FRO - Frontline: Spot Rates Pull Back

2023-04-28 19:06:20 ET

Summary

- FRO had a huge Q4, but spot rates have been pulling back recently.

- A re-opening of China and Ukraine-Russia war should still be positive for tanker rates.

- An aging fleet and low order book bode well a few years out.

Frontline ( FRO ) has been riding some trends in the oil tanker market, but spot rates have started to cool, which will likely impact its 2H earnings.

Company Profile

FRO owns a fleet of tankers that transport crude oil and refined products. It currently operates 22 VLCCs, 26 Suezmax, and 20 LR2/Aframax vessels.

VLCCs, or Very Large Crude Carriers, have a cargo-carrying capacity of around 300,000 dead-weight tons. Suezmaxes are smaller, having a capacity of between 120,000-200,000 dwt, and can travel through the Suez Canal. Most of FRO's Suezmax tankers are around 157,000 dwt. LR2 vessels typically have a capacity between 105,00-115,000 dwt.

Of the vessels it owns, 91% are considered ECO vessels. Meanwhile, ~64% have scrubbers installed. The average age of its fleet is ~5 years.

Opportunities And Risks

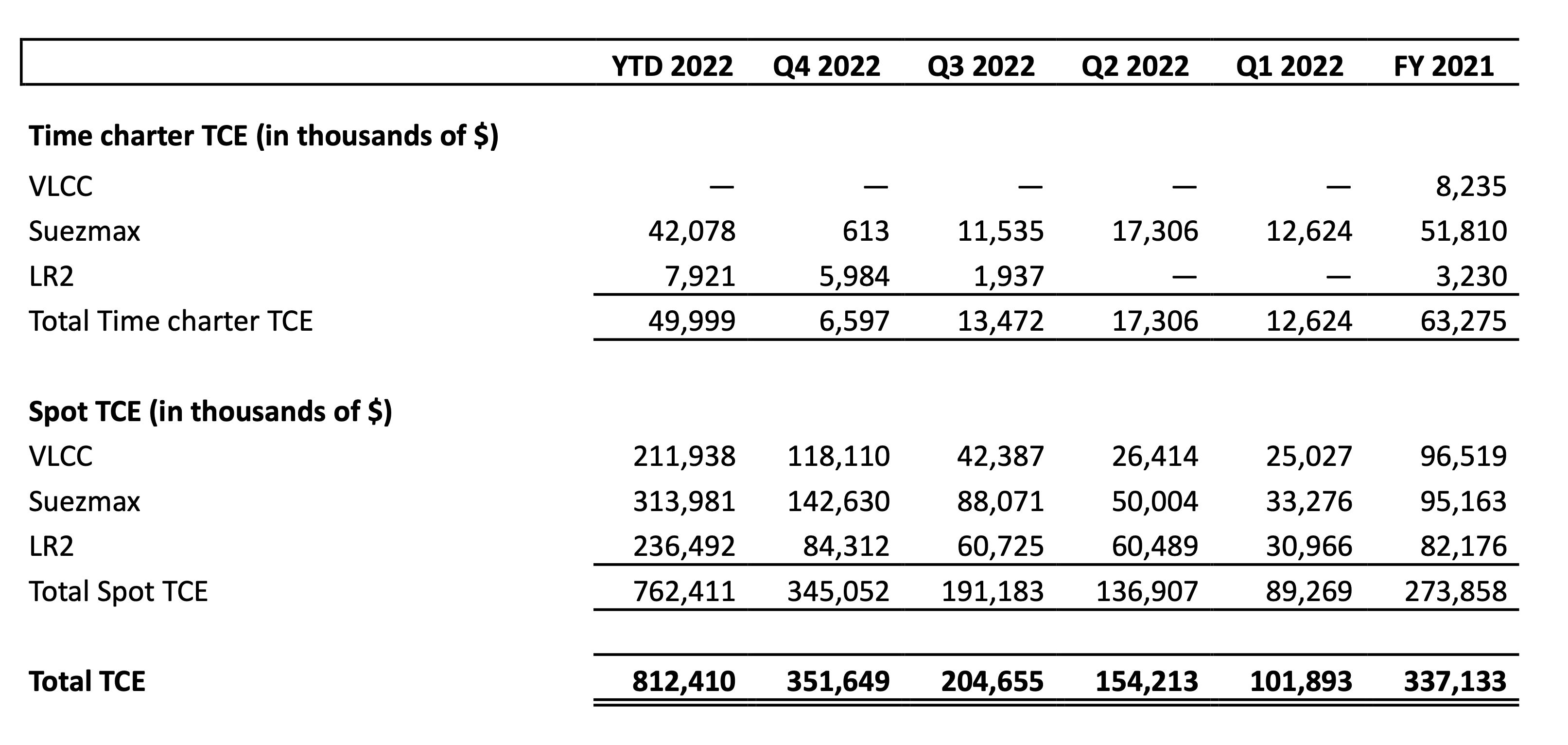

With 98% of FRO's Q4 revenue coming from the spot market or short-term charters, the company is riding some nice trends in the tanker market. As such, the biggest opportunity and risk to the company currently is spot rates.

{kind=link}

As I noted in my recent write-up in Ardmore Shipping ( ASC ), recent geopolitical events have been influencing the tanker and refined product shipping markets. (Note that ASC is a refined product, while FRO is more crude.) The Russia-Ukraine war and later Russian oil price cap is having a huge impact on rates and routes. With the price caps, Russia has shifted its crude oil sales to places in Asia, such as China and India, and away from Europe. These are longer routes, and then Europe needs to get its oil from farther away as well.

