JNK - FTF: Avoid This High Yield CEF

2023-07-02 10:33:40 ET

Summary

- Franklin Limited Duration Income Trust (FTF), a fixed income closed end fund (CEF).

- The main risk for FTF is credit spreads, which have tightened this year. However, with banks tightening credit lending and an increase in bankruptcies, a surge in junk spreads is expected.

- FTF's portfolio is predominantly high yield, with over 80% of the collateral either below investment grade or not rated.

- FTF has a history of overdistribution which has led to a 50% loss in NAV over the past decade. Despite its stated 11% distribution yield, the actual cash-flow based yield is around 6.2%.

Thesis

Franklin Limited Duration Income Trust ( FTF ) is a fixed income closed end fund. The vehicle falls in the category of CEFs that consistently overdistribute, which accounts for the fund's -50% loss in NAV in the past decade. Despite its stated 11% distribution yield, the true cash-flow based yield here is somewhere around 6.2%, based on the most recent Section 19a, which shows a 50% ROC utilization.

This CEF is generally a high yield one, although it does have a multi-asset flavor, with a 15% bucket for AAA and A rated assets. When compared to high yield and multi-asset CEF peers, FTF looks extremely bad:

We are comparing the name with the Pimco Corporate & Income Opp Fund ( PTY ), the unleveraged SPDR Bloomberg High Yield ETF ( JNK ) and the BlackRock Multi-Sector Income Trust ( BIT ). Even JNK, a plain vanilla unleveraged name, has done better than FTF in the past year!

The main risk factor for FTF is constituted by credit spreads. Spreads have tightened this year, and we have not yet had a significant spike. With banks tightening credit lending, it is a matter of time until we see a surge in junk spreads. FTF, a fund which we covered once before, has managed to underperform in a market rally, and in our opinion will manage to 'outperform' on the downside during a risk-off scenario. This CEF is best to be avoided.

State of the High Yield market

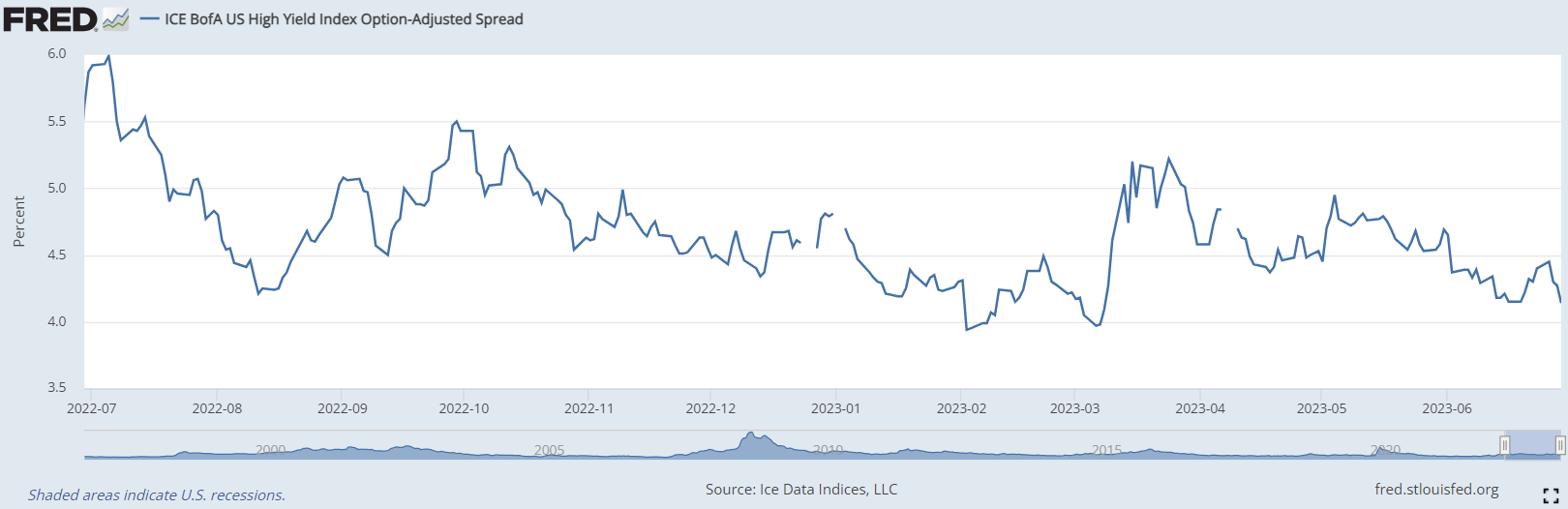

Spreads have firmed up so far this year, partly in correlation to the buoyant equity market performance:

{kind=link}

The above graph presents the ICE BofA US High Yield Index Option-Adjusted Spread. A high spread level means credit is tight, whereas a low spread level is associated with looser economic conditions and bull markets generally. We started the year with spread levels around 5%, which have now tightened towards the 4% levels. Please be mindful of the fact that the above figures are spreads, meaning they are the levels above benchmarks where credit trades. The all-in yields, or actual cash rate paid by borrowers, is calculated by adding the above spreads to the respective benchmark treasury. So for a 5-year-high yield bond, the all-in yield is now close to 9%.

