FRO - Frontline: Spot Rates Have Been Volatile

2023-09-26 23:44:01 ET

Summary

- Frontline reported strong Q2 results helped by high spot TCE rates.

- Since quarter end, spot rates have been on a rollercoaster ride.

- Spot rates could remain volatile in the future due to a number of factors.

Back in April , I wrote that Frontline ( FRO ) had been riding some powerful market trends, but they seem to have cooled recently and I thought the stock was close to fairly valued in normal market conditions. My "Hold" view has proven to be too cautious, as the stock has generated about a 30% return since. Let's catch up on the name.

Company Profile

As a refresher, FRO operates a fleet crude oil and refined product tankers. Its vessels include 22 VLCCs, 25 Suezmaxes, and 18 LR2/Aframaxes. The company also has one Aframax vessel that it manages under a commercial agreement. The bulk of FRO's Suezmax tankers are around 157,000 dwt.

Of the vessels it owns, over 90% are considered ECO vessels, while about two-thirds have scrubbers installed. The average age of its fleet is just over 5 years.

Strong Q2 Results

With nearly all its revenue coming from the spot market, FRO’s results are very dependent on time charter rates. On that end, the company got a boost when it said it saw an unusual spike in rates for VLCC and Suezmax tankers towards the end of Q2 due to a minor weather delay.

For the quarter, the company realized spot TCE rates of $64,000 for VLCCs, $61,700 for Suezmax tankers, and $52,900 for LR2/Aframax vessels. Showing how drastically the market has changed in the past year, the company realized spot TCE rates of $16,400 for VLCCs, $26,500 for Suezmax tankers, and $38,600 for LR2/Aframax vessels in Q2 of 2022.

As a result of the strong rates, FRO recorded its second-highest quarterly profit since 2008, recording a net income of $230.7 million, or $1.04 per share. Adjusted EPS came in at 94 cents, topping analyst estimates by 12 cents.

Revenue for the tanker operator surged 71% to $512.8 million. That sailed past analyst expectations for revenue of $332.8 million.

Adjusted EBITDA rose from $97.8 million a year ago to $300.82 million.

The company declared an 80-cent dividend for the second quarter.

Looking ahead, FRO said that 74% of its Q3 TCE rates were done at $53,200 for VLCCs, which is about a -17% decline from Q2. About 67% of Suezmax TCE rates are at $48,800, which is a -21% sequential decline. LR/Aframax TCE rates, meanwhile, are 57% locked in for Q3 at $40,500, a -23% sequential drop.

Management discussed some of the dynamics impact the tanker market. Chief among them is Asian demand has been increasing, which given the China re-opening from Covid lockdowns isn’t that surprising. The company noted in Q2 that Asia-Pacific volumes were up by 1.8 million barrels a day versus a year ago.

The fallout of the Russia-Ukraine war is still making an impact on the market, with Russian price caps starting to affect rates. The company said with it becoming more complex to ship Russian crude, some ghost vessels have returned to the market, which has put some pressure on rates.

Global refinery maintenance and outages can also have had an impact on the market. The fall is typically the high point for refinery turnaround, but the company said most rates are fixed ahead of time. Meanwhile, it sees refining margins starting to improve.

Discussing the future environment on its Q2 earnings call , CEO Lars Barstad said:

“ I think there's 2 key factors that needs to be watched. One is obviously China. There's mixed signals coming from [China]-- so in our little part of the world, as I mentioned, which is transport of oil. China looks to run on all cylinders, their import numbers are kind of record high every month. And that doesn't tally up with kind of all the other macroeconomic data coming out of China. So if they're building building a lot of inventories into the winter here, they have, at least historically, they've been able to kind of take the foot off the gas pedal and suddenly disappoint by 1 million or 2 million barrels per day in their import program. And if that happens, we'll that's obviously not going to be very, very bullish. So I think that's the big question. Are they either running in preparation for other stimulus that will stimulate their economy to need basically all this oil? Are they importing in order to have the ability to export into the winter season? Or are they basically trying to hoard crude oil before an expected price increase on crude oil or others? It's very difficult to know. But I think that's the thing to watch. And kind of with the imports next to all the economic news we're getting out of China, -- well one tends to become a little bit worried. Secondly, it was obviously the weather and the weather we can't really control. Whether we're going to have a repeat of last year which was fairly warm? Or if we're going to have a proper full-on winter, which is going to kind of affect demand on the positive side. So I think those 2 are the key factors that, at least I'm a little bit concerned about.”

Overall, FRO reported a strong quarter, as spot TCE rates remained strong in Q2. Q3 gets more interesting, as it locked in rates at lower prices. Meanwhile, rates plunged in August on the back of the OPEC+ production cuts in July. Rates are set forward, so this could impact both Q3 and Q4 results.