In addition, China's re-opening is also having a big impact on crude demand . Early during the price caps, small independent Chinese refineries were the primary buyer of Russia oil. However, larger Chinese refineries are also beginning to purchase Russian oil as the world's second-largest economy opens up after Covid restrictions and oil demand increases. This added a lot of demand for tankers at the same time route times have increased.

Discussing the current state of the market on its Q4 earnings call CEO Lars Barstad said:

"I think it's probably not a secret that we are tremendously bullish for the next couple of years. And during the quarter, all segments from an operator performed. It was finally the turn for the VLCCs to shine. The average weighted market earnings for tankers are actually flirting with 2004 highs.... And I think kind of in general, the market hasn't recognized how substantial Q4 ended up being. And this is the average weighted earnings for all tankers and obviously, what's happening on MRs, on LR1s, LR2s, and VLCCs together has made this possible. We are in market conditions where it's not only the VLCC outperforming is basically all segments are performing.

"Chinese imports are back above pre-Covid levels hovering around 10 million barrels per day, and the VLCC shipments to China are actually at all-time high. And I would like to say the big ships are back. During Q4, we saw the G7 crude oil price cap come into effect on December 5th. We have seen already a lot of crude oil and full being redirected to around Europe to Asia and Middle East predominantly. So the effect of the 5th of December cap was somewhat muted. We also need to keep in the back of our head that during to a mild winter in the Northern Hemisphere. Oil prices were also hovering below or around $80 per day, making Russian crude comfortably priced below the price cap."

