FTF - FTF: Deep Discount Could Be Creating A Tactical Play

2023-10-17 18:31:11 ET

Summary

- Franklin Limited Duration Income Trust is a multi-sector bond fund with a shorter-duration portfolio, making it less interest rate sensitive.

- The FTF closed-end fund has historically underperformed its benchmark, but recent results have shown improvement.

- FTF's significant discount and diversified portfolio make it a potentially attractive investment as a tactical play.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Franklin Limited Duration Income Trust ( FTF ) is a multi-sector bond fund that primarily focuses on carrying a shorter-duration portfolio, as its name would imply. That generally means that it is less interest rate sensitive relative to other funds that focus on high-yield bonds or investment-grade bond portfolios.

That being said, with rates increasing, they still face headwinds, and credit risks are worth considering in a lower-quality portfolio. The closed-end fund's deep discount is one of the top-selling points, as it is near the deepest discount in its history aside from the GFC drops. However, the fund has historically put up lackluster results over the long term relative to its benchmark. Results going forward could be better if we see rates stabilize, which would ease pressures on all fixed-income and income-focused funds and investments.

The Basics

- 1-Year Z-score: -1.90

- Discount: -14.60%

- Distribution Yield: 12%

- Expense Ratio: 1.45%

- Leverage: 32.31%

- Managed Assets: $419.7 million

- Structure: Perpetual.

FTF's investment objective is "to provide high, current income, with a secondary objective of capital appreciation." They do this by investing "primarily in high yield corporate bonds, floating rate corporate loans and mortgage- and other asset-backed securities."

The fund is leveraged, and those leverage costs have been rising. This has seen the fund's total expense ratio go from 2.68% at the end of 2022 to 4% at the end of June 30, 2023, according to their semi-annual report . During this time, the fund also saw its leverage come down a touch, going from ~$117 million to ~$111. Since then, it looks like they've taken leverage back up to closer to $136 million.

{kind=link}

Despite the rising costs, thanks to the funds floating rate exposure, the income generation of the portfolio has been mostly flat as increased yields in the underlying portfolio offset the increased borrowing expenses. At the same time, that still means that the limited duration approach has helped hedge against rising costs but has not benefited the shareholders in this fund.

Poor Long-Term Results, But Discount Could Create A Tactical Situation Here

The FTF fund, over the long term, has generally underperformed its benchmark. A cause of this could be the leverage being used while going through a rising rate environment saw the declines come in sharper for the fund than the benchmark. Leverage cuts both ways, as it can increase potential returns but also create more volatility and increase downside risks. A higher expense ratio is also going to be a factor over time.

Where we see a reversal in the underperformance would be the more recent results over the last year. That could be leverage at work again; as recovery started to take place in some areas of the fixed-income market, FTF would have been able to participate in the upside.

FTF Annualized Performance Vs. Blended Benchmark (Franklin Templeton)

{kind=link}

However, it should be noted that this recovery was more for lower-rated credit rather than higher-quality credit, which is often more interest-rate sensitive. With Treasuries back on the rise once again, that's actually pushed investment-grade corporate bonds back down into negative territory for this year. This has set investment-grade corporates up for a third year of losses. Floating rate exposure has also performed well this year, which helped out a meaningful portion of FTF's portfolio as that's primarily where the fund gets its "limited duration."

Ycharts

An additional factor making FTF a potentially better investment going forward would be taking advantage of the fund's significant discount. The fund is trading well below its historical average discount and is close to the deepest discount levels that it generally has traded at historically - excluding the usual GFC and Covid spikes that we often see.

Ycharts

While the fund has been lackluster, so has most fixed-income. Closed-end funds aren't asset classes but are simply a wrapper for holding various assets. However, those underlying assets perform is going to be reflected in the fund's performance. With that being said, if rates ease up and the fund can see a narrower discount going forward, results for this fund could be more attractive in the short to medium term.

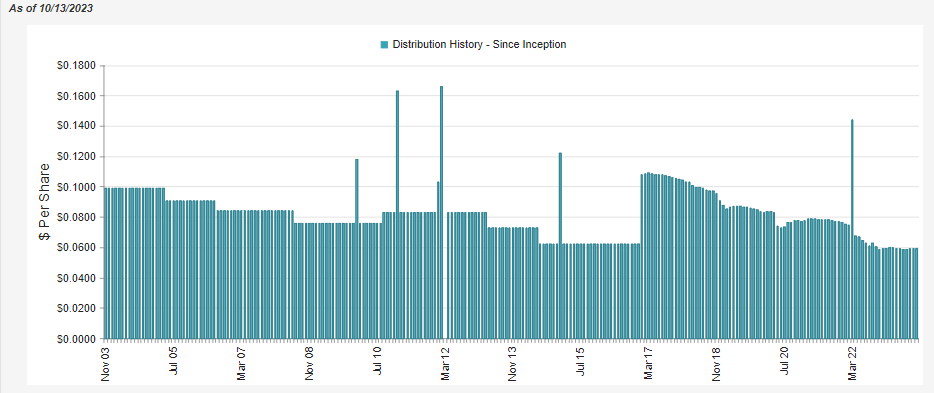

10% Managed Distribution Plan

The fund has a distribution that changes monthly based on a 10% payout annually of its NAV. As the fund saw a rapid decline in fixed income through most of the last few years, that saw its distribution head lower. The fact is also that a 10% yield would have been difficult to achieve during a zero-rate environment, meaning that erosion of the fund was nearly guaranteed.

