FTAI - FTAI Aviation: Qualified Growth Name Compounding Value At Attractive Rates

2023-11-21 01:58:32 ET

Summary

- FTAI Aviation has unlocked substantial risk capital in just 12 months.

- The company is highly profitable but has high leverage and a small ratio of sales to assets.

- FTAI's position in the aerospace value chain provides multiple points of exposure, and its business returns support the notion of long-term capital appreciation of its intrinsic valuation.

Investment briefing

Readers may recall the spin-off and then reverse merger forming the newly named FTAI Aviation Ltd. (FTAI) at the end of 2022. So far this has been a successful move, unlocking substantial risk capital in around 12 months. Investors have lifted the bid on FTAI's market value this year and the company now trades at 16.5x forward EBIT.

What seems as a highly profitable company, producing 203% trailing ROE , also sells at 44x book value. This skews the investor ROE to the downside. The ROE is also skewed by the balance sheet. This is also a highly leveraged company, with total debt comprising 96% of assets, at leverage of 5.1x core TTM EBITDA.

The company requires substantial capital to run but does so with modest efficiency and business returns. The ratio of sales to assets is small. The company's owned assets + inventories are instead highly profitable, producing 30% trailing post-tax margins in Q3.

Critically, this is a function of the company's rather capital-intensive business model. As a reminder, FTAI owns and buys/sells commercial airplanes + jet engines. It also manufactures aftermarket components with various JVs. Its 2 operating segments are:

- Aviation leasing - where revenues are booked on sales + leasing of aircraft and sale of aircraft engines

- Aerospace products - books revenues on the sale of repaired CFM56-7B and CFM56-5B engines , (inc. used material inventory). A key value driver is the recurring revenue obtained from engine management service contracts. This is where the company holds an obligation to provide replacement CFM56-7B and CFM56-5B engines to customers "as they become unserviceable during the contract term "

Growth is the core focus for FTAI, reflected in the change of its market value from 2022 to the backend of '23. Sales have compounded at >110% for the last 4 rolling TTM periods to Q3 2023, with corresponding 2.5-3x operating leverage on this each quarter. Earnings (which we'll call net operating profit after tax here) are in an uptrend and climbed sequentially from $47mm in 2021 to $344mm last period (TTM values).

Both its business segments appear to be performing well. I would have expected to see capital turnover as the profit driver - but turns out FTAI has got it at the profit margin, implying it has consumer advantages in its offerings.