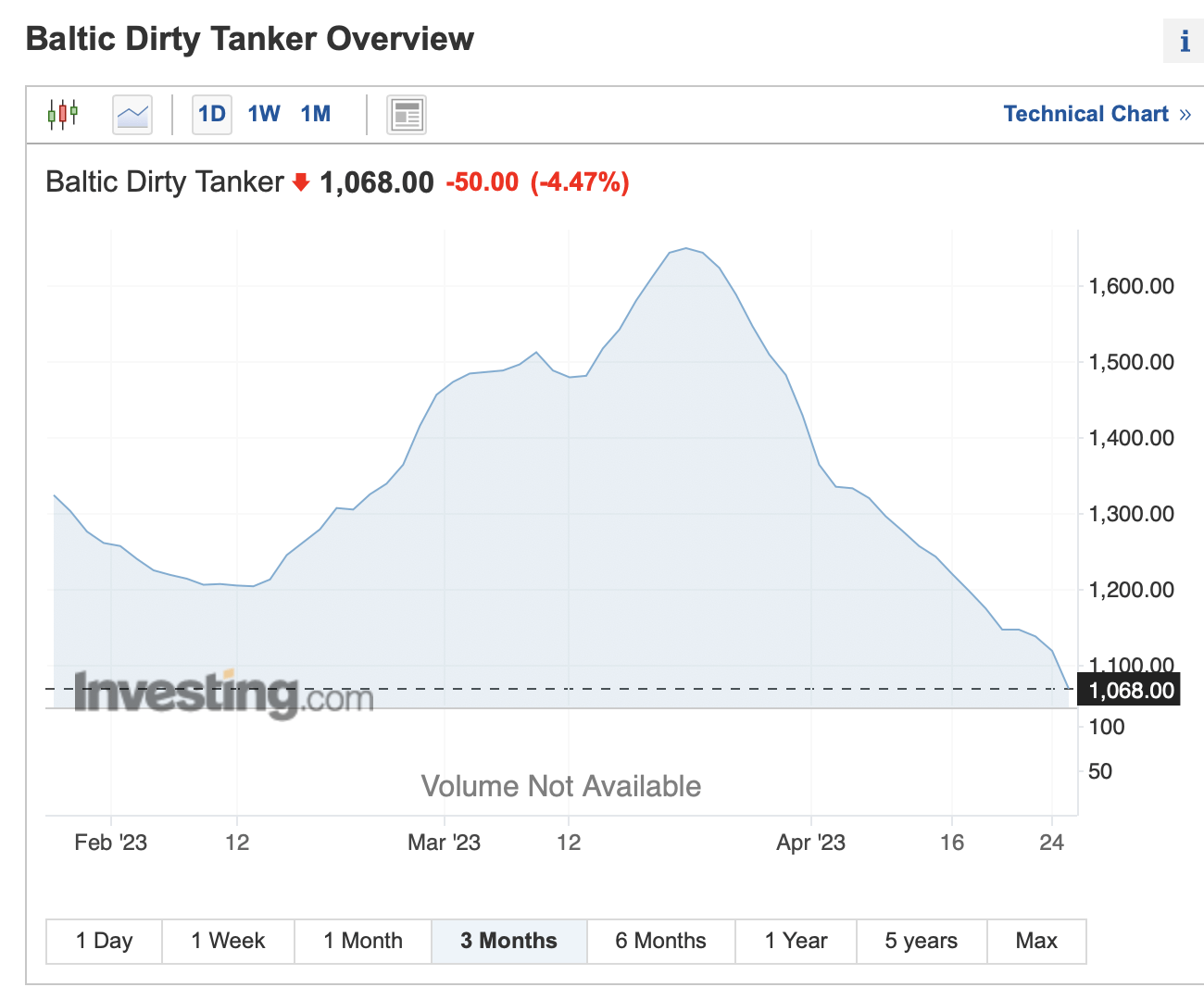

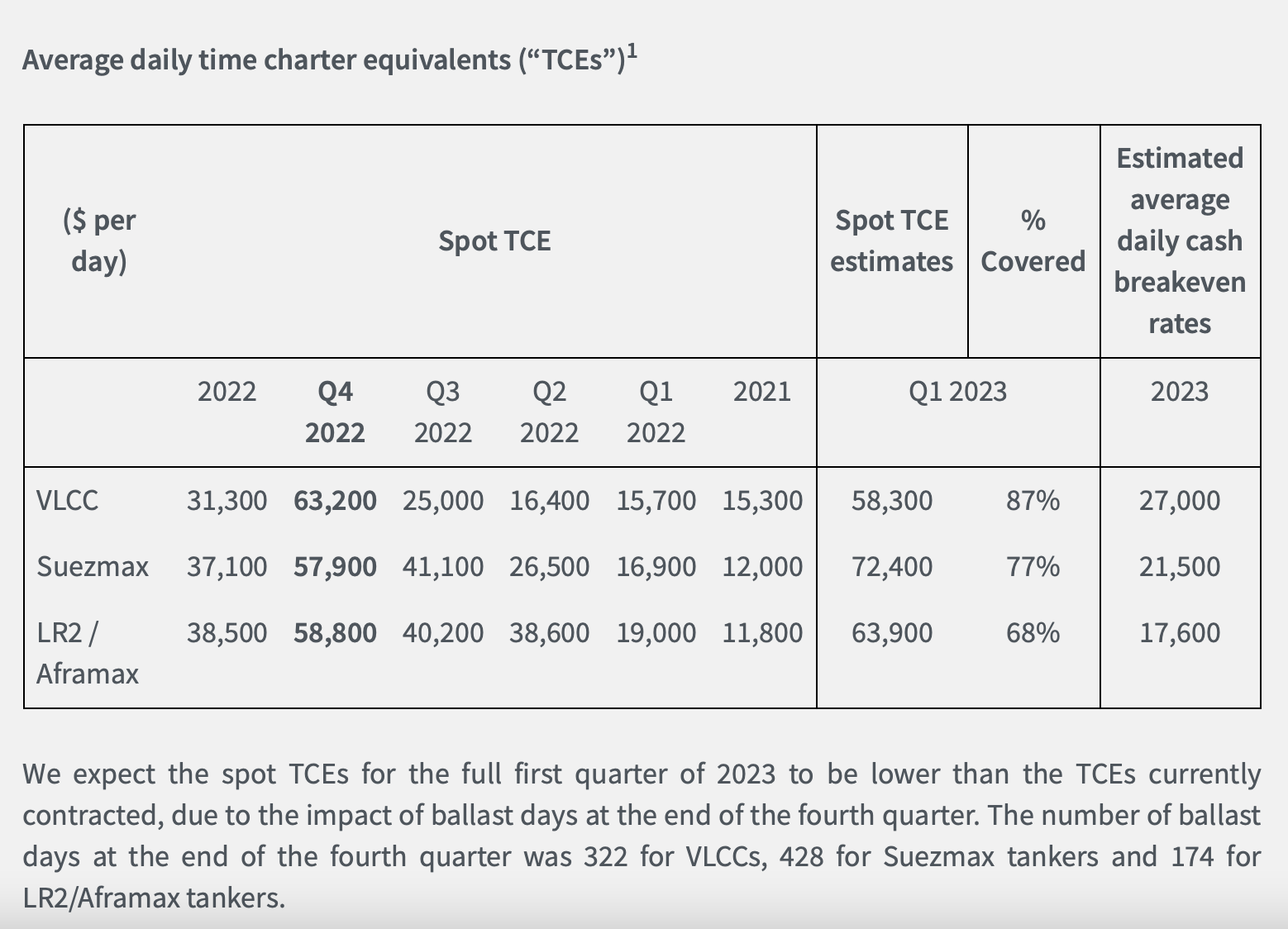

That said, the spot prices for crude tankers have fallen hard since late March. In fact, prices are lower than they were a year ago. While spot rates were pretty strong in Q1, they could impact FRO's Q2 results.

{kind=link}

Now, it is worth noting that FRO's ships do have low breakeven points. The company estimates that its average breakeven for its fleet is rates of $22,300, with VLCCs at $27,000, Suezmaxes at $21,500, and LR2s at $17,600. The company's ECO vessels also get premium prices compared to non-ECO vessels. An ECO vessel with a scrubber got between a $10,300 a day premium rate for an LR2 in Q4, while a VLCC got a $19,400 a day premium.

