FRO - Frontline: Still A Buy At The High Price

2024-01-13 05:14:51 ET

Summary

- The Red Sea crisis and China's growing demand for crude oil are strong tailwinds for crude oil tankers. Frontline remains one of the best ways to bet on that theme.

- FRO's 3Q23 results were disappointing, but the rise of day rates for Aframax and Suezmax ships is promising for future performance. The seasonality supports higher VLCC rates, too.

- The company has an excellent dividend policy, solid financials, and trades below its NAV.

- FRO is not as cheap as a year ago, but it still represents an excellent opportunity for income-minded investors. I give FRO a buy rating.

Introduction

This is my second article on Frontline ( FRO ). It is one of my most significant holdings, and I plan to add even more. The tanker market fundamentals and the Red Sea crisis are strong tailwinds for my thesis. In 3Q23, the company reported a disappointment due to lower day rates 3Q23. The most important is the rise of day rates for Aframax and Suezmax. FRO had contracted for 4Q23 70% of its Aframax and Suezmax ships at 62%/35% higher rates. FRO has a conservative debt repayment schedule over the coming few years. In 1Q24, the company must repay $91 million. The dividends remain attractive, too. FRO still trades below its NAV at 0.84 P/NAV. FRO’s rating remains unchanged; the company is still a buy for me.

Crude tanker market overview

Let's look at the tanker market before jumping to the 3Q23 results preview. The Red Sea crisis is speeding up, China's crude oil inventories are falling, and we enter a strong seasonal period for VLCC.

The crisis in the Middle East unfolds day by day. The last event is the seizure of the tanker St Nicolas by the Iranian Navy. The tanker sails under the flag of the Marshall Islands. It was carrying crude oil from Iraq to Turkey when it was seized and captured by the Iranian Navy in the Gulf of Oman. Approximately 145,000 metric tons of oil, or one million barrels, are transported by the St Nikolas.

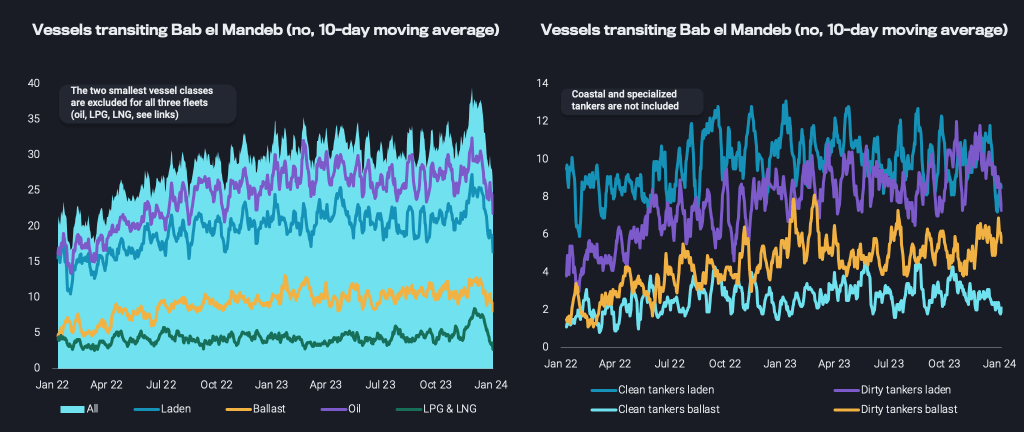

The supply lines are already constrained, and such events add more fuel to the fire. Since the beginning of the crisis, at least eighteen maritime companies have decided to stay away from the Red Sea. This impacts mainly the container ships; freight rates have tripled in a month. However, crude and product tankers are affected, too. Compared to the average for 2023, the number of vessel transits through the area has dropped by almost 15% over the past ten days.

{kind=link}

I assume the disruption is here to stay for longer than we expect. On the other side of the equation, we have China and its growing demand for crude.

China has set import quotas for crude oil totaling 179.01 million metric tons for 2024, up 60% from the previous year. For reference, 111.82 million tons was the limit set in January of the previous year. One of the major Chinese refineries, Zhejiang Petrochemical, was given a 40 million tons quota, meaning the refinery will fully utilize its capacity. Another big private refiner, Shenghong Petrochemical, received 16 million tons.

