FTAI - FTAI Infrastructure: A Cash Cow And A Question Mark

2023-07-17 10:07:10 ET

Summary

- FTAI Infrastructure is a recently spun-off company that owns critical infrastructure, including rail tracks used by major Class 1 railroads.

- The company's core business focuses on investing in infrastructure in sectors such as freight rail, ports and terminals, power and gas, and sustainability and energy transition.

- FTAI Infrastructure's railroad business, particularly Transtar, is a profitable cash cow, while other assets are still developing their potential.

- However, there is one risk that makes me put the stock on my watchlist before I buy it.

Introduction

It has been a while since I have started sharing my research on Class 1 railroads on Seeking Alpha. It all started with the BNSF case study, where I learned from Buffett how to assess a railroad .

Now, this journey leads us a recently spun-off company linked to the industry: FTAI Infrastructure ( FIP ), which owns critical infrastructure such as certain rail tracks that even the major Class 1 railroads need to use.

The company

An overview

As we read from the company's website, FTAI Infrastructure Inc. was "originally formed as part of Fortress Transportation and Infrastructure Investors LLC to develop, acquire, own and operate transportation and energy infrastructure businesses in key markets throughout North America".

On August 1, 2022, it completed its spin-off from FTAI and started trading under the ticker FIP.

The core business of the company is to invest in infrastructure difficult to replicate, such as rail, ports and terminals, and power and gas sectors. Since all of these have a high-barrier to entry, they are assets set to generate strong and stable cash flows with the potential for earnings growth and asset appreciation.

Investors should also know that, given its particular nature, FTAI Infrastructure is externally managed by an affiliate of Fortress Investment Group LLC .

Core business

As said, FTAI Infrastructure focuses on four main sectors: freight rail, ports and terminals, power and gas, and sustainability and energy transition. It develops, acquires, owns and operates transportation and energy infrastructure businesses in North America.

In its first publicly released Annual report we find out how the current portfolio of the company is built.

Railroad

FTAI owns Transtar , a company that owns and operates a group of six freight transportation and rail service businesses that serve a range of industrial markets, as shown from the image below.

FTAI Q3 2022 Earnings Presentation

Transtar is quite small, it only own 273 miles of track, but it has 21 interchanges and 3600 storage spots which show how critical are its properties.

Just to give an example, let's take the Union Railroad Company. It is a Class 3 carrier. However, let take a look at its infrastructure, located in the heart of southwestern Pennsylvania'. As we can see, it operates only a 128-mile network, but it provides its customers direct access to important Class 1 railroads such as Norfolk Southern (NSC), CSX Corporation (CSX) and Canadian National (CNI) and to WLE, a class 2 railroad.

Transtar Rail website

Another example is Gary Railway Company , another Class 3 switching carrier which operates 71 miles of yard track around Gary Works, U.S. Steel's largest manufacturing plant on the south shore of Lake Michigan. It is an interchange for all major Class 1 Railroads (BNSF, UP, NS, CSC, CNI and CP) as well as for other important Class 2 ones.

Ports and terminals

FTAI's ports and terminals business consists of two segments: Jefferson Terminal and Repauno . It is a business strictly linked with energy. In fact, Jefferson Termina sits in Beaumont, TX, one of North America's largest refining and petrochemical centers. It is a critical link for crude oil companies such as Exxon (XOM), Total (TTE) and Valero (VLO).

The Repauno port and rail terminal , is located on the Delaware River and it is a 1,600-acre deep-water, multi-modal storage and logistics facility. Here a variety of natural gas liquids and renewable fuels are stored and transloaded. Formerly, it was known as the home of a DuPont manufacturing facility, but in recent years the site has been redeveloped in a multi-use port. Class 1 railroads such as CSC and Norfolk Southern have access to this important logistical terminal.

Power and gas

This business is primarily comprised of Long Ridge Energy & Power. In 2019, FTAI sold a 49.9% interest for $150 million in cash. Now FTAI no longer has a controlling interest in Long Ridge, but still maintains a significant influence. Long Ridge completed at its terminal in Ohio a few years ago a 485 megawatt power combined cycle gas power plant. The site also has working interests in natural gas production wells and a transloading port and rail terminal.

Linked to this business, the company also focuses its sustainability and energy transition business on investments in companies and assets that utilize green technologies and help reduce the carbon-footprint of many activities.

