FSK - FS KKR's Distribution Has Crossed 13% And I Am Buying More

2023-10-11 09:00:00 ET

Summary

- Shares of FSK have declined by -4.53% since the last article, pushing its yield to 13.07%.

- FSK trades at a significant discount to its net asset value and has been selling off despite a higher for longer rate environment.

- The rising rate environment is beneficial for FSK as it provides a compelling reason for income investors to venture outside of risk-free assets.

Since my last article ( can be read here ) on FS KKR Capital Corp (FSK) was written on 9/7/23, shares have declined by -4.53%, pushing its yield to 13.07%. Over the past month, shares of FSK have declined by -6.15% as they fell below $19 at the beginning of October and then slightly rebounded. I am surprised that shares of FSK have been selling off into the higher for longer environment rather than appreciating. FSK is the 2nd largest Business Development Corporation [BDC] by both net assets and market capitalization, and yet it trades at a significant discount to its net asset value [NAV]. The recent decline has pushed FSK's base yield past 13%, and shareholders have been receiving special distributions due to the strong net interest income being generated. The macro-environment has changed since my last article, and unless the recent events overseas cause oil prices to surge, we are likely to see a higher for longer rate environment, which should be bullish for FSK. I am planning on adding shares of FSK and locking in a yield that exceeds 13% on fresh capital.

{kind=link}

Looking back on my previous article

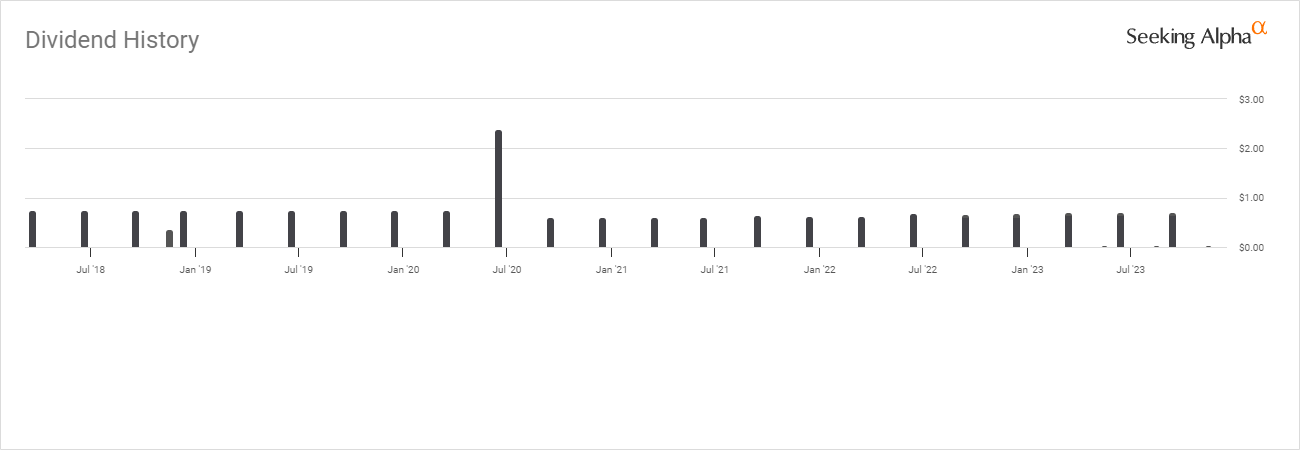

In my previous article on FSK, I discussed their Q2 earnings, the additional distribution being paid, and how FSK was valued compared to a large peer group of BDCs. FSK had generated $0.78 of net investment income [NII] per share in their 2023 Q2 , which was a $0.02 beat from the consensus estimates while producing $462 million in total investment income. This worked out to be $0.82 per share of NII, allowing FSK to pay $0.75 in distributions through its normal $0.64 distribution and a special and supplemental distribution amounting to $0.11. FSK's board has declared a quarterly distribution of $0.70 consisting of the $0.64 base distribution and a supplemental distribution of $0.06 per share in addition to paying the remaining $0.05 installment from their previously declared $0.15 in special distributions. At the time, FSK was trading at a -17.74% discount to its NAV while generating a 12.51% distribution yield. I was bullish in my last article on FSK as their NII was growing, and I felt I was getting a good value on my invested capital by buying FSK's net assets at a discount.

