FSK - FS KKR: The Best 15% Yield I've Seen So Far

2023-05-18 12:49:04 ET

Summary

- FS KKR Capital Corp. offers a compelling 15% yield and a focus on high-quality senior secured debt in defensive industries.

- The company has undergone significant changes since 2018, merging with other BDCs and gaining strong backing from experienced asset managers.

- FSK is trading at a significant discount to its book value, presenting an opportunity for investors and the potential to outperform its peers over the long term.

Introduction

Initially, I wasn't planning on covering FS KKR Capital Corp. (FSK) . However, after discussing its larger peer, Ares Capital (ARCC), I got many requests to dive into this stock, which is what I did.

While I was initially put off by the stock's poor long-term performance, I have to say that the company behind the FSK ticker is a fantastic income play. Not only does this stock come with a juicy 15% yield, but it also comes with a healthy portfolio and competent management. Furthermore, after a few major business changes since 2018, the current FSK company is not what investors were dealing with more than five years ago.

On top of that, FSK trades at a significant discount versus its book value, which sweetens the deal in light of ongoing credit risks.

So, while I wouldn't suggest investors pile into high-yielding credit plays in light of mounting financial instability, I believe that FSK is one of the best business development companies on the market.

If I were in the market for a 15% yield, I would be a buyer, as I believe that FSK is one of the best ways to buy a very high yield with a good risk/reward.

Now, let's dive into the details!

Buying High-Quality High-Yield

I usually invest most of my money in dividend growth companies. In my world, a stock with a 3.5% yield is a high-yield stock.

That said, over the past few months, I've increasingly focused on higher-income plays, as some of my clients are retired investors and because the demand for higher-yielding investments is rapidly rising due to the ongoing retirement wave.

Since the Great Financial Crisis, the number of people seeking a higher income has exploded.

{kind=link}

When adding elevated inflation, we get a scenario where it only makes sense to present some (very) high-yielding investments.

Buying a high-yield investment isn't hard. Everyone with some cash, access to the internet, and time to do a quick Google search can do it.

The problem is buying high-quality high-yield investments, which is hard.

When dealing with yields above 10%, investors are almost always dealing with investments that do not grow. In a lot of cases, investors buy assets that consistently lose value.

For example, 11%-yielding mortgage Real Estate Investment Trusts have lost 65% of their value over the past ten years. Even when compounding dividends, investors have lost 5%. This excludes inflation.

I'm obviously cherry-picking here, but from my experience, it is shocking how many investors buy high-risk trash (I'm sorry, but in some cases, it's true) and end up losing a big part of their savings.

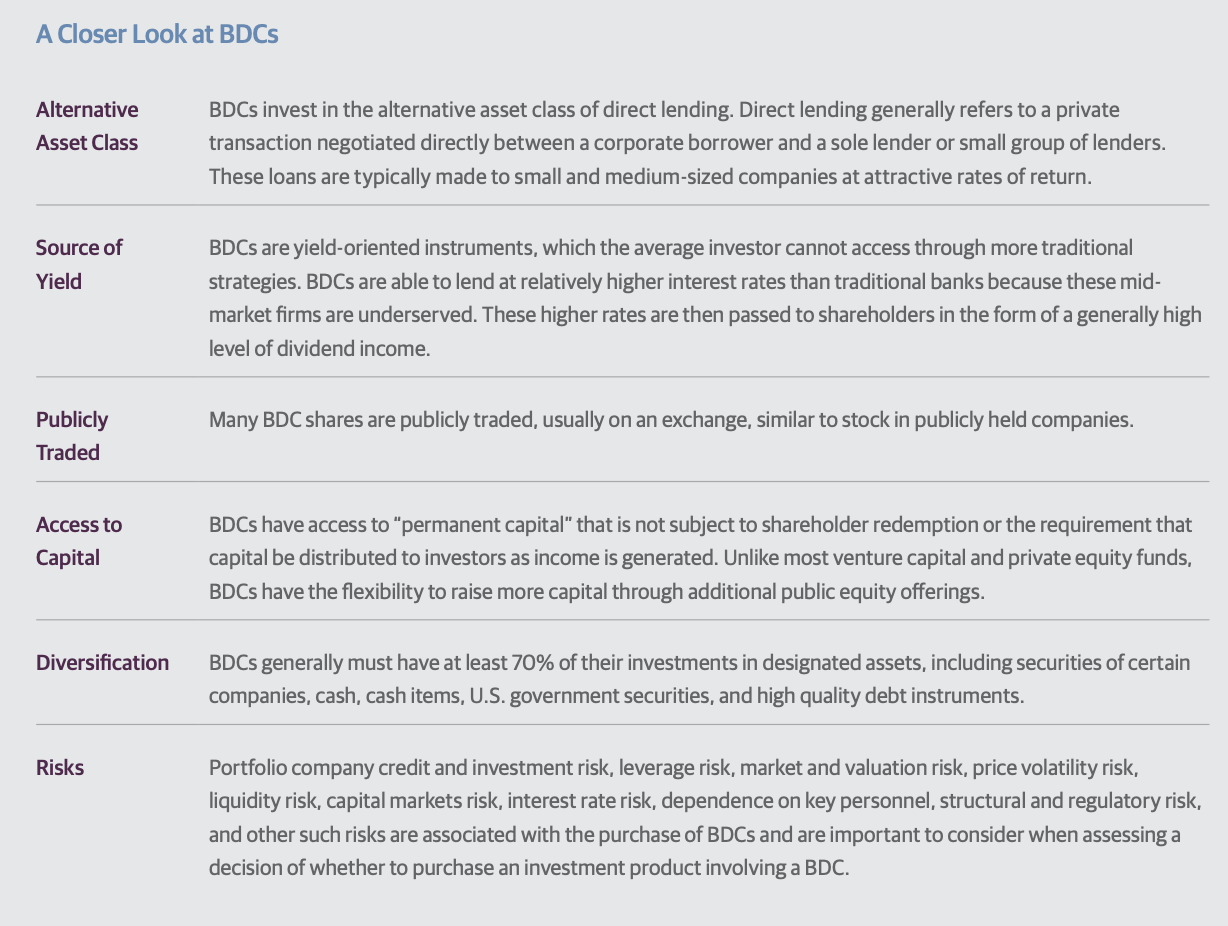

FS KKR is a so-called business development company. As I wrote in my ARCC article (emphasis added):

Business development companies are closed-end investment companies that serve the purpose of investing in small and emerging businesses , as well as financially distressed enterprises .

By investing in BDCs, individuals gain exposure to a diverse range of assets within private companies' capital structure, including senior secured and subordinated debt and preferred and common equity.