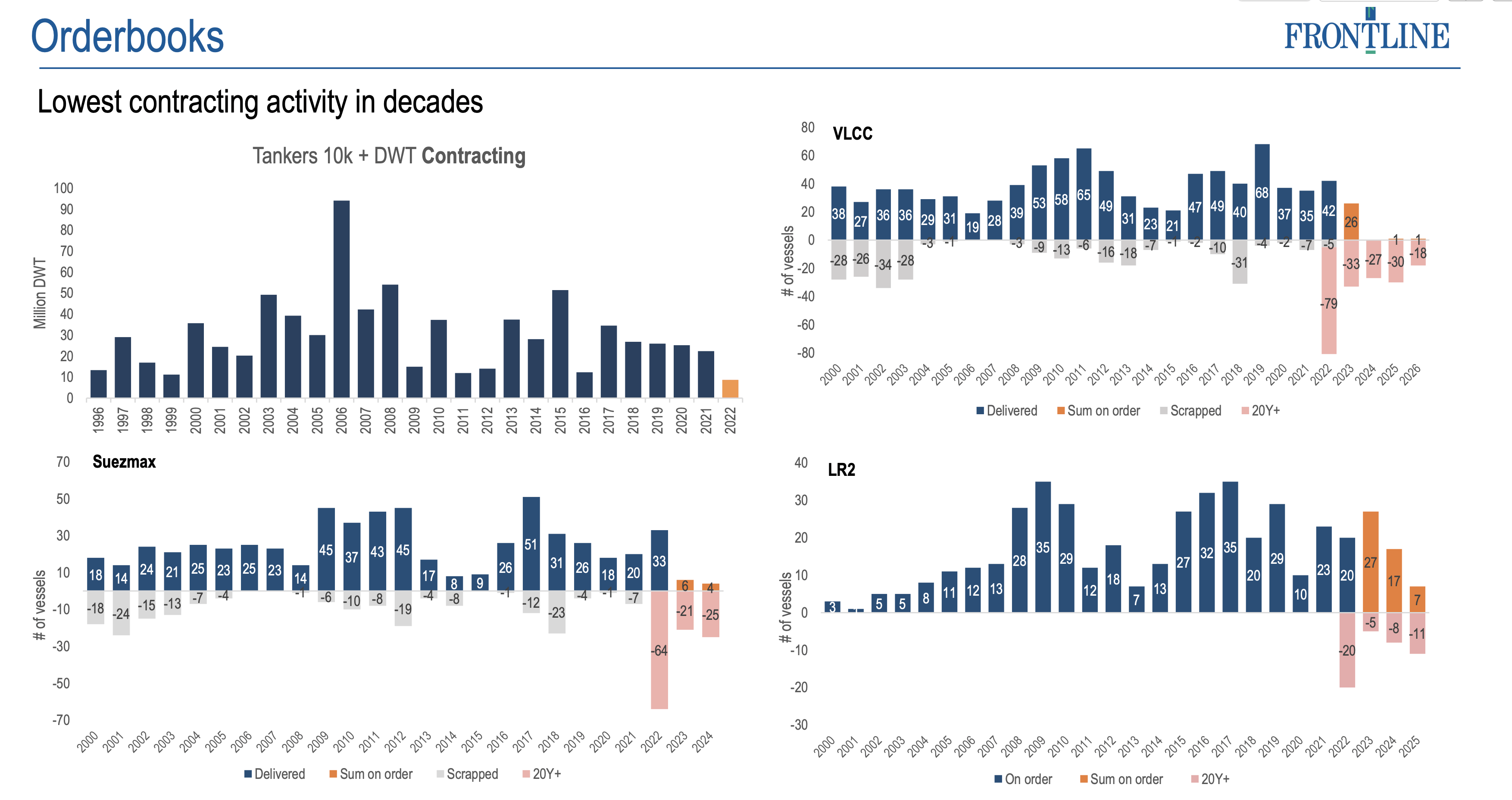

Over the long term, the supply of ships also plays a big role in market rates. On that front, the tanker order book is at its lowest levels in decades. There is also a significant number of vessels over 20 years, which is when companies typically consider scrapping vessels in a normalized market. The order book and scrapping dynamics for VLCC and Suezmaxes look particularly attractive in upcoming years.

{kind=link}

On its Q4 call, Barstad said: "If you look at the VLCC fleet isolated, there are now during 2023, we'll have 112 VLCCs passing 20 years. That will be 13.2% of the entire fleet. The order book stands at 28 units, and that represents 3.3% of the existing fleet. If you look at the suezmax, this is even more pronounced. By the end of 2023, 85 vessels will be above 20 years. That represents 14.5% of the fleet. The order book is at a modest 10 vessels, and that represents 1.7% of the fleet."

Dividend

FRO was unable to pay a dividend for a while due to its impending and then canceled merger with Euronav. However, after a February ruling that dismissed an emergency arbitration request for Euronav, the company paid out both a Q3 and Q4 dividend together. The Q3 dividend was for 30 cents and the Q4 dividend was for 77 cents.

The company will pay a variable dividend going forward. It will likely be about 70-80% of adjusted earnings.

Valuation

FRO trades at 5.7x the 2023 EBITDA of $929.9 million and 7x the 2024 EBITDA consensus of $760.9 million.

On a PE basis, it trades at 6x EPS estimates of $2.61. Based on the 2024 consensus for EPS of $2.26, it trades at 6.8x.

