FRO - Frontline: Trading At Large Premium To Fleet Value

2023-12-11 00:17:24 ET

Summary

- The spot market for tankers remains volatile, as seen in the big sequential decline in FRO's Q3 results.

- Frontline announced the acquisition of 24 VLCCs from Euronav, resolving a long-running dispute.

- The stock is trading at a large premium to the secondary market value of its vessels, limiting the upside.

Back in April , I wrote that Frontline ( FRO ) had been riding some powerful market trends, but I thought the stock was close to fairly valued in normal market conditions. I followed that up in September, saying that its current valuation looked full. Let's catch up on the name after it reported results at the end of November .

Company Profile

As a reminder, FRO operates a fleet of crude oil and refined product tankers that is comprised of 22 VLCCs, 25 Suezmaxes, and 18 LR2/Aframaxes. The fleet has an aggregate capacity of approximately 12.6 million DWT.

Of the vessels it owns, 92% are considered ECO vessels, while 65% of its fleet has scrubbers installed. The average age of its fleet is 6.4 years.

Q3 Results and Vessel Acquisition

With nearly all its revenue coming from the spot market, FRO's results are very tied to time charter rates. While the company got a nice boost last quarter, Q3 saw a big sequential decline.

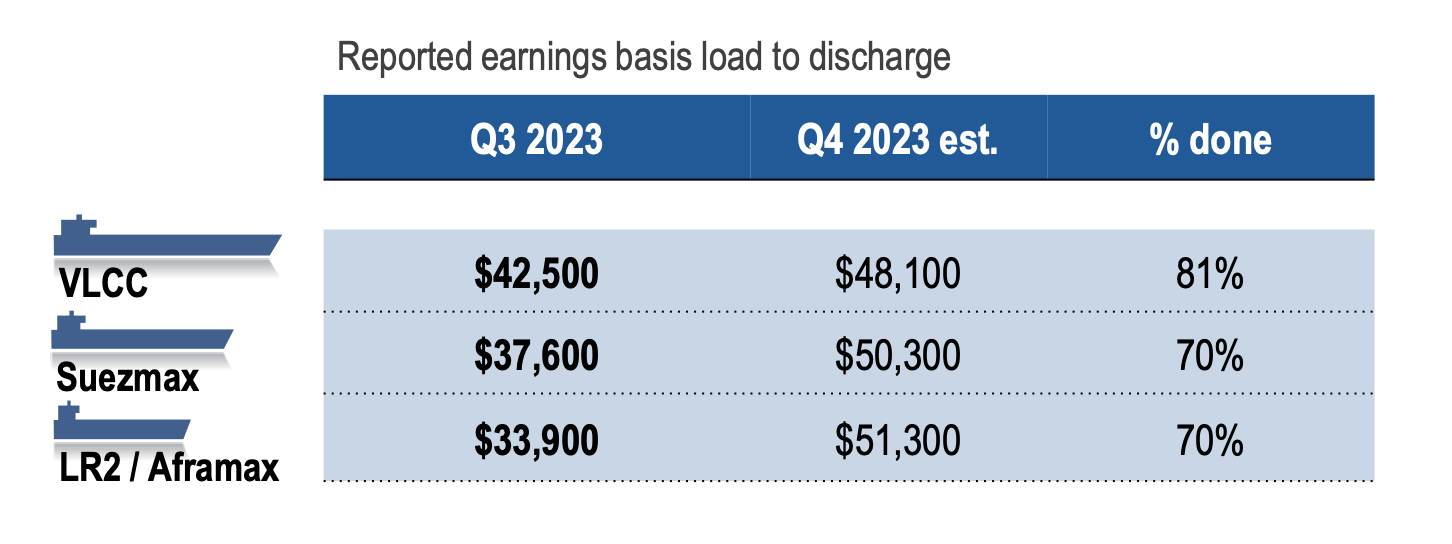

For the quarter, the company realized spot TCE rates of $42,500 for VLCCs, $37,600 for Suezmax tankers, and $33,900 for LR2/Aframax vessels. That's a big drop-off from its Q2 realized spot TCE rates of $64,000 for VLCCs, $61,700 for Suezmax tankers, and $52,900 for LR2/Aframax vessels.

As a result, FRO recorded a net income of $107.7 million, or 48 cents per share. Adjusted EPS came in at 36 cents, missing analyst estimates by 11 cents.

Revenue for the tanker operator edged lower by -1% to $377.1 million.

Adjusted EBITDA rose 17% from $148 million a year ago to $173 million.

The company declared a 30-cent dividend for the third quarter.

Looking ahead, FRO said that 81% of its Q4 TCE rates were done at $48,100 for VLCCs, which is about a 13% increase from Q3. About 70% of Suezmax TCE rates are at $50,300, which is a 34% sequential increase. LR/Aframax TCE rates, meanwhile, are 70% locked in for Q4 at $51,300, a 51% sequential jump.