That's changed in the latest environment, where higher rates mean higher yields and higher income being generated in the portfolio. Of course, that also has to include the fund's rising borrowing costs, which means that getting ahead is difficult for this fund.

From 2021 to 2022, we saw a meaningful increase in the NII per share, going from $0.52 to $0.62. In the last semi-annual report, we see the NII per share at $0.32, which puts it on pace to come in at $0.64 for the year if it continues at this rate. 2022 also saw a dilutive rights offering, which probably didn't help the fund's NII per share, either.

{kind=link}

All that being said, it is a much better environment for getting at least closer to a 10% rate that is achievable. Which is what we see reflected in the NII coverage going up to around 88% from the 80% at the end of last year.

With some recovery on the fund level, we've already seen the payout respond, as it has been more or less flattish through most of this year now - at least, the more rapid trend of reduced payouts appears to have leveled out relatively speaking.

{kind=link}

For tax purposes, the majority of the distribution was classified as ordinary income. This is something we would expect as a fixed-income focused fund, which will generally derive the vast majority of its income generation from interest-based income. There is some return of capital as well, as coverage of the distribution has come in short of that 10% target they are shooting for, which would be destructive ROC.

{kind=link}

FTF's Portfolio

The managers are fairly active in this fund, with turnover coming in at 46.64% in the last six-month period. That puts FTF on pace to be similar to last year's 95.50% turnover. In the prior four years, all turnover rates came in at over 100%, with 2018 touching nearly a 200% turnover rate.

Given that, we could expect to see some changes fairly regularly with this fund. As of their last report, they were holding a fairly evenly split portfolio in terms of corporate bonds and senior floating rate loans, which represent the majority of the portfolio. From there, they had other marketplace loans, MBS and ABS securities, with negligible equity exposure. The effective duration of this fund comes to 1.61 years.

FTF Sector Allocation (Franklin Templeton)

These were nearly identical weightings to what we saw at the end of 2022 ; despite such a high turnover rate, they still keep the overall asset structure of the fund fairly stable.

If you go back further, looking at the 2019 portfolio breakdown , there was similar exposure listed as well. Corporate bonds were the largest weighting, followed by senior loans. However, one thing that they've seen an increase in weighting was marketplace loans.

Marketplace loans are broken down and listed in the semi and annual reports if one wants to look at all of them. This is what really bumps up the fund's total holdings to 15,885. There are thousands of these loans within this 17.2% allocation for the fund. They range anywhere from around $100 loans up to ~$30k loans. These loans are spread out to mature anywhere from 2024 to 2029.

Rates, if they aren't zero coupons, come in anywhere from 7% to 30%, but some are over 30%. While they are offering high yields, that is to account for those that won't ever see repayment. This would only become increasingly more likely if the economy turned lower, as unemployment would likely increase and make it more difficult for these loans to get paid off. Marketplace loans are also considered level 3 securities.

Of course, a weak-performing economy would also mean more defaults in the corporate bond and senior loan space as well. This has historically been true of lower-rated credit qualities, which is where FTF is mostly positioned. At the end of June 2023, they listed that 74.1% of the fund's portfolio was held in either below-investment grade positions or unrated securities.

That does still leave some of the portfolio, a fairly meaningful amount, in higher quality credit. That allocation includes mostly the agency MBS exposure. The agency MBS shows up in their top ten holdings as well, which has a fairly heavy weighting, but these are pooled mortgages with hundreds or thousands wrapped up in these securities.

So, in general, they hold very little exposure to any specific individual or corporation. Instead, it's spread across tens of thousands of different loans. When also factoring in the marketplace loans, we could be seeing over 100k different "holdings." The marketplace loans are all pooled into the Square Capital, Freedom Financial and Prosper holdings. We also see those in the top ten.

{kind=link}

Conclusion

Franklin Limited Duration Income Trust is a fairly interesting fund, but it has had a lackluster long-term record. However, some of those fortunes seem to be reversing, with the fund beating its benchmark in the shorter term. The fund is certainly diversified, with different exposures to thousands of loans and bonds. The fund's discount is also historically attractive, which could make it a worthwhile tactical play in the shorter term.

For further details see:

FTF: Deep Discount Could Be Creating A Tactical Play