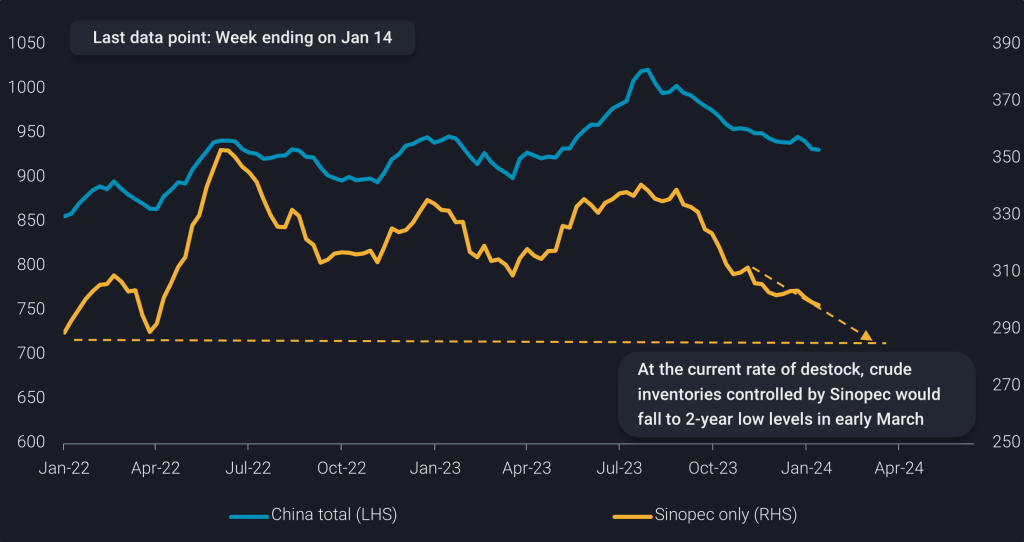

China's crude oil inventories are falling, as seen in the graph below:

{kind=link}

The state owned refinery Sinopec saw its reserves drop below 300 million barrels. Sinopec inventories might reach a two-year low just before regular spring refinery maintenance starts if this trend continues. I expect Sinopec to boost its crude oil purchases to restock its inventories.

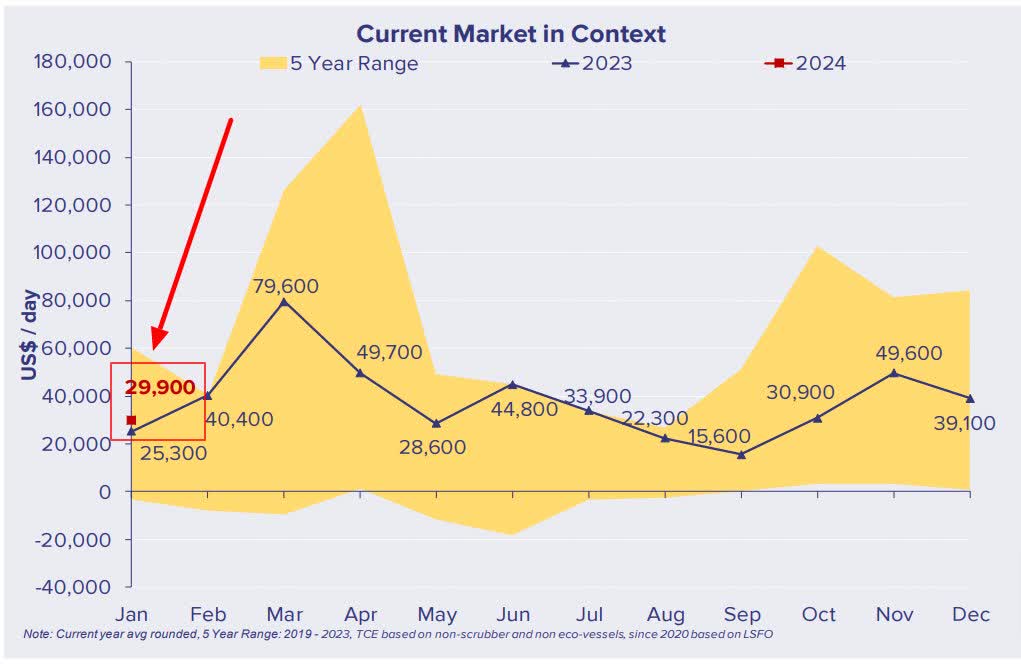

The seasonality supports higher VLCC TCE rates, too.

