FTHY - FTHY: Attractive Discount For A High-Yield Fund

Summary

- FTHY is trading at an attractive discount and looks like a candidate, with the Fed slowing the pace of interest rate increases.

- These interest rate increases might even be near an end, with the latest 25 basis points expected to be one of the last.

- This fund's distribution yield is also quite enticing; however, distribution coverage has fallen due to lower income generation and higher interest expenses.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on February 2nd, 2023.

First Trust High Yield Opportunities 2027 Term Fund ( FTHY ) launched mid-year 2020. The fund enjoyed a period of rebounding equity and bond markets, fueled by 0% interest rate increases. That came to a swift end in 2022 when the Fed aggressively raised interest rates. Each raise through 2022 seemed only to be met with an outlook for an even more aggressive Fed.

However, in 2023 we are in a completely different environment. Indeed, interest rates are now much higher, but the pace of increases is slowing. In fact, with the latest 25 basis points that the Fed just announced, some market participants are saying that could be it.

On the other hand, the Fed has kept up with the idea that they have more to do. Taking the Fed's cue, I'd also have to suggest that we could see more interest rate increases, but there is no denying that we are ultimately near the end.

This is incredibly important not only for leveraged closed-end funds such as FTHY but, in particular, fixed-income focused funds such as FTHY. It impacts the fund's underlying portfolio as rates rise to bring yields up with it, and its portfolio takes a hit.

Simultaneously, while rates are rising, the leverage costs of their borrowings also rise. With the stabilization of interest rates, the outlook for FTHY is much better as the damage is largely in now. If we even have potential rate cuts later in 2023 or early 2024, that would benefit the fund even more.

We've already seen what a little bit of a rally in the broader market and a decrease in the 10-Year Treasury yield can do for shares of FTHY. Since our last update, the fund has performed quite well. This is representative of share price performance only, not the underlying portfolio. So this reflects the discount narrowing from around 13.5% to ~9% now. The S&P 500 is not an appropriate benchmark, but it can give context to what the overall 'market' is doing.

FTHY Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 0.37

- Discount: 8.97%

- Distribution Yield: 10.42%

- Expense Ratio: 1.95%

- Leverage: 15.34%

- Managed Assets: $700 million

- Structure: Term ( anticipated liquidation around August 1st, 2027)

FTHY's investment objective is "to provide current income." They intend to do this by "investing at least 80% of its Managed Assets in high yield debt securities of any maturity that are rated below investment grade at the time of purchase or unrated securities determined by the Advisor to be of comparable quality. High-yield debt securities include the U.S. and non-U.S. corporate debt obligations and senior, secured floating-rate loans ("Senior Loans")."

This fund carries one of the highest expense ratios, and it isn't entirely clear why that is the case as they aren't investing in anything overly complicated, relatively speaking. Generally, if a fund has global exposure or private level 3 investments, expense ratios can be elevated. Additionally, expense ratios can be high if a fund is incredibly small. With around nearly $700 million in managed assets, it's not that small for a CEF.

In this case, the advisory fee is at 1.35% even though the portfolio is fairly straightforward. This is above the standard 1% advisory fee we see in many other funds, so this explains to some extent why it is elevated. So I'd consider the high expense ratio a negative for the fund.

Additionally, when factoring in leverage costs, we see that the total expense ratio comes to 3.09%. With leverage costs rising, that is a jump from the prior year. The fund hasn't directly hedged against the higher rates. However, due to the portfolio carrying a meaningful weighting to floating rate securities, it could be considered hedged in that way.

The borrowings are based on SOFR plus 0.90%. The weighted average interest rate for these borrowings came to 3.34% for the six months ending November 30th, 2022. At the end of the period, it came in at 5.01% from 1.84% previously. This is a testament to how drastically interest rate expenses have risen. Since then, it's only gone higher.

Previously they reduced their leverage, and with this latest look, they've once again bulled down their borrowings to $107 million. At one point earlier in 2022, the fund was carrying borrowings of $306 million.

FTHY Leverage Information (First Trust)

Performance - Attractive Discount

The fund's discount has narrowed quite a bit since our previous update. However, the fund still remains attractively discounted even at the current level. It isn't that old of a fund, so historically, the range might be less meaningful. That being said, it is well below the average still, for what it is worth.

Ycharts

Comparing FTHY to the taxable fixed-income space, the fund is heavily discounted on that basis. The last report from RiverNorth showed that the category's average discount comes to -3.55%.

