CION - FSCO: Use This Opportunity To Add Safe High Yield Income To Your Retirement

2023-09-04 12:15:56 ET

Summary

- I apply an Income Compounder investing strategy to focus on generating passive income in retirement through high-yield investments.

- With the backing of FS Investments, FSCO dynamically allocates to private and public credit markets to generate an attractive total return.

- FS Credit Opportunities has seen its price rise and its discount to NAV narrow, making it a potentially attractive high-yield investment option.

You work hard for decades, plan for retirement, save as much as you can, and reduce your spending so that when the time comes you can enjoy the golden years. There are many ways to save for retirement including investing in individual stocks, bonds, mutual funds, ETFs, CEFs, REITs, and BDCs, many of which pay regular dividends. Over the past several years as my retirement date approached, I changed my investing tactics from a growth-oriented strategy to develop what I call the income compounder portfolio. And now that I have officially retired, I am in a solid financial position to generate passive income from my investments that pay dividends on a quarterly and, often, monthly basis.

I have written several articles recently highlighting some of the high-yield investments that I hold in my Income Compounder portfolio - see Moving My Cheese - An Income Compounder Portfolio Update . For yield chasers seeking very high yields that exceed 15% annually, I provided some ideas here . In another recent article, A Dozen Income Picks Yielding 12% Or More , I highlighted another dozen securities that offer yields exceeding 12%. In that article, I discussed a couple of winners and a couple of what I like to call learners (rather than losers, because I always learn something from my bad investments).

One of the learners that I discussed in that article is Brookfield Real Assets Income Fund (RA). When I published the article in early July, the fund had just announced yet another in a series of inline monthly distributions of $0.199 per month, which the fund had faithfully paid every month following its inception date of December 2016. Unfortunately, the fund was unable to continue covering that high yield distribution and announced on August 29 that starting in October the monthly dividend will be reduced to $0.118 per share, a drastic decrease of about 40%. The takeaway from that investment experience is that even if there is a long history of paying a steady distribution, that does not necessarily mean that the future will continue to perform just as well. This is especially true in the case of RA, when most of the holdings include infrastructure, energy, and fixed-income assets such as MBS (mortgage-backed securities), all of which have suffered from rising interest rates.

