FTHY - FTHY: Discounted High Yield Exposure

2023-08-18 15:42:10 ET

Summary

- First Trust High Yield Opportunities 2027 Term Fund offers exposure to high-yield bonds and floating-rate senior loan investments.

- The fund's discount has narrowed but remains at an attractive double-digit level.

- The fund's distribution coverage has decreased, but its large discount provides appeal due to its term structure.

Written by Nick Ackerman, co-produced by Stanford Chemist.

First Trust High Yield Opportunities 2027 Term Fund ( FTHY ) offers investors exposure to both high-yield bonds and floating-rate senior loan investments, with some floating rate exposure in the portfolio that has benefited from the Fed raising rates. However, they have chosen to favor more exposure to high-yield bonds since their launch. The fund is anticipated to liquidate in 2027, and that could provide some alpha as investors realize the discount as we draw nearer to that liquidation date. At this point, we still have a few years before that becomes more of a catalyst for this fund.

Since our last update , the fund's discount has narrowed some, but it still remains at an attractive double-digit level. The fund has also put up positive total returns thanks to the distribution, while the share price has stayed nearly flat. (At the time of writing this, it is one penny higher than when we last covered it).

FTHY Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 0.19.

- Discount: 10.77%.

- Distribution Yield: 11.34%.

- Expense Ratio: 1.86%.

- Leverage: 17.22%.

- Managed Assets: $685.153 million.

- Structure: Term ( anticipated liquidation around August 1st, 2027).

FTHY's investment objective is "to provide current income." They intend to do this by "investing at least 80% of its Managed Assets in high yield debt securities of any maturity that are rated below investment grade at the time of purchase or unrated securities determined by the Advisor to be of comparable quality. High-yield debt securities include the U.S. and non-U.S. corporate debt obligations and senior, secured floating-rate loans ("Senior Loans")."

As usual, with every update on FTHY, I like to highlight the fact that the fund's expense ratio is on the higher end. That being said, it did come down from the 2.02% it was last fiscal year, so any further reduction there could be a positive.

That being said, when including the fund's leverage expenses, we see the total expense ratio come to 3.05%. That's higher than the 2.41% we saw last year. Borrowing costs have been rising for closed-end funds, in general, due to the Fed raising interest rates. Most CEF borrowings are based on LIBOR, SOFR or OBFR plus a spread. LIBOR has been discontinued, so SOFR and OBFR have been more common. For FTHY, it is based on SOFR plus 0.80% currently, but prior to July 22, 2022 was based on 1-month LIBOR plus 0.80%.

At the end of their last fiscal year, the period ending May 31, 2023, the average interest rate for borrowings came to 6.09%. The fund doesn't hedge this directly through interest rate swaps or going short future contracts, but that's where a portion of the underlying portfolio being exposed to the floating rate can help mitigate some of these higher costs.

The fund has also dropped its total borrowings considerably over the last year, and it remains modestly leveraged. Fiscal 2021 saw $309 million in borrowings, which went down to $278 million by fiscal 2022 and then fiscal 2023 saw borrowings drop to $123 million. Today, the last update shows borrowings at $118 million, which is an increase of $1 million from our prior update.

FTHY Leverage Info (First Trust)

Performance - Attractive Discount

Since the fund's inception, performance hasn't been too pleasant. Of course, not much in the fixed-income bond world has provided strong results over the last several years when factoring in 2022's terrible year for fixed-income. That being said, one area that has been a bit more promising is the senior loan space. That can be represented by Invesco Senior Loan ETF ( BKLN ).

YCharts

Despite rising rates, FTHY has still chosen to favor high-yield bonds. For a period of time, that was the right choice as well. The fund, on a total NAV return basis, held a close correlation with iShares iBoxx High Yield Corporate Bonds ( HYG ) for quite a while too. However, both FTHY and HYG were surpassed easily for performance during this period by BKLN.

Both HYG and BKLN are non-leveraged ETFs with a lower expense ratio, but they can still give some color to FTHY's performance. It started out of the gate with some promise but then faltered as they shifted their portfolio heavier into high-yield bonds, and then deleveraging in the last year has likely meant further lagging results due to not participating in this recovery once things started to bounce higher in October.

That being said, future results could prove more promising. One of the catalysts for more promising results could come from the fact that they do have significant leverage capacity to add more to their portfolio. Yields have been rising once again, and that has meant lower bond prices. Additionally, when the fund is anticipated to liquidate, that would result in another ~10% return between now and the liquidation date.