{kind=link}

We are in the red square on the left with $29,900/day TCE. The upper bound is at $160,000. I am not saying the rates will go there. The present rates offer opportunities with lower downside risk and higher upside.

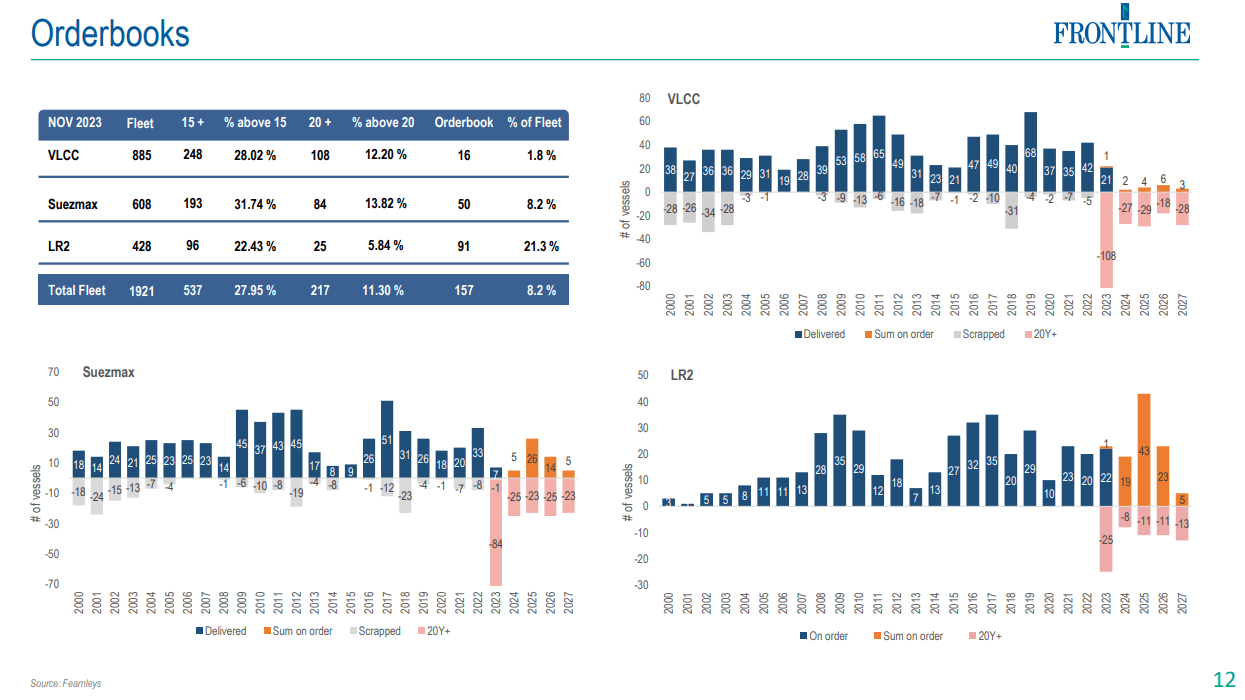

Apart from China and Red Sea development, the supply side in the equation remains limited. The order book stays at record low levels while the crude tankers age.

{kind=link}

VLCC order book is at 1.8%, while the vessels exceeding scrap age (20 years) are at 1.8%. Suezmax's order book is 8.2%, and 20+ older ships represent 13.8% of the fleet. Aframax/LR2 fleet fairs better considering its order book (21.3%) and 5.84% of the ships older than 20 years.

3Q23 preview

The 3Q23 report was disappointing due to lower revenues, EBITDA, and EPS YoY and QoQ. Given the circumstances, I expect better figures in 4Q23. Let’s dig into the details and see why.