BDCs face certain investment restrictions and primarily allocate their funds to eligible portfolio companies. Typically, these companies include small businesses in the early stages of development or financially troubled enterprises lacking access to conventional financing options. With traditional lenders, such as banks, burdened by increased regulatory requirements, they struggle to provide loans to small and mid-sized businesses.

Here's an overview of some of the basic things that apply to BDC investing.

{kind=link}

In other words, investors invest in companies that lend to firms that wouldn't fare so well in the traditional lending market. That doesn't scream confidence. That's also why most of these funds have high yields.

The good thing is that there are some fantastic companies on the market.

While investors are still investing in loans with elevated risks, there are great ways to generate a very satisfying risk/reward by doing so. This includes buying companies with competent management and backing from larger corporations.

One of them is FS KKR.

Why I Like FSK's 15% Yield

The New And Improved FSK

As I already briefly mentioned, the FSK chart was a major turnoff for me. The stock has lost roughly half of its value since 2015, which means that investments in companies like Ares and Main Street Capital (MAIN) seem to be the better option.

FINVIZ

However, FSK has changed. It isn't what it was back in 2015.

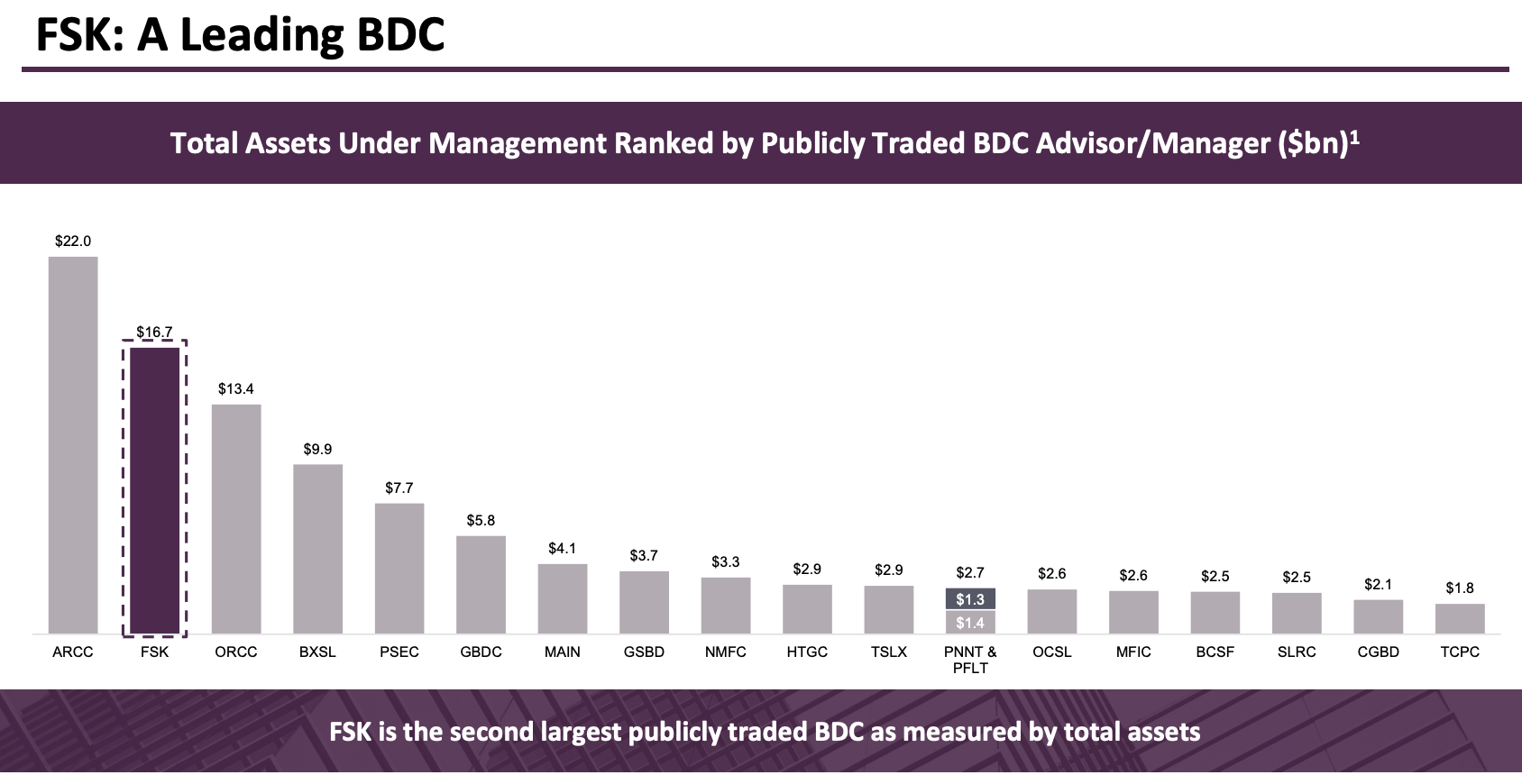

Using a company slide from last year, we see that FSK was different prior to 2018. Since 2018, the company has merged six separate BDCs, which includes the merger between FS Investment Corporation and Corporate Capital Trust.

Hence, the FSK ticker emerged in 2018. Before 2018, we were essentially dealing with a whole different company, a company that had the second-largest assets base in its industry last year.

{kind=link}

Additionally, in 2021, the company completed its acquisition of FS KKR Capital Corp. II through a merger agreement. Following the merger, the company entered into a new investment advisory agreement with FS/KKR Advisor, LLC.

In other words, FSK is a relatively young company. It has little in common with the somewhat poorly managed BDCs of the past.

