TAN - FTC Solar: Profit Story Still Possible But Risk Management Required

2023-09-28 13:54:43 ET

Summary

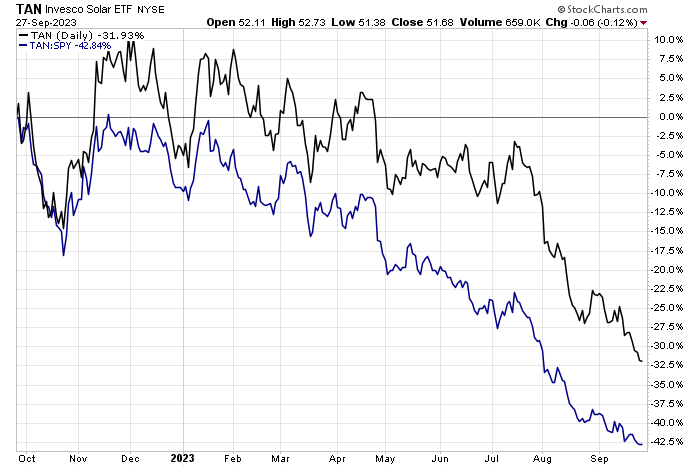

- Solar-related stocks have performed poorly in 2023, with the Invesco Solar ETF down over 30% from last year.

- FTC Solar is a small and speculative solar systems company with potential for growth if valuation and growth story play out.

- FTC Solar reported weak sales in August but mentioned an uptick in project activity and wins and a growing backlog.

- Investors must be prudent and mindful of the chart - I spot a key price point to watch.

Solar-related stocks have suffered so far in 2023. Shade has been cast on the group going back to the market lows of 2022. The Invesco Solar ETF (TAN) is down more than 30% from year-ago levels - underperforming the S&P 500 by about 43 percentage points. I have been bearish on the group throughout the year, but recently pointed out some potential green shoots . I may have been too early in my upgrade of the fund, though.

Today, I am initiating coverage on one small and highly speculative solar systems, software, and engineering services company. I have a hold rating on FTC Solar (FTCI). If the valuation and growth story plays out, it's a buy today, but from a risk perspective, there is a key price point that must be regained.

Solar Stocks Sinking in 2023

{kind=link}

According to Bank of America Global Research, FTC Solar, Inc. is a provider of solar tracking systems, with its core offering being a two panels in-portrait (2P) single-axis tracker solution as well as its newly launched software platform for performance and yield enhancement and value-added project management. With current and potential customers in the United States, Asia, the Middle East, North Africa, and Australia, FTCI targets ground-mounted utility-scale solar installations.

The Texas-based $139 million market cap Electrical Components and Equipment industry company within the Industrials sector has negative trailing 12-month GAAP earnings and does not pay a dividend. Ahead of earnings due out in early November, shares trade with an extremely high 119% implied volatility percentage, and short interest is likewise elevated at 11.1%.

