FSK - FS KKR Capital: The 13% Dividend Is Not As Juicy As You May Think

2023-07-14 08:57:38 ET

Summary

- FS KKR Capital Corp. is a $5.5 billion business development company focusing on providing tailored credit solutions to privately-held middle market companies in the United States.

- By most of the business metrics I looked at in my today's article, FSK KKR looks very stable.

- But given the nature of its portfolio and its debt, I think the recession, I expect in late 2023 or early 2024, will hit the company's bottom line hard.

- When I weigh the dividend yields against the leverage ratios of FSK and its peers, I conclude that this BDC is currently fairly valued.

- I rate FSK stock as a "Hold." Over the long term, you may like the yield. But there should be even better entry points.

The Company

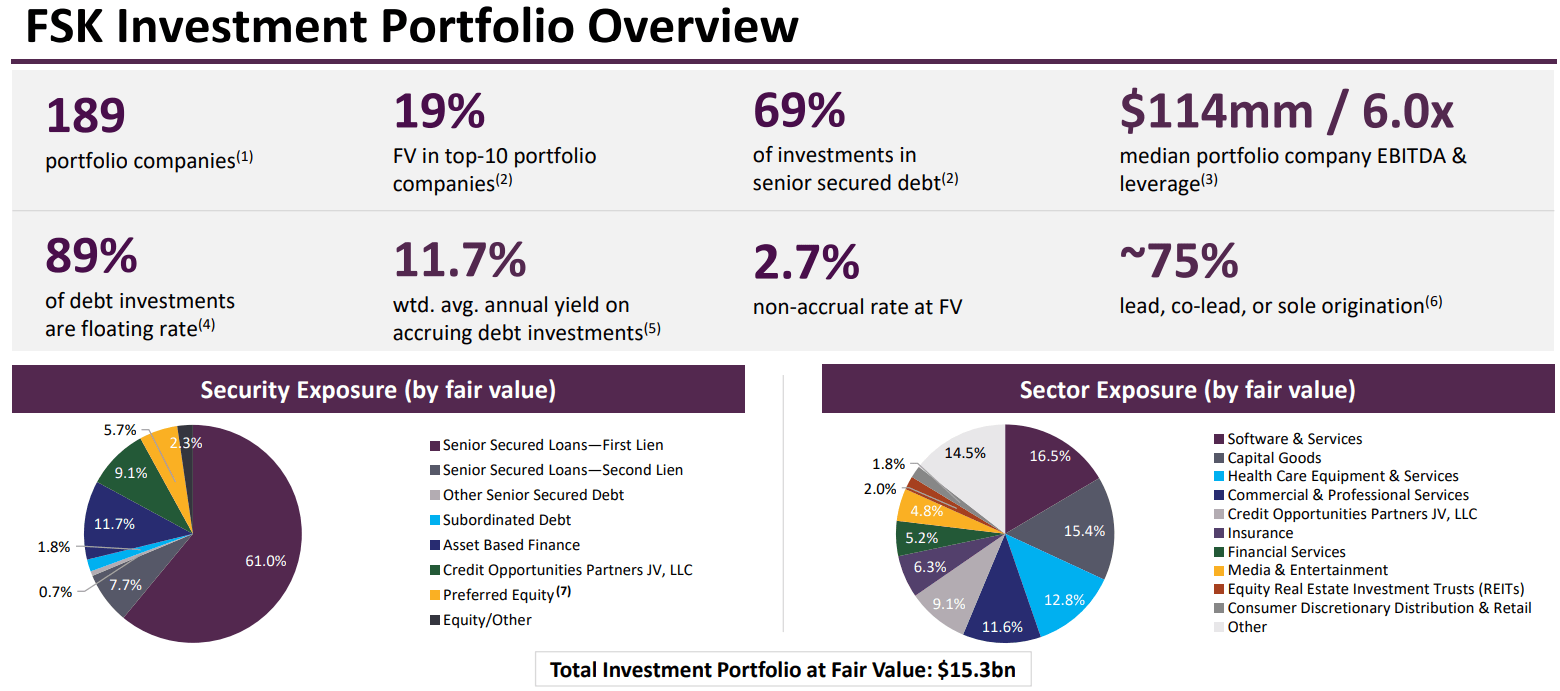

According to Seeking Alpha, FS KKR Capital Corp. (FSK) is a $5.5-billion business development company focusing on providing tailored credit solutions to privately-held middle market companies in the United States. The company primarily invests in senior secured debt, with a smaller portion allocated to subordinated debt. These investments are acquired through secondary market transactions or directly from target companies. They also invest in first-lien senior secured loans, second-lien secured loans, and occasionally subordinated or mezzanine loans. In addition to debt investments, the company may receive equity interests such as warrants or options. They also purchase minority interests in common or preferred equity, either in conjunction with debt investments or through co-investments with financial sponsors.