{kind=link}

The macroeconomic environment has changed since my last article, and I feel it's bullish for FSK

For months, there have been discussions and debates as to when the Fed would cut rates. I listened to many different opinions and felt that the narrative that was getting the most traction throughout the spring and summer was that the Fed would cut rates at the September or November meeting. In June, inflation fell to 3%, and despite commentary indicating that this was a backward-looking indicator and the Fed had done too much, the Fed raised rates by 25 bps on 7/26, then paused at the September meeting. At the last meeting, the Fed left nothing open for inspiration as Jerome Powell delivered a hawkish speech, indicating that no rate cuts were coming in 2023, the rate environment would be higher for longer, and the door was open for another hike if the data called for it.

This Thursday, 10/12, we're getting a critical CPI and Core CPI report at 8:30 am. as the CME Group Fed Watch Tool is showing an 11.2% chance of a .25 bps increase for November and a 39.5% chance we see a .25 bps increase in December. Core CPI has steadily declined as CPI has increased for the past two months. If the September numbers come in hot for both Core CPI and CPI, it could set the stage for the Fed to raise rates again before the year ends. The other key aspect is oil, as the conflict emerging in Israel has made the price per barrel for Brent jump from $83.93 on 10/5 to around $88. The Fed has been walking a tightrope, and while they have come close to breaking things during the tightening cycle, they haven't actually broken anything yet. If oil skyrockets until the next FOMC meeting, it could play a role in the Fed's decision because oil over $90 could pressure the Fed to leave rates where they are or pivot sooner than expected.

{kind=link}

Unlike many traditional equities paying a 2-4% dividend, I think the rising rate environment is good for FSK. Right now, the risk-free rate of return on the 12-month treasury is 5.45%, so many income investors are less inclined to take on equity risk at a lower yield when the risk-free rate of return is 5.45%. The rising rate environment has made lower-yielding equities less attractive to income investors because we are no longer living in a yield-starved environment, and they aren't being paid enough to make the risk make sense.

{kind=link}

I feel that a higher for longer rate environment benefits FSK in 2 ways. First, FSK's distribution yield in the low double-digits provides a compelling reason to venture outside of risk-free assets. There is enough delta between the risk-free rate of return and the 13.22% yield that FSK provides from the base distribution to consider taking on equity risk. This distribution can also be automatically reinvested to lower the initial cost basis and generate a larger forward distribution. The rising rate environment has made traditional low-yielding equities less attractive for income investors, which is a positive for FSK. I believe strong high high-yielding assets such as MLPs and BDCs are being looked favorably upon as income investors are looking to lock in higher rates on their invested capital.

The second reason why a rising rate environment is positive for FSK is because banks are in a restrictive environment and are less inclined to lend to private middle-market companies. This puts BDCs in a prime lending position and allows them to benefit from high rates when negotiating terms. FSK has 68% of its investments in senior secured debt, and 89% of its debt investments are floating rate. This has allowed FSK to increase its weighted annual yield on accruing debt investments to 12.1% while the weighted average effective interest rate on FSK's borrowings is 5.2%, creating a net interest margin of 6.9%. By investing in new debt obligations as rates increased, FSK has been able to drive more investment income from its investments, which has correlated to a growing NII per share QoQ over the past year. These new investments could also become more valuable next year if the Fed pivots because they should theoretically have larger yields than debt being issued when rates are lower.

