BXSL - FS KKR: Investment Grade Yet Fat 13% Dividend Yield NAV Keeps Me Worried

2023-12-13 09:59:34 ET

Summary

- FS KKR Capital Corp offers an investment grade backed 13% base dividend yield set to be boosted by supplementals next year.

- The BDC currently covers its base dividend distribution by 125% and has 2.5 quarters of spillover income as of the end of its fiscal 2023 third quarter.

- A discount to net asset value per share currently running at around 20% presents an opportunity for investors.

An investment grade rating is a stamp of safety, stability, and top-tier creditworthiness and typically means lower yields when compared to non-investment junk-rated securities. FS KKR Capital Corp ( FSK ) is rated Baa3 by Moody's and BBB- by Fitch and is the second largest publicly traded business development company ("BDC") as per total assets. It last declared a base dividend distribution of $0.64 per share for a 13% annualized forward dividend yield. There will also be a $0.06 per share supplemental and another $0.05 per share special distribution for an incremental dividend yield of around 0.56%. A double-digit dividend yield from a ticker-rated investment grade going into 2024 could form a driver for strong total returns in a year set to see headwinds for private credit get compounded.

{kind=link}

FSK also held 2.5 quarters worth of spillover income, around $1.60 per share at the end of its fiscal 2023 third quarter. Management was asked about their outlook of the supplemental for 2024 during the third quarter earnings call, and outright stated that they intend to continue paying the $0.06 per share supplemental for the foreseeable future.

I think by definition, that means we feel confident about the supplemental as well kind of in the near term. And I think you should expect the basin supplemental to remain in the coming quarters.

Dan Pietrzak

Net Asset Value, Underwriting Quality, And Repayments

Total returns could notch 14.2% next year assuming flat NAV growth for 2024. However, FSK is currently swapping hands for a roughly 21% discount to NAV. This discount has proved incredibly rigid at stands at odds with peer BDCs like Ares Capital ( ARCC ) and Blackstone Secured Lending ( BXSL ), which are both trading at single-digit premiums.

Critically, whilst FSK's NAV per share at the end of the third quarter was up 20 cents sequentially, the market continues to extrapolate the downtrend in performance in place since the summer of 2021. FSK's NAV per share is down 7.3% over this period, around $1.95 per share. This came in a period often described as the Goldilocks era for private credit, with a strong U.S. economy and sustained hikes to interest rates driving record investment income.

{kind=link}

FSK recorded a total investment income of $465 million during the third quarter, up 13.14% over its year-ago period even with its investment portfolio at fair value of $14.7 billion falling from $15.8 billion. This was as its weighted average annual yield on accruing debt investments expanded 180 basis points year-over-year to 12.2% at the end of the third quarter. FSK is well diversified with its investments spread across 200 companies. The portfolio realized a 2.4% non-accrual rate at fair value at the end of the third quarter, a 10 basis points sequential improvement. This non-accrual rate was 4.8% at cost, unchanged from the second quarter.

