FRO - Frontline Plc: Feast Or Famine We Look At Possible Outcomes

2023-03-27 08:28:28 ET

Summary

- We like Frontline plc for its large, modern and diverse tanker fleet.

- Spot market throws off large free cash flow, which is expected to continue in the next few quarters.

- History shows that the period of feast does not last long, but so do famines.

- A shift away from reliance on astronomical spot rates to lower but predictable rates from period charterers might be wise.

Frontline logo (Frontline)

Investment thesis

Investors and traders that took long positions in maritime tanker-owning companies early last year have made good returns.

The share price of Frontline and peers (SA)

{kind=link}

In November last year, we concluded in our last article on Frontline plc ( FRO ) when the share price was $13 that the "easy money had been made" and that we would be reluctant to enter a position at that time. As such, we gave it a Hold stance.

Four months on, with FRO delivering good results in Q4, its CEO Lars Barstad stated this during the conference call :

We are tremendously bullish for the next couple of years"

Therefore, we want to share our view with our readers on our take on FRO.

FY 2022 financial results

- Profit & Loss

FRO ended the year 2022 on a high note, recording its highest net quarterly profit in Q4 since 2008.

It delivered an adjusted net income of $240 million, or $1.08 in EPS.

More meaningful than q-o-q earnings is to look at the TTM EPS. This was $2.21.

Spot rates do fluctuate a lot and when earnings have to be accounted for on a load port to discharge port too, it can distort the earnings on a quarterly basis.

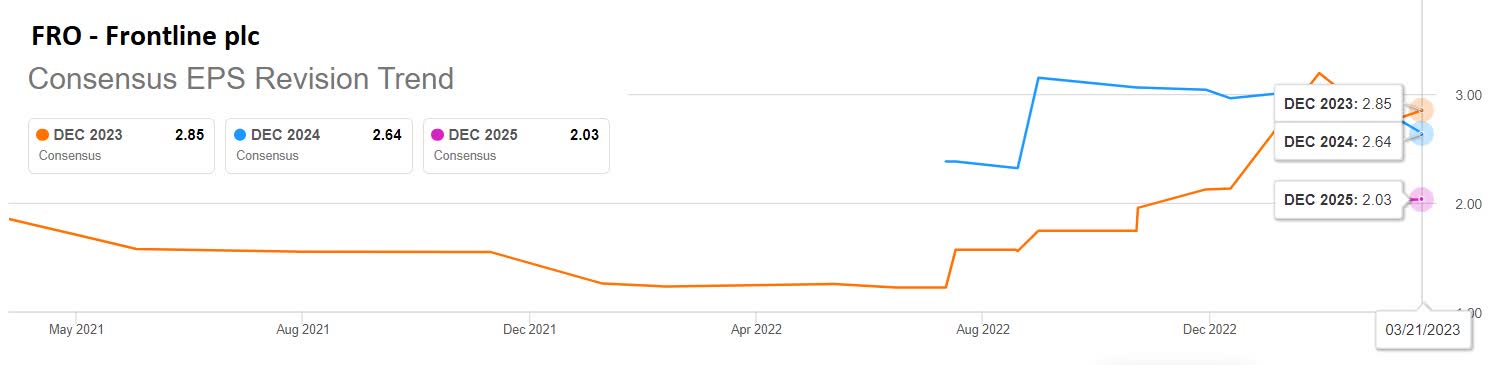

Any trailing earning is obviously like looking in the rearview mirror, and we know that it is more important to focus on what is ahead. Analysts as per data from SA have given an estimate of future earnings for FRO.

FRO - consensus EPS forecast (SA)

{kind=link}

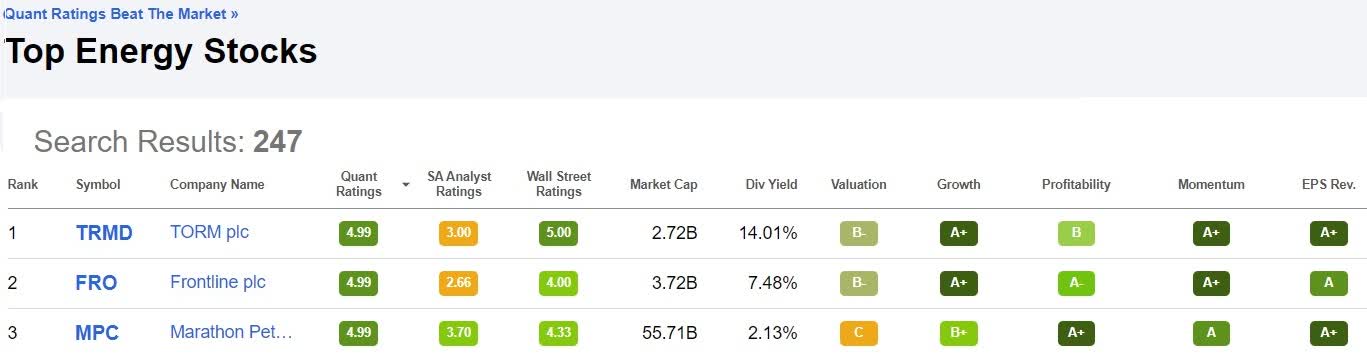

If we use SA's quant rating, we get a very good rating. Out of 247 energy companies, FRO is only beaten by just one peer, namely TORM plc ( TRMD ).

FRO is number 2 of 247 energy companies (SA quant rating)

{kind=link}

That is impressive.

FRO achieved an average of $63,200 per day from their VLCC fleet, $57,900 per day from the Suezmax segment, and $58,800 per day from the LR2/Aframax fleet.