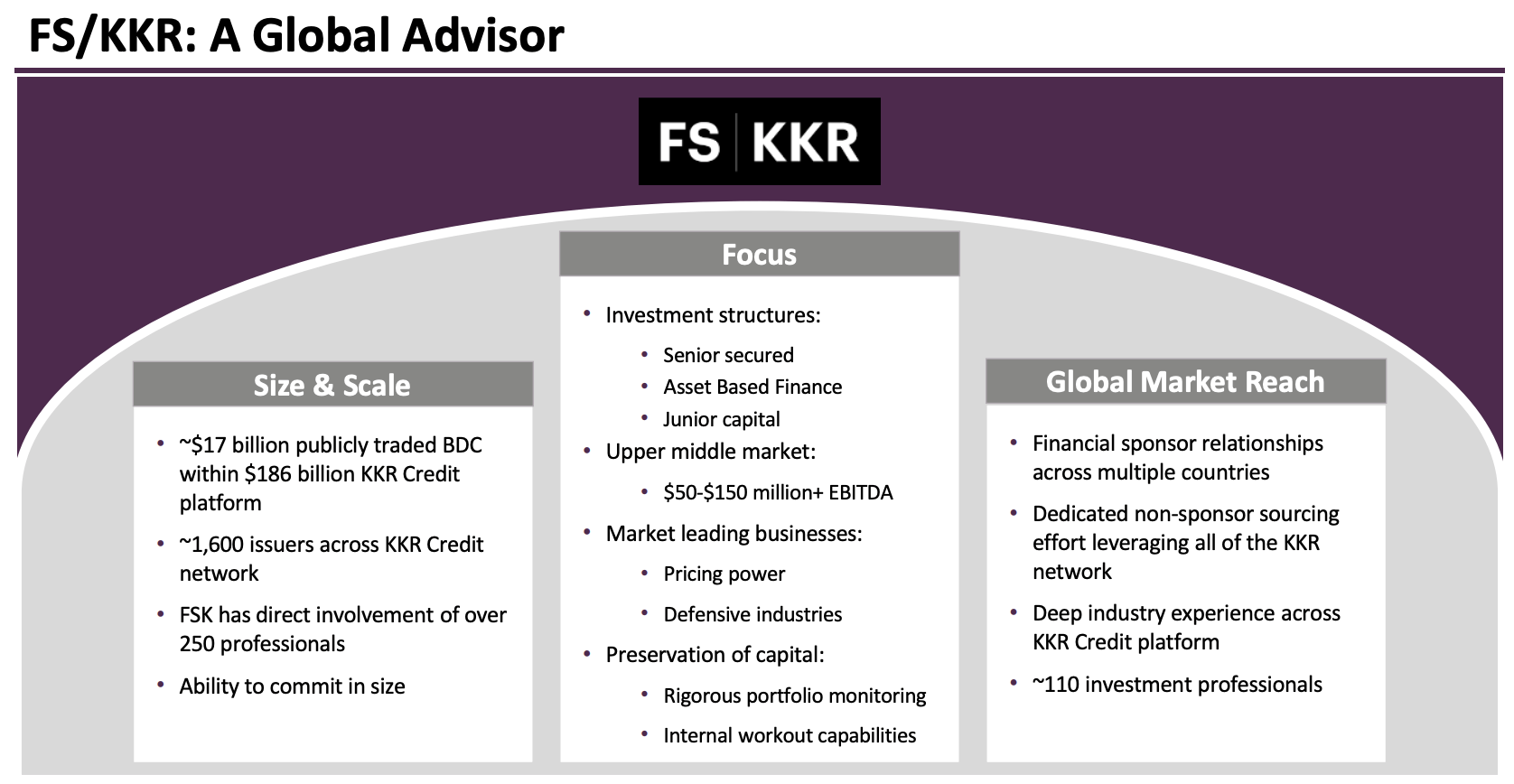

Now, FSK is one of the nation's largest BDCs with backing from strong and experienced asset managers. Essentially, the company's advisor is a partnership between an affiliate of Franklin Square Holdings (which does business as FS Investments) and KKR Credit, which is an investment advisor with close to $200 billion in assets under management. It's also a subsidiary of the mighty KKR Corporation ( KKR ).

Now, the company uses its expertise and connections to focus on high-quality senior secured debt in the upper-middle market segments, where it helps companies with pricing power in defensive industries. All of this helps to improve the risk/reward of its juicy dividend yield.

{kind=link}

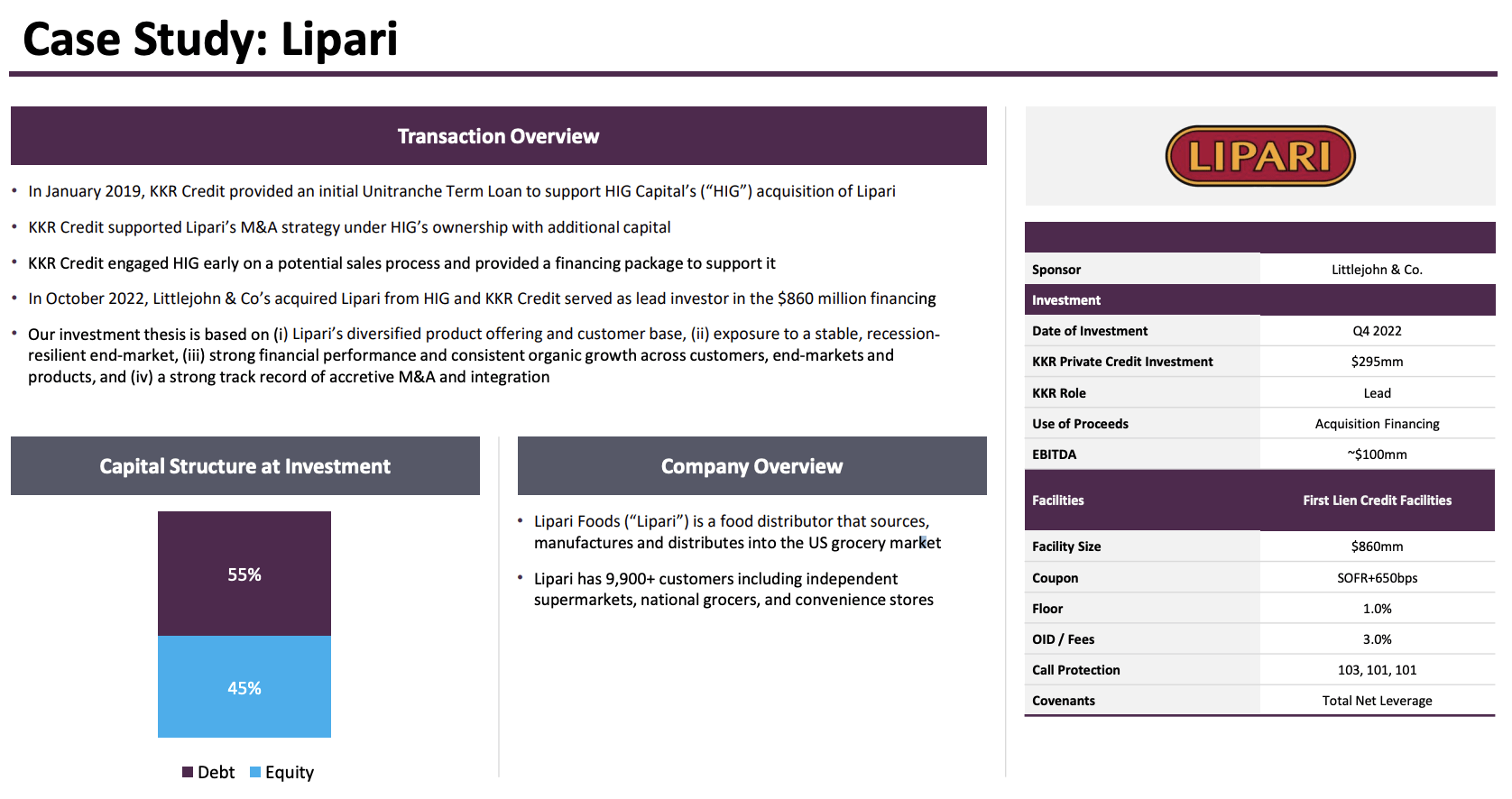

On a side note, the company provided a case study last year, which shows how it does business and how it manages both its clients' interests and the interests of its investors, who seek a balance between risks and returns.