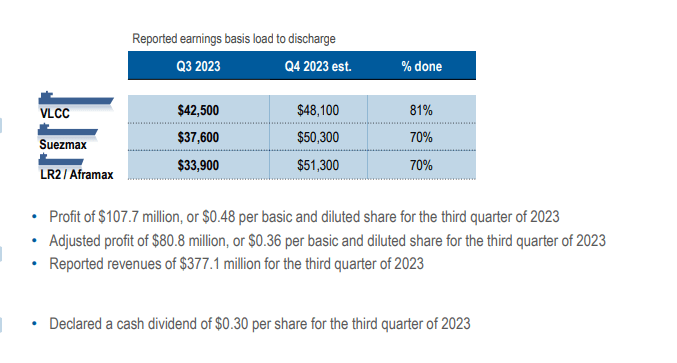

The company`s vessels were contracted at VLCC at $48,100/day, Suezmax at $37,600/day, and LR2/Aframax at $33,900/day. 4Q23 Suezmax and Aframax contracts are at significantly higher rates:

- VLCC: $48,100 per day, 81% of the days were reserved.

- Suezmax: $50,300, 81% of the days were reserved.

- LR2/Aframax: $51,300, 81% of the days were reserved.

{kind=link}

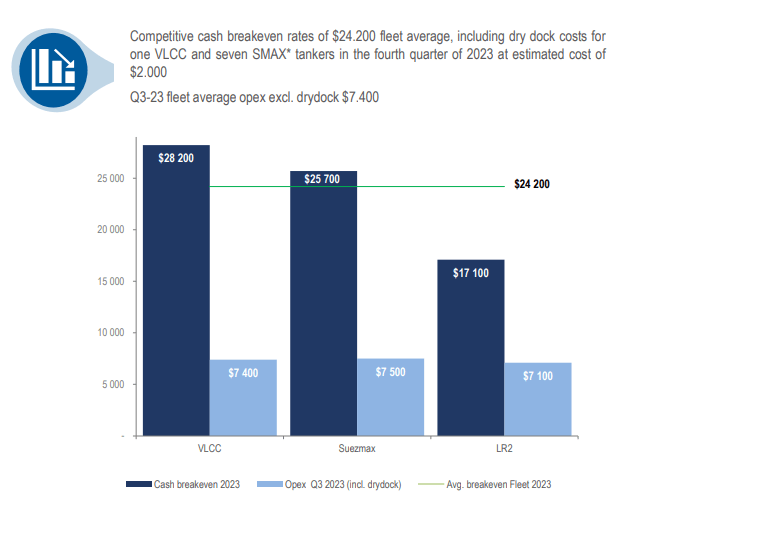

FRO maintained its break-even and operational costs well below the current TCE rates.

{kind=link}

The breakeven for the fleet is as follows: VLCCs $28,200/day, Suezmax $35,700/day, LR2/Aframax $17,100/day. The estimated fleet average is $24,200/day, including dry docking costs for seven Suezmax tankers and one VLCC. The average daily OpEx for the fleet, excluding dry dock, was $7,400. Divided by vessels are VLCCs at $7,400, Suezmax at $7,500, and LR2/Aframax at $7,100, including dry dock costs.