{kind=link}

FSK is still very attractive compared to its peer group

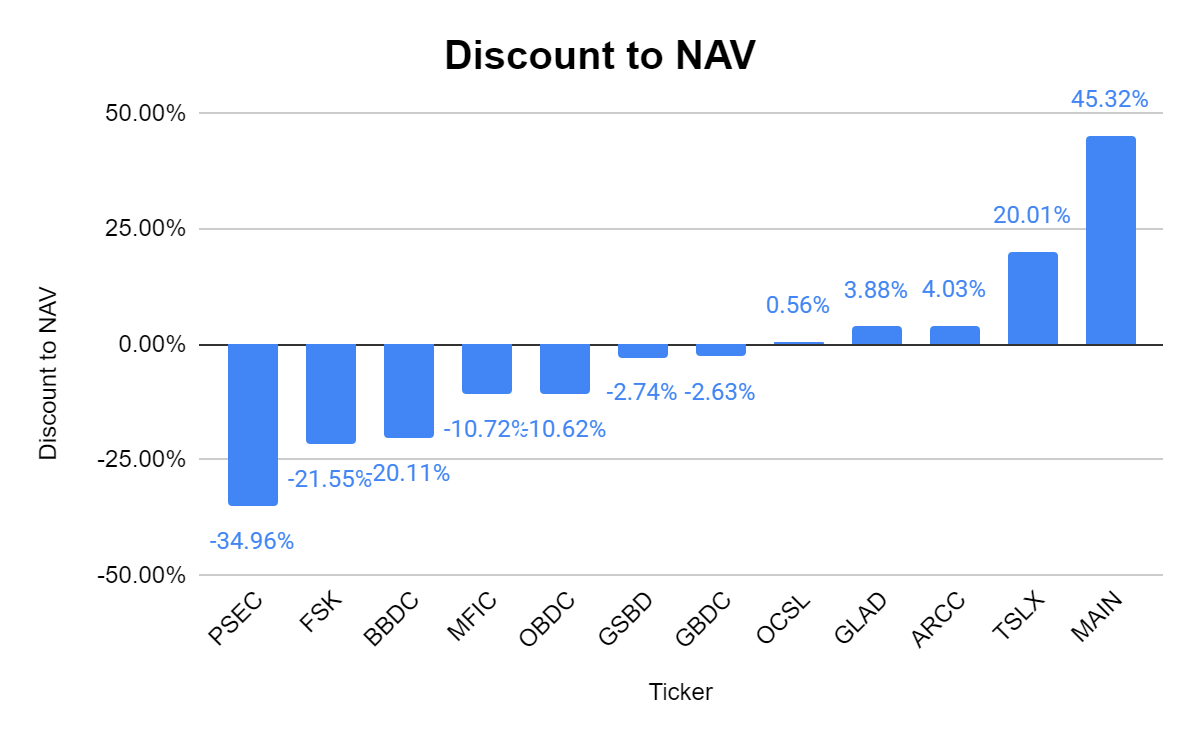

I compared FSK to the following BDCs and the valuation still looks very compelling:

- Prospect Capital Corporation ( PSEC ).

- Barings BDC ( BBDC ).

- Main Street Capital ( MAIN ).

- Blue Owl Capital Corporation ( OBDC ).

- MidCap Financial Investment Corporation ( MFIC ).

- Goldman Sachs BDC ( GSBD ).

- Oaktree Specialty Lending Corporation ( OCSL ).

- Golub Capital BDC ( GBDC ).

- Ares Capital ( ARCC ).

- Gladstone Investment (GAIN).

- Sixth Street Specialty Lending ( TSLX ).

{kind=link}

FSK trades at the 2nd lowest market cap to NII multiple of 6.24x while the peer group average is 8.35x. Today, I am able to add shares of FSK at a lower multiple on NII than most of its peers, and FSK is the 2nd largest BDC and produces the 2nd largest amount of NII.

{kind=link}

FSK still trades at the 2nd most discounted BDC compared to its NAV at -21.55%. This is another reason why I feel shares are still very attractive, as investors are still getting a steep discount compared to its assets on the books. I feel this should change into a Fed pivot.

{kind=link}

I invest in BDCs for income, and FSK now has the largest yield of its extended peer group. Today I can pick up shares of FSK at the 2nd lowest multiple on its NII, at a -21.55% discount to NAV, and at a yield that exceeds 13%.

{kind=link}

Conclusion

FSK is one of my favorite BDCs, and I feel that Mr. Market is overlooking the underlying strength of its assets. FSK has produced $877 million in NII over the TTM and continues to drive its NII per share higher. FSK continues to reward investors through special distributions that I didn't take into consideration when discussing the base yield of 13.22%. I think FSK should trade closer to where ARCC trades in relation to the premium to NAV, and when the Fed pivots, FSK's assets will become much more valuable. This should create appreciation in shares as the gap closes between its market cap and NAV. I think now is a good time to add to FSK and collect the large distributions while waiting for shares to rise in value.

For further details see:

FS KKR's Distribution Has Crossed 13% And I Am Buying More