Some of the discounts seem warranted due to significant underperformance. The fund is a hybrid of high-yield and senior loans. Mostly high yield as they've kept senior loans to a fairly limited allocation. This seems like one of the opposite things you'd have wanted to do through 2022, but in 2023 it could be better positioning.

Underperformance relative to the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) and the Invesco Senior Loan ETF ( BKLN ) can be due to several factors. The primary factors would include poor portfolio positioning and the utilization of leverage.

They've deleveraged throughout the year, but it wasn't early enough. Now that they are deleveraged, we are getting a rebound which is working against the fund's performance as they have fewer assets to rebound with.

Another factor, of course, is going to be the fund's higher expense ratio taking a bite out of returns.

HYG and BKLN carry no leverage, don't have to deal with wildly varying discounts/premiums, and have much lower expense ratios. They help represent a base of context for the results we see or could see with FTHY.

Ycharts

Despite that deleveraging, they are still, of course, leveraged. That appears to have played out some in the last month, as we've seen different results. FTHY has taken the lead above these two non-leveraged ETFs. The results on a total NAV return basis were virtually identical to HYG, as it seems the senior loan exposure has no effect on FTHY's results.

On the other hand, the total share price return has substantially exceeded the results from these non-leveraged ETFs due to discount contraction. When you buy a CEF, it's incredibly important to your results - buying at large discounts helps make it easier that the end result will be a positive one.

Ycharts

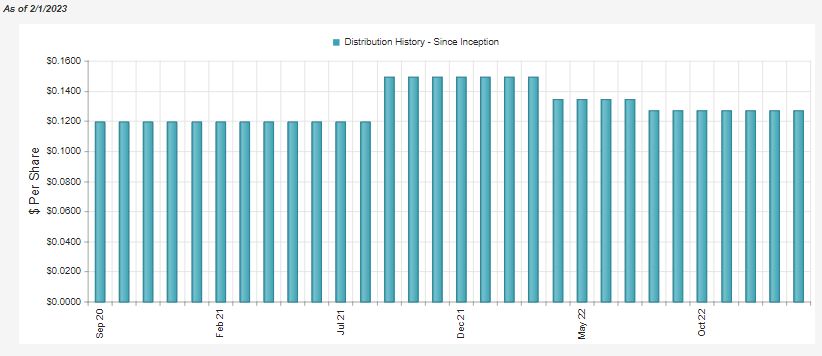

Distribution - Lack of Coverage

When the fund launched, they were paying a relatively attractive payout to investors. It was mostly covered in those early reports. However, they then wanted to get cute and bump up the distribution significantly despite not having the coverage.

Since then, as I've mentioned on at least a couple of occasions, they'd be at risk for a cut. That has happened with two cuts now after raising. The raise initially seemed bizarre, and I'm not sure exactly what they were going for. Generally, CEF investors tend to gravitate towards higher distribution yields, but if funds plan to hold them there for a period of time. CEF investors tend to shun funds that make frequent adjustments.

{kind=link}

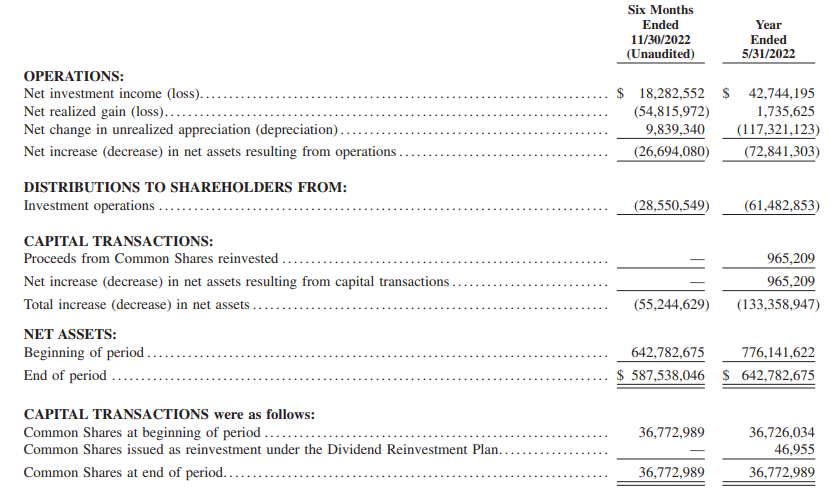

If they were heavier in senior loan investments, as I expected they would be in 2022, it could have been a different story. However, due to over distributions and deleveraging, the coverage is now at a new low. Net investment income coverage comes in at 64%; we'd generally want to see this at over 100% for a fixed-income fund.