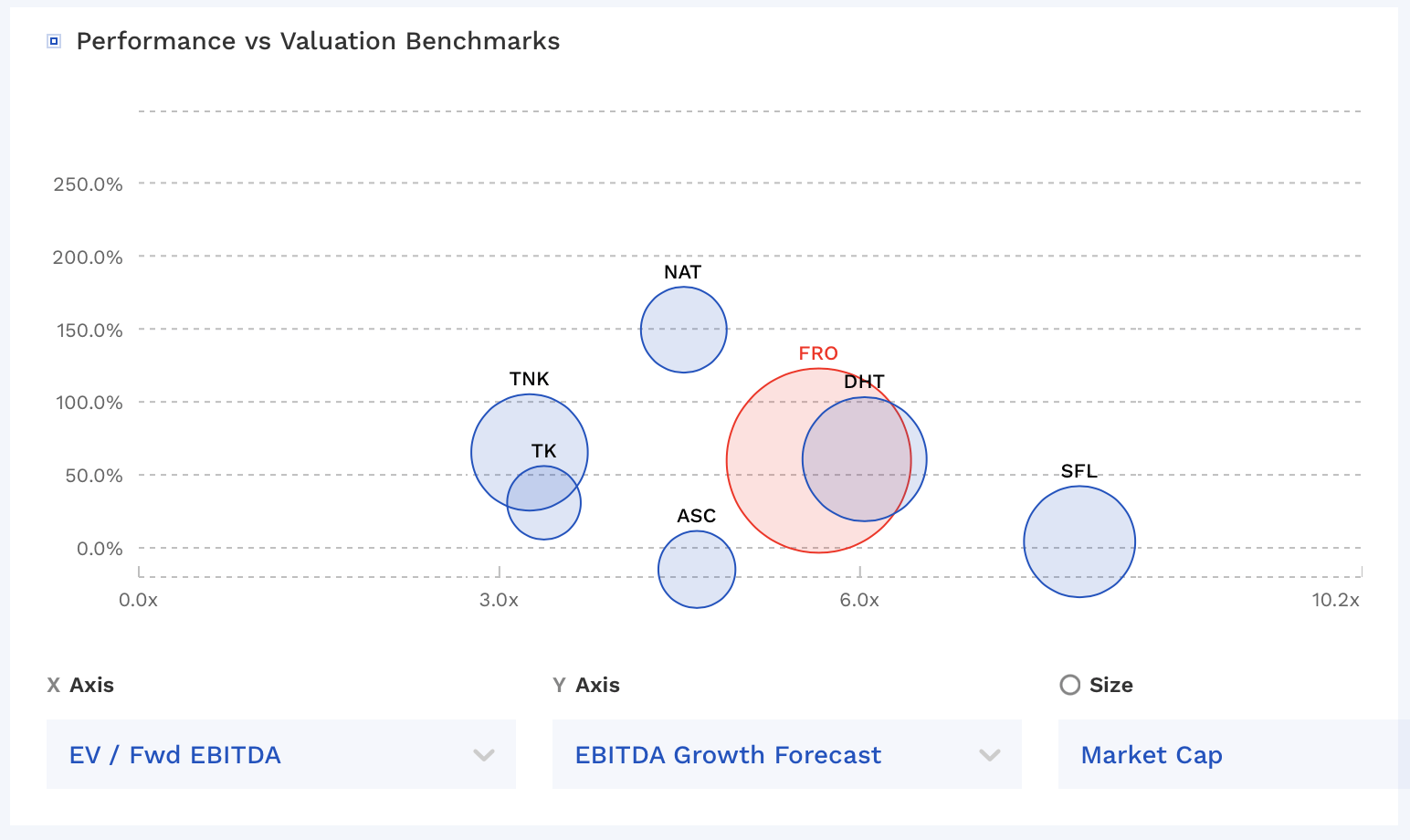

FRO stock trades towards the middle of other marine shipping companies.

FRO Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

FRO had been riding some powerful market trends, but they seem to have cooled recently. We'll see if spot rates pick up again, as seemingly China re-opening and the Russian oil caps should keep rates attractive. However, OPEC+ cutting production did add the fear that oil demand could weaken.

In a normalized environment, FRO is probably trading near fair valuation. And we may be heading back there sooner than expected if spot rates don't rebound. However, the long-term dynamics of the fleet age for VLCCs and Suezmaxes along with a light order book bode well for the medium term as well.

As for the dividend, I wouldn't expect a 77-cent dividend again. The next dividend will be strong given that it booked its fleet on some solid rates, saying it "booked 87% of our VLCC days at $58,300 per day, 77% of or Suezmax stays at a cool $72,400 per day and 68% of our LR2/Aframax days at a solid $63,900 per day." However, unless these rates have been chartered further out, I'd expect the dividend after this one to be a good deal lower.

{kind=link}

Overall, I view the stock as a "Hold" at the moment, with the knowledge that the current dividend will be lowered moving forward.

For further details see:

Frontline: Spot Rates Pull Back