Currently, the company's portfolio sees three main businesses:

- Aleon and Gladieux. The former is working to develop a lithium-ion battery recycling business across the United States. The latter specializes in recycling spent catalyst produced in the petroleum refining industry.

- FTAI formed a joint-venture with Clean Planet USA ecoPlants to build green plants to convert traditionally non-recyclable waste plastics into ultra-clean fuels and oils, and circular naphtha to support the manufacture of new plastics.

- FTAI owns $10 million in convertible notes of CarbonFree, which has developed patented technologies to capture carbon dioxide from industrial emissions sources and convert it to usable and storable products.

Weight of each business and main customers

As the company reports, at the end of 2022, FTAI's railroad business accounted for 57% of total revenue. Ports and Terminals business accounted for 25% of total revenue. Corporate and other sources accounted for the remaining 18% of total revenue.

As we can easily understand, FTAI's customers consist of global industrial and energy companies, including corporations that refine crude oil and trade petroleum products, manufacturers and local electricity markets and traders. The company discloses that a substantial portion of its revenue has historically been derived from a small number of customers. As of and for the year ended December 31, 2022, the largest customer accounted for 51% of total revenue and 31% of total accounts receivable, net.

This means that from a limited number of customers comes a significant portion of FTAI's revenue. In other businesses this could be a serious risk, however, the importance of the assets the company owns is a protection against this risk since the loss of a customer could be replaced by other important players needing to use that specific infrastructure.

Real competition comes from other infrastructure asset mangers, seeking to acquire other opportunities. But once a certain asset is purchased, the company finds itself with a high-barrier-to-entry infrastructure that can't be replicated in a certain area.

Financials

The company has almost no operating history nor experience as an independent company. This will create a little trouble when looking at its financials, since we only have one annual report actually available.

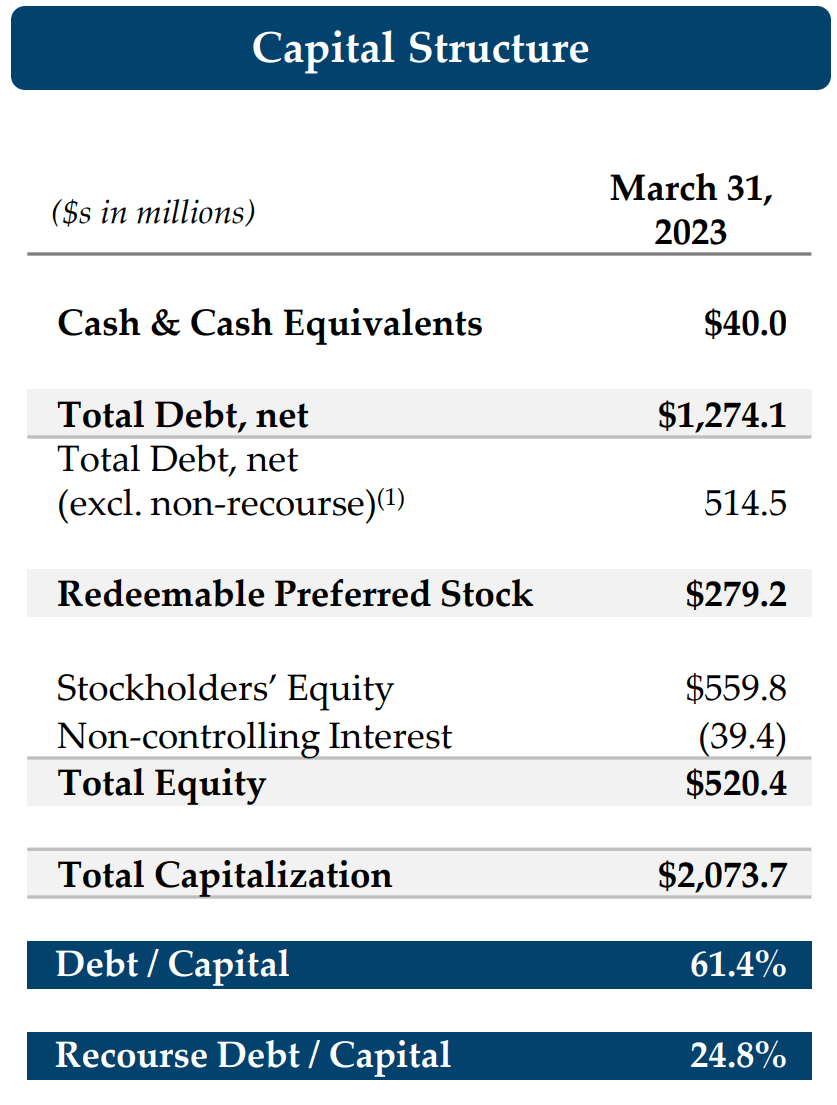

Let's look at the capital structure, as of March 31st, 2023.