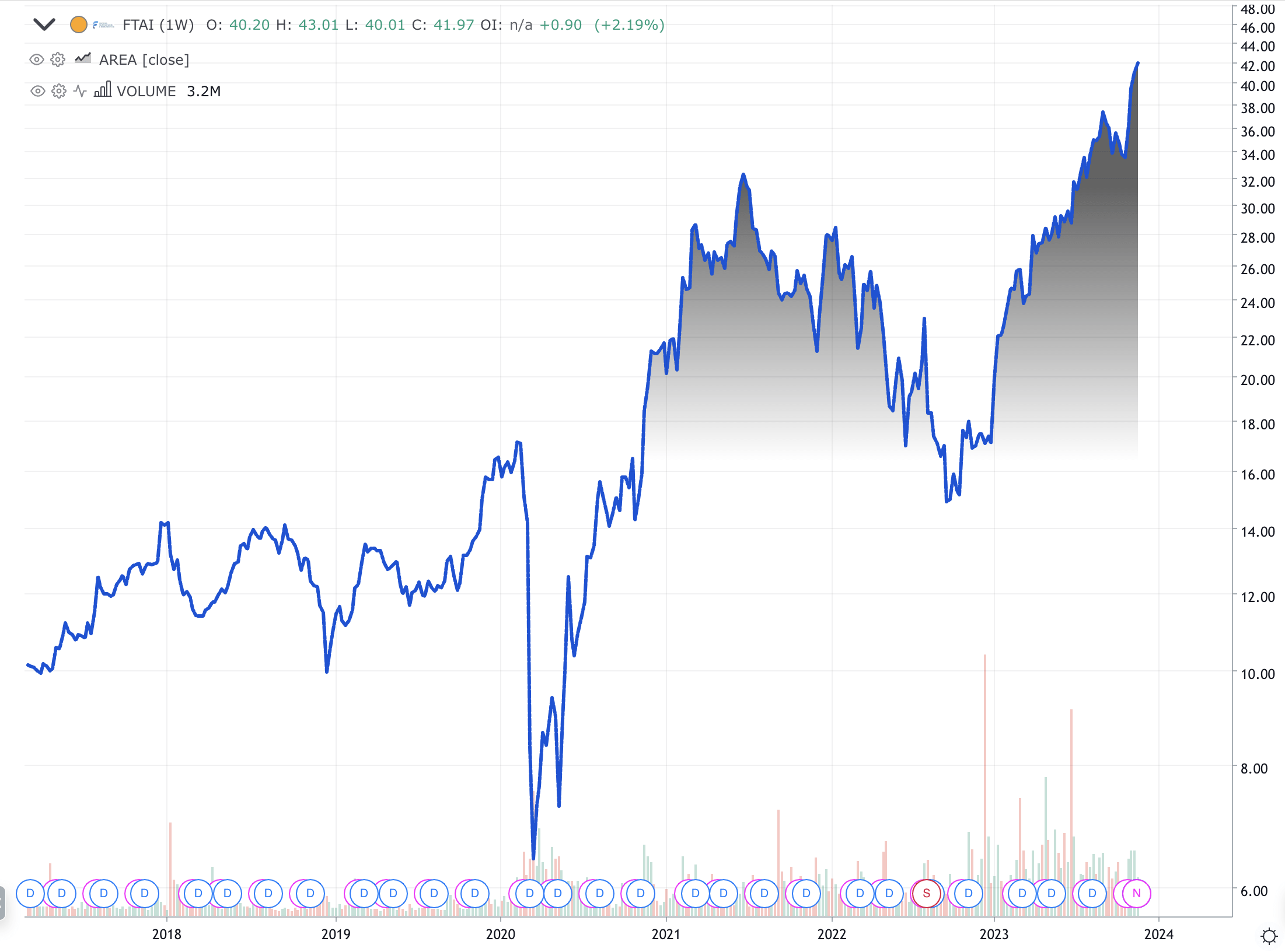

The market believes FTAI is worth its all-time highs (Figure 1), and the question is what's the investment opportunity from here. For those investors seeking long-term capital appreciation, FTAI's business returns exhibit this. For sales + earnings growth with decent multiples, FTAI is competent. Net-net, I rate FTAI a buy across all investment horizons.

Figure 1. FTAI Long-term price evolution

{kind=link}

Talking points

- Industry positioning a competitive advantage

The first point is that global general aviation and avionics sales continue to exhibit robust growth. In Q3 2023, sales were up 10% YoY to ~$814mm, according to the AEA Avionics Market Report. This brings the total in global sales this YTD to $2.42Bn, a 15-16% growth rate from this time last year. As noted in Figure 2, industry growth rates continue to show exceptional growth percentages since 2018.

Figure 2. Historical sales data (inc. growth rates) from AEA Avionics Market Report

{kind=link}

Secondly, FTAI's position along the aerospace value chain provides multiple points of exposure in the one investment security. Remember, the company both owns and sells assets that generate durable cash flows with earnings growth + capital appreciation. Moreover, it has an experienced team of managers with transportation acquisition history. Hence in owning FTAI, you are exposed to transactional and operational features of the industry.

- Factors of economic value

The market has been projecting a period of better business for FTAI in the coming 12-24 months by lifting the bid on its market value. The rally across 2022-'23 is clear indication of this view. Three undercurrents stand out in this regard.

One, FTAI is a capital intensive enterprise. Earnings produced on capital in the business are sensitive to changes given the enormities involved. Secondly, margins and rates on cost are well managed, driving profitability of the firm's assets. Finally, FTAI is reinvesting good percentages of internal cash flows at high rates of incremental returns.