Fundamentals however are now beginning to deteriorate with a number of bankruptcies starting to occur:

- Tattooed Chef is planning to file for bankruptcy

- Lordstown Motors Corp ( RIDE ) announced a strategic restructuring

- David's Bridal is also trying to restructure

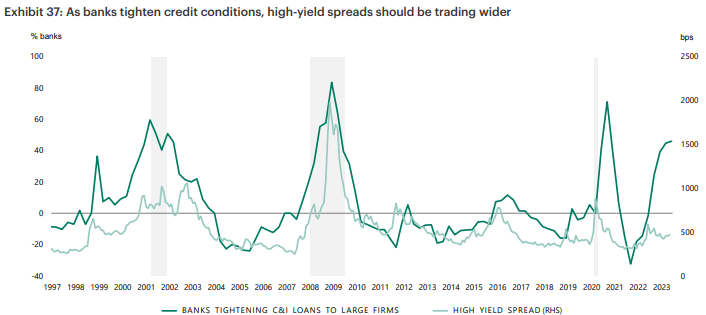

The availability of liquidity and easy credit made it possible for many businesses to stay afloat even in the face of deteriorating fundamentals. Following the regional banking crisis earlier in the year and deteriorating fundamentals in the CRE space, we are seeing banks tightening lending standards:

{kind=link}

Historically, as banks tighten credit conditions liquidity becomes scarce, which in turn 'helps' underperforming companies to restructure. Increased bankruptcies are accompanied by wider credit spreads. With credit conditions worsening, we are hard-pressed to see a scenario without a jump in high yield spreads this year. It is going to happen, the question is around timing.

Distributions

FTF is one of those CEFs that heavily overdistributes:

{kind=link}

The closed end fund structure allows portfolio managers to give shareholders their own principal bank under the guise of interest income. However, they are forced by regulators to disclose such actions, and they do under the 'Return of Capital' line in their Section 19a. We can see that as of the latest distribution, 51% of the cash received is actually return of capital. This basically translates into the fund having an actual, supported yield of only around 6%, versus what an investor notices in the dividend yield column for the name.

A policy of overdistribution is always bad for shareholders in the long term, because it results in NAV destruction and a continuous underperformance versus well run peers:

The graph above shows us how this CEF has lost almost 50% of its NAV in the past decade, mostly because of overdistribution.

Holdings

This CEF falls in the HY category for us, with over 80% of the collateral either below investment grade or not rated:

Ratings (Fund Fact Sheet)

Please note the bar-belled approach, where 15% of the fund is invested in AAA and A securities, while the HY portion is overweight single-B names.

High yield corporates and leveraged loans are the main holdings in this fund:

Holdings (Fund )

The first three components for the fund account for 70% of its holdings. Please note that marketplace loans are a new asset class, and it references peer to peer lending:

Marketplace lending uses online platforms to connect borrowers with investors willing to offer loans. It offers both new loans and refinancing. A worldwide industry has developed to launch and expand these platforms. In 2017 alone, according to Fintech Global , venture capital firms invested $8.9 billion in 233 deals related to lending platforms. That’s because a lot of money is flowing through these sites — enough to attract the attention of some of the world’s largest banks. No less a player than Goldman Sachs has established its own marketplace lending platform. Transparency Market Research reports that, in 2015, this channel accounted for $26.2 billion in loans worldwide, a little under half of which were in the U.S. If the study’s projected 48.2% annual growth rate holds up, worldwide platforms like these will have the $1 trillion mark in their sights by the end of 2024.

This asset class is generally very illiquid and is usually not rated.

Conclusion

FTF is a fixed income CEF. The fund focuses on high yield, although it has a multi-asset approach to its portfolio. This CEF has a history of overdistribution, and its actual cash flow yield is closer to 6.2%. The latest Section 19a shows a 50% ROC utilization, with the fund having lost -48% of its NAV in the past decade due to this feature. Credit spreads are the main risk factor for this name, and we expect a spike higher this year in spreads based on deteriorating fundamental conditions. A laggard, FTF has failed to outperform even the unleveraged high yield ETF ( JNK ) in the past year. There is not much to like about FTF, and we fear the CEF will 'lead' on the downside when the risk-off event does occur. Best to avoid this CEF given its outlook.

For further details see:

FTF: Avoid This High Yield CEF