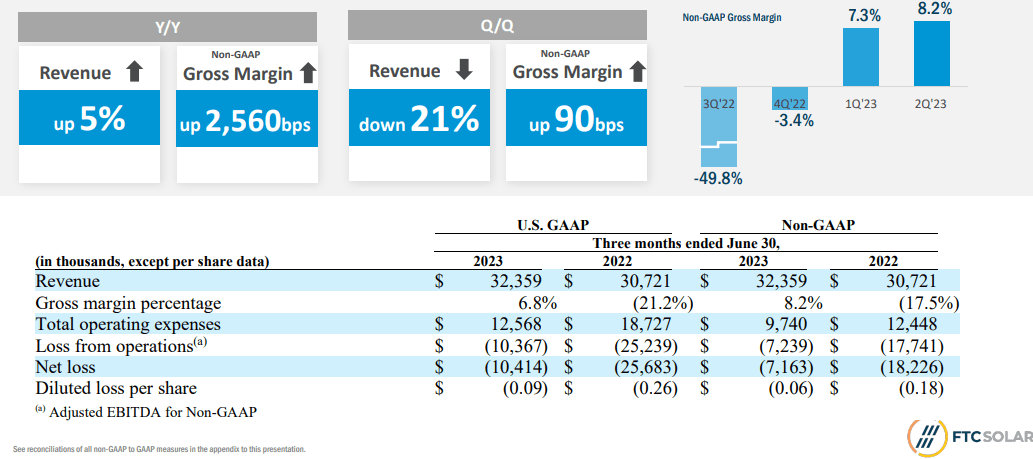

Back in August, FTCI reported a disappointing quarter . Sales came in very light at just $32.4 million, considerably below the consensus target of $47 million, though it was a 5.3% year-over-year increase. The firm cited project delays related to domestic content review for incentives for the top-line miss. Earnings verified in-line, and the Q3 2023 outlook now targets $24 to $34 million with Q3 2023 adjusted EBITDA guidance of $(10.3)-$(6.9) million, which was largely lackluster - BofA had expected a positive turn in adjusted EBITDA by Q3 this year, but that now seems unlikely.

On the earnings call , the management team mentioned that there was a significant uptick in project activity and wins in the past few weeks and that the company is positioned for growth in 2024. The project backlog now stands at $1.6 billion, up $259 million in recent weeks. The firm sees the backlog being converted in 2024 with an increase in total revenue next year.

Keep your eye on how insiders trade the stock - there was a $101,000 buy by the company's CFO earlier this month - more buying activity would be a bullish sign. But bearish news came about back on September 8 when a 10% owner sold $87,000 of shares.

Key risks include a slower positive turn in the domestic solar industry and margin weakness should further delays occur. Rising commodity prices are also a potential headwind.

Delayed projects impact revenue. Gross margin shows continued improvement.

{kind=link}

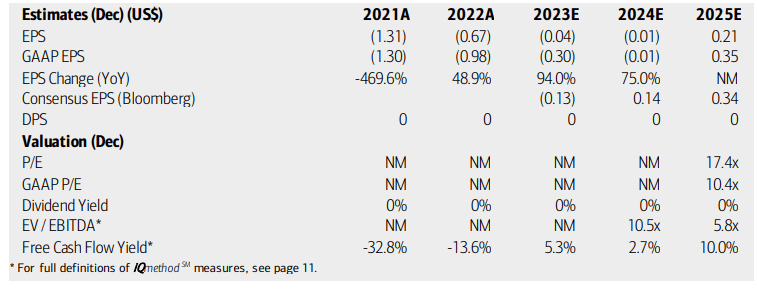

On valuation , analysts at BofA see earnings continuing in the red this year, but operating losses may cease in outer quarters. In fact, the current consensus, as indicated by Seeking Alpha, shows 2024 non-GAAP earnings inflecting positive next year with larger EPS gains in 2025. Of course, no dividends are expected to be paid on this stock, considering that the company has produced negative free cash flow per share of -$0.45 in the last 12 months. What is encouraging, however, is that FTCI's free cash flow yield could accelerate to the good side by 2025.

FTC Solar: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

On valuation, with no earnings per share, it is tougher to figure an intrinsic value. But let's assume $0.35 of 2025 operating EPS and provide a sufficient margin of safety. If we assign a below-market 15 multiple on those earnings, then shares would be near $5.25. Applying a 30% discount, we arrive at a stock price closer to $3.50. That would imply about a 9x EV/EBITDA ratio - a slight discount to some of its industry peers. The current enterprise value is $108 million.