For more on these points, consider the following:

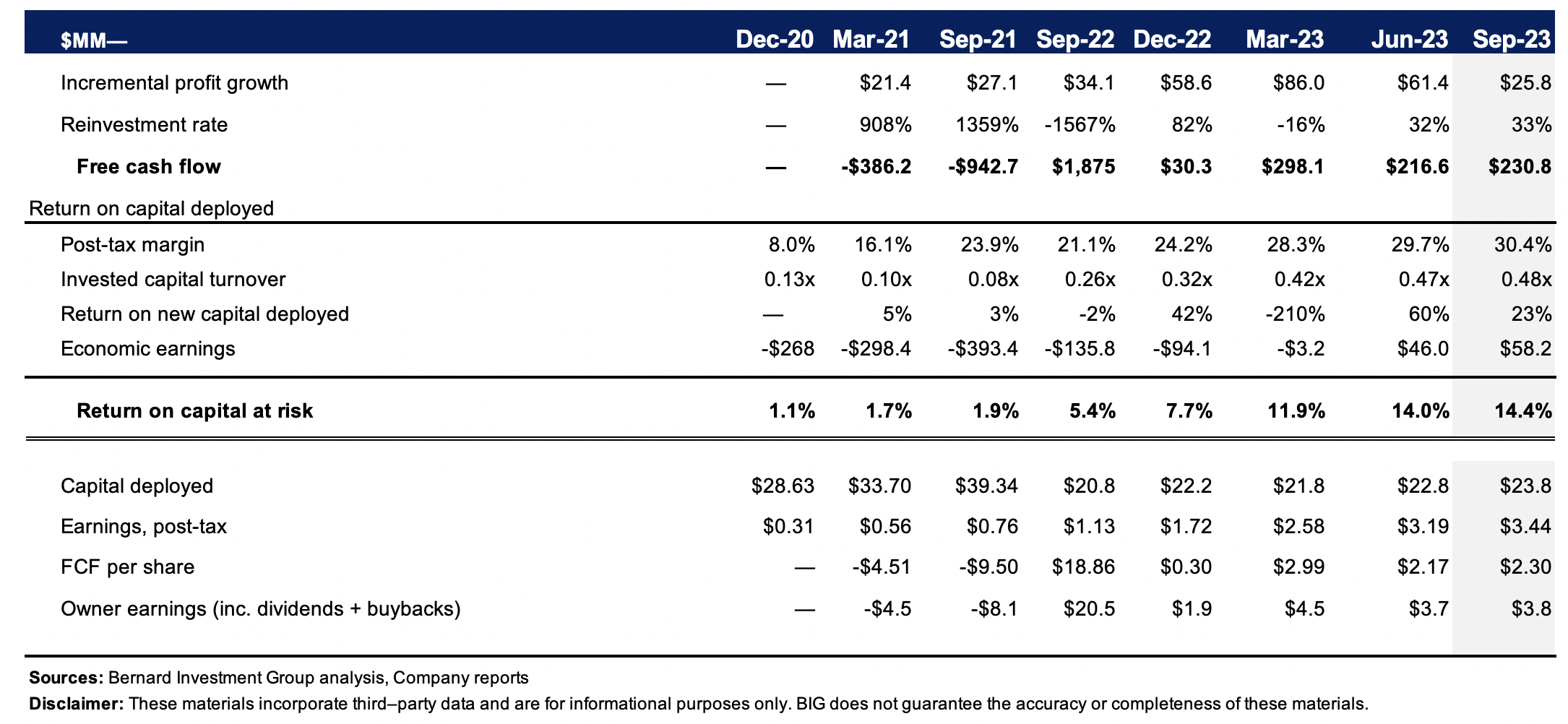

- Structurally, FTAI is far less capital intensive than adjacent participants in aviation (airline operators for example). Utilization, whilst low, is also improving, from 10% in 2021 to ~50% last period. Capital turnover at ~0.5x illustrates the ratio of sales to assets. It does not enjoy production advantages (fits well with the story).

- For what sales are made are profitable. It has increased post-tax margins from 8% in 2020 to 30% in the TTM. This tells me it enjoys consumer advantages and likely differentiates on cost (charges above industry average). Both good signs in the playbook.

- $23.80/share of capital invested produced $3.44/share earnings last period, a 14% return on investment. Notice the sequential gains in return on capital from 2020, 1.1% ROIC to ~14.5%. The market has been eyeing these numbers in my opinion and is weighing FTAI higher based on its propensity to compound capital.