Their main focus is on private upper-middle market companies with annual EBITDA between $50 million and $100 million at the time of investment - no start-ups, turnaround situations, or companies with speculative business plans. The company aims to exit its investments by selling them in a privately negotiated over-the-counter [OTC] market.

{kind=link}

{kind=link}

Despite some volatility in the market, FS KKR's investment team originated approximately $270 million of new investments during the latest quarter [Q1 FY23]. While M&A transaction volumes were expected to remain below average, activity levels and inquiries began ramping up in recent weeks of the quarter, indicating potential opportunities in the market.

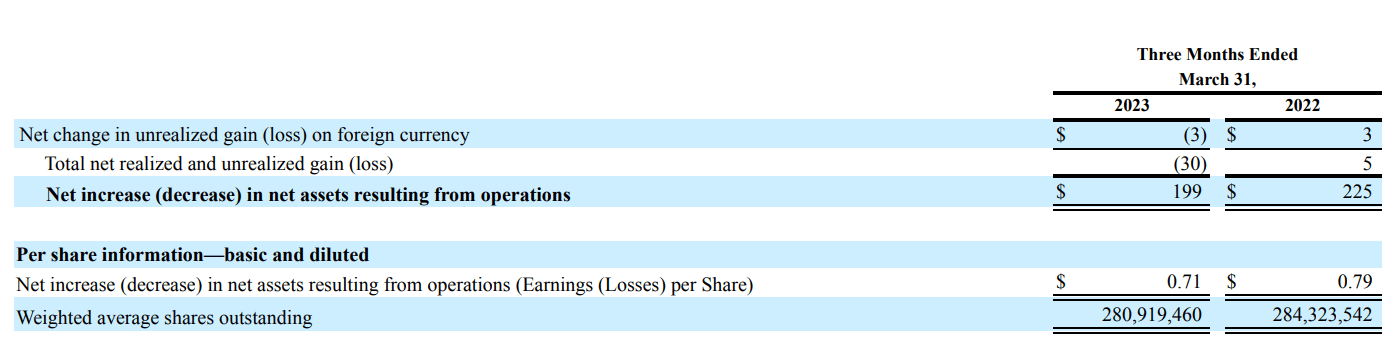

FSK delivered strong operating results in Q1 FY2023 as far as I see it. Rising loan lending rates enabled the company to significantly increase its total interest income [+25.3% YoY], which became the main growth driver of total investment income [+15.15% YoY]. However, rising market rates also had a negative impact - FSK's net expenses increased by almost 29% YoY in Q1. However, the overall change in net income was approximately 4.1% YoY, which was sufficient to exceed market expectations on a per-share basis. Adjusted net investment income also exceeded expectations at $0.78 per share.