{kind=link}

Thanks to these improvements, FSK shares have outperformed both MAIN and ARCC over the past three years. In this case, I'm comparing FSK to the two other BDCs I like a lot.

With all of this in mind, let's take a closer look at its assets.

The FSK Portfolio & Capital Structure

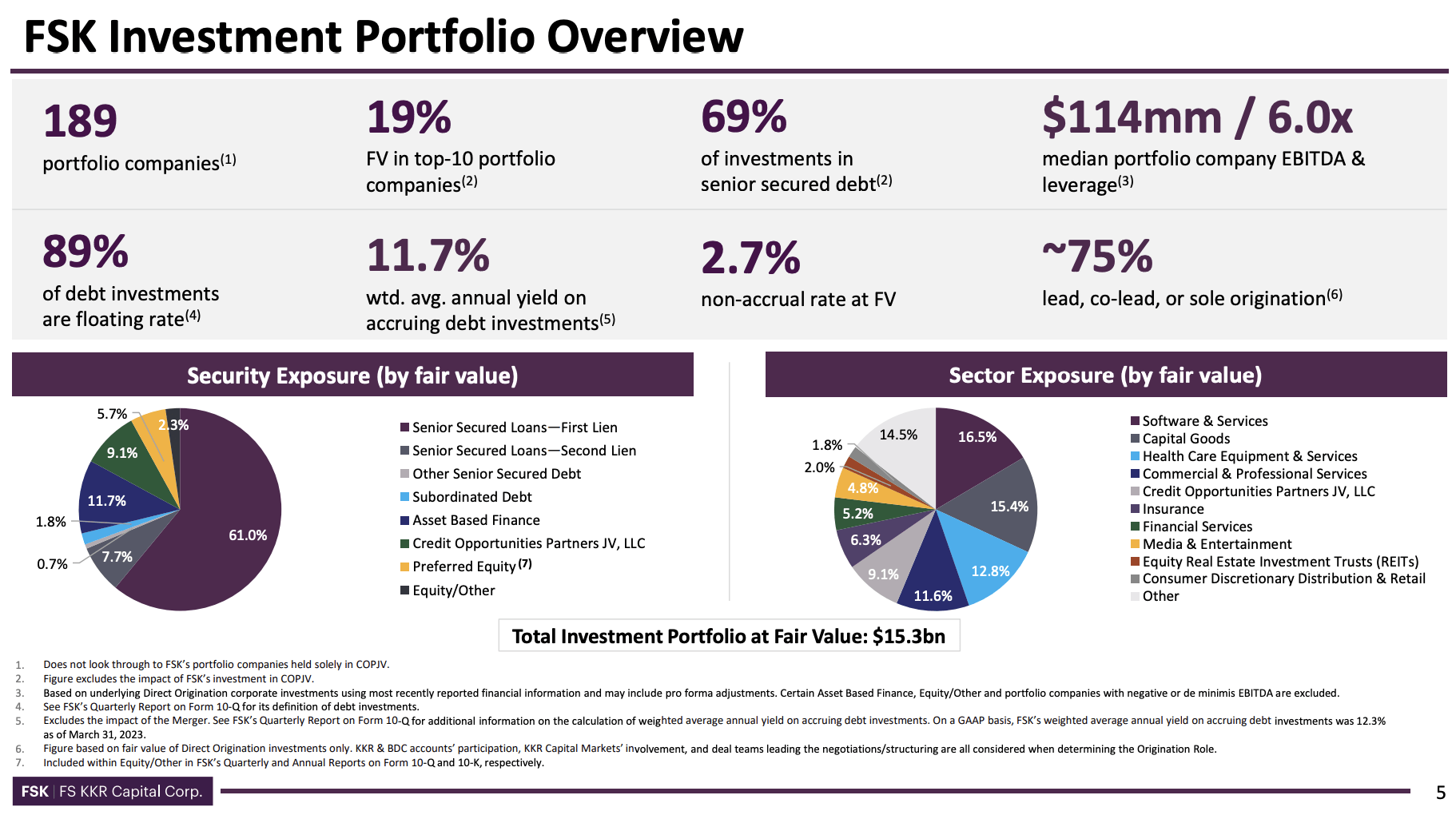

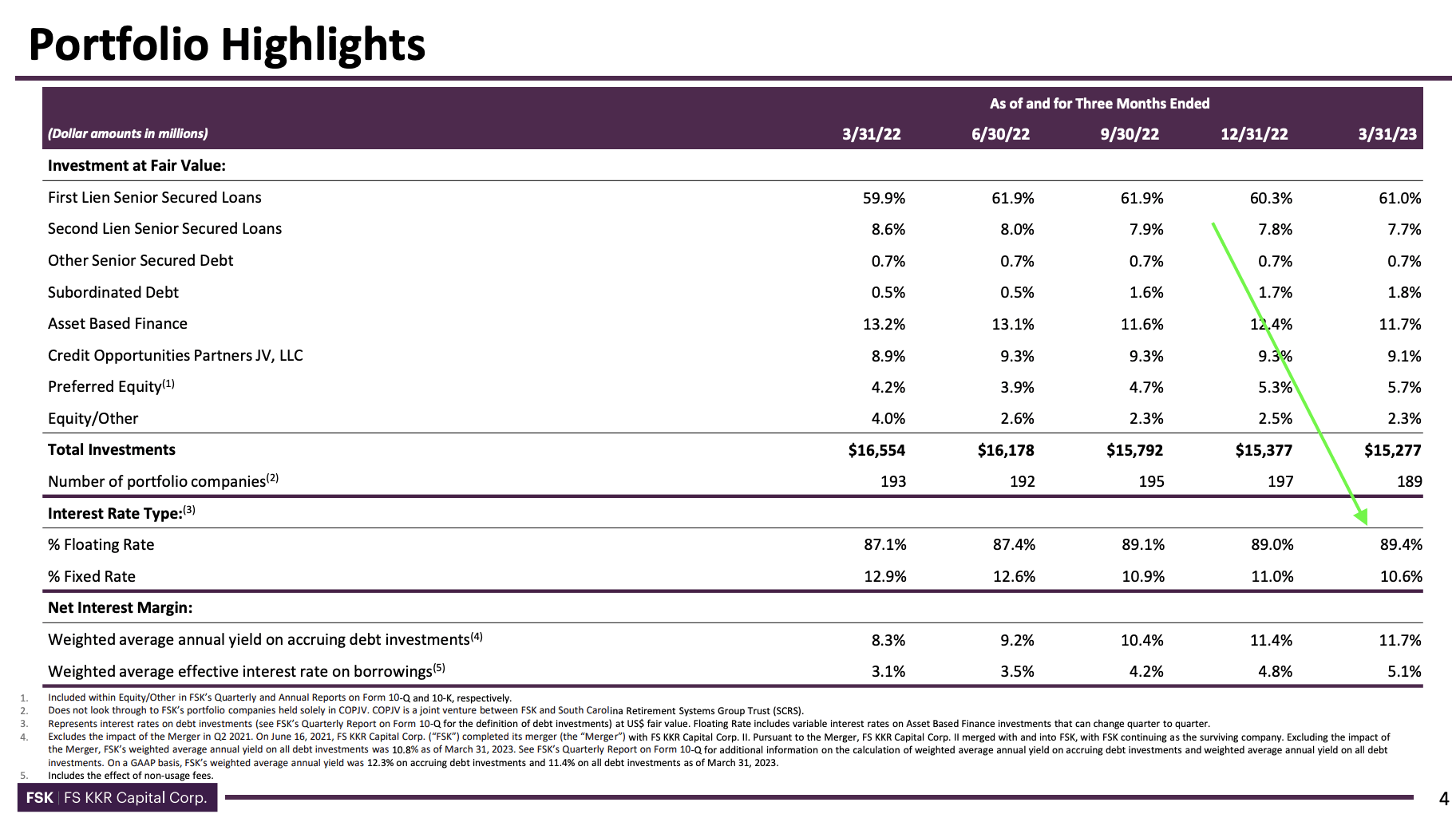

As of March 31, 2023, FSK's investment portfolio had a fair value of $15.3 billion, consisting of 189 portfolio companies. This represents a slight decrease from $15.4 billion and 197 portfolio companies as of December 31, 2022.

{kind=link}

