FSK - FS KKR Capital: A Christmas Gift With A 13% Yield

2023-12-09 00:10:14 ET

Summary

- FS KKR Capital is trading at a 20% discount to net asset value despite strong growth in net investment income in the last year.

- The BDC has a well-diversified portfolio focused on senior secured loans and a joint venture with similar assets.

- The dividend is well-supported by NII, but there is a risk from the Fed ending its tightening policy.

The third-largest BDC in the market, FS KKR Capital ( FSK ), is trading at an unreasonably large discount to net asset value, despite management doing a solid job in growing its NII. The BDC is focused on senior secured loans, has good portfolio diversification and grows its income consistently. Despite those accomplishments, FS KKR Capital’s shares are priced at a 20% discount to net asset value. I see potential for the gap between net asset value and share price to close over the long term if the BDC can maintain its current level of dividend coverage. As a result, I believe FSK has up to 24% revaluation potential and that the risk profile for FS KKR Capital is favorable!

Previous rating

I worked on FS KKR Capital about two-and-a-half years ago, in March 2021 -- Merger Provides Unique Opportunity To Correct Undervaluation -- which is when I recommended the BDC for dividend investors. The merger between FS KKR Capital Corp. I and FS KKR Capital Corp. II made FS KKR Capital the third-largest BDC in the industry, after Ares Capital ( ARCC ) and Blue Owl Capital ( OBDC ). Given that the BDC’s shares trade at an unreasonably large discount to net asset value, I believe FSK remains a buy for dividend investors.

A well-oriented portfolio following a senior focused investment strategy

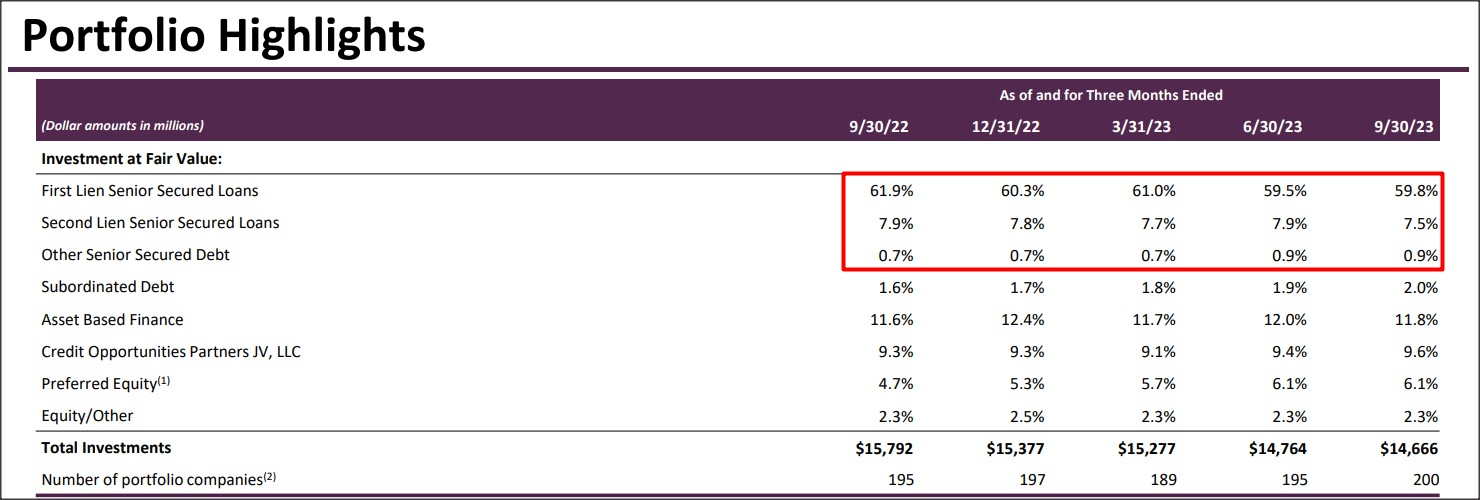

FS KKR Capital invests chiefly in first and second lien senior secured notes as well as other senior secured debt. At the end of the September quarter, these three most heavily weighted debt investments had shares in the BDC’s portfolio of 60%, 8% and 1%... and they remained fairly consistent investment percentages in the last year. FS KKR Capital had investments worth $14.7B on its balance sheet, showing a $1.1B decline over the year-earlier period and the decline is due to a slowdown in lending activity in a high-rate world.