FTCI: Earnings Anticipated In Later Quarters, Priced Low On Sales

Seeking Alpha

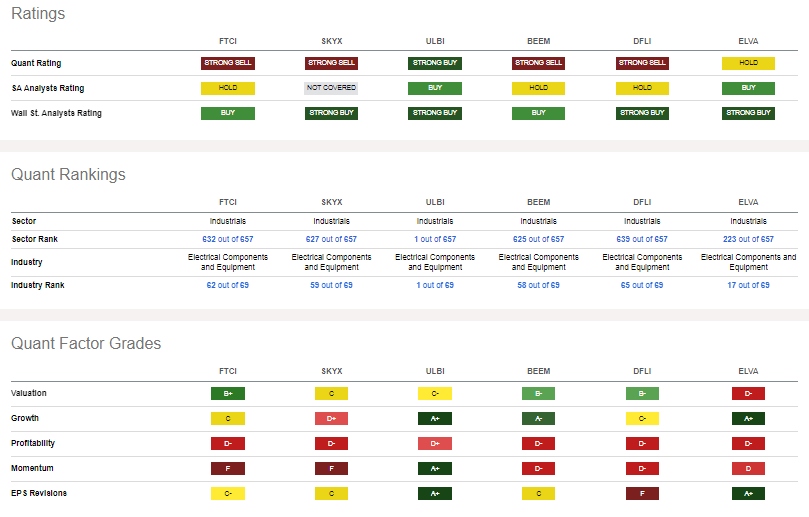

Compared to its peers , FTCI features a decent valuation, considering the low multiple of sales, but it's really all about how well the firm turns around the profitability picture . As it stands, growth prospects look okay, but we need to see better quarterly execution. In a troubled industry, share price momentum is about as bad as you can get, so being mindful of risk management is key. EPS revisions are also weak - and following the disappointing August report, I would expect more bearish headline risks to be in play with further analyst EPS downgrades .

Competitor Analysis

{kind=link}

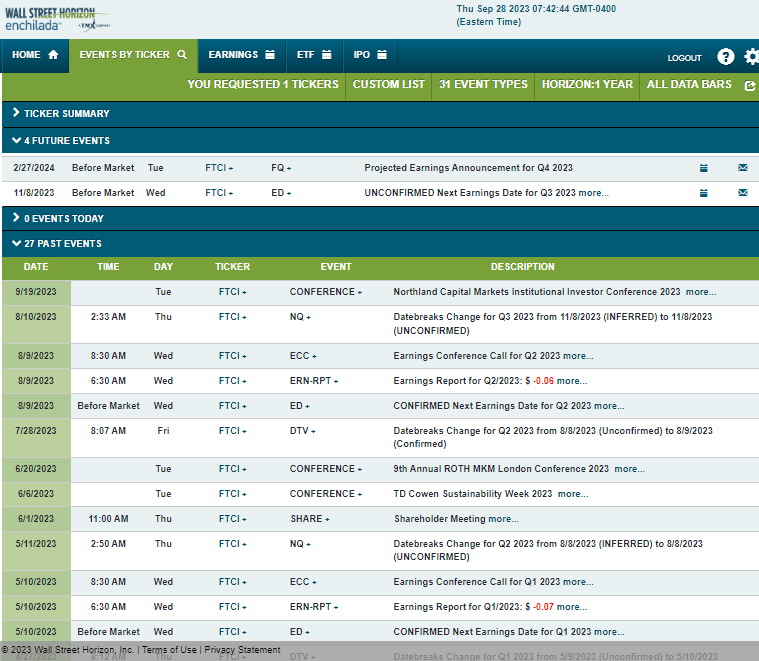

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q3 2023 earnings date of Wednesday, November 8 BMO. No other volatility catalysts are expected in the near term.

