CSWC - FS KKR Capital: The Road Ahead Looks Promising

2023-08-07 13:00:00 ET

Summary

- Although externally managed, management seems to be more aligned with shareholders with frequent special dividends when compared to their more conservative peer Ares Capital.

- FSK reported a rise in non-accruals in quarter-over-quarter, but the percentage is still below the KBW BDC average.

- The merger has resulted in NII growth and improved competitive positioning for FSK as the now second-largest BDC.

- FSK is trading at a huge discount to its NAV share price and pays a large dividend, which I think is safely covered.

- FSK has a healthy portfolio with a focus on first-lien loans, and a strong balance sheet with no debt maturities in 2023 and $3 billion in liquidity.

Introduction

Since becoming a Seeking Alpha reader a few years ago and long before I became an analyst, I would often read articles about BDCs. I quickly became a fan of these high yield investments because of the dividends they paid out to shareholders. I would often hear about FS KKR Capital Corp ( FSK ) along with other popular BDCs like Ares Capital ( ARCC ), Capital Southwest ( CSWC ), and Main Street Capital ( MAIN ), and while I am familiar with FSK, I am not as familiar with this BDC as I am with others.

I love business development companies! They are often considered risky investments, and because of my rate in the military for the last 21 years, taking risks was part of the job. To be great one has to take risks and I see investing as no different. I am a huge fan of REITs and BDCs, two sectors investors often avoid for safer investments such as big growth names like Apple ( AAPL ), Starbucks ( SBUX ), and Meta ( META ). These two sectors might not offer the same growth as those names, but they typically give investors high income, which is my primary goal. Stable and reliable dividend income for the long-term. A few of my followers asked for my analysis on FSK, so let's dive into what I think about the second largest BDC.

Who Is FSK Capital?

FSK is an externally managed business development company focused on providing customized credit solutions to private middle market U.S. companies. "They seek to invest in senior secured debt and, to the lesser extent, the subordinated debt of private middle market U.S. companies to achieve the best risk-adjusted returns for investors". The company currently has an investment grade of Baa3 (stable) from Moody's.

{kind=link}

FSK is scheduled to report earnings on Monday, August 7th after market close. Analysts expect NII (Net Investment Income) to come in at $0.76, $0.05 less, or a 6% decrease from Q1, but a $0.04 increase year-over-year.