The ten largest portfolio companies accounted for roughly 19% of the portfolio's fair value. FSK continues to prioritize senior secured investments, with 61% first lien loans and 69.4% senior secured debt in the portfolio.

A first lien term loan is senior secured debt that maintains first right on collateral and first payout position.

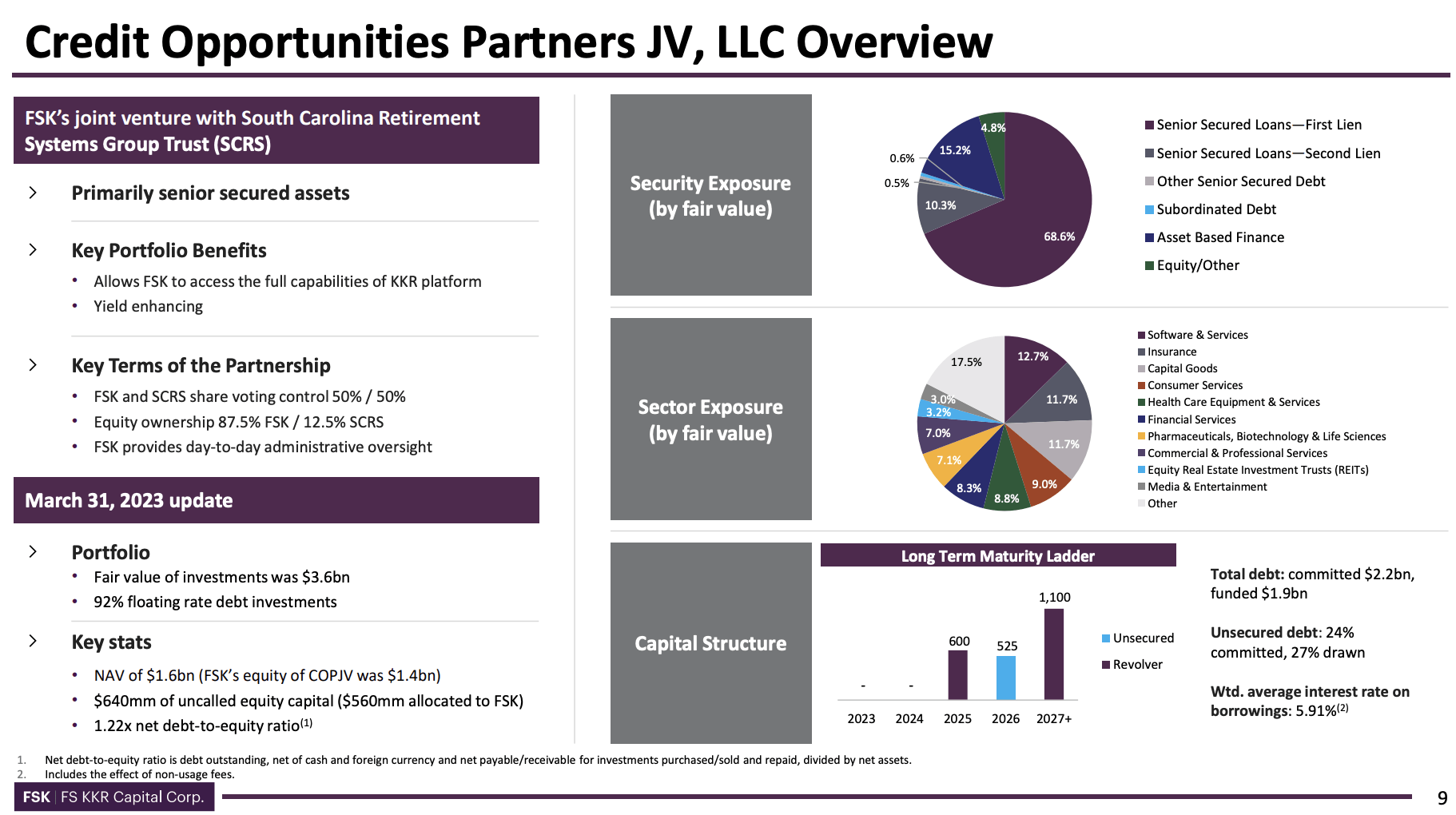

FSK's investment portfolio includes a joint venture representing 9.1% of the fair value and asset-based finance investments representing 11.7%.

{kind=link}

The majority of asset-based finance investments consist of first-lien loans or secured asset-based finance investments.

When considering the investments in the joint venture, 77% of the total portfolio consists of senior secured debt as of March 31.