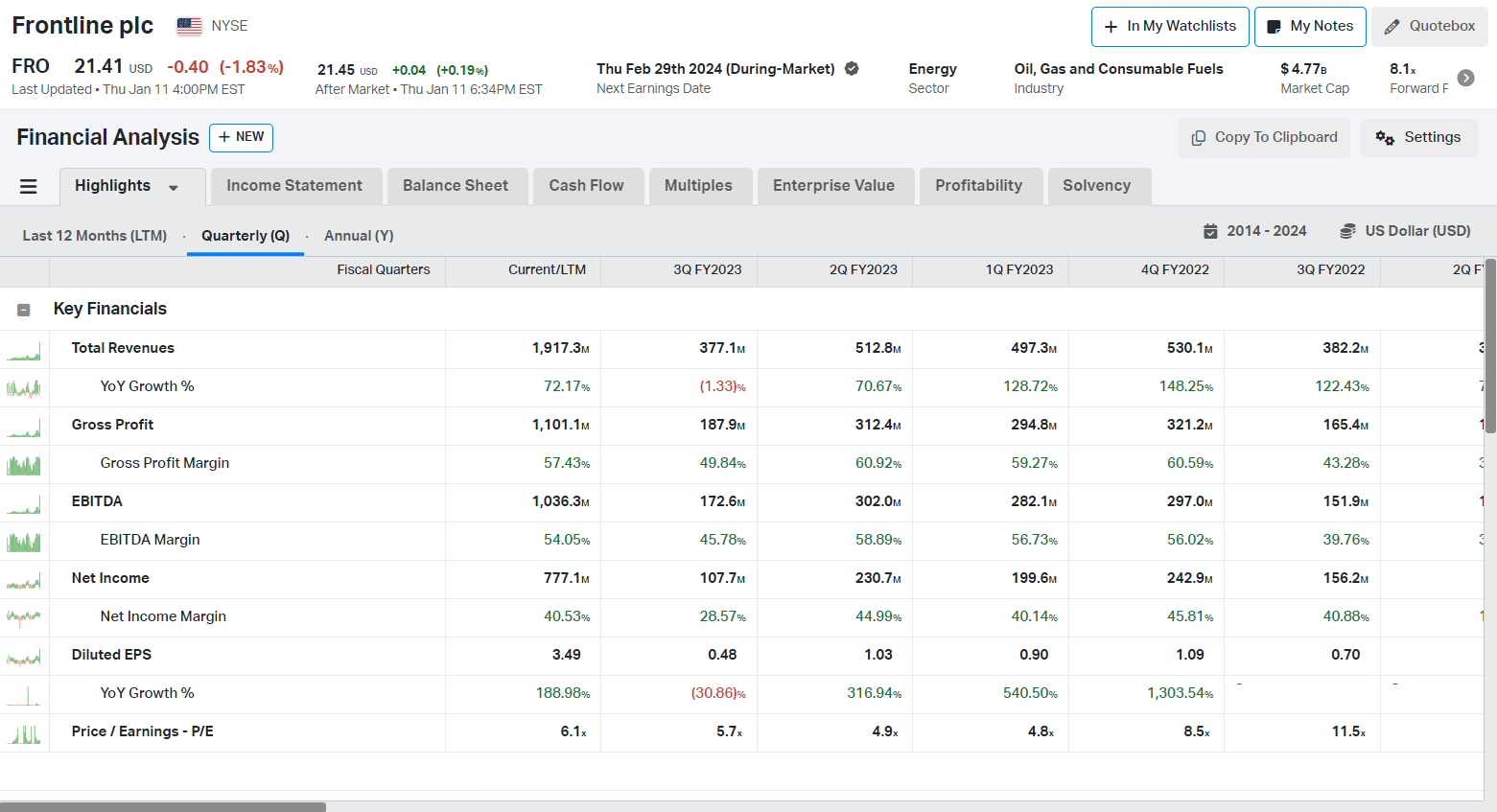

Financially, FRO disappointed investors with declining revenues and profits.

{kind=link}

3Q23 revenue was $377 million, 2% lower YoY and 56% lower QoQ. FRO EBITDA ($173 million) from the same period was not bad compared to 2Q23. 3Q23's net income is $107.7 million, resulting in $0.48 per share.

As of September 30, 2023, FRO has $715 million in cash and equivalents, indicating a healthy position in terms of liquidity. FRO refinanced $91 million in November 2023, and the $75.3 million associated with a credit facility extended until the first quarter of 2026 make up the current long-term debt: no significant debt maturities or pledges to build new structures until 2027.