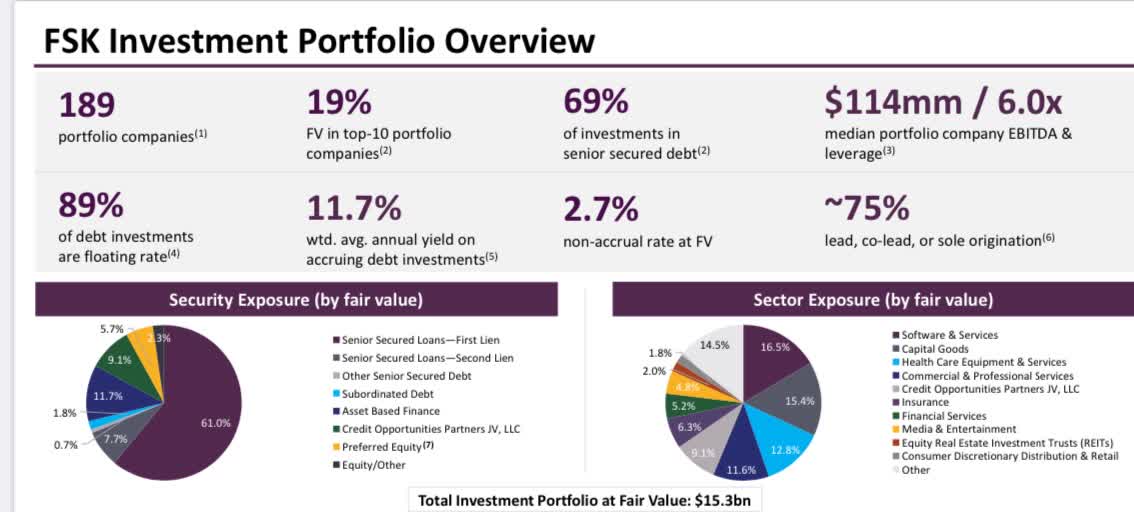

Portfolio Highlights

The BDC had 189 portfolio companies at the end of March 2023 compared to 197 in Q4 , with Software & Services being their biggest sector exposure at more than 16%. This is similar to ARCC's with the exception of Capital Goods. FSK more than quadruples its exposure to this sector with 15.4% to its peer ARCC at 3%. Capital goods are similar to consumer goods, except that these are man-made products by a business to produce consumer or other capital goods. These include buildings, machinery, tools, etc. Consumer goods are things like food, appliances, automobiles, etc. In short, consumer goods satisfies customers needs while capital goods are used to produce other products. Consumer goods are personal and final, while capital goods are typically not.

{kind=link}

First Lien Focused

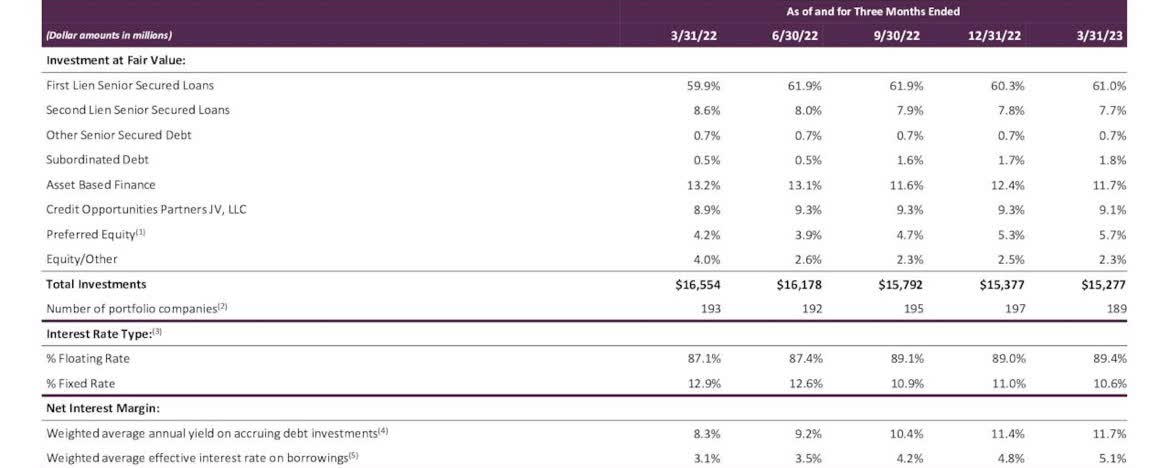

One thing I like about FSK is their focus on first-lien loans. First lien loans are 67% of the portfolio with second lien loans at 8.8% and 90% of their debt investments are floating rate. This is in comparison to ARCC whose first and second lien loans currently sit at 42% and 18% respectively. During Q1 earnings the BDC delivered strong operating results, generating NII of $0.81 and adjusted NII of $0.78. I also like that the company was able to grow its NAV quarter-over-quarter from $24.89 to $24.93, but this declined from $27.33 a year ago. Although I like to see continued NAV growth, management did state that their new originations consisted of approximately 82% in first lien loans, 11% in asset-based finance investments, 3% in subordinated debt, and 4% in equity and other investments. Going forward in 2023 I think FSK will continue on its path to NII and NAV growth.

The Merge Impact On NII Growth

In June 2021 FSK merged, creating the second largest BDC behind ARCC. This greatly increased scale and liquidity, allowing the BDC to participate in more upper middle-market private debt deals. This merger was expected to create long-term NII accretion for shareholders and improved competitive positioning. Seems like the merger has indeed paid off for shareholders. NII grew more than 10% from 2021 to 2022 from $2.76 to $3.05