{kind=link}

Management discussed some of the dynamics impacting the tanker market. Chief among them are G7 price caps and increased scrutiny on vessels that were carrying Russian crude. This led to more vessels returning to the global, non-Russian fleet, which increased vessel supply. Meanwhile, China continued to import more oil as it came out of lockdowns, while the U.S. began to export more oil. U.S. sanctions on Venezuela were also lifted, which will bring new export barrels to the market. OPEC, meanwhile, has continued to look to balance the oil market with production cuts.

Discussing the future environment on its Q3 earnings call , CEO Lars Barstad said:

We've included in this presentation what we call a very long view. And this is kind of an interesting observation, both from a products point of view, but also from a crude point of view. East and West of Suez and how the pipelines of the ocean seem to be stretching. New oil production capacity and shale is contributed from the west of Suez. We've seen Brazil increasing production we've seen the new production coming out of Guyana, we're seeing Venezuelan exports increasing, and we see that shale continue to increase productivity. At the same time, we're seeing a strong refinery capacity to be built up or having been built up and to continue to be built up East of Suez. This would benefit both crude transportation as feedstock into these refineries, and products trade would benefit from this development as the clean product or refined product will flow back west of Suez. And I think it's important to note that the future tanker capacity is not reflecting these projections and the trade extension whatsoever."

FRO also announced that it will acquire 24 VLCCs from Euronav for $2.35 billion. The vessels have an average age of 5.3 years. The bulk of the vessels will be delivered in Q4 with the rest in Q1 of 2024. These vessels will drop the percentage of its fleet with scrubbers from 65% to 57%.

The company has entered into a number of financing agreements to help pay for the acquisition. Most of the debt is variable based on the Secured Overnight Financing Rate ("SOFR") plus a margin.

I was originally expecting a stronger quarter from FRO based on the rates it had locked up for Q3, but a difficult spot market pushed its overall rates considerably lower. However, spot rates remain very volatile, and quickly bounced back in a big way starting in October, especially for smaller Suezmax and Aframax vessels.

The big news, though, is the purchase of vessels from Euronav, which ends a long-running dispute between the two companies as well as Euronav shareholder Compagnie Maritime Belge ("CMB"). FRO nixed a $4.2 billion merger with Euronav in January. FRO will also sell its stake in Euronav to CMB for $252 million. Getting this resolved is a nice positive for the firm.

Valuation

FRO trades at 6.1x the 2023 EBITDA of $986 million. Based on 2025 EBITDA and taking into account the acquisition and its financing, it trades at 5.6x the $1.47 billion estimate.

On a PE basis, it trades at 7.1x EPS estimates of $2.74. Based on the 2024 consensus for EPS of $3.87, it trades at 5.0x and 4.4x the 2025 estimate of $4.42.

