oil and refined products. The company operates a fleet of tankers of various sizes, primarily Very Large Crude Carriers (VLCCs), Suezmaxes, and Aframaxes. At present, Frontline is actively managing its fleet to optimize utilization rates, adhering to strict environmental regulations, and looking to expand its operational capacity, demonstrating adaptability and resilience in a sector known for its volatility. Due to strategic moves such as selling old tankers, acquiring superior ones, and dumping some shares to increase investment capital, I believe Frontline plc is a buy.

Financials

Frontline plc stands out in the maritime shipping sector with a solid financial base and a strategic vision that supports a buy thesis. The Q3 2023 earnings call , despite acknowledging the prevailing industry headwinds, demonstrated management's confidence in the company's resilience and future growth potential.

Financially, Frontline navigated through softer market conditions characterized by lower Time Charter Equivalent (TCE) rates, which, although impacting revenues, did not significantly diminish the company's robust cash flow position. With $715 million in cash reserves, Frontline is well-capitalized to pursue strategic fleet expansions and withstand market volatilities. The management has shown prudence by not fully hedging its positions, allowing Frontline to benefit from potential market recoveries—a stance that underpins my positive outlook for the company.

Frontline's strategy to maintain a significant spot market presence is indicative of its agile business model. While this exposes the company to market fluctuations, it also positions Frontline to capitalize on anticipated increases in shipping rates as the industry grapples with low order books and extended lead times for new vessels.

The company's financial prudence is also evident in its operational efficiencies. The increase in administrative income and reduction in expenses suggest effective cost management. The strong net cash from operating activities reflects the company's capacity to generate healthy cash flows, reinforcing my confidence in its financial situation.

Admittedly, the canceled merger with Euronav (EURN) and increased operational costs due to higher bunker prices and fleet expansion have posed questions. However, Frontline's strategic adaptability and positive revenue trends offer convincing rebuttals to these concerns. The company's proactive approach to managing market changes, such as varying oil export dynamics and geopolitical headwinds, further support a buy rating.

Deal with Euronav

Though the merger fell through, the recent acquisition of Euronav tankers by Frontline plc underpins my Buy thesis for several compelling reasons. This move means scaled operations and will augment the company's competitive edge in the crude transportation sector. Not only does this expand Frontline's fleet size but it also consolidates its position in a market where scale can significantly drive efficiencies and bargaining power.

In purchasing these vessels, Frontline will capitalize operational cost savings and increased revenue. The expanded fleet brings more flexibility and capability to meet the diverse needs of global clients, especially at a time when the demand for energy transportation is expected to remain robust. It's a proactive step, one that anticipates and positions Frontline to benefit from the market's long-term trends.

The sale of Euronav stock by Frontline is a judicious reallocation of capital in order to reinvest in core business areas that promise better returns.

Sale of Old Tankers

Frontline's strategic sale of its five oldest VLCCs (Very Large Crude Carriers) also goes along with my buy thesis for several reasons. The company has capitalized on the current upswing in the value of used tanker tonnage, fetching an impressive $290 million for these vessels, subsequently generating a robust net cash inflow of approximately $207 million post-debt repayment. This move not only bolsters the financial standing of Frontline but also resonates with its long-term strategy to pivot towards a more modern, fuel-efficient fleet.

I am particularly encouraged by the strategic foresight of this transaction. By offloading older, less efficient vessels, Frontline is effectively streamlining its operations, reducing maintenance and operational costs associated with aging tankers. This divestment aligns well with the broader industry shift towards eco-friendly and cost-efficient maritime solutions, positioning Frontline at the forefront of this transformative wave.

Most importantly, the sale generates substantial capital that can be strategically reinvested to further modernize the fleet or to strengthen the company's balance sheet.

Risks

While my stance remains a confident buy, it is prudent to acknowledge the inherent risks in the investment. The following reasons are why I am not recommending Frontline as a strong buy. The cyclical nature of the shipping industry means that Frontline's financial performance is susceptible to global economic shifts and trade flows. Lower Time Charter Equivalent (TCE) rates, as witnessed in recent quarters, have squeezed margins and impacted revenues. Moreover, the company's aggressive fleet expansion strategy, while forward-thinking, does introduce financial strain, partially offset of course by the sale of old tankers. The capital expenditure and debt undertaken to modernize the fleet and acquire new vessels must be weighed against the potential for prolonged downturns in the shipping cycle, which could hamper the company's ability to generate expected returns and service its debt.

The industry's move towards eco-friendliness, while a strategic fit for Frontline's modern fleet, also comes with regulatory risks. Stricter environmental regulations could increase operational costs or necessitate additional capital outlays for compliance. There's also the matter of geopolitical tensions affecting trade routes and, consequently, shipping rates. For instance, the Red Sea crisis and the volatile oil export landscape present both opportunities and challenges that could swing either way for Frontline.