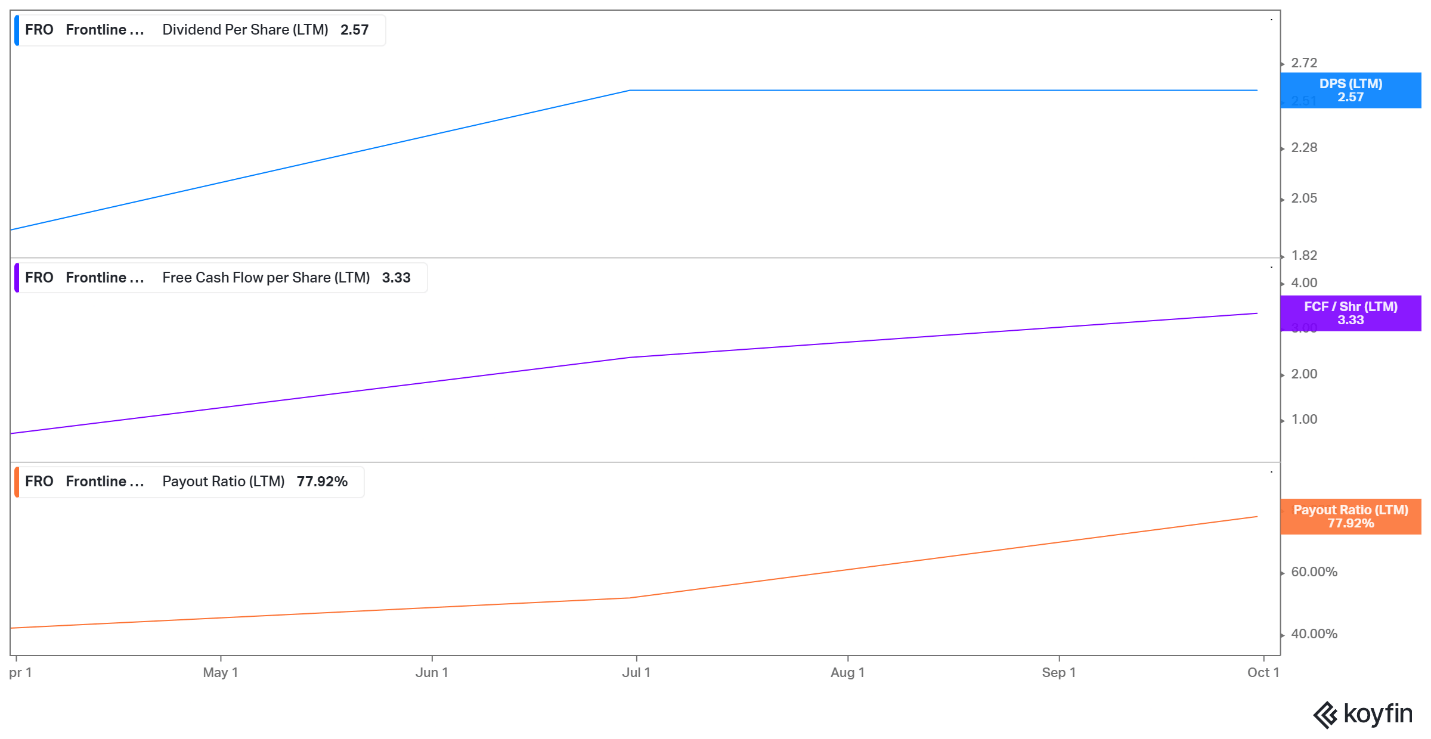

With growing day rates, I expect FRO`s profitability to improve in 2Q23 and 1Q24. The shareholder would continue to get juicy dividends. FRO maintained its yields despite the lower TC rates and declining profits.

{kind=link}

FCF covered dividend payments a few times. FCF per share is $3.33, while the dividends were $2.57. The payout ratio is not excessively high at 77%.

FRO Valuation

To estimate the value of FRO, I use P/NAV and relative valuation. Let’s calculate the first company's net asset value. I picked data from the last Fearnelys report to determine the value of FRO's vessels. The quoted prices are for five- and ten-year-old vessels. Given FRO’s average fleet age of seven years, I use 5% annual depreciation to estimate the price discounting the price of a five-year-old ship.

Frontline fleet consists (excluding Euronav vessels) of 22 VLCC, 25 Suezmax, and 18 Aframax vessels.

The inputs for the NAV equation are as follows:

- VLCC 5Y old $95 million

- Aframax 15Y old, $61 million

- Suezmax 5Y years old, $71 million

- Current Assets: $855 million

- Total Liabilities: $2.374 million

- FRO share price: $21.41

TNK NAV = $5,655 million

P/NAV = 84%

FRO, at the present price, still provides some margin of safety. Another way to estimate how much I pay for FRO is to compare its dividend yields and EV/EBITDA.

