FSTA - FSTA: Consumer Staples Are Not A Safe Heaven Anymore

2023-10-06 06:55:11 ET

Summary

- Fidelity MSCI Consumer Staples Index ETF has performed poorly in 2023, down over -7%, due to higher rates and lack of a recession.

- The MSCI USA IMI Consumer Staples 25/50 Index provides the framework for FSTA's holdings, which are highly concentrated.

- Valuations for consumer staples are stretched, and growth levels are slowing, leading to a continued de-rating for FSTA.

- Expect further price pressures in the sector until the Fed starts cutting rates.

Thesis

The Fidelity MSCI Consumer Staples Index ETF ( FSTA ) is an equities exchange traded fund. The vehicle invests at least 80% of its assets in securities included in MSCI USA IMI Consumer Staples 25/50 Index , and uses a representative sampling indexing strategy.

Consumer staples are considered a defensive sector in the equity market given the propensity of consumers to satisfy basic needs even in recessionary times:

The term consumer staples refers to a set of essential products used by consumers. This category includes things like foods and beverages, household goods, and hygiene products as well as alcohol and tobacco. These goods are those products that people are unable-or unwilling-to cut out of their budgets regardless of their financial situation. Consumer staples are considered to be non-cyclical, meaning that they are always in demand, year-round, no matter how well the economy is-or is not-performing. As such, consumer staples are impervious to business cycles.

FSTA has not been a safe haven in 2023, being down over -7%:

The main culprit for this state of affairs is constituted by rates. When risk free rates were 1%, consumer staples funds like FSTA represented viable alternatives with their 2.5% yields. Not when risk free rates are at 5%.

The second culprit for a poor showing by FSTA in 2023 is represented by the lack of a recession. Investors came into the year defensively positioned, waiting for a major sell-off in Q1 that never materialized. As the AI revolution took hold and capital started piling into tech mega-caps, it moved out of classic 'defensive' sectors such as consumer staples, utilities and health-care.

Many institutional investors have strict investing mandates that do not allow the portfolio managers to sit in cash above certain thresholds (10% is usually the top of the range). When portfolio managers expect recessions they tend to cut high beta equities in favor of defensive ones like FSTA. However, when the economic and markets pictures improve, the fund flows reverse. This is what we are experiencing in 2023.

Historically the MSCI IMI Consumer Staples Index has posted mostly positive annual total returns:

MSCI IMI Consumer Staples Index Performance (Index Fact Sheet)

We can see from the above table that the only years with negative total returns were 2018 on the back of higher rates, and 2022 on the back of a wide-spread market sell-off. We are of the opinion we will add 2023 to that list, with a forecasted negative price return to exceed -10%.

MSCI USA IMI Consumer Staples 25/50 Index

As per its literature, the index attempts to isolate consumer staples companies in the small, mid and large cap sectors of the market:

The MSCI US IMI Consumer Staples 25/50 Index is designed to capture the large, mid and small cap segments of the US equity universe. All securities in the index are classified in the Consumer Staples sector as per the Global Industry Classification Standard. The index also applies certain investment limits to help ensure diversification--limits that are imposed on regulated investment companies, or RICs, under the current US Internal Revenue Code.

The index provides the framework which is used by FSTA to purchase its constituents. FSTA is passively managed, thus portfolio managers do not try to extract alpha by having allocations which digress from the index.

FSTA Holdings

The ETF is composed of traditional consumer staples sub-sectors:

Sectors (Fund Fact Sheet)

The highest weighting is assigned to Beverages, followed by Merchandise and Household Products.

Its top holdings are highly concentrated:

Top Holdings (Fund Fact Sheet)

The top-10 names in this fund account for over 61% of the collateral pool., while the top-50 names represent more than 93% of the fund. Total holdings in the ETF come to 107 names.