- We have calculated the capital employed using the financing approach as well (not shown here), with negligible difference to the outcomes.

Figure 3.

{kind=link}

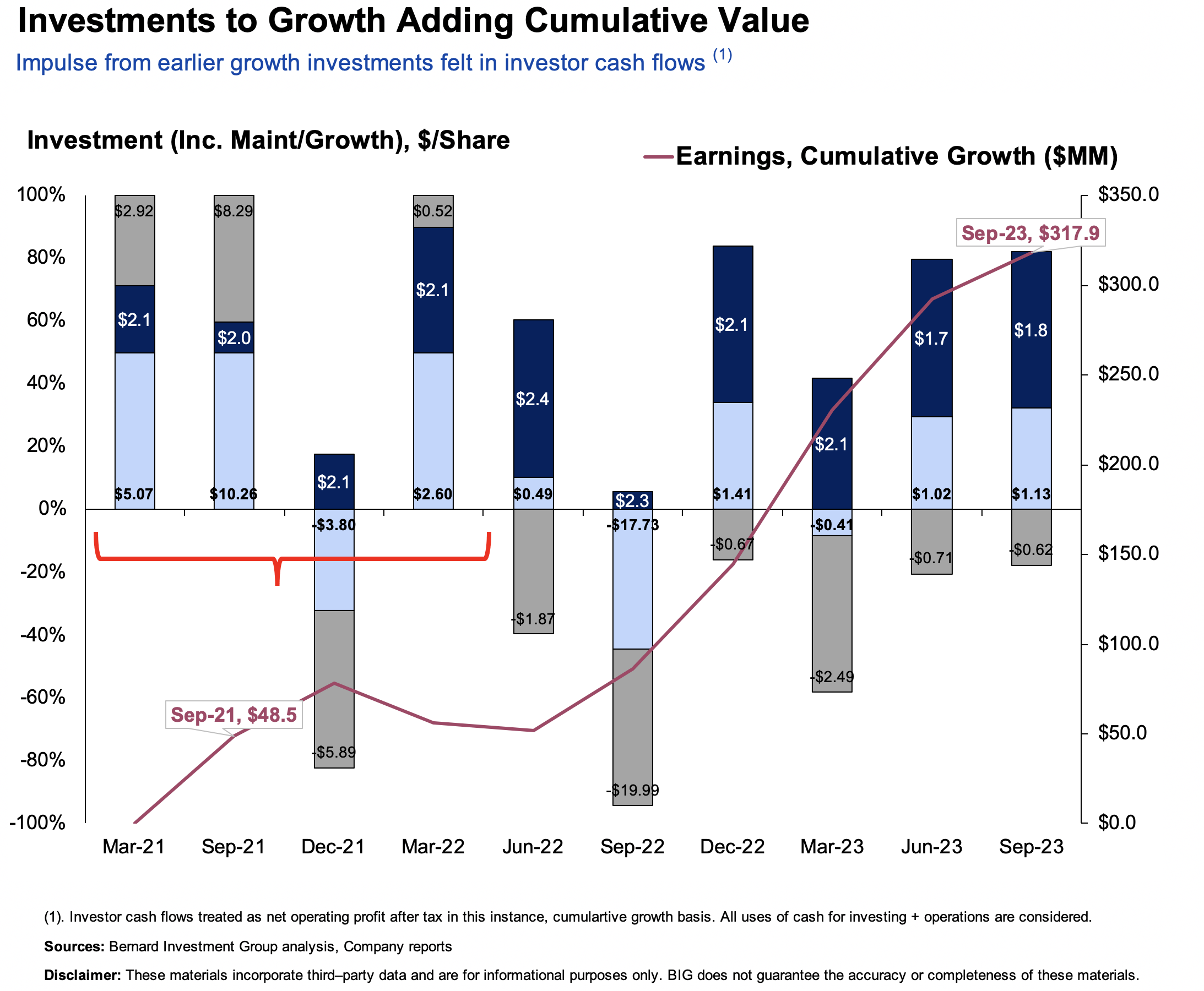

As to where FTAI is reinvesting - firstly, we know it has been allocating heavily to growth capital. Total fixed capital investments (maintenance + growth) were heavy across 2021-'22, as seen via the sky blue bars in Figure 4. Here, we approximate maintenance investment (grey bars) as the depreciation charge. Only investment above this level is considered growth capital.