{kind=link}

Expected Revenue And Net Income Forecast

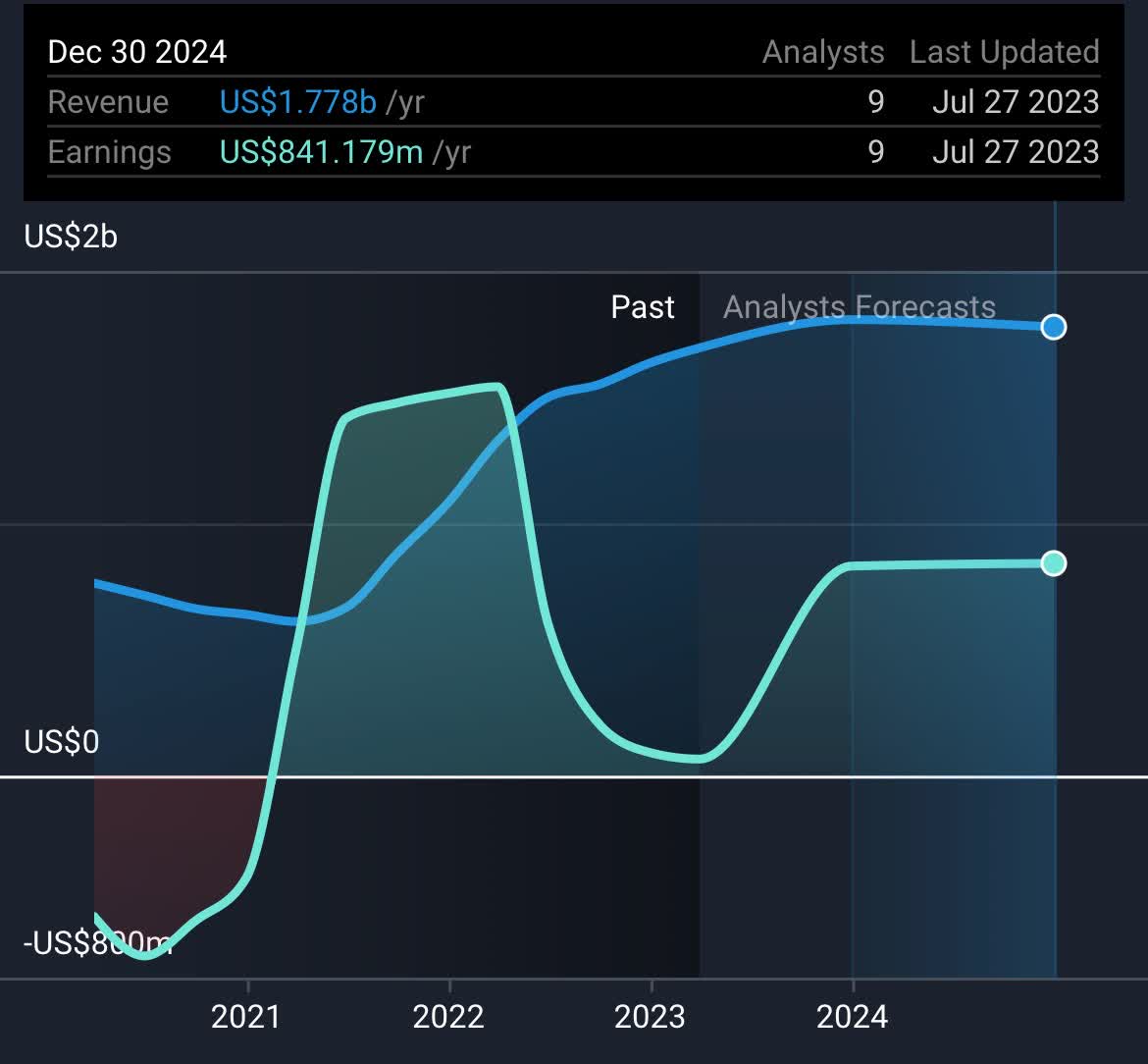

FSK's end-of-year net income for next year is expected to come in at $841.179 million and revenue at $1.778 billion, up from $92 million and $1.64 billion the year prior. Revenue is expected to continue growing, while earnings are expected to level out in 2024. Furthermore, since 2019, net income has grew more than 250% from $246 million to $865 million for FY 2022.