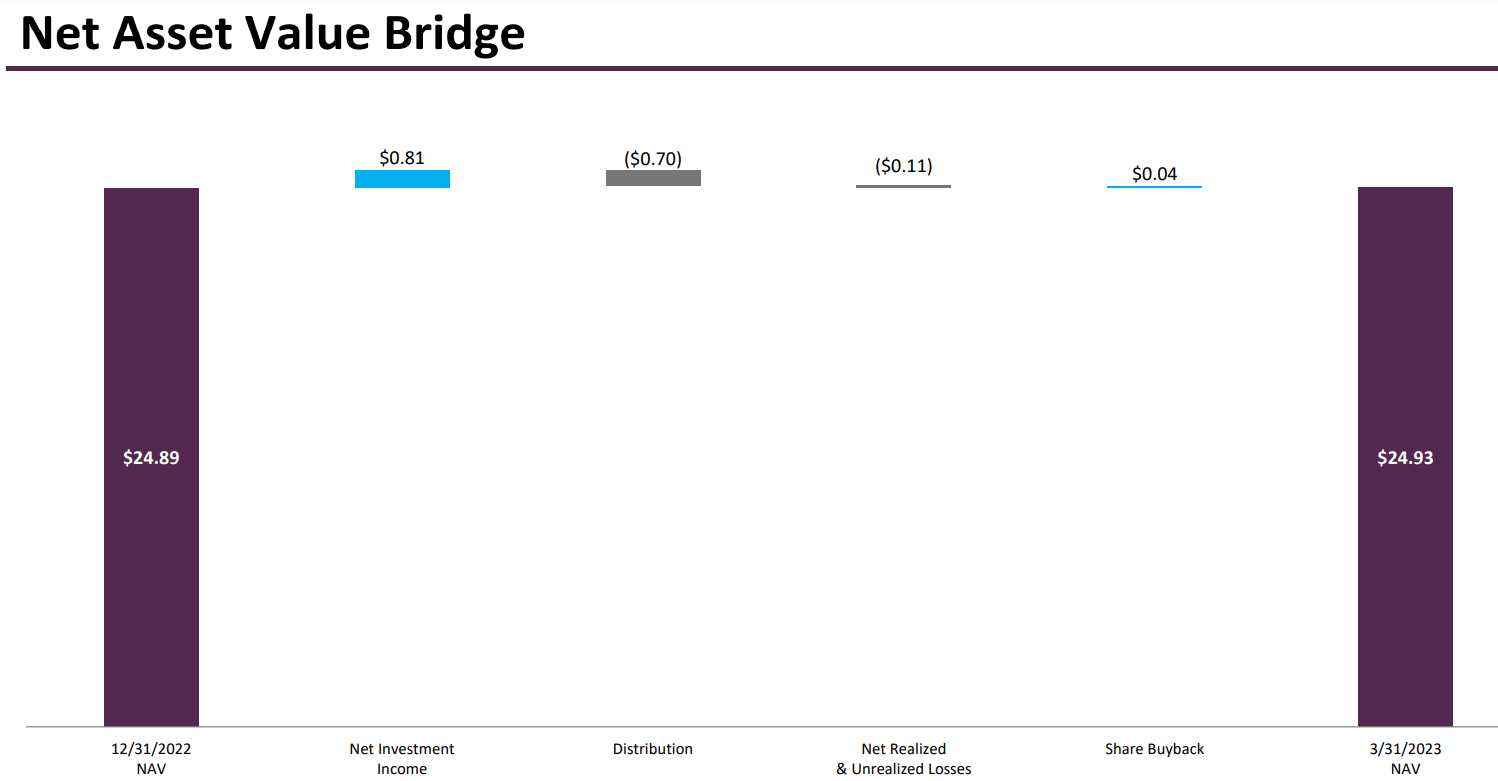

The company's NAV managed to grow slightly despite all the difficulties:

{kind=link}

The company ended the quarter with ~$3 billion of available liquidity - that's over 54% of the whole market cap. In March 2023, it completed the remaining portion of its previously committed $100 million share repurchase program, repurchasing ~$32 million worth of shares. The share count is therefore reduced by ~1.19% on a YoY basis:

{kind=link}

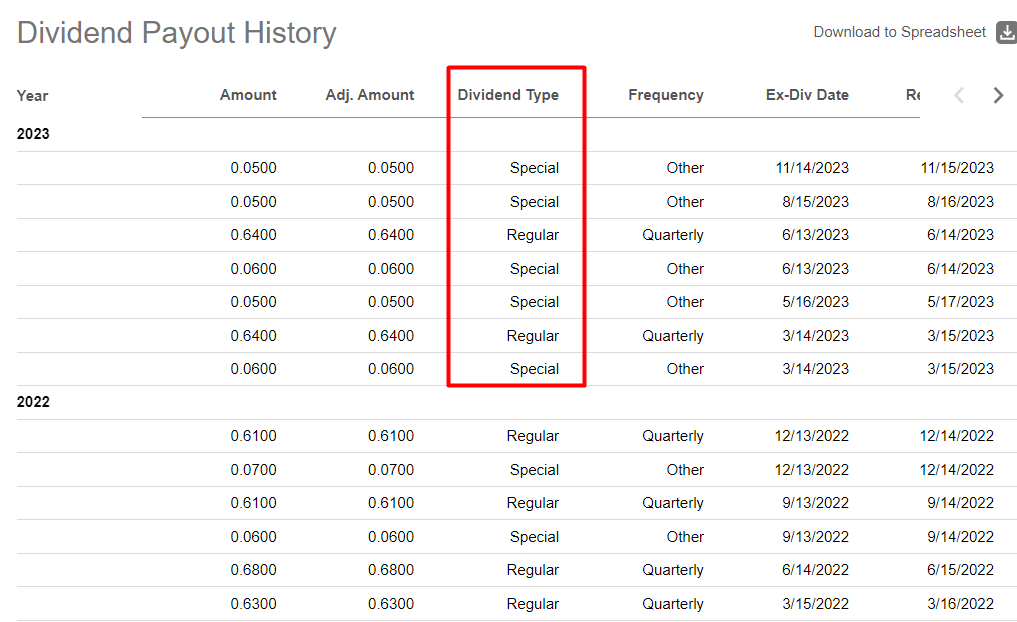

As for dividends, based on strong financial results, the company expects investors to receive a total of at least $2.95 per share in distributions this year. On an annualized basis at the current share price, this translates to a dividend yield of about 15.02% over yesterday's FSK closing price. Although, of course, we cannot simply extrapolate this yield, as it consists in part of special dividends already paid , which have already been announced and paid several times:

{kind=link}

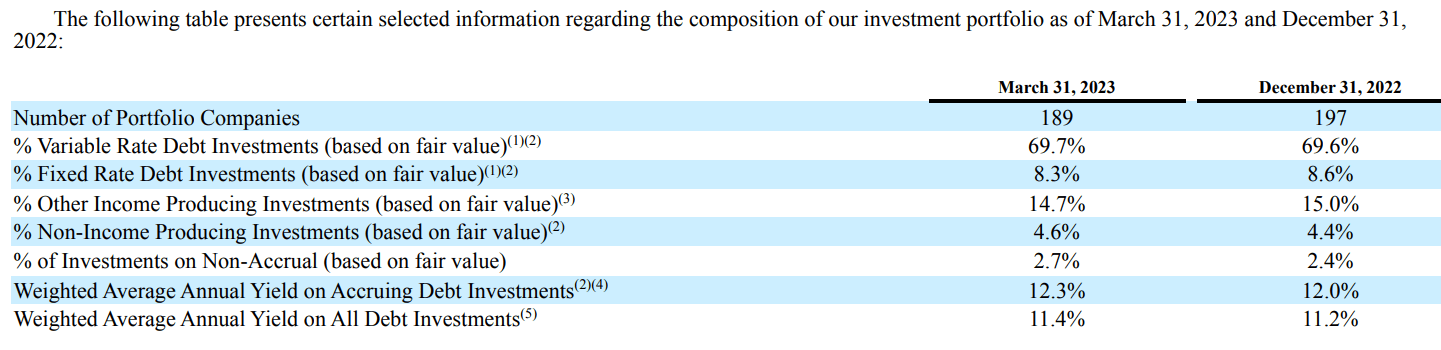

As I learned from the recent earnings call , the management expects inflation to remain elevated, so investors won't likely avoid increased volatility in financial markets. They also expect the higher interest rate environment to last longer than expected. So FSK plans to take advantage of this. They believe that floating-rate asset structures and investment strategies with inflation protection, such as large portfolio companies and asset-based finance investments tied to collateral pools, will continue to be attractive.

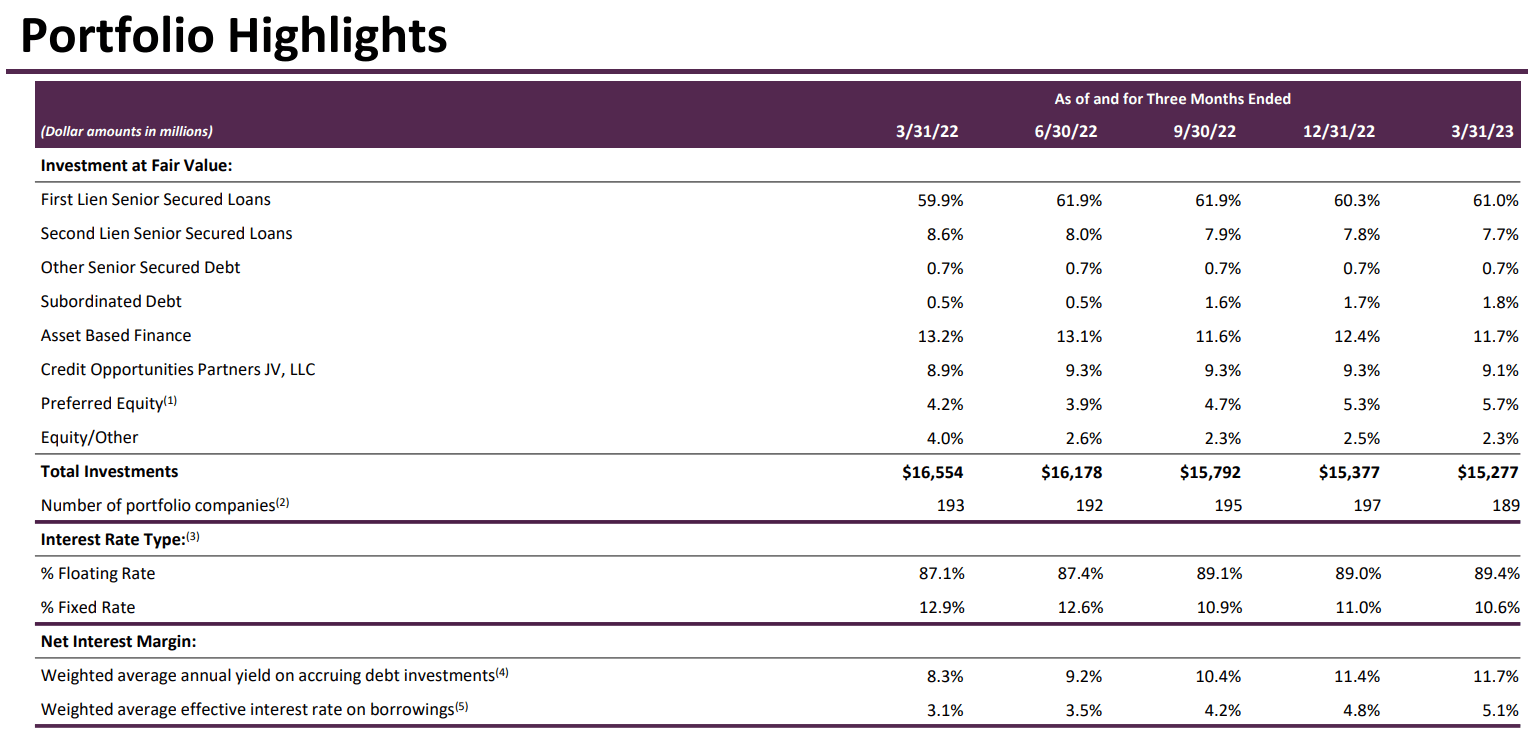

And if we look at the development of the share of loans in the structure of the company's portfolio, we will see that this is precisely what is happening - from quarter to quarter, the share of floating-rate loans is increasing:

{kind=link}

I consider the management's outlook to be quite likely and am therefore positive about such a strategic decision. Overall, FS KKR has demonstrated solid financial performance, active investment origination, and a commitment to returning value to shareholders through distributions and share repurchases.

Valuation

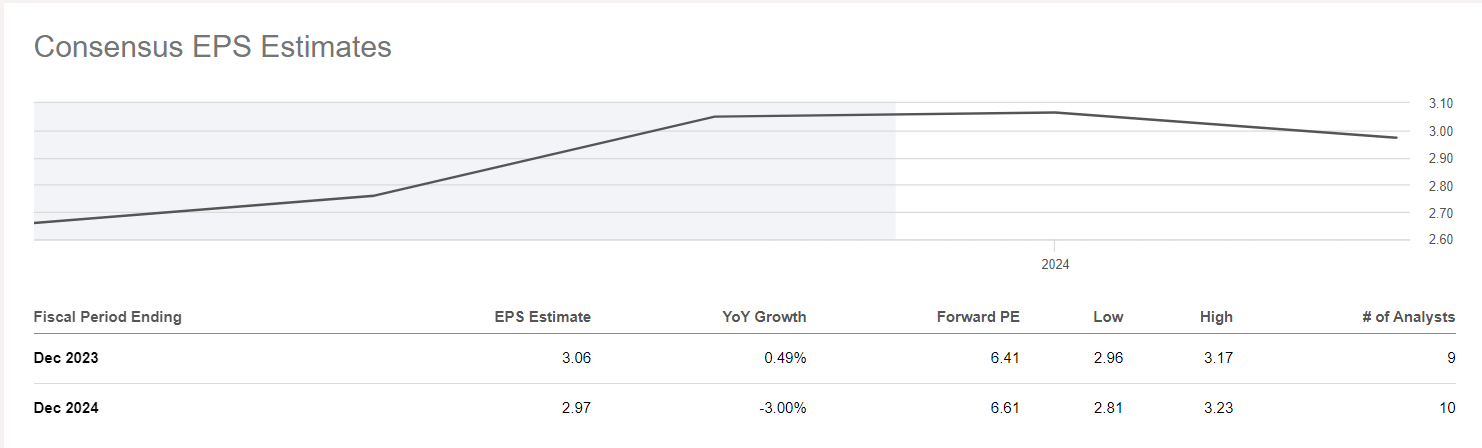

FSK is currently trading at 6.41x of forwarding P/E, which implies a multiple expansion of ~9% multiple. What does this mean? The market expects EPS to decline 3% in FY24:

