FSK - FS KKR: 13% Distribution Yield Special Distributions And Still Undervalued

2023-11-13 08:45:00 ET

Summary

- BDCs have outperformed other high-yield investments in the rising rate environment, with FSK being one of the most undervalued BDCs.

- FSK reported strong Q3 earnings, with a GAAP EPS beat and growth in NII and book value.

- FSK's high-rate environment has allowed them to issue new debt investments at larger yields, and they continue to deliver significant distributed income to shareholders.

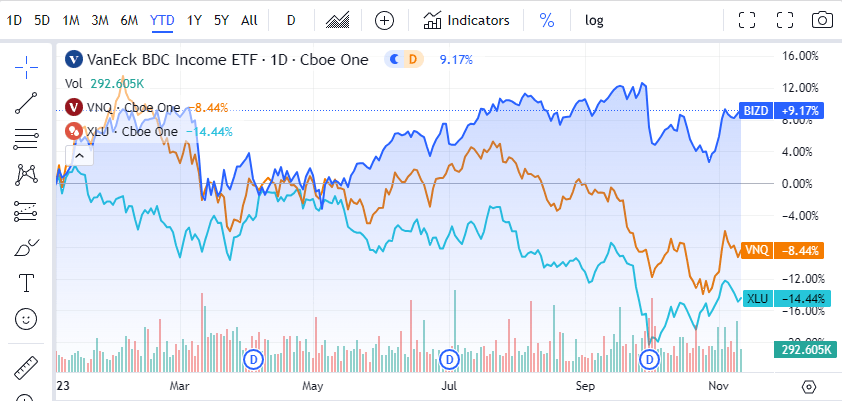

Compared to real estate investment trusts (REITs) business development corporations ((BDC)) are having a good year. Many high-yield investments, from utilities to REITs, have underperformed during the rising rate environment. In 2023, the Utilities Select Sector SPDR ( XLU ) has declined -12.85%, and the Vanguard Real Estate Index Fund ETF ( VNQ ) has fallen -8.44%, while the VanEck Vectors BDC Income ETF ( BIZD ) has increased by 9.17%. FS KKR Capital Corp ( FSK ) is the 2 nd largest holding within BIZD with a portfolio weight of 12.95%, and it’s still one of the most undervalued BDCs I follow. FSK delivered a massive beat in Q3 as their GAAP EPS came in at $0.95 while the street was looking for $0.80. FSK has become an income distribution machine, and the high-rate environment has served them well. After Q3 earnings, I think FSK is one of the most attractive BDCs as they trade at a low market cap to net investment income ((NII)) multiple, trade at a discount to their net asset value ((NII)) and have a dividend yield that exceeds 13%.

{kind=link}

Seeking Alpha

Following up on my previous article on FS KKR

In October, I wrote an article on FSK ( can be read here ) as the distribution yield exceeded 13%. I provided an update on the macroeconomic environment, looked at how FSK benefited from higher rates, and discussed my reasoning for adding to my position. Now that FSK has reported its Q3 earnings along with many of the other large BDCs, including Ares Capital ( ARCC ), I wanted to follow up with a new article and discuss the quarter and why I feel FSK is still grossly undervalued.