{kind=link}

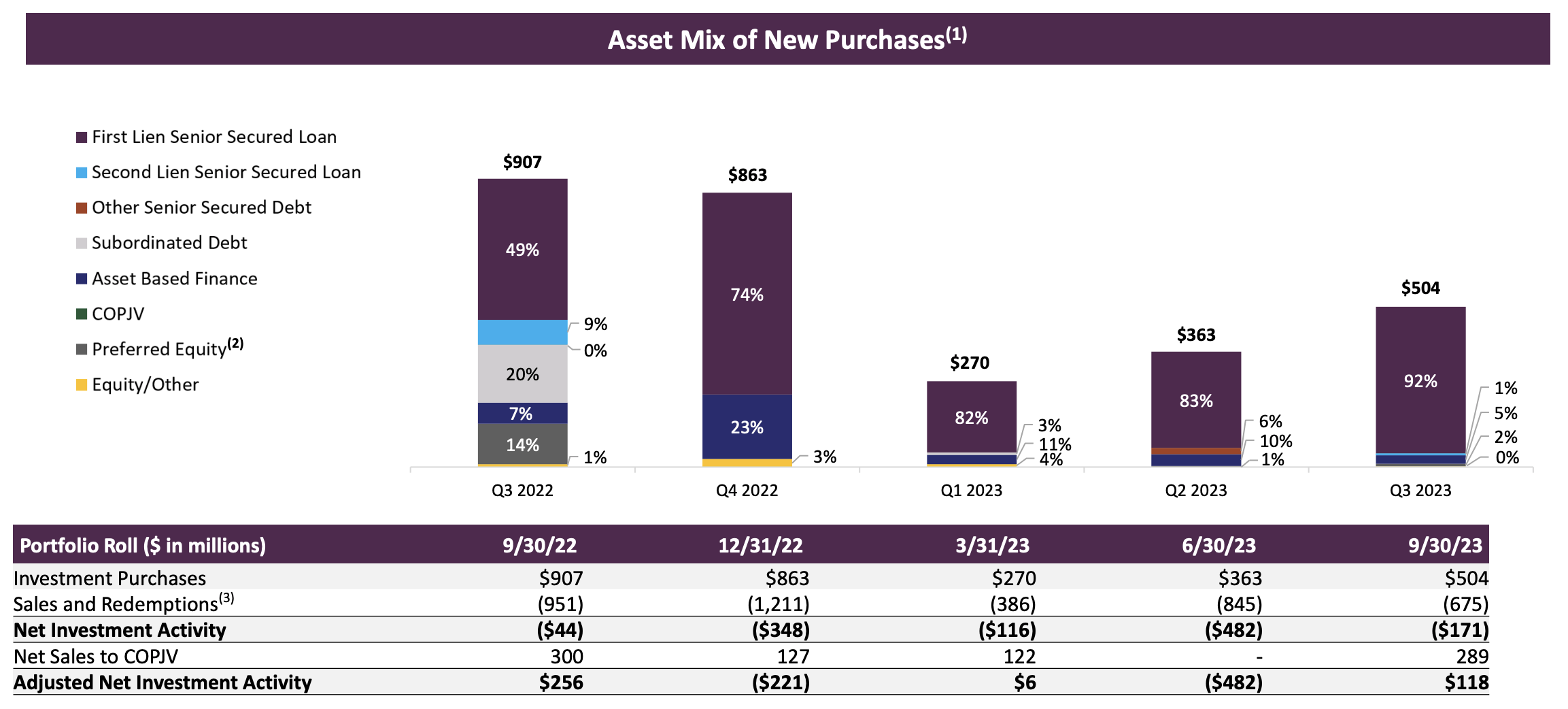

Investments rated 3 and 4, the lowest tiers of FSK's rating scale, saw an improvement to 4% in the third quarter from 6% at the end of the prior fiscal year. This describes investments where there is some loss of interest or dividend possible and there are concerns about the recoverability of principal or interest. The improvement has come on the back of a general reduction in the size of the portfolio, with FSK realizing repayments that were in excess of purchases by $171 million during the third quarter and around $770 million year-to-date . Further, these new investments have also tilted heavily towards higher security first-lien senior secured loans. These constituted 92% of third-quarter purchases, versus a 59.8% first lien exposure of the wider portfolio.

{kind=link}

Fed Rate Cuts, Dividend Outlook, And Closing The Discount

FSK's adjusted net investment income came in at $0.80 per share at the end of the third quarter, up 2 cents sequentially and by 7 cents versus its year-ago period. This means the BDC covers its base dividend yield by 125%, hence, with at least $1.60 per share of spillover at the end of the third quarter FSK holds an immense amount of flexibility for the direction of its aggregate dividend distributions next year. The BDC covered the base and supplemental by 114%.

{kind=link}

There could also be more stock buybacks in 202 with an initial $100 million share repurchase program at the closing of the merger of FS KKR Capital Corp. and FS KKR Capital Corp. II back in 2021 due for a follow-up program. A potential total return scenario for shareholders next year would be the base dividend kept at its current level but buffeted by supplementals and with an up to 100% reduction of the current discount to NAV. The best-case scenario would see a 20% uplift in the stock price for existing shareholders in addition to the double-digit dividend yield. This will depend on FSK being able to at minimum not realize a decline in its NAV per share.

{kind=link}

It also comes with broad market expectations that the Fed will start to peel back interest rates as early as May next year, as headline CPI continues to fall. The CME FedWatch Tool , which visualizes 30-Day Fed Funds futures pricing data, has placed the probability of zero rate cuts by the end of astronomical summer next year at a low 0.55%. The current base case is for interest rates to sit at 4.50% to 4.75%, a reduction of 75 basis points. This will form a headwind for most BDCs if paired with a recession, as non-accruals will likely see upward pressure. FSK's strong double-digit dividend yield and a substantial discount to par mean it remains a buy, unchanged from my last coverage .

For further details see:

FS KKR: Investment Grade Yet Fat 13% Dividend Yield, NAV Keeps Me Worried