When reflecting the distribution cut, in the future, the fund should pay out $27,998,954 based on the shares outstanding in the last report. That would only bring up NII coverage to 65.3%.

{kind=link}

The reduction in leverage meant their overall total investment income dropped from $30.185 million to $27.534 million . Due to leverage costs rising, "interest and fees on loan" increased to $3.425 million from $1.345 million in the year-ago six-month period.

Overall, further distribution cuts in the future wouldn't be surprising in the least.

For tax purposes, the fund listed both of the last years as being almost entirely ordinary income. For 2022, they are showing that a tiny $0.032522 of the $1.5978 distributed in 2022 was characterized as short-term capital gains. The end result is still being taxed at ordinary income rates, so it doesn't make much of a difference in that classification. A small portion was listed as long-term capital gains at $0.029835. This is fairly normal for a fixed-income fund. Therefore, it could be best to hold it in a tax-sheltered account.

FTHY's Portfolio

The largest allocation of the fund is positioned in high-yield bonds. A significantly smaller allocation follows this dedicated to senior loans. Then we have an immaterial allocation to "other."

FTHY Asset Class Allocation (First Trust)

This minimal exposure to senior loans dropped from the ~27.5% allocation the fund had near the beginning of 2022. So throughout 2022, as interest rates were rapidly rising, they reduced their senior loan exposure. It would seem that one reason to sell off senior loan investments would be to reduce borrowings from securities that were holding up fairly well. Bonds were hit harder through 2022 as they are generally more sensitive to interest rate changes.

Despite this shift from senior loan investments, the average effective duration has still dropped. At this time, it comes in at 3.70 years from the previous 4.23 years. That was a positive development for the fund.

Additionally, as the price of the underlying securities dropped, that has opened up additional discounts that can be realized at some point. That would also be in addition to the discount the fund is showing from its underlying NAV too. If the fund holds some of these securities until maturity, it should receive face value back. That would take the average price of $89.18 to realize $100. Of course, as an actively managed fund, there is no way of knowing exactly what they would hold to maturity or not.

FTHY Portfolio Stats (First Trust)

Previously they listed an average price of their underlying securities at $94.27 earlier in 2022. So that helps provide an idea of why the underlying portfolio has declined.

Overall, the portfolio in high-yield bonds and senior loans is riskier. Naturally, that means the overwhelming majority of their portfolio is listed as below investment grade. In particular, they are carrying over 20% in the riskiest of these categories, in the triple C category.

Depending on the depth of the potential and expected recession this year, this could be a significant headwind for the fund as they'd likely experience defaults at a fairly high rate. That's why we see such a discount on the price of their underlying holdings, as it reflects the risk.

FTHY Credit Quality (First Trust)

On the other hand, the fund is quite fairly diversified across several different industries can help minimize this risk. When one industry is struggling, it doesn't necessarily mean all industries are struggling just the same.

However, it might not be as diversified as some other funds we cover when looking closer at individual exposure. They listed the number of holdings at 197 (excluding cash.) This is low for a high-yield CEF but still gives quite a bit of diversification. This more minimal number of holdings shows in the fund's top ten issuer weightings.

FTHY Top Ten Issuers (First Trust)

These are some of the highest weightings I've seen for companies relative to their junk-holding CEF peers. I think this reflects why the fund can significantly underperform, as we saw above. It means they need to have more success to pull off positive results.

For some context, HYG carries 1204 positions. BlackRock's ( BLK ) CEF version of HYG, BlackRock Corporate High Yield Fund ( HYT ), carries 1339 holdings.

Conclusion

FTHY is at an attractive discount, combined with the fund's underlying portfolio discount on the holdings, and it looks like a solid deal. That helps to balance this fund's negatives that come in the form of a lack of distribution coverage and riskier positions in a more narrowly focused portfolio. The fund deleveraged through the last year, so that would have taken down some risk for investors coming in today.

Admittedly, they didn't position the fund how I would have expected through most of 2022. I thought they'd ramp up their senior loan exposure due to rising interest rates. So I believe that hurt the fund last year. However, looking forward now is more important than what the fund did in 2022.

The fund's discount has narrowed from our prior update as the market has rebounded. Additionally, the Fed is near the end of its interest rate hikes. That stabilization should be a good thing for FTHY going forward. We've already seen quite an impressive move higher due to yields coming down on risk-free U.S. Treasuries despite the Fed still raising.

For further details see:

FTHY: Attractive Discount For A High-Yield Fund