{kind=link}

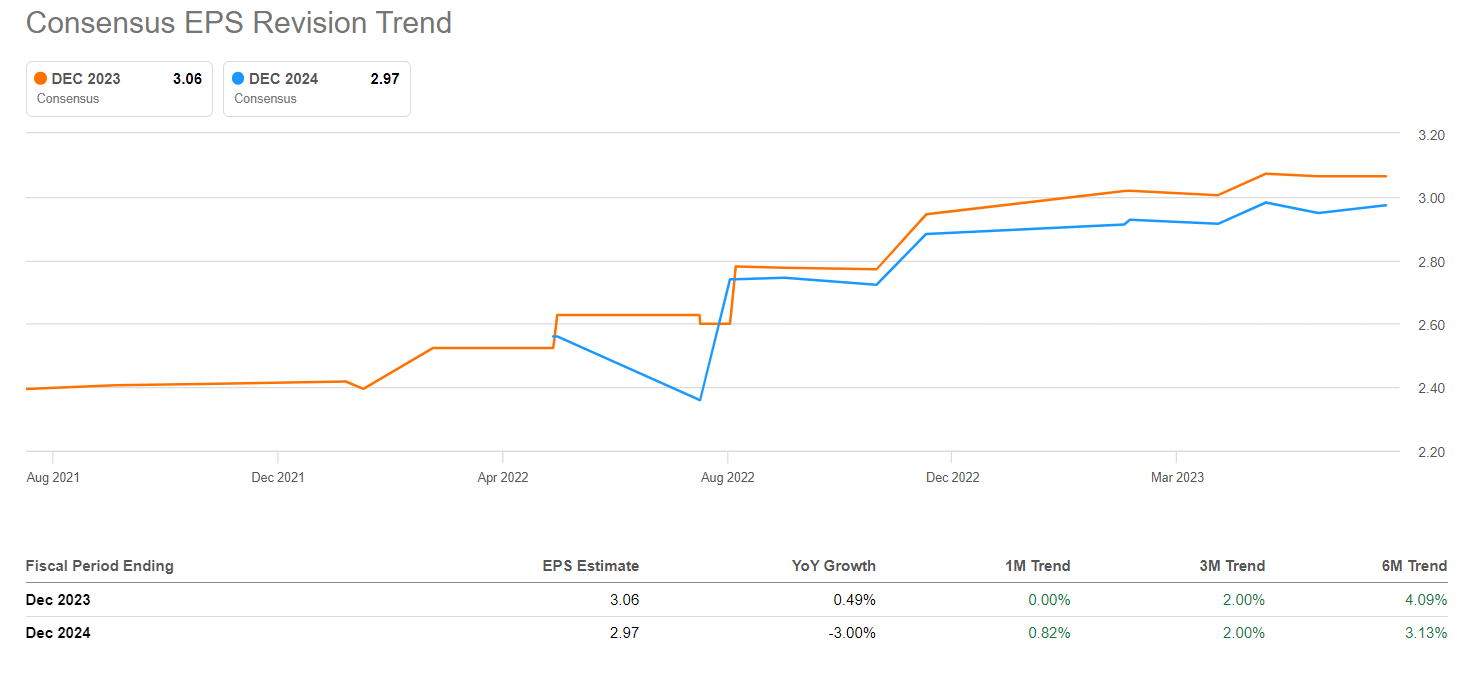

However, judging from the latest earnings revisions , we see that this forecast began to improve six months ago, giving FSC stock an "A-" grade in terms of revisions, based on Seeking Alpha's Quant system.

{kind=link}

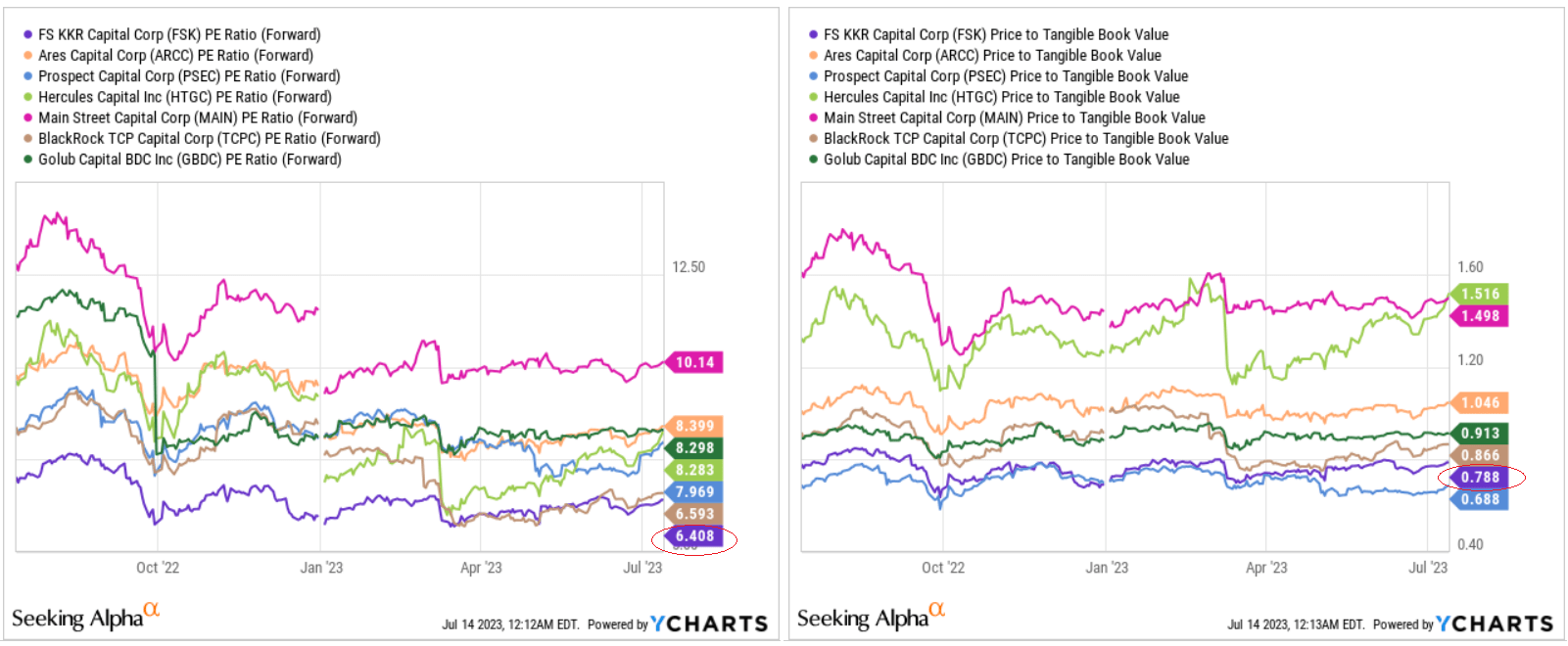

In absolute terms, FSK is the cheapest BDC stock among its peers if we look at next year's price-to-earnings ratios. FSK also looks very attractive in terms of its price-to-tangible-book:

{kind=link}

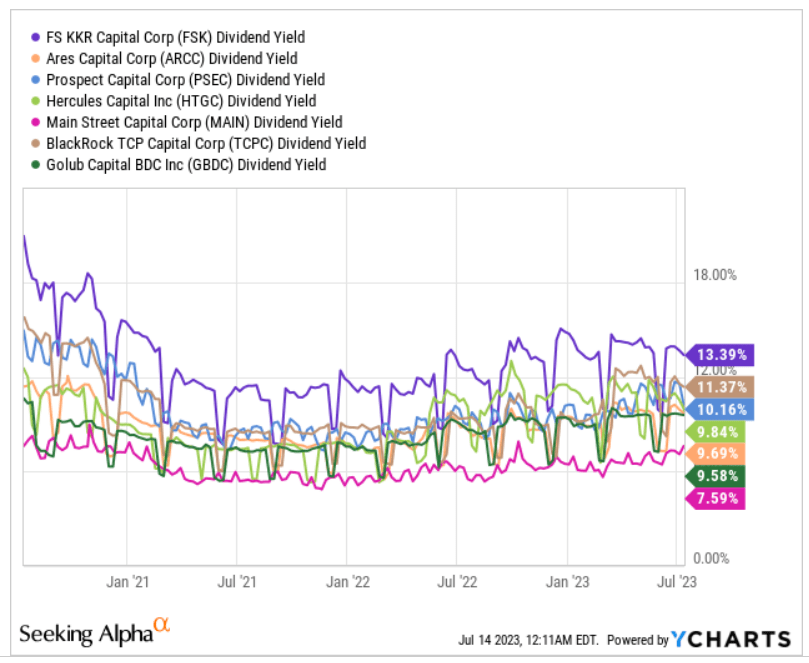

The company also has a dividend yield that is higher than other peers - in some cases, the spread reaches 3.81-5.8%, which is extremely high:

{kind=link}

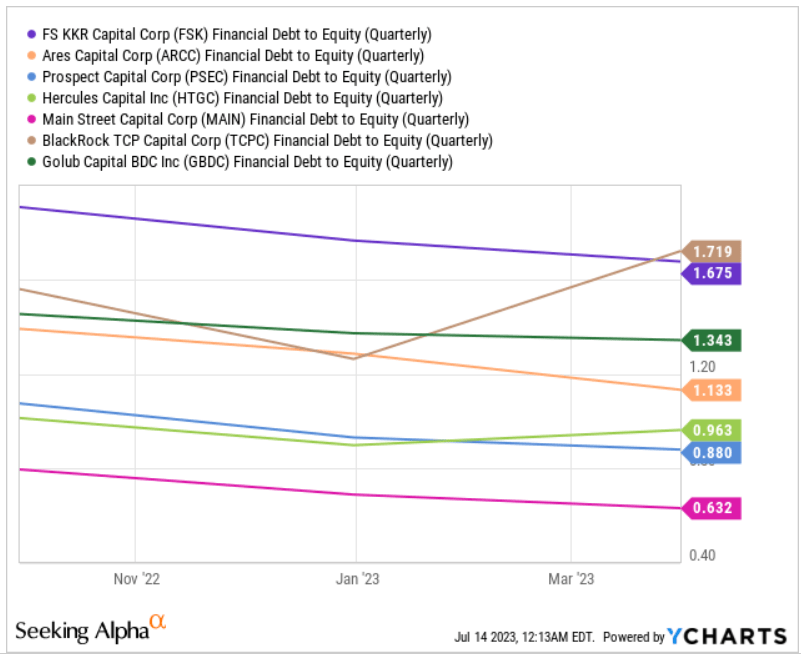

Every time such a situation occurs, one has to ask why the market allows such a picture. My opinion is that the severe comparative undervaluation of FSK is explained by the company's increased debt burden. In 1Q FY23, the firm's gross and net debt-to-equity ratios remained unchanged from the previous quarter, with unsecured debt accounting for a significant portion of the balance sheet. In absolute terms, FSK's net debt is well above the peer group average:

{kind=link}

The most important question is, how fairly the market "punishes" the FSK stock for its debt?