FSK produced a big Q3 as the rising rate environment has worked in their favor

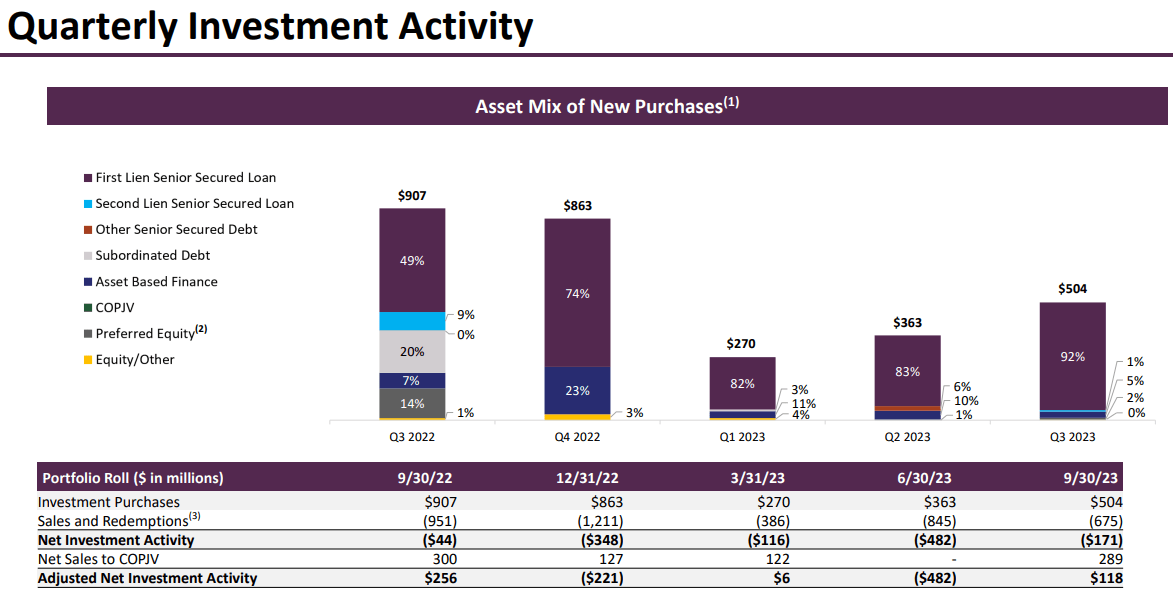

Q3 2023 was a solid quarter for FSK as it delivered $0.95 of GAAP EPS, grew NII by $0.02 QoQ, and increased its book value by $0.20 QoQ. On a per-share basis, FSK generated $0.84 of NII and had a book value of $24.89. In Q2 2023, FSK had an adjusted net realized and unrealized loss of $0.27 per share in Q2 and in Q3, they delivered an adjusted net realized and unrealized gain of $0.14. In Q3, FSK made $504 million of investment purchases and $675 million of sales and repayments, including $289 million of sales to its joint venture Credit Opportunities Partners JV, bringing their adjusted net investment activity to $118. FSK’s total fair value of investments was $14.7 billion, and 68% was invested in senior secured securities. FSK has a weighted average annual yield on accruing debt investments of 12.7%, while its weighted average annual yield on all its debt investments came in at 11.9%.

FSK has grown its portfolio companies to 200 with a median EBITDA of $118 million and a 6x leverage ratio. FSK has issued 88.5% of its interest at a floating rate and 11.5% at a fixed rate. This has allowed FSK to drive its NII per share from $0.76 to $0.84 YoY and get on the positive side of its net realized and unrealized gains. While many investments have been under pressure because of the higher rate environment, BDCs have done well because lending from traditional banks has become increasingly restrictive. BDCs are serving a segment of the business landscape that the banking industry has traditionally underserved, and as rates stay higher for longer, its allowing FSK to issue new debt investments at larger yields. The Fed continues to discuss higher for longer, and while many have predicted rate cuts would have already occurred, the Fed has stayed the course. While many still don’t believe the Fed, if rates do stay higher for longer than the floating rate debt that FSK has on the books, it should help FSK outperform over the next several years.

{kind=link}

FS KKR

BDCs are considered income investments, and FSK delivers significant distributed income to shareholders. FSK declared its Q4 distribution of $0.70 per share, consisting of a base distribution of $0.64 per share and a supplemental distribution of $0.06 per share. FSK is also paying the previously announced $0.05 special distribution, bringing their quarterly distributed income to $0.75 per share. This will be paid at the beginning of January to shareholders of record on December 13 th . The board has also approved another special distribution totaling $0.10 for the first half of 2024. This will be paid in two installments, the first coming in February of $0.05, and the second $0.05 distribution will be paid in May. FSK continues to perform on an operating level and rewards shareholders through a growing-based distribution while augmenting the income with supplemental and special distributions.