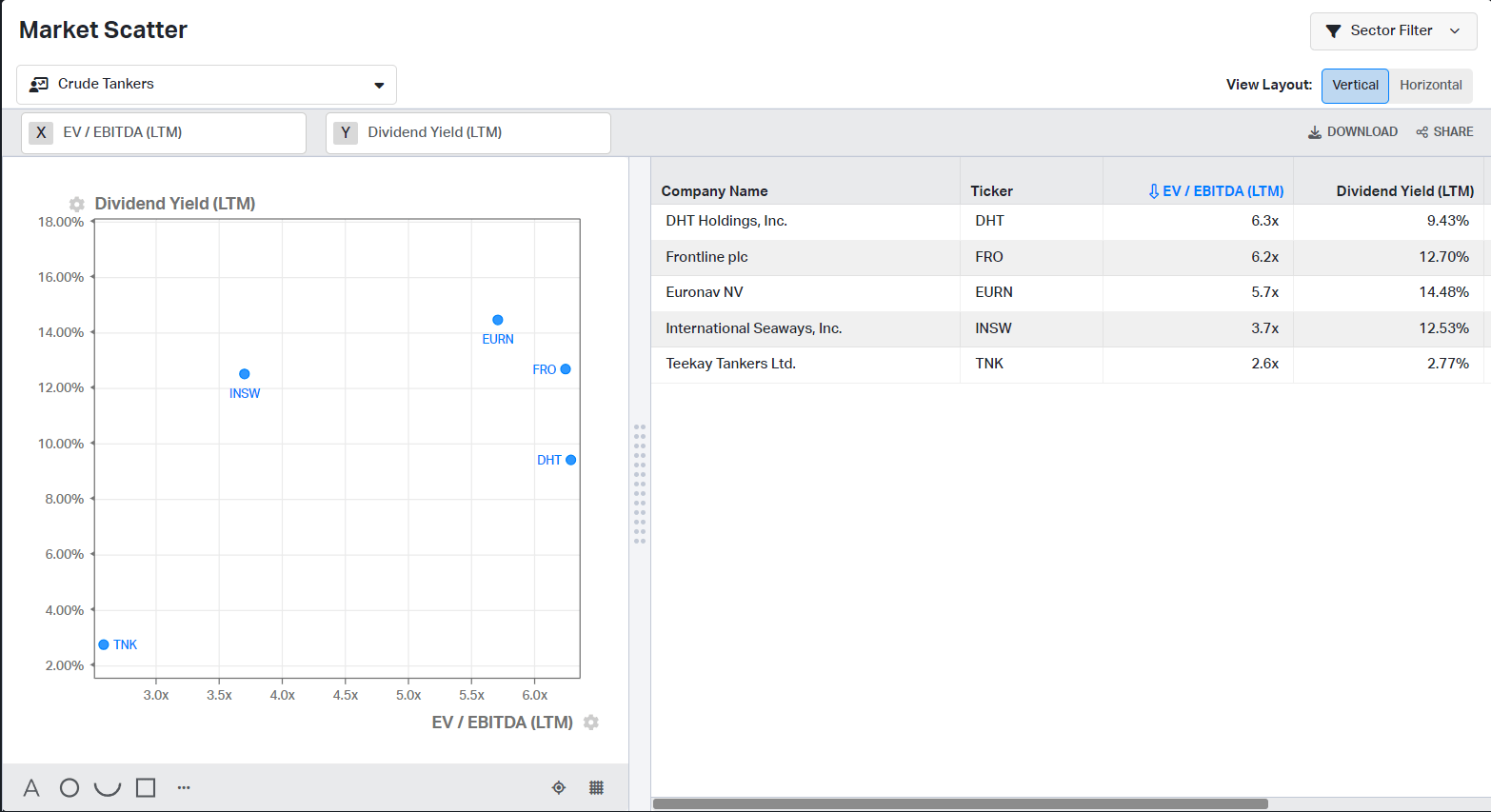

{kind=link}

To obtain a 12.7% yield, we have to pay 6.2 EV/EBITDA. Teekay Tankers ( TNK ) trades at 2.6 EV/EBITDA and delivers 2.77% yields. EURN pays the dividends with the highest yield in the group, although it trades at lower EV/EBITDA compared to FRO. Historically, FRO trades below its EV/EBITDA and EV/Sales.