{kind=link}

I think it is highly expected to see such a high amount of debt in the capital structure of a company that owns and operates infrastructure. A lot of capital is required to maintain and enhance these properties.

The real point is to understand whether or not these are cash-flow generating assets or not.

However, before we think this balance sheet is too levered, we have to consider that of the $1.3 billion of debt shown, $473 is issued at the holding company and another $700 million is issued at Jefferson on a non-recourse basis. As the management discloses:

we view the Jefferson debt more as an asset than a liability with extremely low interest cost, average maturity of 14 years, the flexibility to pay dividends from Jefferson with excess cash flow, and not callable in the event of a sale. That will become increasingly relevant as we anticipate Jefferson generating meaningful cash flow in 2023 and the years ahead. Now that the new Exxon contract has commenced and we continue to see momentum down in Beaumont.

Here, we learn something that will need to be monitored closely in the upcoming quarters: the new Exxon contract is rolling in and this should create a strong tailwind for Jefferson.

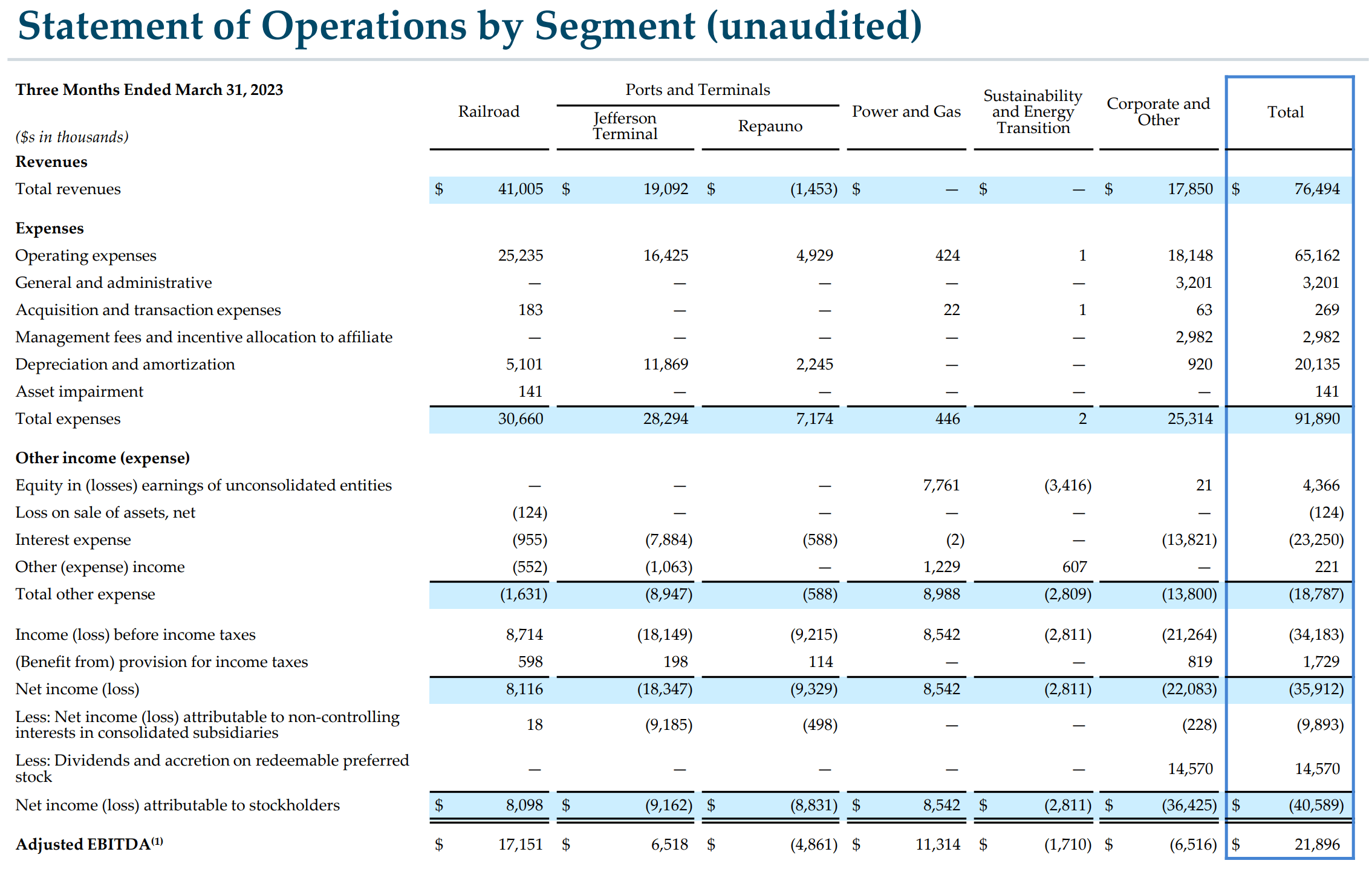

Now, let's look at the quarterly statement of operations by segment. Here we can have an overlook at how each segment is performing.

{kind=link}

From this table, we can see one clear thing: railroad is the cash cow of FTAI as of now. In fact, at the end of FY 2022 Transtar posted revenue of $150 million and adj. EBITDA of $64.3 million in fiscal 2022, with cashflow for the year at $66.7 million.

Now, in the most recent reported quarter, Transtar continues to be a cash cow, with adj. EBITDA coming in at $17.2 million, up 27% in just one quarter.

Since I came across FTAI Infrastructure due to my interest in railroads, I am paying more attention to Transtar than to the other assets, which, in any case, are quite important for the company.

However, we have once again the proof that railroads are quite profitable businesses, no matter the size of the tracks they are managing.

As we can see from the table above, it is currently Transtar that, operationally speaking, is running profitably. The other businesses, due to recent investments and other facts, still need to unleash their promising potential.

Future developments

For example, FTAI Infrastructure is seeing Jefferson beginning to handle higher volumes of refined products under its new Exxon contract. We should therefore see profitable quarters starting from Q2.