Since the first CapEx cycle in 2021-'22, FTAI has produced earnings growth from $48.5mm to $317mm over this period. Either (i) the company's new investments have converted to earnings growth, and/or (ii) its existing capital produced the same. Investment in growing the business has pared back for now, with maintenance CapEx steady at $1-$1.15/share.

Figure 4.

{kind=link}

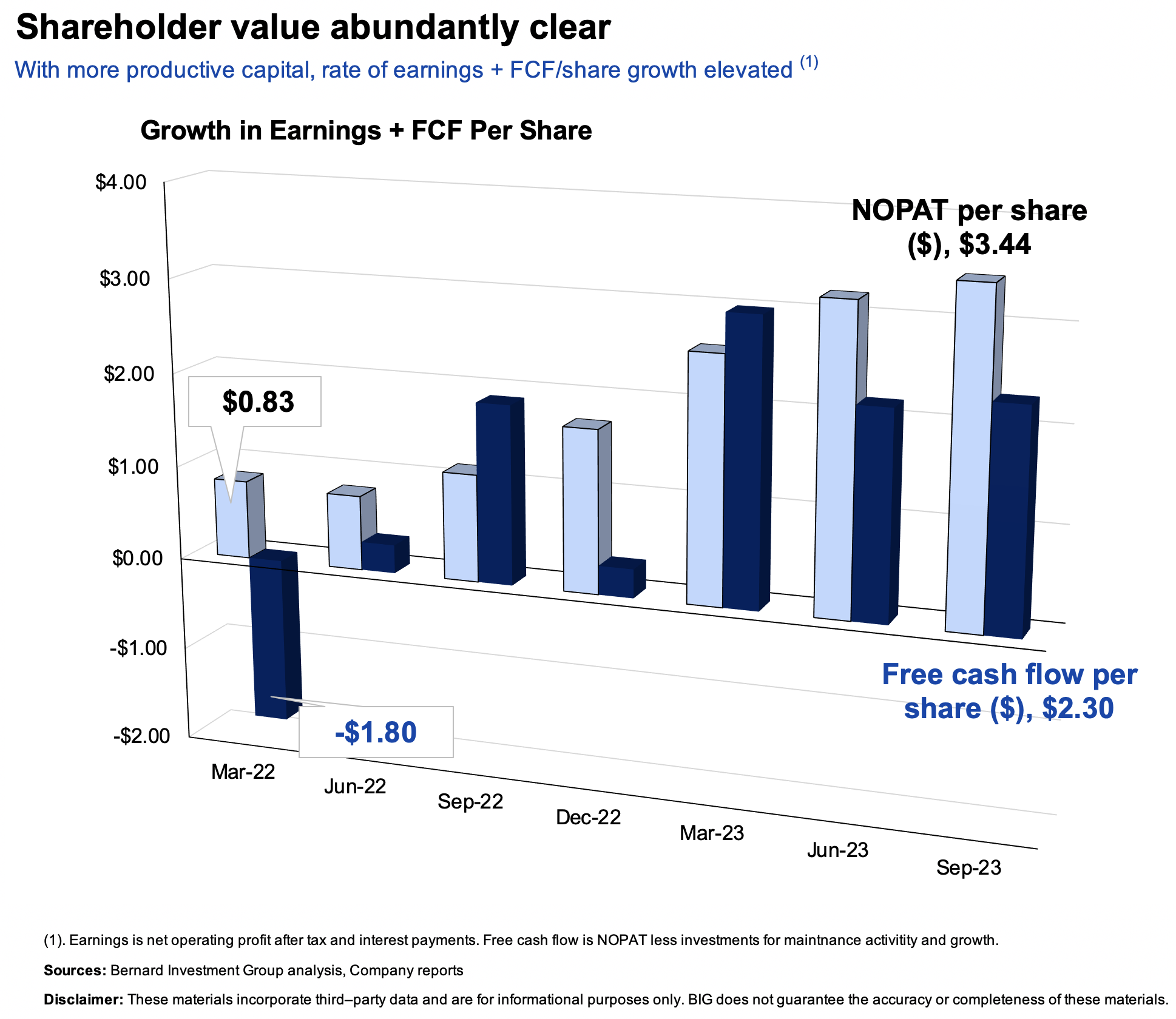

This is exemplified in Figure 5. Keep in mind the context of the company's investment and capital allocation bridge from above. Also of note, is a firm's value is the present value of its cash flows (compared to capital and sales). Trends are important too:

- From Q1 2022 to Q3 '23, FTAI grew post-tax earnings from $0.83/share to $3.44/share (TTM values)

- FCF/share up from negative $1.80 to $2.30

These are exquisitely focal economics that simply cannot be ignored. The ability to allocate growth capital whilst growing earnings for the business and spinning off cash to shareholders. That's one clear path to value in my opinion.

Figure 5.

{kind=link}

Q3 insights

Much is gleaned on next 12 months expectations from the company's Q3 earnings (posted October 26 2023). Robust quarter with growth verticals throughout the P&L. Quarterly EBITDA was $154mm, up 42% YoY. Leasing segment was the main contributor, with roughly 2/3rd of pre-tax earnings vs. $40mm from aerospace. It pulled this to earnings of $0.33 per share.

Management now see adj. EBITDA of $600mm at the upper for FY'23 (full year), with $450mm stemming from leasing income. It also threw some numbers out for '24 guidance. Interestingly, it eyes 2024 pre-tax income of $600-725mm in aviation and aerospace pre-tax income of $250mm. Keep an eye on the mobility of those numbers.

Circling back to the quarter, the specific highlights include:

- The aerospace products segment did $107.1mm of business. It generated $40.6mm pre-tax at a 38% margin.

- The company sold 41 modules Q3'23 to 11 unique customers. The breakdown was 2 new customers and 9 repeat customers.

- Has produced $492mm in FCF year to date. It intends to make all of this available for asset and investment activity.

- It sold $55mm in liquidation value of assets, net gain $17mm. Closed the deal on 23 engines, and 10 aircraft. These could be potentially accretive to aviation earnings.

- Dividend confirmed of $0.30/share, marking the 49th in company's inception.

These percentages align with a company in a more mature growth phase that can redeploy capital to attractive growth projects to compound intrinsic value.

Valuation and conclusion

FTAI's investment outlook for the next 12 months is supported by reasonable attractive starting valuations. The stock sells at 16.5x forward EBIT, just 8% premium to peers at 15x. But the sector is priced low in my view, with 12% ROE, and well below the benchmark indices. FTAI's ROE is exceptionally high given the capital structure - 203% - but reduces to 4% for the investor who is paying 44.5x book value to buy the company today. However, consider:

(1). The market has high expectations for FTAI. It has priced the company at 2.7x EV/invested capital (cleaner measure than P/B), and expects just a 6% required rate to compensate for the risk in owning the company (ranging from 0.6%-15% under various scenarios shown in Figure 6 below). So asset factors are high, along with earnings power in my opinion.

(2). It also sells at 12.2x post-tax earnings, and grew profits by 23% forward last period (4,210/334 = 12.2x). Considering the same 12.2x multiple, the company is worth $5.17Bn (344x1.23x12.2 = 5,170), or $51.70 per share, 26% return objective.