{kind=link}

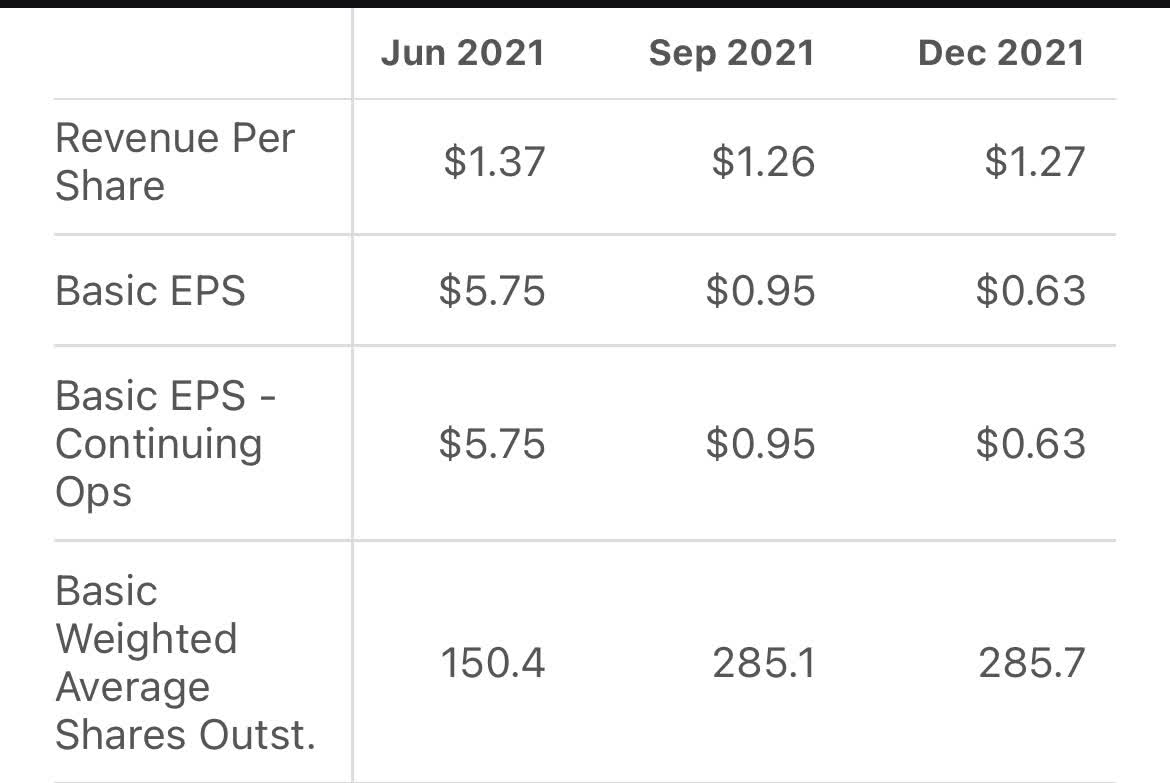

Buyback Program

As noted in the chart above, FSK did experience a massive drop in earnings from March 2022 to March 2023, but this was due to the $100 million share repurchase program announced in Q3 2021. As seen below, the share count almost doubled from 150 to 285 after the merger. I think this speaks volumes of their management team, as BDCs typically issue shares to raise capital and fund growth. This typically doesn't sit well with investors, as this dilutes shareholders.

{kind=link}

FSK finished their repurchase program in Q1 2023 all while the stock was trading at a significant discount to its NAV. Additionally, the chart below shows that the BDC continued to out-earn its dividend in NII and adjusted NII in each quarter. This does not include special and supplemental dividends paid during these periods.

| FS KKR |

| Q1 2022 |

| Q2 2022 |

| Q3 2022 |

| Q4 2022 |

| Q1 2023 |

| PORTFOLIO COMPANIES |

| 193 |

| 195 |

| 195 |

| 197 |

| 189 |

| DIVIDEND |

| $0.60 |

| $0.61 |

| $0.61 |

| $0.64 |

| $0.64 |

| NII |

| $0.77 |

| $0.76 |

| $0.76 |

| $0.80 |

| $0.81 |

| ADJUSTED NII |

| $0.72 |

| $0.73 |

| $0.73 |

| $0.81 |

| $0.78 |

Valuation & Dividend Coverage

Currently, FSK is trading at a huge discount to its current NAV. Investors looking to start a position can get this BDC at an almost 20% discount. Their Price to Book Value is also below the sector median of 1.11 at 0.81. FSK's current dividend yield is over 12% which can seem like a yield trap, but I believe the current dividend of $0.70 is safe. Even with the special dividend of $0.05 expected at the end of this month, FSK is safely covering the dividend with the Q1 NII of $0.81 and its adjusted net investment income of $0.78 per share. For being an externally managed BDC, FSK seems to be more aligned with shareholders. The company has been very generous with its special dividends, declaring three installments this year. Even if NII becomes tight over the next couple of quarters, management could just drop the special dividend while income continues to stabilize.