Valuations are stretched at current forecasted growth levels

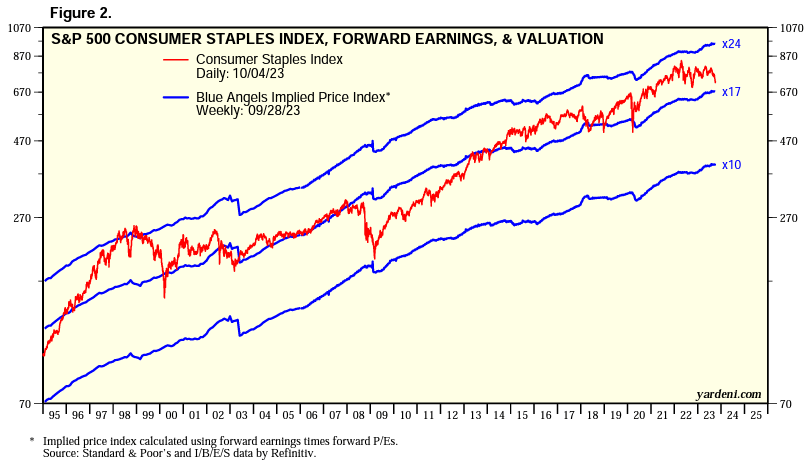

From a P/E standpoint, current valuation levels are close to historic high levels:

{kind=link}

The red line in the above graph courtesy of Yardeni gives us the sectoral P/E ratio. We can see the line at 18x, after it had spent last year above 20x. A similar rates environment was present in 2018, when the Fed started raising rates. We can see P/E levels in the sector moving down during that time frame, and breaching 17x prior to moving back up after the Fed started cutting Fed Funds in 2019. It is not going to be different this time around. Expect a continued de-rating until the Fed starts cutting rates again.

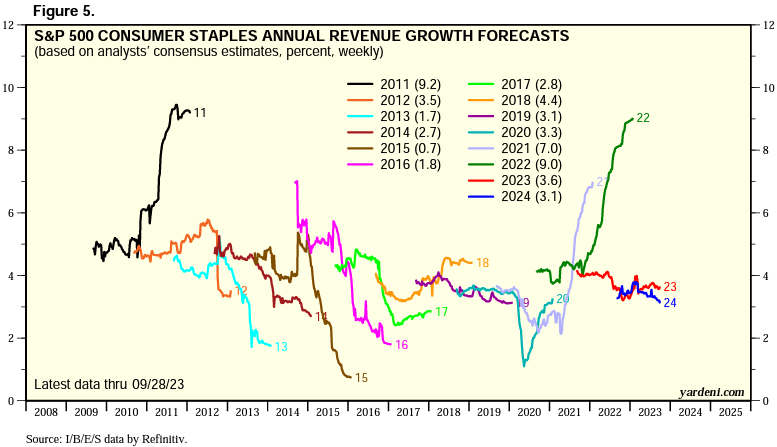

Another valuation aspect moving against consumer staples presently is represented by a very significant slowdown in growth levels:

{kind=link}

The above graph presents in a table and graph format the yearly revenue growth forecasts. So while 2022 was a great year with a 9% growth rate, 2023 and 2024 are seeing growth estimates at only 3.6% and 3.1% respectively.

The lower the growth rate for a sector, the higher the 'bond like' features for the respective section. As with any bond-like sector, FSTA has been negatively affected by higher rates. If intermediate rates keep going higher do expect FSTA to continue to lose value. We need to see higher growth forecasts for this sector in order for it to be perceived differently in terms of correlations to bond yields.

What is next for FSTA

We feel that higher rates are here to stay, and the fed funds forward market agrees with that statement, pricing a Fed cut only in mid 2024. As long as rates stay elevated, all the factors negatively affecting FSTA as described above, will remain in the equation, thus valuations will remain depressed.

We do not see FSTA outperforming until the Fed starts cutting rates, a mild recession is present, and market participants move capital back to consumer staples. We actually see a continued P/E de-rating during the rest of the year, which should result in a further negative performance for FSTA.

Conclusion

FSTA is an equities exchange trade fund. The vehicle focuses on consumer staples equities via a passive replication of the MSCI USA IMI Consumer Staples 25/50 Index.

Despite its defensive status, FSTA is down over -7% year to date, and more loses are expected. There are a number of factors working against FSTA this year, including higher rates, stretched valuations and investors moving into tech mega-caps as safe havens. As long as rates are high expect a continued P/E de-rating for FSTA. We are a Sell for this name here, expecting to revisit it only once the Fed starts cutting rates.

For further details see:

FSTA: Consumer Staples Are Not A Safe Heaven Anymore