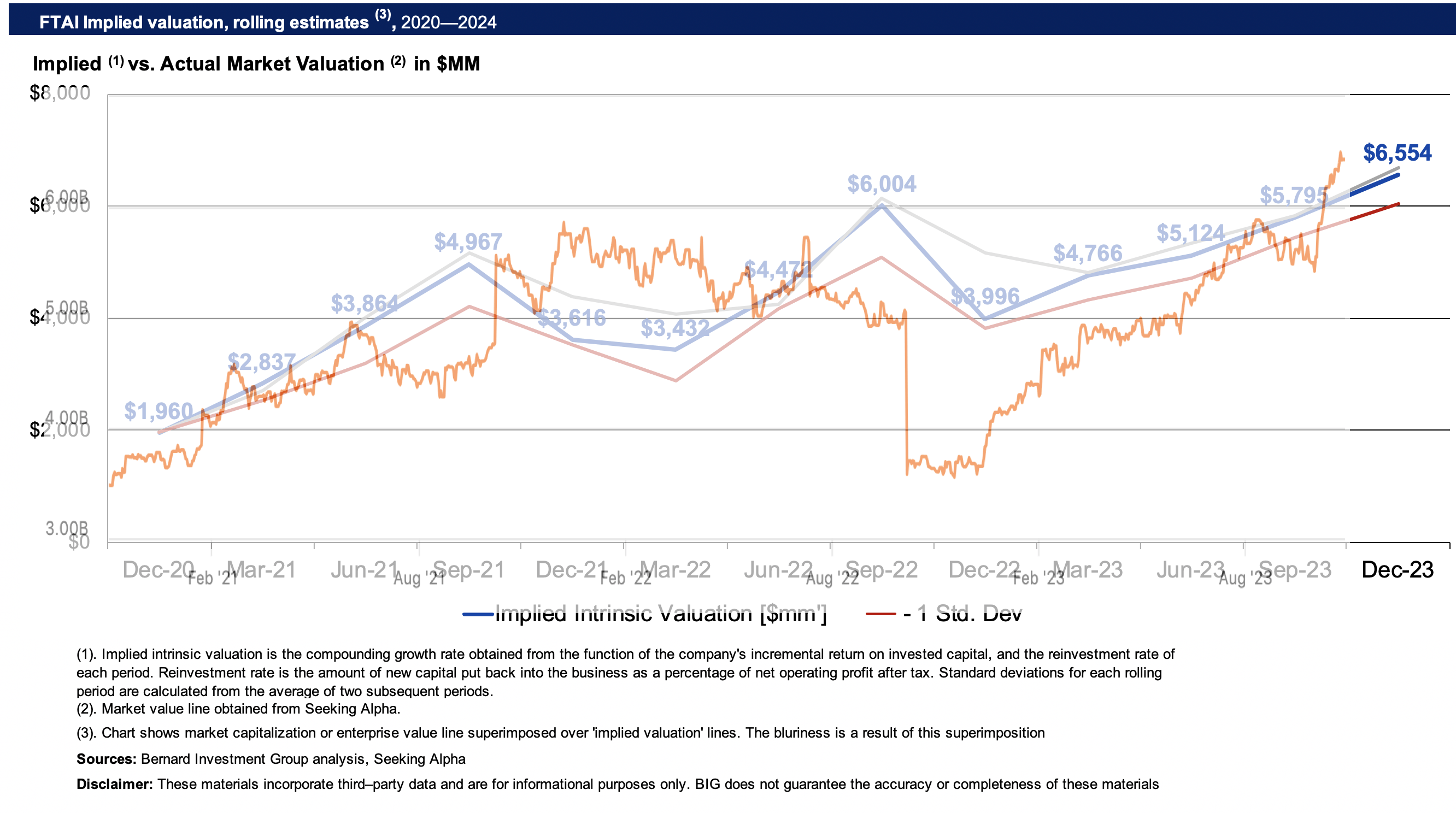

(3). Compounding FTAI's intrinsic value at the function of its ROICs and earnings reinvestment rates, illustrates the market has been a fairly good judge of fair value to this time (Figure 7). Looking forward, an extension of these high expectations could see FTAI trade higher.

Figure 6.

{kind=link}

Figure 7.

{kind=link}

Discussion summary

What you have in FTAI is a sensible company where you're working with a sound investment logic. One, look for company with durable cash flows. Two, filter for those growing said cash flows or earnings. Three, pay a fair price.

FTAI satisfies these 3 criteria in my view. It has proven its exceptionalism to statistically compound capital these past 2 years. Earning growth is in an uptrend, so can continue. It is throwing off plenty of cash whilst doing this, with a strong reinvestment runway ahead. The price of 12-16x post to pre-tax earnings is a fair price for this kind of economics. Normally, this industry is a capital hungry, drought-like environment for investors. All if any profits are typically consumed by the business to maintain a competitive position. FTAI mitigates this somewhat, with a reasonably high margin of FCF to earnings. Net-net, I rate FTA a buy.

For further details see:

FTAI Aviation: Qualified Growth Name Compounding Value At Attractive Rates