The operating expenses are only $8,800/day for VLCCs, $17,600 for Suezmaxes, and $8,700 for LR2 tankers. If we consider the cost of finance, we get breakeven rates of $27,000 for VLCCs, $21,500 for Suezmaxes, and $17,600/day for the LR2s.

The catalyst for these good numbers is a combination of China's increasing import of crude and a continuation of longer distances covered as a result of the shift in trade patterns.

This trend is expected to continue for several quarters going forward, with plenty of cash going to be generated, provided the market stays elevated as it now is. And that is the difficult question.

Their CFO informed during the conference call, that if VLCC rates stay at $75,000/day level and when they model estimated corresponding rates for Suezmax and LR2s using historical data, FRO could generate a free cash flow of more than $1.4 billion or $6.46 per share.

It is a bit optimistic but certainly not impossible.

- Returning capital to shareholders

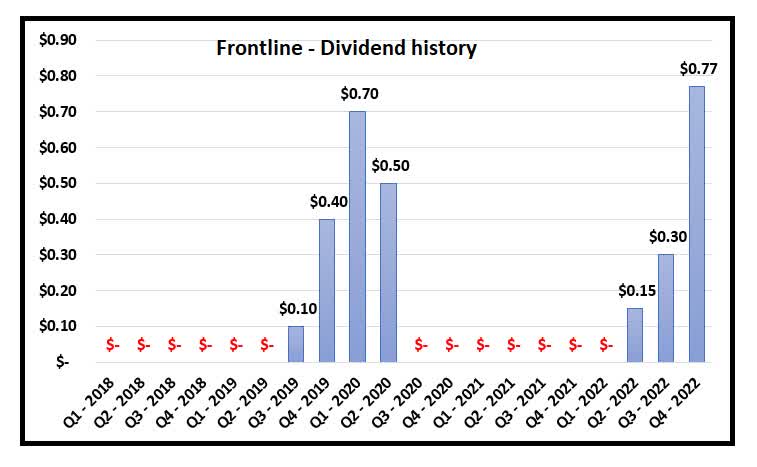

FRO's dividend policy is to aim to distribute close to, or equal to, earnings per share adjusted for non-recurring items.

For Q4, the board decided to pay a dividend of $0.77. Based on their TTM dividend of $1.22 per share, you get a dividend yield of 7.6%.

FRO - dividend history (Data from Frontline plc. Graph by author)

{kind=link}

The problem is that dividends are not consistent.

FRO - Dividend consistency grade (SA)

Management is very optimistic, and we have no reason to believe this optimism is not grounded in sound and realistic projections about the future.

However, the problem is that history is not on their side. This time, it really has to be "different".

- Balance sheet

With the 6-month USD LIBOR now standing at 5.14%, floating rate loans are becoming more expensive to service.

FRO's long-term debt stood at $2.11 billion at the end of 2022. However, their main tangible assets consist of vessels with a book value of $3.66 billion, and cash plus marketable securities and other current assets totaling $0.88 billion.

This leaves us with a leverage ratio of 46% which is quite acceptable in view of the fact that their fleet is very modern.

In February 2023, they also repaid $60 million of a $275 million senior unsecured revolving credit facility it has from Hemen, which is John Fredriksen's private investment holding company.

Starting from Q1 this year, they have revised the estimated useful life for their vessels from 25 years to 20 years, which is expected to increase depreciation expense by approximately $59 million in 2023. According to their CFO Inger Klemp, these additional costs will reduce the earnings by 5 to 6 US cents on a quarterly basis.

Business development

As of the end of February this year, when FRO reported Q4, they had 87% of their VLCC days fixed at an average earning of $58,300 per day, 77% of its Suezmax days at a very strong $72,400 per day and 68% of the LR2/Aframax days at a $63,900 per day.

Supply and demand dynamics do support their optimistic view of the next couple of years.

On the supply side, things are clear since data is readily available.

FRO expects that we will have a growth in the total fleet of tankers of about 3% this year. It will actually be a slightly negative growth in 2024 and 2025.

Whenever we experience high market rates, it always puts a damper on the scrapping of vessels. Although as many as 12% of the tanker fleet is older than 20 years, many of these ships can still make good money for scrupulous actors that are willing to trade in what is now described as the "dark fleet market".

Newbuildings can be ordered now, but shipyards are not able to deliver a new tanker before 2025. Those are mostly from yards in China.

One concern we have is that if we are going to see elevated rates of the $75,000/day that FRO is talking about, and it stays elevated for a prolonged time, the Chinese government, which owns many of the large reputable shipyards in China may take action to boost yard capacity and try to build more VLCCs as the cost of transporting all this crude is becoming too expensive. As a guidance, the freight cost of one VLCC cargo from US Gulf to China is now as high as $11 to 12 million. It will take time, which is good for FRO.

On the topic of China, we believe they have ambitions for their refinery industry to become a larger exporter of refined oil products. We have seen that the refineries are getting h igher quotas for the export of refined oil products over the last year.

Risks to the thesis and conclusion

The main risk to the thesis is that it is very difficult to predict the future of the demand side, and FRO is very dependent upon what the spot market has to offer.

A hard recession and weak oil consumption will put a damper on oil demand.

If spot rates give owners $75,000 or more per day, and you only can achieve $35,000 for a 2 to 3-year time-charter, the heart tells you to "keep dancing while the music is playing".

The brain should tell you to put away a certain percentage of the fleet at such levels, which still makes you money, just not as much.

But history has shown that the heart often wins over the brain.

We share FRO's optimistic view, but not enough to change our stance from Hold to a Buy.

There are too many "known unknowns" that keeps us on the sideline. We still have exposure to the industry through SFL Corporation ( SFL ).

For further details see:

Frontline Plc: Feast Or Famine, We Look At Possible Outcomes