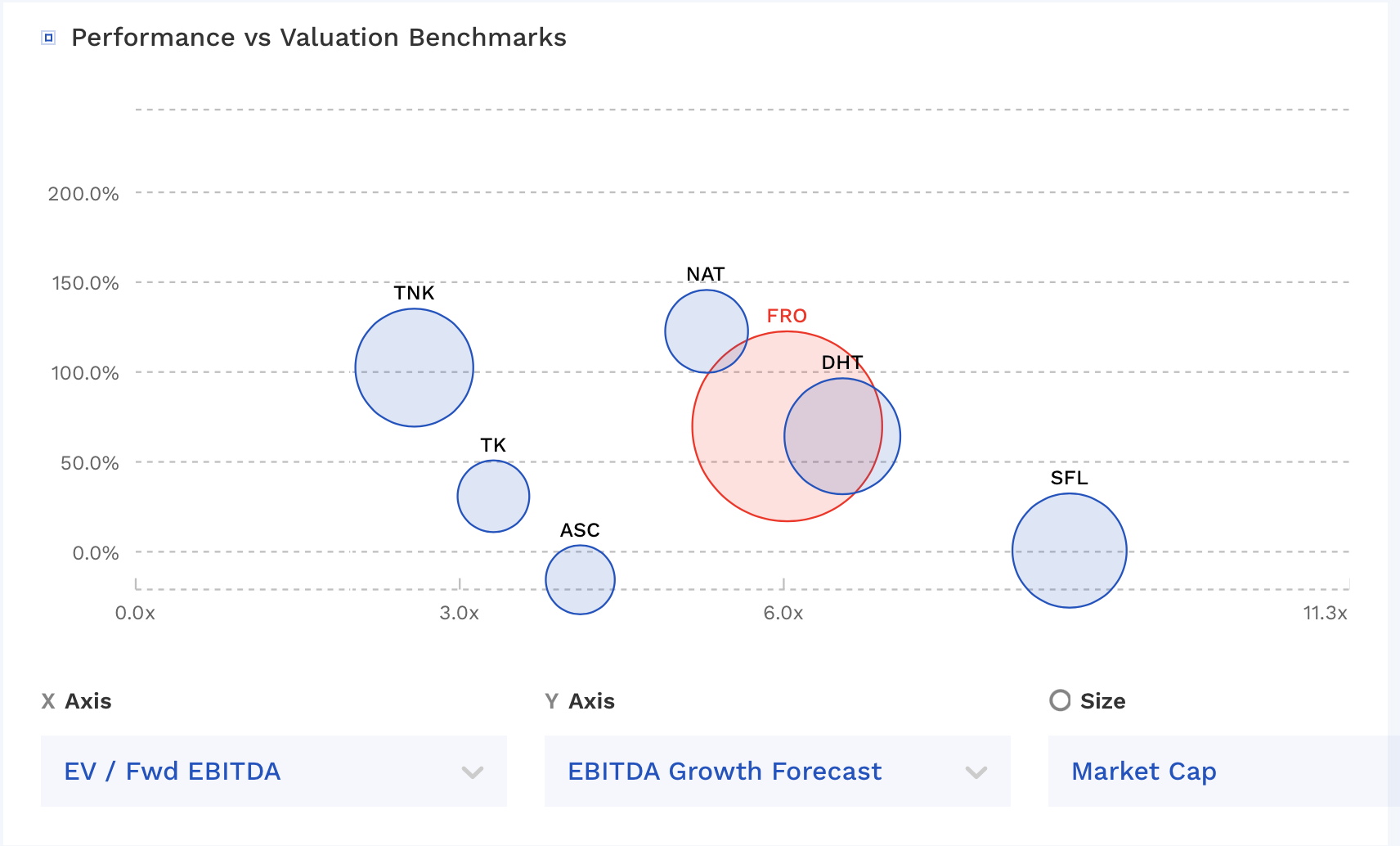

FRO stock trades towards the middle of other marine shipping companies.

{kind=link}

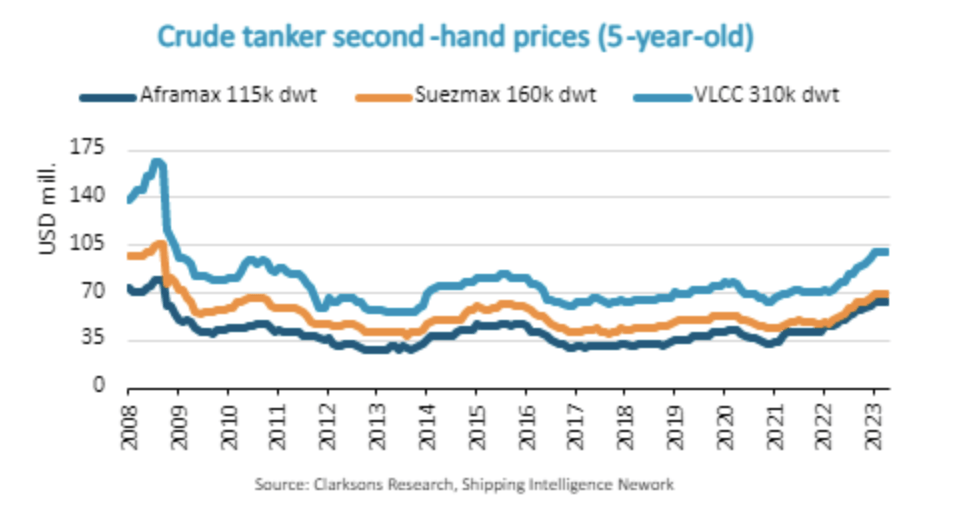

FRO bought 24 vessels at $2.35 billion, or about $98 million each. Based on that valuation, FRO's fleet would be worth $21 per share. However, second-hand Suezmaxes are cheaper, valued at about $68 million and Aframaxes are at around $62 million. That would value its fleet at about $14 per share.

{kind=link}

Conclusion

At the end of the day, FRO is trading at a pretty significant valuation compared to the secondary market value of its fleet. Now it can be argued that it should trade at some type of premium given its relationships and infrastructure, etc., but an over 35% premium seems a bit high. At the very least, it should keep a cap on capital appreciation potential moving forward

The tanker market itself, meanwhile, remains very volatile. There are a lot of moving parts that can impact near-term and longer-term rates. One recent theory is that the Saudis and OPEC could reverse course and try to flood the market with oil to drive down prices and halt U.S. production gains. That would likely be near-term good for spot rates, but a medium-term negative if it hurt Western production and exports.

Regardless, I'm "neutral" on FRO, as I do not think there is much upside given the premium it is already trading at compared to the value of its ships.

For further details see:

Frontline: Trading At Large Premium To Fleet Value