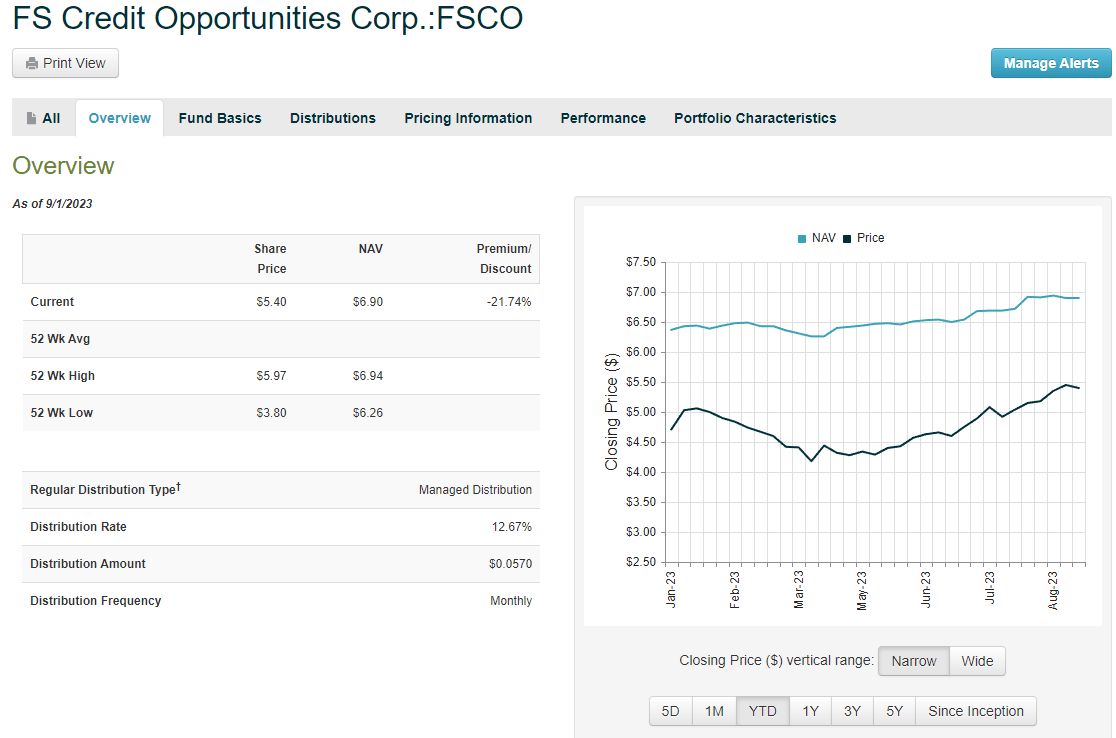

On the other hand, (a phrase that many economists love to use) one of the winners that I highlighted was FS Credit Opportunities ( FSCO ), a relatively new addition to my Income Compounder portfolio. The fund was originally established in 2013 by Franklin Square Capital Partners and went public in November 2022 using a direct listing approach. The direct listing was completed in May when the final third of the company shares were listed and the price has been rising ever since, although it still trades at a substantial discount to NAV, which also continues to increase.

When I wrote about FSCO in early July it was trading at a -25% discount and had just announced a 15% increase in the monthly dividend, to $0.057 per share, resulting in a forward annual yield of ~12.7%. Now, as of September 1, the market price closed at $5.40 and the NAV rose from $6.68 at the end of June to $6.89 as of September 1, narrowing the discount to -21%. The chart below from CEFConnect shows the increasing price along with the rising NAV over the past eight months.

{kind=link}

Fund Overview

The fund adviser, FS Global Advisor, LLC, employs a dynamic credit strategy that invests across public and private credit markets to generate attractive total returns. The portfolio managers include Andrew Beckman, with 27 years of experience, and Nicholas Heilbut, with 25 years of experience. They lead a team of 10 investment professionals each with an average of 17 years of experience with access to FS Investments , a global alternative asset manager. If you are not familiar with FS Investments, they also team with KKR Capital to offer the BDC called FS KKR Capital Corp (FSK), which I have also previously covered and currently own as well.

According to the FSCO fund website as of June 30, 2023, the portfolio holdings consist of 52% first lien senior secured loans, 8% in 2nd lien senior loans, 17% senior secured bonds, 7% subordinated debt, 6% asset-based finance, and 10% equity/other holdings. Those holdings are spread across 85 portfolio companies in diverse industries, with the highest concentration in health care equipment/services.

FSCO website

About 58% of the holdings include floating rate assets (as of June 30) and the funds are split between public and private investments at a ratio of about 55%/45%. FSCO is one of the largest credit-focused CEFs on the market, with about $2.1B in AUM. The fund is almost a hybrid between a CEF and BDC with the mix of investments they manage. In fact, portfolio manager Andrew Beckman addresses this unique aspect of FSCO on the FS Credit Opportunities Corp. ((FSCO)) Q2 2023 Earnings Call Transcript :

So FSCO has a dynamic investment strategy. And as mentioned, we have an allocation to both privately sourced and privately originated and structured investments, as well as more liquid investments that are made through traded securities. We think that differentiates us from a typical closed-end fund. It kind of puts us in between a closed-end fund and a BDC. And as such, our fee structure straddles the closed-end fund space and publicly traded BDCs. So our management fee is in between the two. And if you look at our incentive fee, we have an incentive fee on income. We do not have an incentive fee on capital gains and our incentive fee is also in between not having an incentive fee and the incentive fees that BDCs have.