{kind=link}

Seeking Alpha

FSK still looks like an opportunity as it is undervalued compared to its peers

I am invested in several BDCs and update several metrics on a quarterly basis. Of the 11 BDCs I follow, 8 have reported their Q3 earnings. I look at their market cap to NII multiple, discount or premium to NAV, and dividend yield. Below are the BDC’s I follow and the overall grid sorted by NII generated.

- FS KKR Capital Corp ((FSK))

- Prospect Capital Corporation ( PSEC )

- Barings BDC ( BBDC )

- Main Street Capital ( MAIN )

- Blue Owl Capital Corporation ( OBDC )

- MidCap Financial Investment Corporation ( MFIC )

- Goldman Sachs BDC ( GSBD )

- Oaktree Specialty Lending Corporation ( OCSL )

- Golub Capital BDC ( GBDC )

- Ares Capital ((ARCC))

- Gladstone Investment ( GAIN )

{kind=link}

Steven Fiorillo, Seeking Alpha

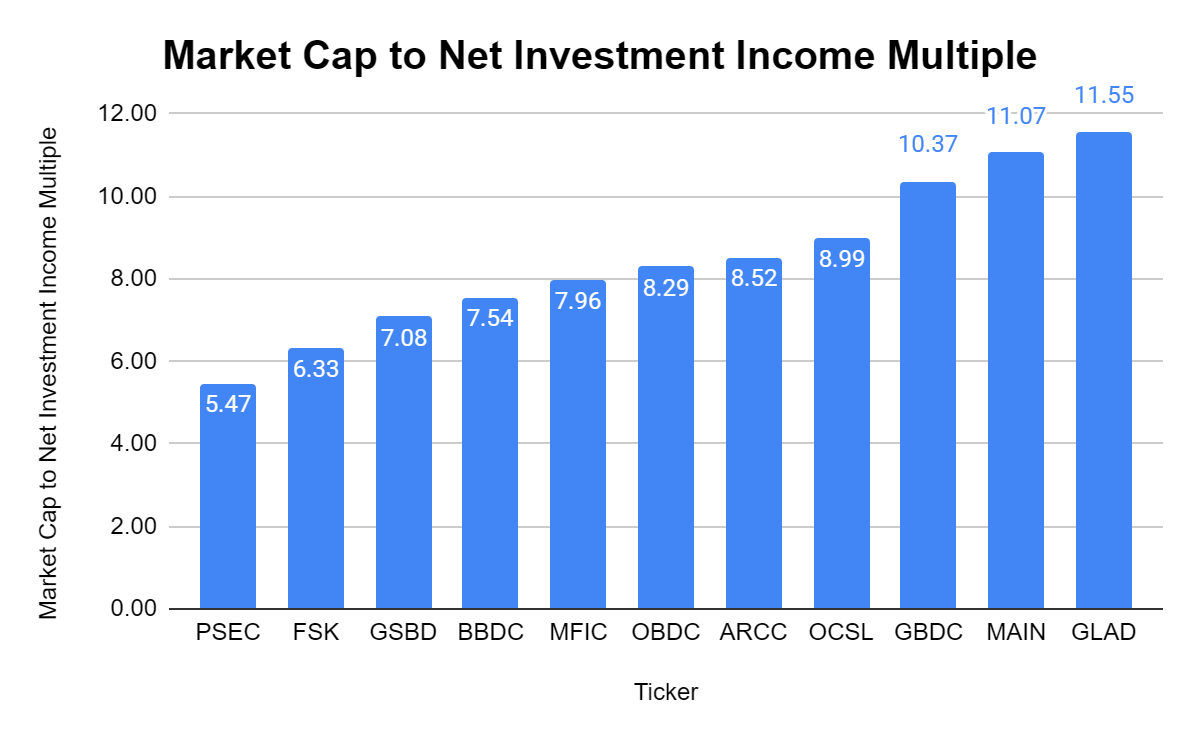

The first thing I look at is the market cap to NII multiple Mr. Market has placed on each of these BDCs. I want to pay the best possible price for a BDCs NII, and while I am willing to pay a slight premium for a great company, I would rather get a great company at a bargain. The average market cap to NII multiple in this peer group is 8.47x, and FSK is trading at 6.33x. FSK is still being undervalued based on its market cap to NII. FSK has also generated the 2 nd largest amount of NII in the peer group at $877 million on a trailing twelve-month ((TTM)) basis.