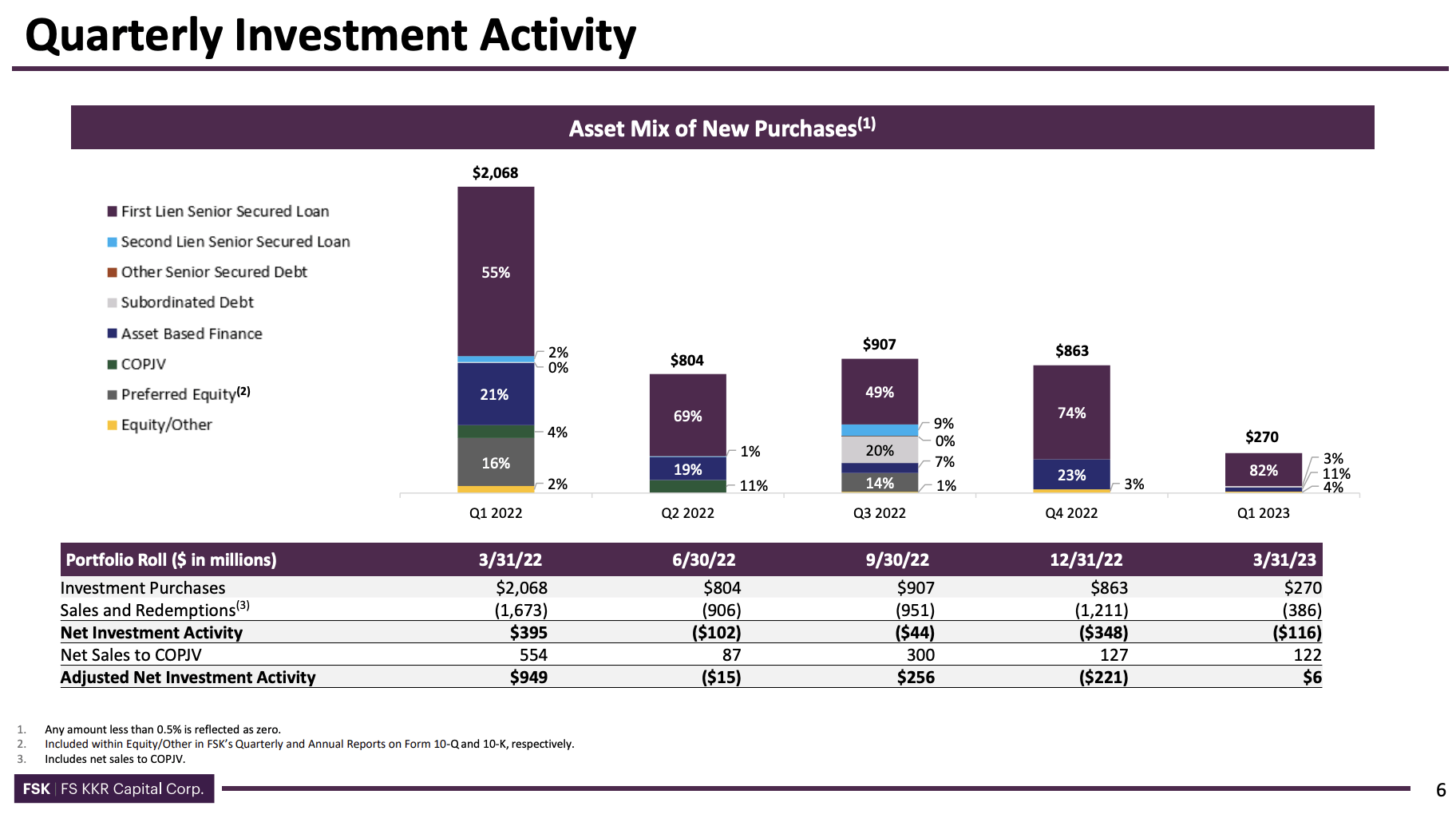

During the first quarter, new originations included roughly 82% in first-lien loans, 11% in asset-based finance investments, 3% in subordinated debt, and 4% in equity and other investments.

{kind=link}

The weighted average yield on accruing debt investments was 11.7% as of March 31, 2023, compared to 11.4% as of December 31. This increase in yield is attributed to rising base rates and higher yields on recent originations.

Related to that, it also needs to be said that 89.4% of debt has a floating rate, which means that rising interest rates result in a higher portfolio yield. This is visible in the table below, which also summarizes some of the other portfolio characteristics we just discussed.