From the opposition's viewpoint, the canceled merger with Euronav and the potential overvaluation of assets in a buoyant used tanker market could signal caution. However, I think Frontline is doing plenty to offset the challenges presented by such events. The divestment of older vessels and the acquisition of Euronav's more efficient fleet is a calculated move to stay ahead of industry trends and position the company as a leader in a future-proofed market. Thus, while risks are an undeniable aspect of the investment, I maintain that Frontline's strategic decisions and solid financials present a compelling case for long-term growth and affirm my buy thesis.

Valuation

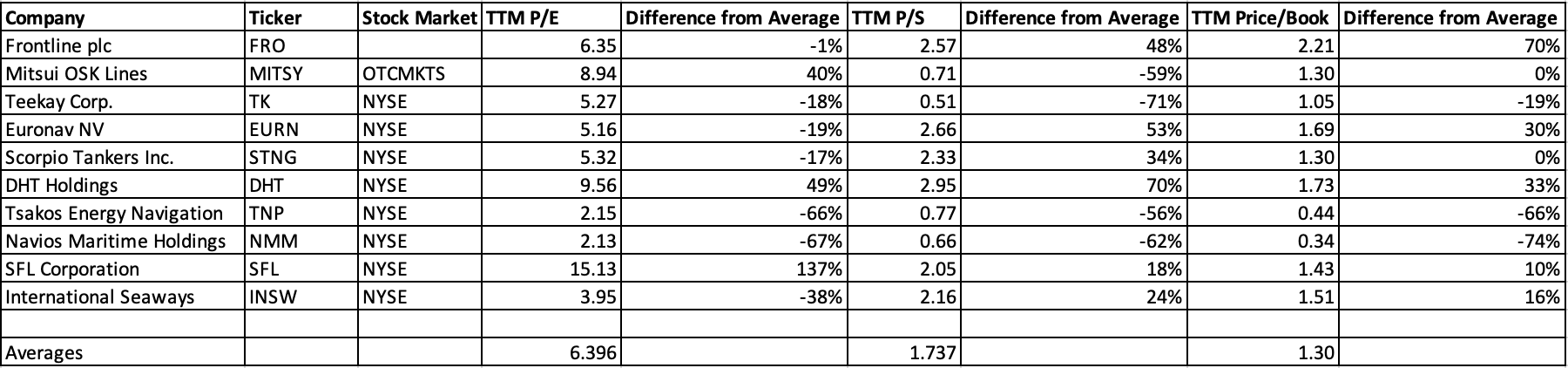

Getting into the financials of the company compared to a peer group I put together, it's clear that Frontline is positioned well among its competitors. Also, I’m aware that Seeking Alpha articles usually prioritize forward financials, but I could not get FWD stats for most of the competitors, so TTM will have to suffice. With a TTM P/E ratio that hovers just below the peer average, Frontline seems undervalued, especially when considering its strategic maneuvers in fleet expansion and efficiency gains. This slightly lower P/E ratio, in my opinion, hints at an attractive entry point for investors, as it suggests potential for an upward revaluation should the company continue to deliver strong earnings.

Looking at the P/S ratio, Frontline stands out again. Its P/S ratio, which is notably higher than the peer average, could typically raise eyebrows, suggesting a premium pricing. However, another way to look at this metric is that, buoyed by the company’s efficient and modern fleet, it reflects the market’s willingness to pay more for each dollar of Frontline’s sales, possibly due to the anticipated benefits from its recent acquisitions.

The P/B ratio further cements my confidence. Frontline’s P/B is significantly higher than the group average, underlining a market recognition of value in the company's assets beyond the balance sheet figures. This is an important marker for a company like Frontline, whose strategic investments in a modern eco-friendly fleet position it to capitalize on the evolving demands of the shipping industry.

Peer Group Financials (Seeking Alpha)

{kind=link}

Conclusion

Frontline plc stands out as a compelling investment in the maritime shipping industry. Despite the inherent risks associated with the cyclical nature of the sector and the potential challenges of regulatory changes and geopolitical tensions, Frontline's strategic decisions—particularly its fleet modernization, financial prudence, and recent asset reallocation—solidify its position as a forward-thinking and resilient player. The company's robust financials, strategic fleet expansions, and proactive market positioning amidst industry headwinds underscore its potential for long-term growth. While cautious consideration of the outlined risks is advisable, the overall picture painted by Frontline's recent maneuvers and financial health presents a great case for it being a buy in the current market landscape.

For further details see:

Frontline Is A Solid Buy Despite Canceled Merger With Euronav