Corporate Event Risk Calendar

{kind=link}

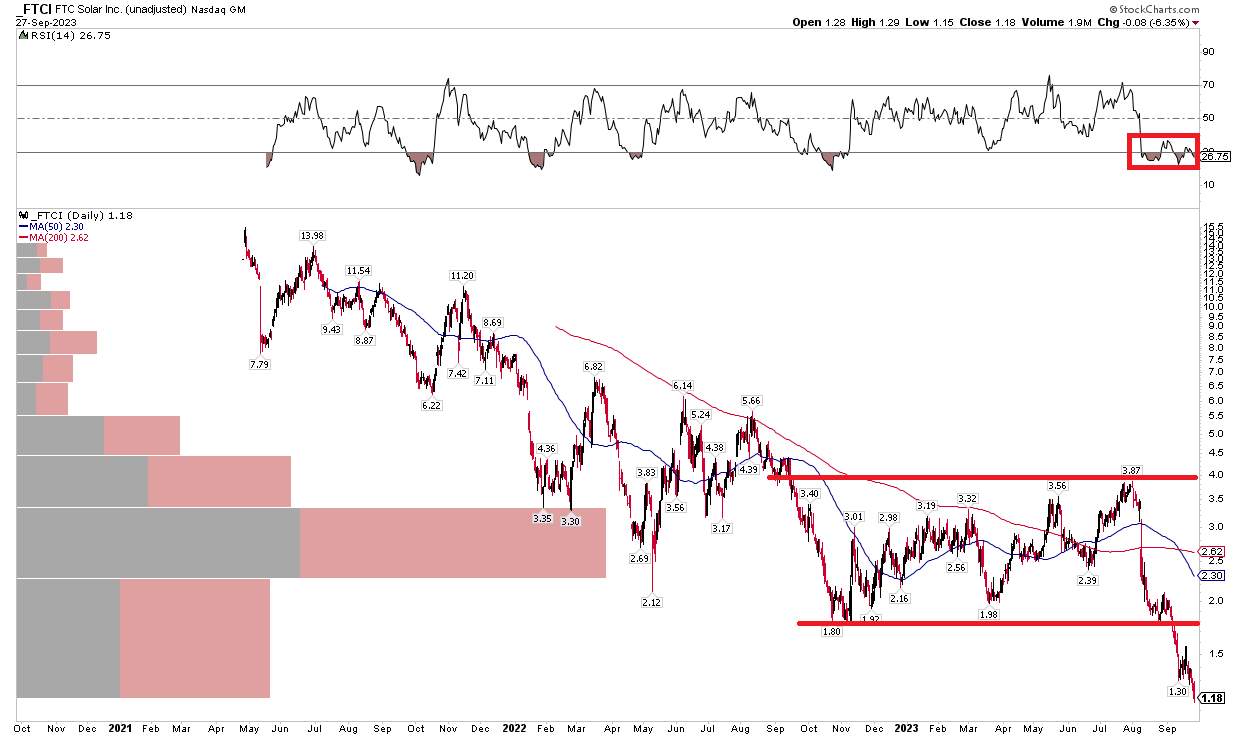

The Technical Take

Since going public more than three years ago, shares have been in a protracted downtrend. Notice in the chart below that FTCI was actually rangebound, though, from Q4 last year through this past summer. The dismal earnings report sent the bulls scurrying, and shares broke down through key support at the $1.80 mark.

The major point here is that the stock must reclaim $1.80 to stop the technical bleeding. Until it does, the stock is a 'no touch.' I see further resistance just shy of $4. Also take a look at the RSI momentum indicator at the top of the graph - it has been mired in a very bearish low range between 20 and 30. With a falling long-term 200-day moving average, the bears are clearly in control.

Overall, the chart is extremely bearish, offsetting my sanguine stance on a potential value turn in the business.

FTCI: Bearish Range Breakdown, $1.80 Key

{kind=link}

The Bottom Line

I have a hold rating on FTCI. Despite a lousy Q2, earnings could still inflect higher. If the growth story pans out, then shares should be multiples of where they trade today. Unfortunately, we must pay attention to risk, and shares, in my view, need to climb above $1.80 before a long position is taken.

For further details see:

FTC Solar: Profit Story Still Possible, But Risk Management Required