{kind=link}

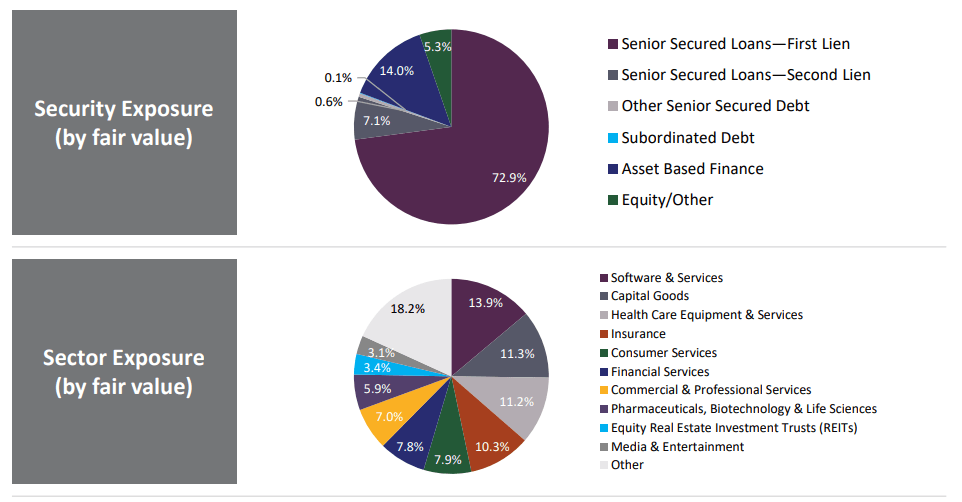

As far as diversification and portfolio risks are concerned, I don’t see any weaker diversification metrics than I do with other BDCs. Key target industries for FS KKR Capital include recession-resistant industries like Software, Capital Goods, Health Care, Insurance and Financial Services which offer stable revenue and cash flow prospects even during recessions.

FS KKR Capital

A unique element of FS KKR Capital is that the BDC has an equity ownership in a major joint venture, called Credit Opportunities Partners JV, with the South Carolina Retirement Systems Group Trust being its partner. The joint venture (in which FS KKR Capital has an 87.5% equity ownership) is a mini-BDC itself which follows a senior secured investment strategy like FS KKR Capital and accounted for roughly 10% of its investments. The mini-BDC had $3.4B in investable assets and, compared to FS KKR Capital, the JV's first liens were even more heavily weighed with a share of 73%.

{kind=link}

NII trend and dividend coverage look promising

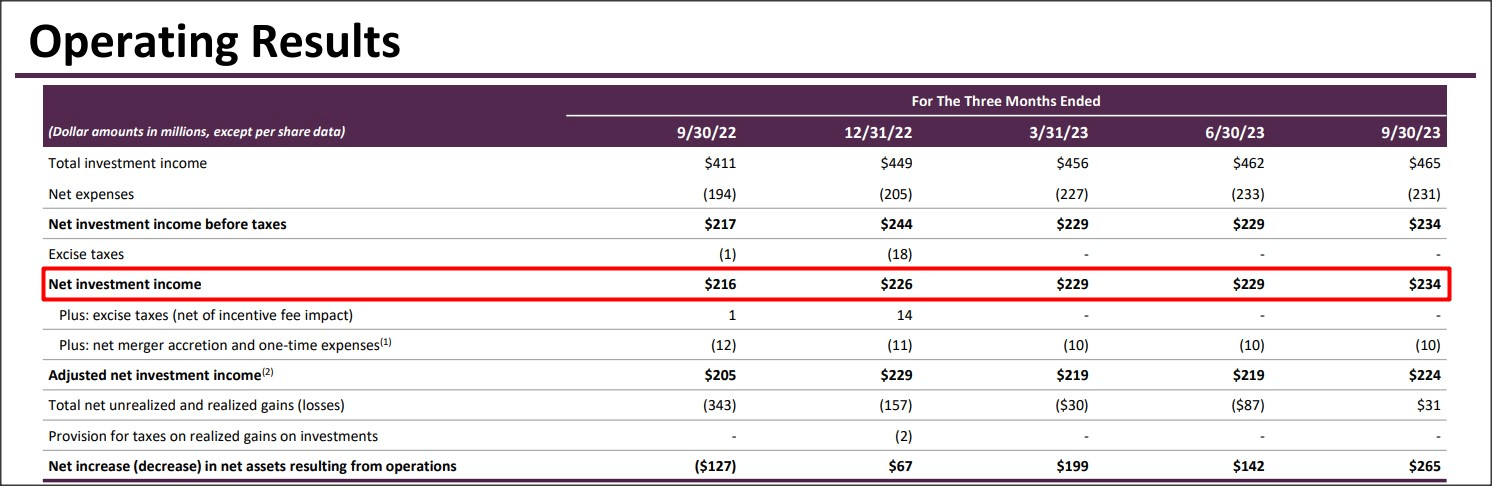

Although FS KKR Capital has seen a decline in its total investments in the last year, the BDC managed to capture higher net investment income from its assets. The investment firm generated $234M in net investment income in the third-quarter, showing 8% year over year growth and the trend in NII has been a positive one throughout FY 2023: FS KKR Capital’s NII grew, on a sequential basis, in three quarters (one was a "flat" quarter with 0% Q/Q NII growth) in the last year, driven by higher income generated by its rate-sensitive debt investments.