{kind=link}

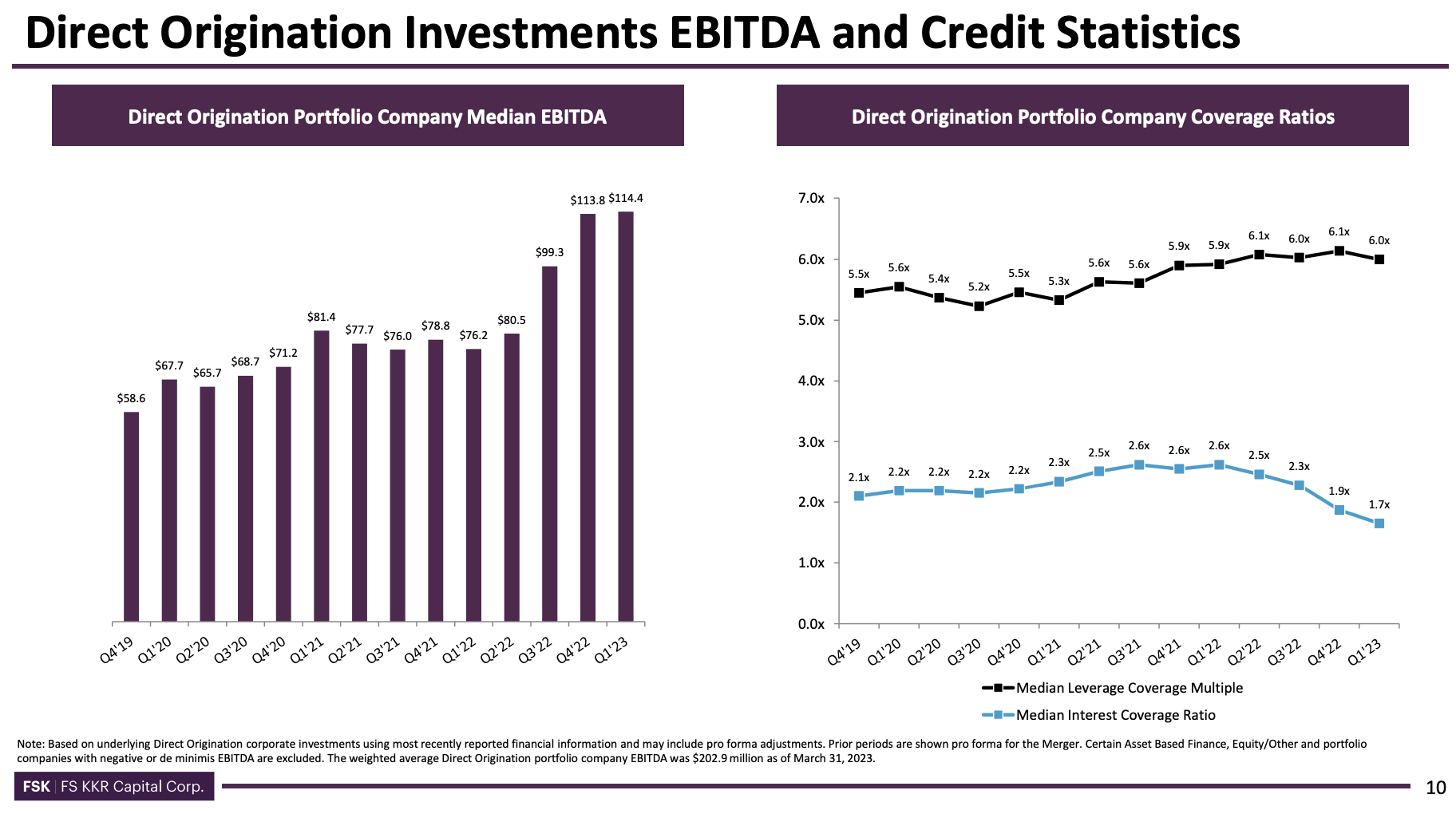

With that said, because of the company's rigorous investment approach, it holds a portfolio of healthy companies. The median portfolio company has experienced an increase in its EBITDA, which is a good sign.

However, it needs to be said that while the median leverage ratio remains unchanged at roughly 6x EBITDA (which is good news), the median interest coverage ratio has started to drop quite significantly since the start of 2022.

Essentially, that's when the surge in inflation and rates started, which increased interest payments due to the floating rate characteristics of most loans. Leverage remained healthy as companies did not have to take on more debt or saw a deterioration in financial health.

{kind=link}

In other words, right now, FSK has a very strong portfolio. The risk here is a recession. A recession could (read: likely will) cause EBITDA to fall, which would further reduce the interest coverage ratio and cause a spike in the median leverage ratio. However, it would have to be a rather big recession to seriously hurt this portfolio.

According to the company :

[...] we remain extremely selective in our underwriting and origination process. Also, during periods of market stress, we benefit from our portfolio monitoring unit and are dedicated workout and governance teams. These dedicated internal teams are able to work seamlessly alongside our deal teams to navigate situations which potentially arise during more challenging operating environments.

That being said, through the end of the first quarter, we have not experienced a significant increase in amendment requests, which we view as a positive .

Furthermore, FSK expects elevated inflation and a more prolonged period of higher interest rates than anticipated by some market observers. In this environment, the company believes that floating rate asset structures and investment strategies with inflation protection, such as large portfolio companies and asset-based finance investments tied to collateral pools, will remain appealing.

I also need to mention that the surge in rates benefits BDCs, in general, as it is harder to get access to traditional funding, as banks are rapidly tightening lending standards.

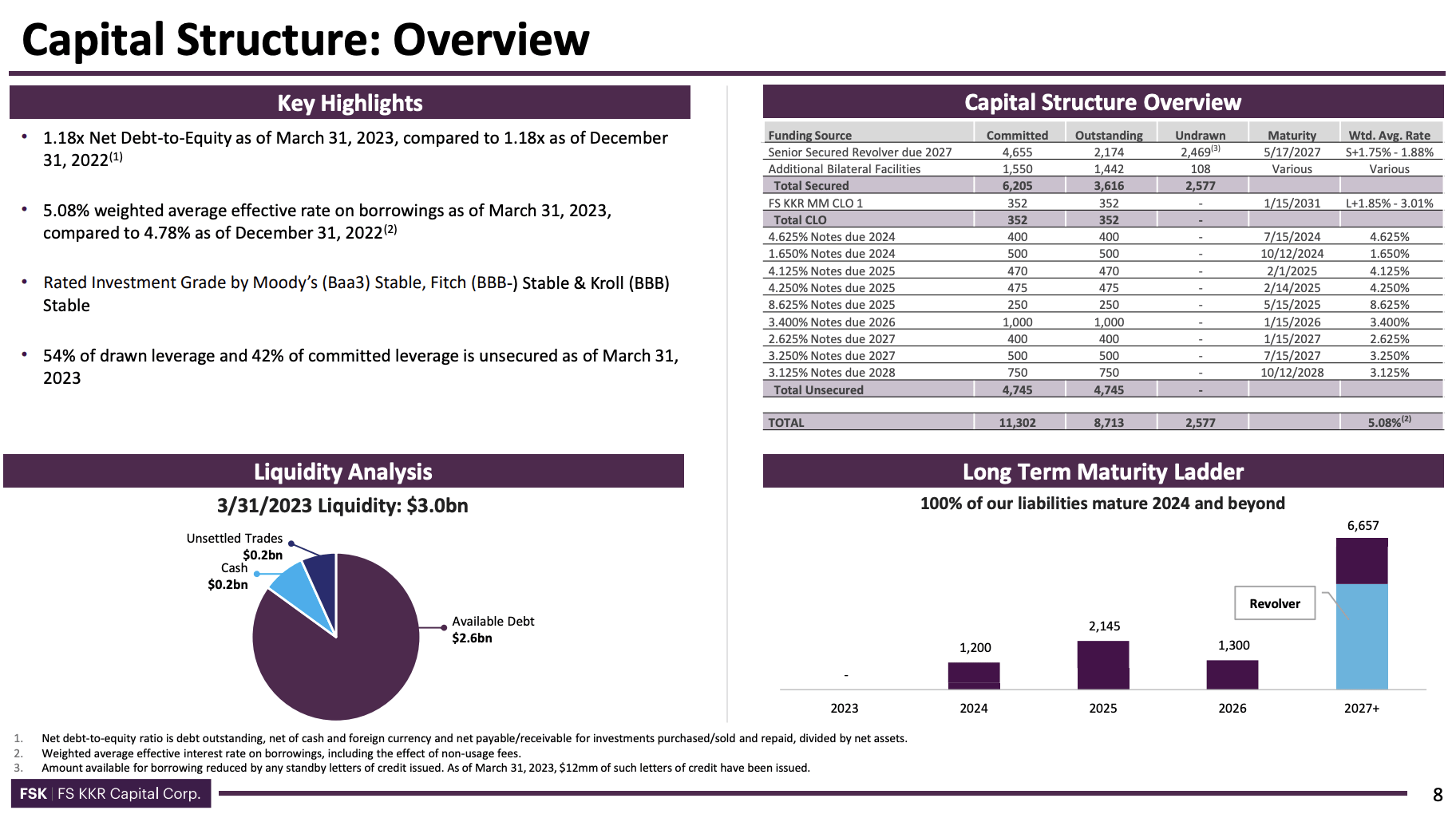

With that in mind, FSK's capital structure isn't bad, either.