{kind=link}

Steven Fiorillo, Seeking Alpha

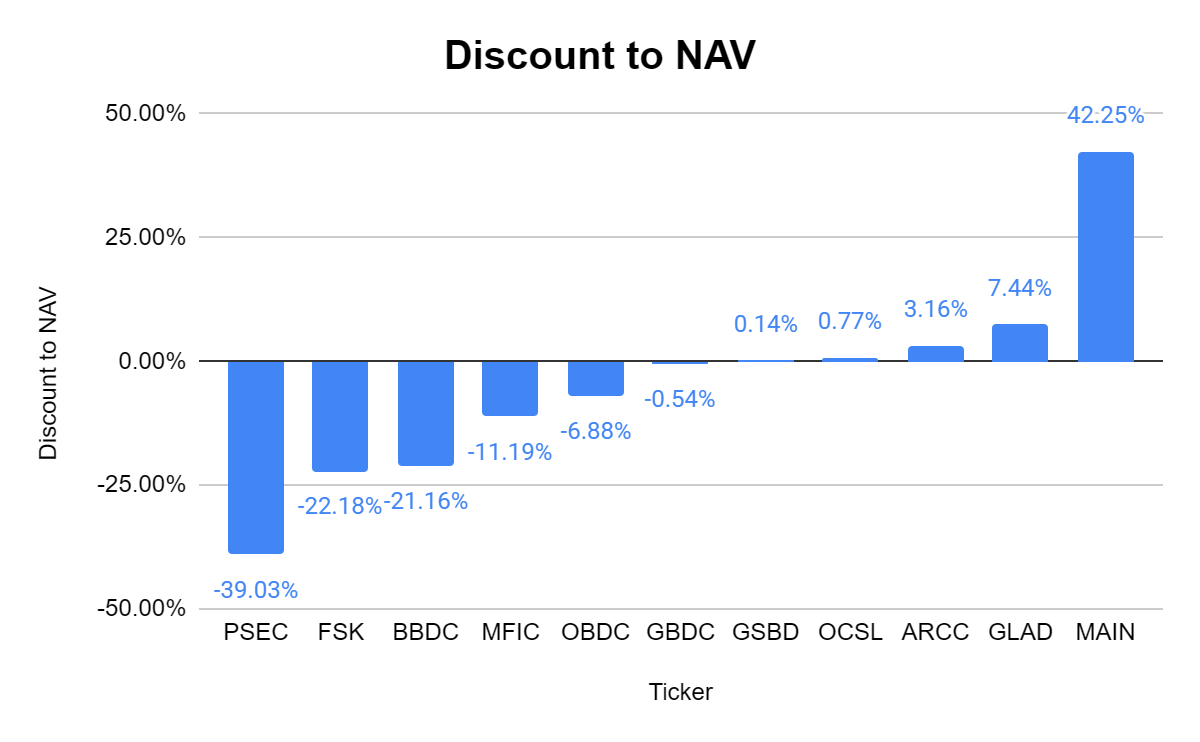

To help validate my thesis on whether a company is undervalued or trading at a premium, I look at its share price compared to its NAV. I recently added shares of ARCC when it dipped because they were trading at less than a 1% premium to NAV, and for ARCC, whenever it trades at a slim spread, I try to add to my position. Today, the average BDC I follow trades at a -4.29% discount. FSK is being deeply discounted compared to its peers as it trades at a -22.18% discount to its NAV. This is intriguing because I can pay the 2nd lowest multiple for FSK’s NII and get their net assets at a double-digit discount.