In addition, FTAI Infrastructure also acquired the nearby property in Beaumont called Jefferson South. This is a 600 acres property bought at $25 million, with two existing tenants and 200 acres still available for development. Thanks to the two tenants, the company knows there are no net operating expenses for the site so the acquisition is at almost no-impact, as of now. In any case, the company expects Jefferson South "to contribute incremental EBITDA as early as this year and to ultimately represent up to $50 million of opportunity for incremental EBITDA

At Repauno, the EBITDA loss was linked to the forced sale of natural gas liquids in inventory. The company was required to remove them prior to commencing its new multiyear tolling contract on April 1st, which is expected to generate an operating profit from now then on.

At Long Ridge, after an important outage in Q4, operations were back to normal and the company recorded $11.3 million of adj. EBITDA.

All of these opportunities make the company give a 2023 adj. EBITDA guidance of $200 million. Yet, given the high amount of D&A and interest expenses seen on the Jefferson Terminal ($12 million of D&A and $8 million of interest expense for the quarter alone). and the Corporate and Other ($14 million of interest expense) columns, there is still some room to go before the company achieves a net income.

Rating

Overall, I think the assets FTAI Infrastructure owns are quite interesting and promising. They may be exposed to come cyclicality and to the industrial cycle, but overall, there is always need for infrastructure in an economy.

The main risk I see at the moment is that the company has no experience as a stand-alone business. In addition, the picture of how most of its assets, in particular Ports and Terminals and Energy and Gas, are going to be managed to be turned into additional cash cows is still a bit unclear.

It is obvious how Transtar is a profitable and promising business that owns some unique properties well-insulated from competition. Had the company had only this business, it would be a clear buy to me. Yet, until at least Jefferson terminal becomes a profitable business, I rate the company as a hold.

It is an interesting pick to have on my watchlist, and I will monitor its progress along the way to assess if it is well-managed and worthy of being a quality company that enters into my portfolio.

For further details see:

FTAI Infrastructure: A Cash Cow And A Question Mark