The company has no debt maturities in 2023, $2.6 billion in available debt, a net leverage ratio of just 1.2x, and a credit rating of Baa3/BBB-.

{kind=link}

So, what about the dividend?

The FSK Dividend

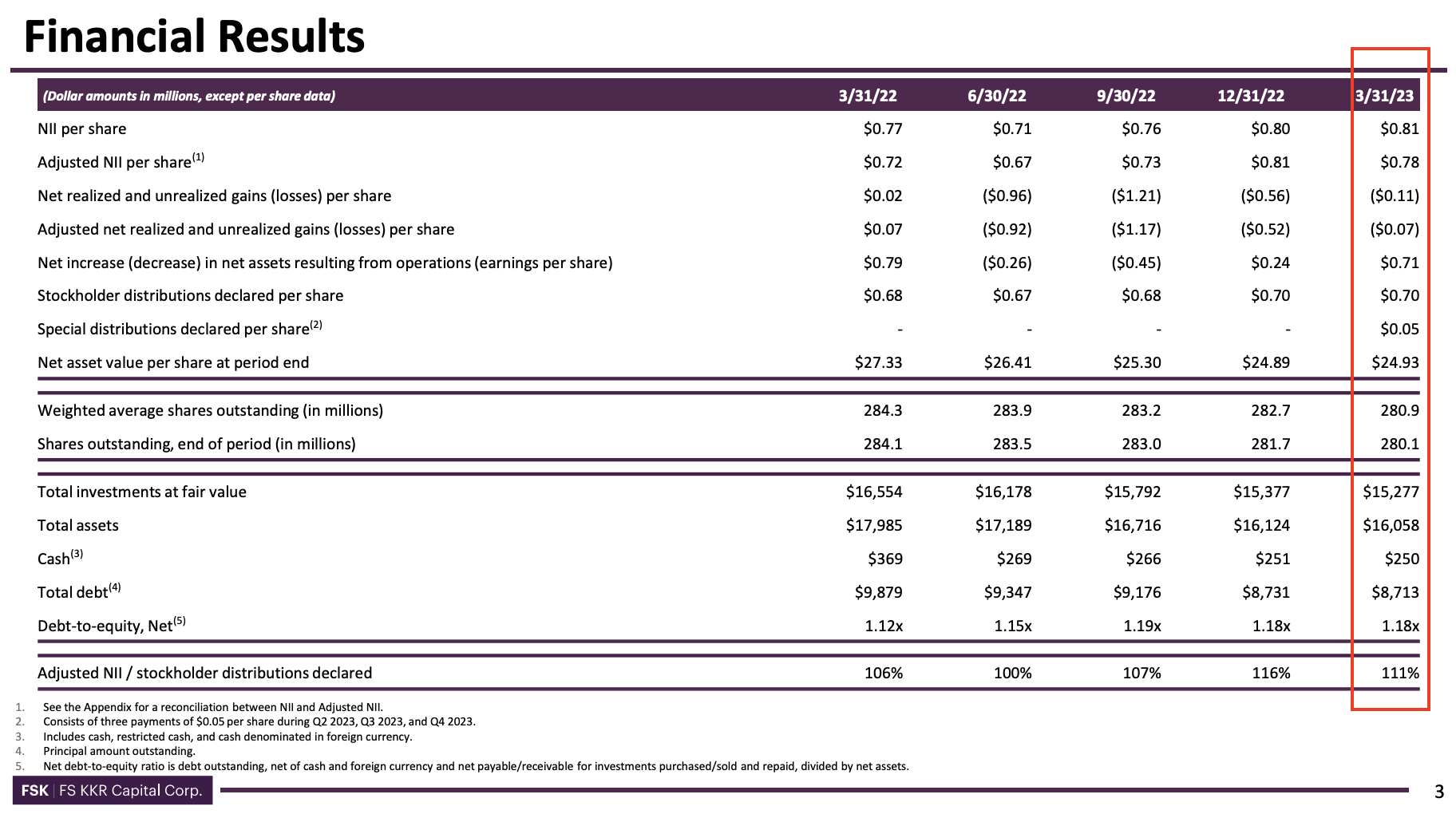

In 1Q23, FSK's Board declared a second-quarter distribution of $0.70 per share, consisting of a base distribution of $0.64 per share and a supplemental distribution of $0.06 per share. This translates to an annualized yield of 14.7%.

The company expects the quarterly supplemental distribution to be at least $0.06 per share throughout 2023. FSK also announced special distributions totaling $0.15 per share, to be paid in three equal installments by the end of 2023. This additional income is a result of achieving targeted spillback income levels, which is essentially a post-dividend reserve that will now be distributed as a (special) dividend. This further boosts the dividend yield.

{kind=link}

The company's dividend coverage is 111%.

Please bear in mind that FSK is dependent on net interest income. In 1Q23, that number was $0.78 (adjusted). In times of lower rates and/or portfolio company default, that number will come down, causing the dividend to come down too.

So, please be aware that this 15% yield isn't safe.

The biggest takeaway here is that its dividend will remain juicy in the double-digit range, but not necessarily 15%.

Valuation

FSK is one of the few high-quality BDCs, which is trading below its book value. Not only that, but it's trading at $0.76 for every dollar in book value.

At this point, I would make the case that this is well-known. It took me roughly 10 seconds to produce the chart above. Every asset manager in the world can look this up. So, this valuation isn't a hidden secret.

That said, I believe a discount this big is not warranted. FSK is a much better company than it was a few years ago. It has a great balance sheet, a strong loan portfolio, and it's backed by competent advisors.

While I won't make the case that FSK will suddenly rise 25% to make up for its valuation discount, I believe that FSK will likely outperform its peers on a prolonged basis.

I really like the stock and would be a buyer if I required a higher portfolio income.

Takeaway

FS KKR Capital Corp. is a business development company that offers a compelling income opportunity for investors. Despite its previous poor performance, FSK has undergone significant changes since 2018, merging with other BDCs and gaining strong backing from experienced asset managers.

With a current yield of 15% and a focus on high-quality senior secured debt in defensive industries, FSK presents a favorable risk/reward profile. The company's portfolio consists of healthy companies, although there is a potential risk during a recession.

FSK's capital structure is solid, with no debt maturities in 2023 and a credit rating of Baa3/BBB-.

The dividend is attractive, with a yield of 14.7% and a supplemental distribution expected throughout 2023. While the 15% yield may not be sustainable on a long-term basis, FSK's dividend will likely remain in the double-digit range.

Moreover, FSK is trading at a significant discount to its book value, presenting an opportunity for investors.

Overall, I consider FSK to be one of the best BDCs on the market, with the potential to outperform its peers over the long term.

For further details see:

FS KKR: The Best 15% Yield I've Seen So Far