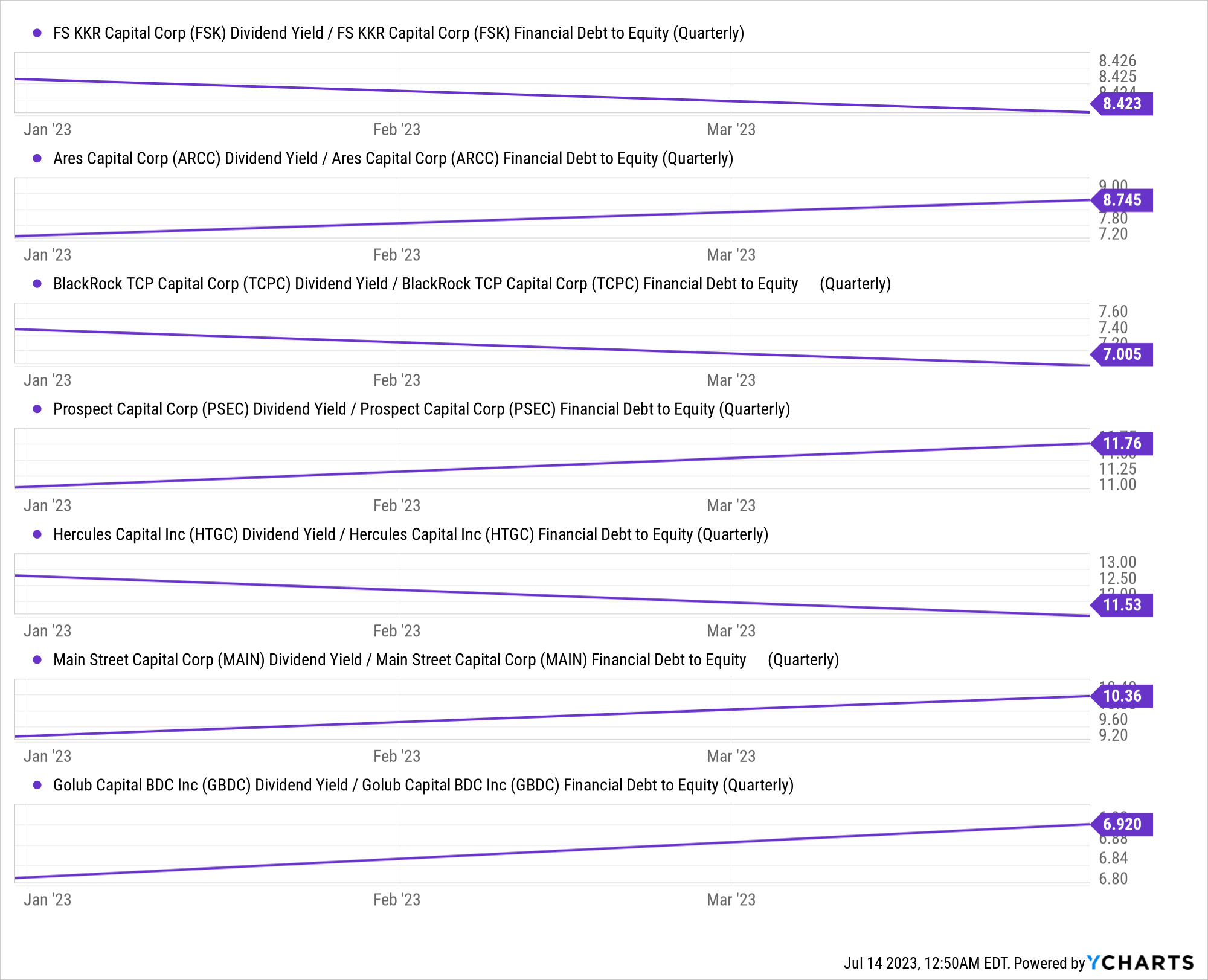

I propose to conduct a little experiment using basic algebra and a little logic. We know that dividend yield should embed risk - the higher the yield offered by the market, the riskier the investment. The debt-to-equity ratio is also a measure of risk. And BDCs should look to it all the more given the specifics of their operations. Okay, then why not use these 2 indicators simultaneously to evaluate a BDC's valuation? If we divide the dividend yield by the leverage ratio, we get a synthetic metric that may reflect the fairness of the valuation (as I understand it). The higher this ratio is, the more attractive the company is. Just that simple.

{kind=link}

The average of this group is 9.249, which is 9.8% higher than FSK's metric. Based on this analysis, it can be concluded that FSK's yield is fairly valued by the market.

Bottom Line

By most of the business metrics I looked at in my today's article, FSK KKR looks very stable. But given the nature of its portfolio and its debt, I think the recession I expect in late 2023 or early 2024 will hit the company's bottom line hard - perhaps even harder than analysts currently expect. That could eliminate special dividends, and the dividend yield calculated for today's prices will lose its practical meaning. When I weigh the dividend yields against the leverage ratios of FSK and its peers, I conclude that this BDC is currently fairly valued.

For all these reasons, I rate FSK stock as a "Hold". Over the long term, you may like the yield. But there should be even better entry points.

Thank you for reading!

For further details see:

FS KKR Capital: The 13% Dividend Is Not As Juicy As You May Think