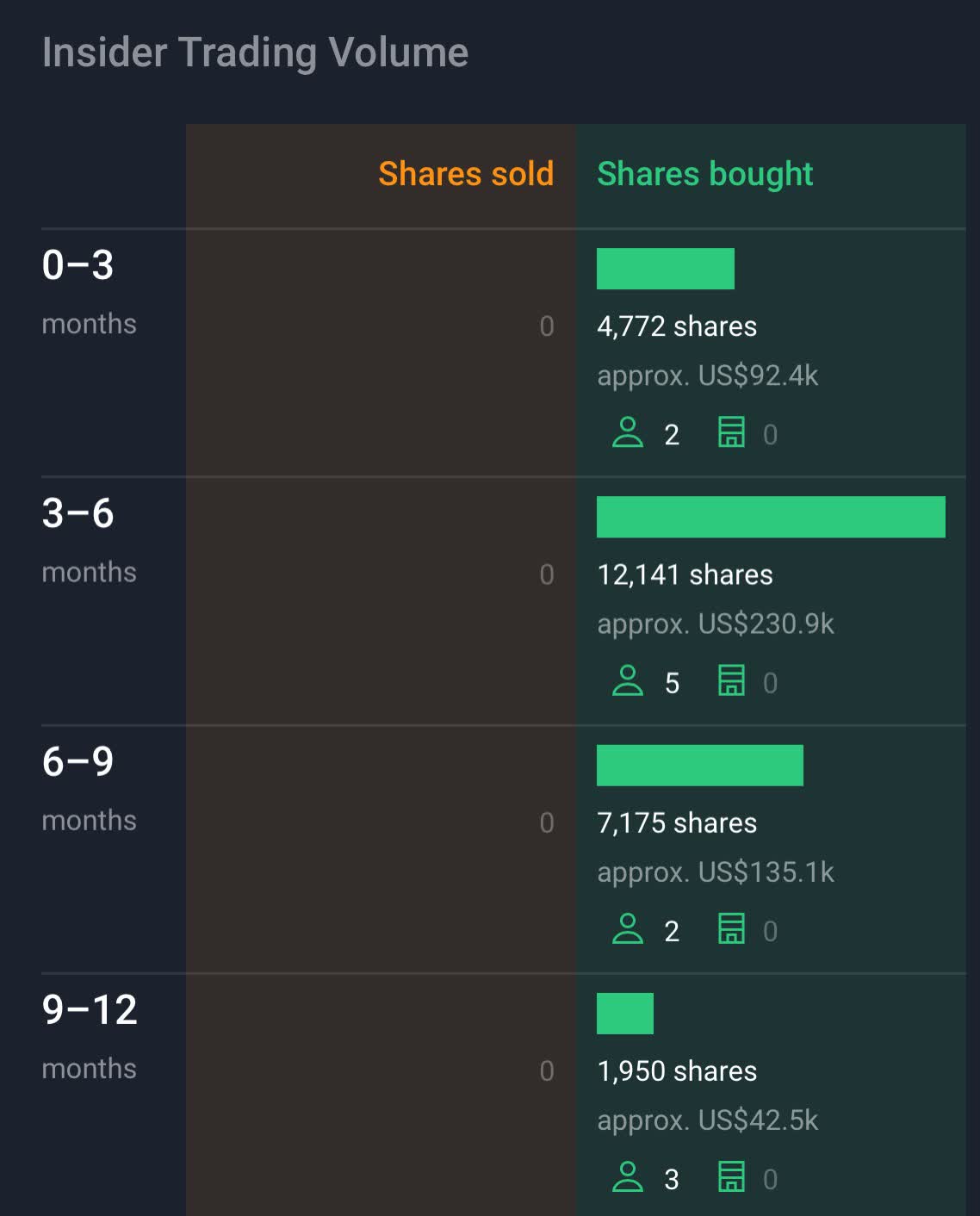

Insider Buying

Below is the trading volume over the last 12 months. As you can see, no shares have been sold and the highest amount of shares have been bought over the last 3–6 months. This is an important metric to look at, as insider buying may be a sign of confidence in the company's growth. The great Peter Lynch once said: Insiders sell shares for a number of reasons, but they only buy for one; the price will rise.