Distributions and Liquidity

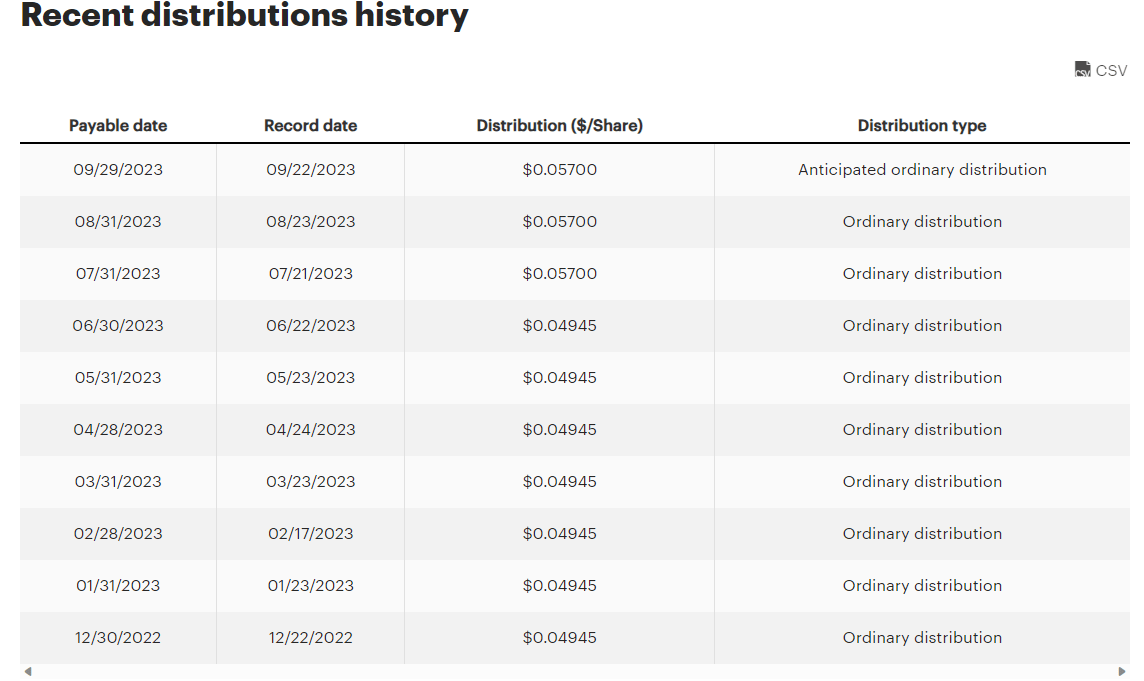

The fund has a short history as a public company and as such, there is not a lot to be gleaned from the distribution history except to note that it was recently raised as I mentioned above.

{kind=link}

The distributions are based 100% on NII and are well covered as explained by Andrew Beckman on the earnings call.

The Fund offers a highly attractive annualized distribution yield of approximately 9.9% based on NAV and a current yield of approximately 13% based on stock price, which we believe is attractive on an absolute and relative basis compared to our peers. The distribution has been fully covered through net income since I joined FS Investments and the current investment team assumed management of the Fund in January of 2018. Over that time, net investment income has represented 116% of distributions paid to shareholders.

Leverage employed by the fund amounted to about 34% as of June 30 with a debt mix of roughly 40% debt and 60% preferred stock. On August 1, the fund paid down $100M of debt maturing during the month, and as a result, the remaining preferred debt matures in 2024 or beyond. The fund had $39 million in cash on the balance sheet and ample availability of credit facilities should a liquidity need arise.

Summary and Risks

The portfolio mix, which is dynamically allocated based on current credit conditions, offers a substantial advantage over similar peer funds that focus on public credit investments only. The access to private credit markets is something that I have seen in other BDCs such as CION Investment (CION), which I have previously covered , but is not as common in a CEF structure, at least not to my knowledge. That advantage is discussed in the Q&A portion of the earnings call by Andrew Beckman in response to a question regarding where the best investments are being seen now:

So if you ask me about private versus public credit right now, I would tell you private credit is more attractive. We can get the returns we're looking for and the structured documentation and covenants we're looking for. Within private credit, we tend to find the best opportunities in non-sponsored transactions, so not competing against the huge amounts of capital that were raised in private credit to do sponsor-driven finance. And then, within public credit, we are still focused on some idiosyncratic situations. There are some things that are overlooked by more typical kind of public credit investors. They tend to be event-driven situations. And that's where our focus is there.

There is certainly a risk to future fund performance if the economy in the US should take a sudden downturn and credit markets tighten again. The current bullish market sentiment that seems to be expecting a "soft landing" despite the call for another increase in interest rates could lead to excessive risk-taking in the capital markets in which FSCO plays.

But there are indications that the credit market will remain strong through the 3rd quarter of 2023 and into 2024. This recent insight, Q3 2023 Corporate credit outlook: Can the good times roll? , highlights the strength of the credit market this year and what is likely to happen in the coming months.

Halfway through the year, markets have broadly displayed almost unwavering strength. Absent the brief period of volatility induced by a bout of bank failures in March, markets have moved higher while volatility - as measured by the VIX Index - has fallen to levels not seen since just prior to the pandemic. Credit markets rose alongside equities with riskier, CCC-rated credits, leading the way. Despite stubborn concerns about the potential for a recession later this year or in 2024 - concerns we share - investors have displayed little interest in adopting a risk-off approach so far.

My assessment of FSCO is that the fund managers appear to have their pulse on the credit markets and with the ability to dynamically allocate between private and public credit investments, the fund is generating solid income that supports the high yield distribution. While the fund continues to trade at a substantial discount to NAV, which is rising, and with a recently increased monthly distribution, I rate FSCO a Buy for income-oriented investors who are looking for a relatively safe high-yield investment.

For further details see:

FSCO: Use This Opportunity To Add Safe, High Yield Income To Your Retirement