{kind=link}

Steven Fiorillo, Seeking Alpha

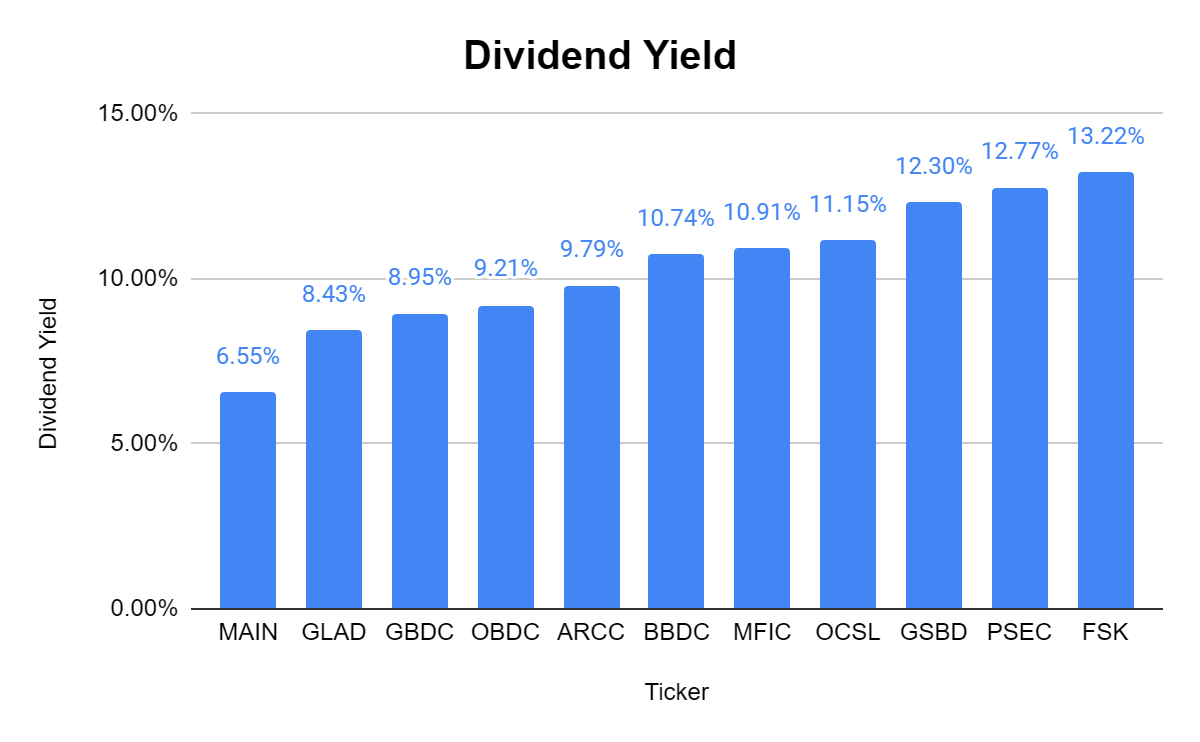

While the valuation metrics are very interesting, I am shocked that FSK has the largest yield without even incorporating the supplemental and special distributions. The average yield of the peer group is 10.36%, and FSK has a yield of 13.22%. It’s hard to look past this because when I add in the additional income that FSK generates, the yield jumps past 15%.

{kind=link}

Steven Fiorillo, Seeking Alpha

Conclusion

I think that BDCs will continue to do well into the end of 2023 and throughout 2024. The Fed hasn’t caved, and while we could see a pivot in the first half of 2024, I think we will see rates higher for longer. FSK is delivering on an operational level and making strong strategic investments that should continue generating solid NII going forward. I think there are several interesting investments in the BDC sector, but FSK continues to look undervalued. FSK is the 3 rd largest BDC by market cap, yet it generates the 2 nd largest amount of NII. At its current valuation, you can pay 6.33x its NII, get its NAV at a -22.18% discount, and lock in a 13.22% yield before the special or supplemental distributions. There is a good chance I will increase my position in FSK this week for the Dividend Harvesting Series ( can be read here ) on Seeking Alpha.

For further details see:

FS KKR: 13% Distribution Yield, Special Distributions, And Still Undervalued