{kind=link}

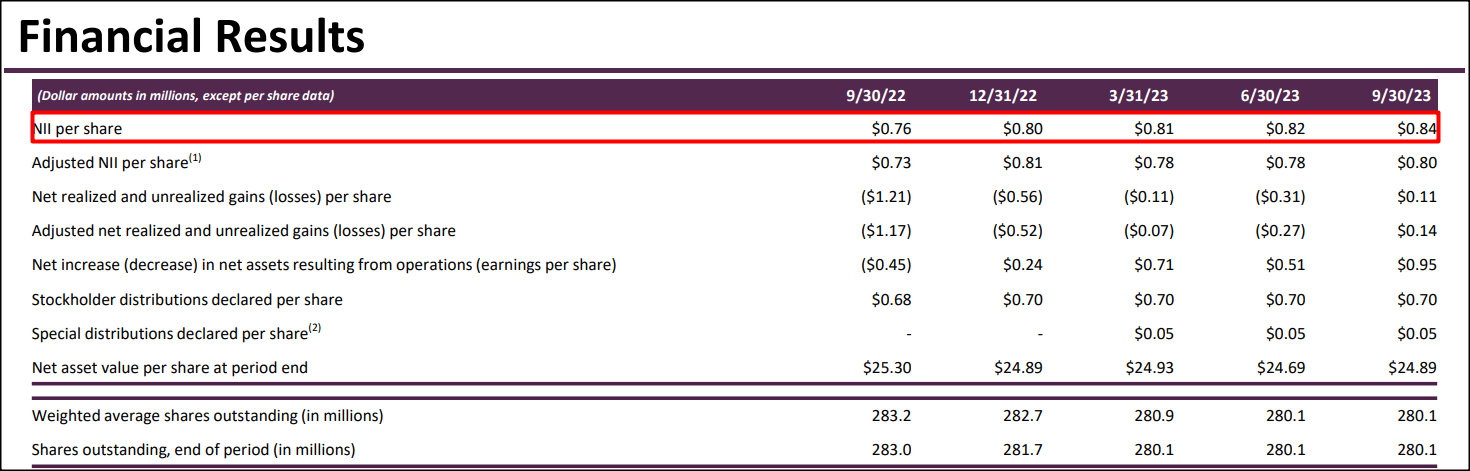

I use GAAP net investment income to calculate the firm's dividend coverage, not adjusted net investment income. The latter accounts for a BDC's merger effects and excise taxes. Based off of GAAP net investment income, which is more comparable figure, FS KKR Capital has good dividend coverage: the BDC generated $0.84 per-share in net investment income in Q3’23 and $2.47 per-share in the first nine months of the year which calculates to dividend coverage ratios of 112% and 110%.

{kind=link}

13% yielding FS KKR Capital is a bargain...

FS KKR Capital Corp. is trading at a large, and in my opinion difficult-to-understand, 20% discount to net asset value despite offering what most other BDCs offer: a senior secured debt investment approach (including JV investments), a well-structured debt portfolio and rather good dividend coverage.

FS KKR Capital, despite being the third-largest BDC by market cap, is valued at a much lower price-to-NAV ratio than its BDC rivals Ares Capital and Blue Owl Capital are.

If FS KKR Capital can consistently deliver dividend growth and provide good coverage (110%+), I believe the gap between share price and net asset value could ultimately diminish. My fair value estimate for FSK is $24.89 (the firm's net asset value) and I see 24% revaluation potential for FS KKR Capital in the long term.

Risks with FS KKR Capital

Even if the gap between share price and net asset value doesn’t close, FS KKR Capital’s 13% dividend is attractive and well-supported by NII. The BDC, however, has about 89% of its assets invested in debt that pays a variable rate... meaning FS KKR Capital’s NII is vulnerable to the Fed ending its tightening policy.

Final thoughts

I don’t see why FS KKR Capital’s shares should trade at a 20% discount to net asset value, especially because the BDC supports its dividend with NII, the portfolio is well-structured and the firm has paid $0.15 per-share in additional, non-recurring dividends (which were included in the dividend coverage calculation).

There are BDCs that have higher percentages of first liens than FS KKR Capital, but I believe the portfolio itself is well-balanced and the JV investment with South Carolina Retirement Systems Group Trust includes additional senior secured assets in addition to the 69% senior secured asset percentage reported on the BDC portfolio level. In my opinion, the 20% discount to net asset is excessive, especially when compared against Ares Capital and Blue Owl Rock!

For further details see:

FS KKR Capital: A Christmas Gift With A 13% Yield