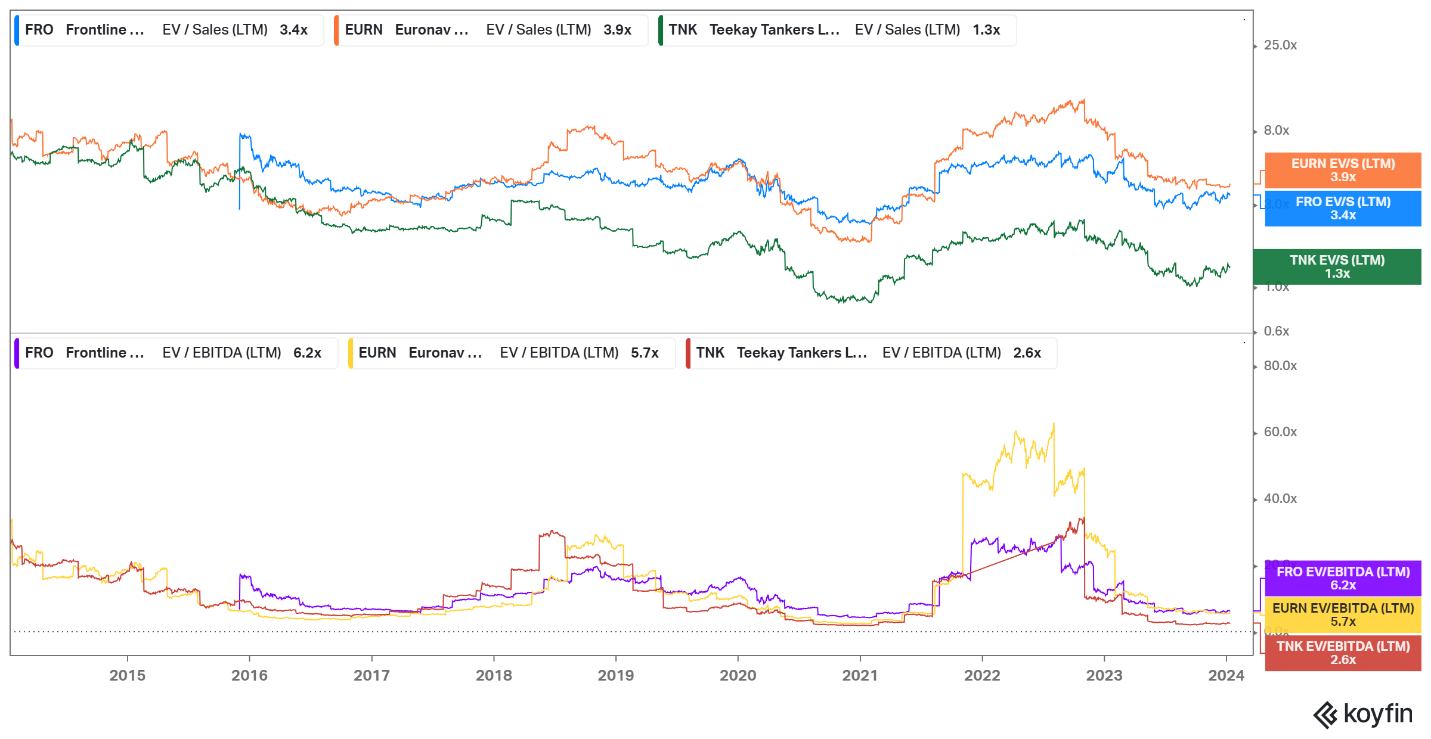

{kind=link}

Over the last ten years, FRO and Euronav ( EURN ) have been shifting places. TNK has been the laggard in the group. FRO commands higher multipoles due to its fleet qualities: size, scrubber-equipped vessels, and average age. Considering its 0.84 P/NAV FRO, it is a good deal. Its stock is not cheap, but it still offers upside potential at this price.

Risks and Investors' Takeaways

FRO keeps on giving to its shareholders. At least, the macro picture remains supportive for higher day rates over the coming few months. China remains the trump card in the equation. I am bullish on China in 2024. However, this is my opinion; the market can prove me wrong. If the Chinese economy suffers another contraction, it will cause a ripple effect across the energy and mining industries. The rising quotas for Chinese crude will boost the demand for crude oil tankers.

The Red Sea crisis, however, will not end any time soon. The asymmetric warfare waged by the Houthis represents an extreme challenge for the US forces. The last event with the St. Nicolas tanker happened in the Strait of Hormuz. The latter is one of the most significant choking points for oil transport. Around 18% of the global oil trade is constrained if blocked. China still imports a lot of Iranian oil. The blockade of Hormuz will push China to seek alternatives. That means longer voyages and higher demand for crude tankers.

FRO is perfectly positioned to benefit in such a scenario. The company has an excellent dividend policy, solid financials, and trades below its NAV. It's not as cheap as a year ago, but it still represents an excellent opportunity for income-minded investors.

For further details see:

Frontline: Still A Buy At The High Price