{kind=link}

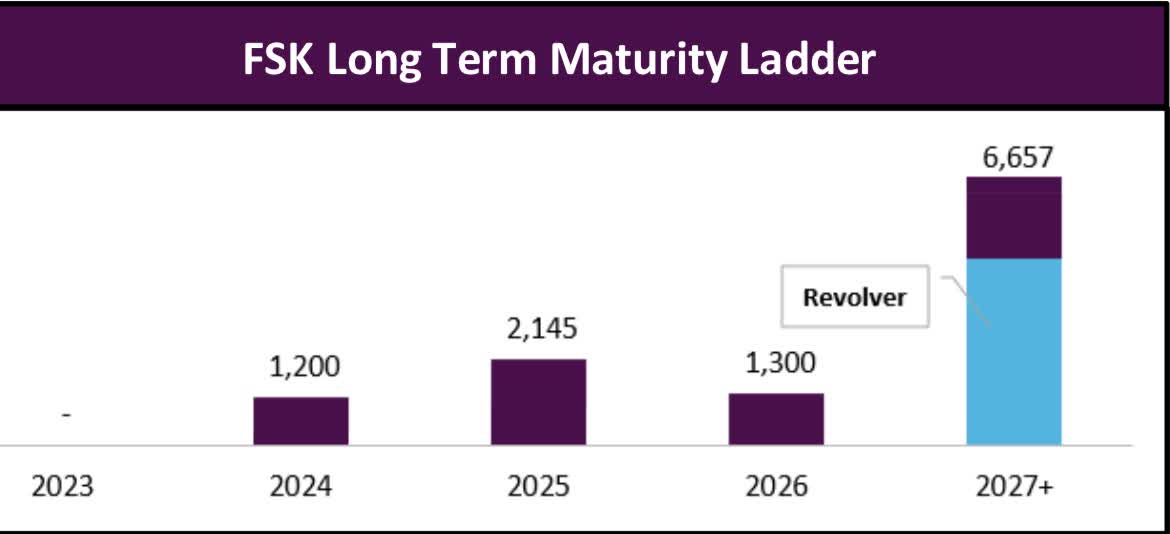

Strong Balance Sheet

FSK has an IG rating from Moody's and ended the quarter with $3 billion in liquidity. Another great thing about this BDC is their well-laddered debt maturities. The company has no debt maturities in 2023 making them prepared to navigate the promised higher for longer environment. The FED has three more meetings this year, and although they left the door open for further potential rate hikes, I don't see this being a problem for the BDC in the near future. Many are suspecting the rate cuts by the end of this year.

{kind=link}

Inflation Risks

While BDCs typically benefit from inflation with higher interest rates, one thing investors need to be aware of is the rise in non-accruals. FSK saw an uptick in Q1 to 2.7% from 2.4% in the prior quarter. This is below the KBW BDC average of 3.8%, but this could potentially become a problem in the near future with the higher for longer environment. The FED recently raised rates another .25 bps, so investors should keep an eye out for further potential raises in non-accruals during these next few quarters. And even with inflation seeming to cool, that doesn't mean the FED will automatically begin to cut rates because of this. This persistent inflation led FSK to place two companies, Reliant Rehab and Miami Beach Medical Group, on non-accrual during the quarter. Their Co-President stated that this was due to the several macroeconomic factors across the healthcare services industry, including a decline in contract labor, and increase in contract labor given a tight labor market in the U.S.

Investor Takeaway

Although FSK has had problems in the past, specifically during COVID, the BDC seems to have put their prior problems behind them with the merger. Even though they are externally managed, management seems to be aligned with shareholders paying out special dividends frequently, while peer ARCC prefers to be more conservative during the current macro environment. Additionally, they have no debt maturities in 2023 which is essential during the current high-interest environment and sport a stable IG rating from Moody's. As the now second largest BDC, I expect FSK to continue on its path to growth and could potentially become a long-term hold for investors seeking income. Even though there are better BDCs out there, in my opinion, I currently rate them a speculative buy as the road ahead looks promising.

For further details see:

FS KKR Capital: The Road Ahead Looks Promising