Notably, tanker rates have begun to nicely rally recently ahead of winter. There is also the possibility that once OPEC+ loosens its supply curbs, that tanker rates could soar next year as more supply hits the market.

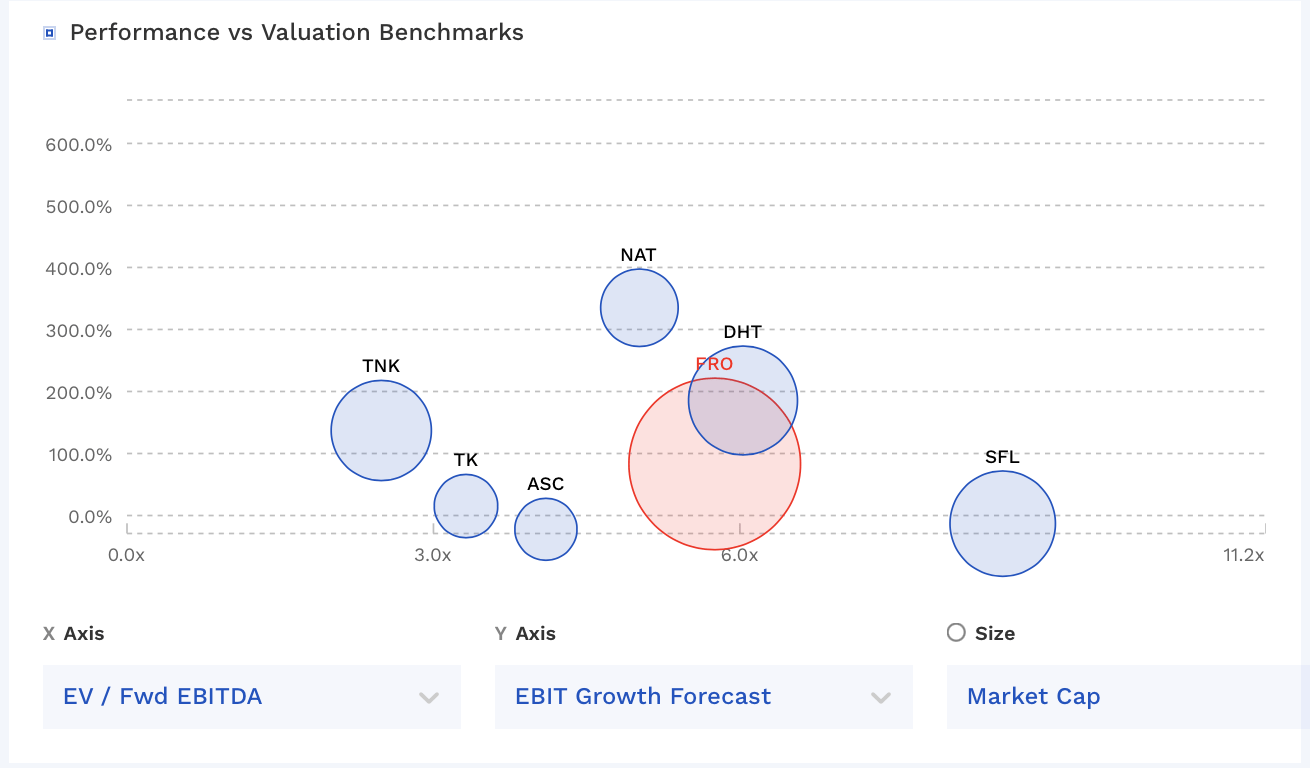

Valuation

FRO trades at 5.6x the 2023 EBITDA of $1.03 billion and 6.4x the 2024 EBITDA consensus of $903.3 million.

On a PE basis, it trades at 6.1x EPS estimates of $3.00. Based on the 2024 consensus for EPS of $2.70, it trades at 6.8x.

FRO stock trades towards the middle of other marine shipping companies.

{kind=link}

Conclusion

The tanker market has shown a lot of volatility in the past several months. While rates have softened versus Q2 levels, they are still healthy, although as evidenced by the past few months, rates can change on a dime in either direction. While the 2024 set-up looks good, there are still uncertainties around China’s turnaround and the overall global economy.

At the same time, this winter will bring a strong El Nino. This not only affects weather in the U.S., but it other threatens crops in Asia through warmer weather and droughts and brings colder winters to Northern Europe. How this impacts the global economy and crude uptake is a wildcard.

At its current enterprise value, you could theoretically replicate FRO’s fleet with newbuild vessels. Of course, that would take years to build out, but it gives you a sense of the company’s current valuation. As such, given its valuation and a volatile market, I continue to rate the stock a “Hold.” While difficult to predict, I'm looking for a 60-70 cent dividend next quarter, which is still a very robust yield for oriented investors.

For further details see:

Frontline: Spot Rates Have Been Volatile