As we get closer and closer to 2027 liquidation, the alpha potential becomes more and more if the discount remains this wide.

YCharts

As is the case with the majority of term funds, there is a way that the fund's termination date can be extended . That would come through only with permission from the Board, while shareholders aren't given a say.

...if the Board of Trustees determines it is in the best interest of the shareholders to do so, upon provision of at least 60 days prior written notice to shareholders, the Fund's term may be extended, and the Termination Date deferred, for one period of up to six months by a vote of the Board of Trustees. In determining whether to extend the Fund's term beyond the Termination Date, the Board of Trustees may consider the inability to sell the Fund's assets in a time frame consistent with termination due to lack of market liquidity or other extenuating circumstances. Additionally, the Board of Trustees may determine that market conditions are such that it is reasonable to believe that, with an extension, the Fund's remaining assets will appreciate and generate income in an amount that, in the aggregate, is meaningful relative to the cost and expense of continuing the operation of the Fund.

One thing I've also noted on this fund previously is that there are no terms for going perpetual. That's generally another standard wording in a prospectus when the fund is being offered to provide an eligible tender offer that can take place before going perpetual potentially.

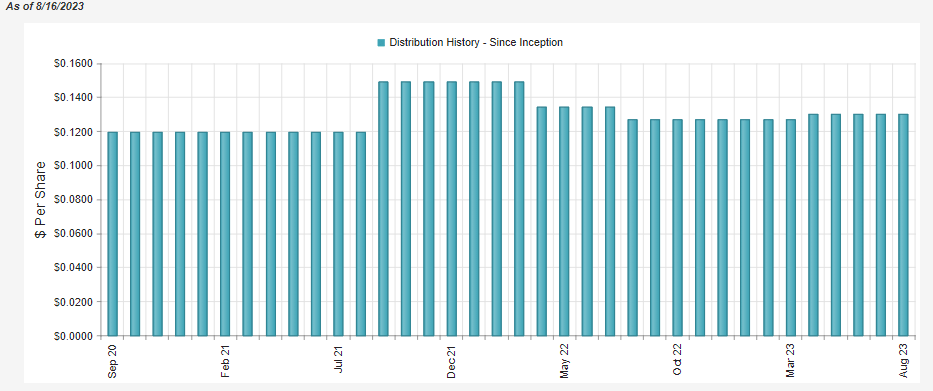

Distribution - Coverage Sinks

Another factor that deleveraging has impacted while borrowing costs have risen would be the fund's distribution coverage. They raised earlier this year, but that only meant distribution coverage has fallen further.

{kind=link}

I have to admit, I'm not sure what the team is going for with their distribution policy here. If it's to annoy investors by making many changes in a short period of time, they are probably succeeding.

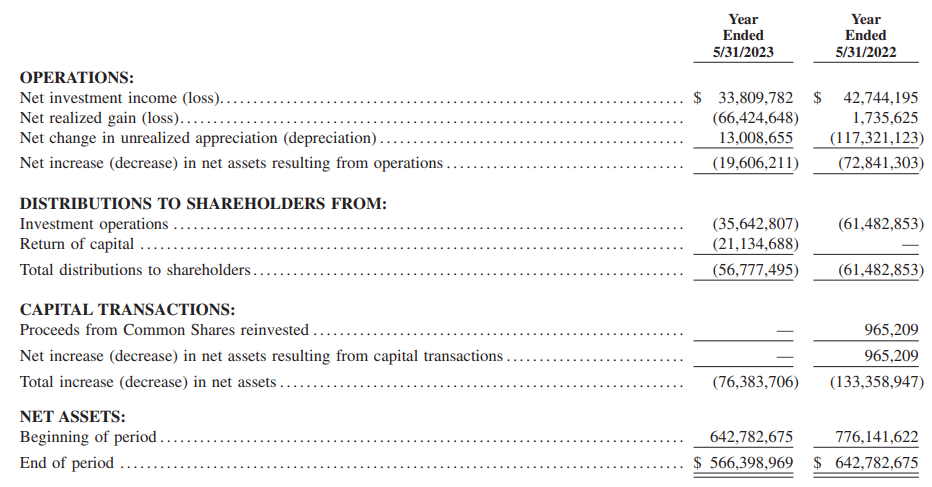

With that being said when looking at the last annual report for net investment income coverage, we see it came in at around 60%.

{kind=link}

Based on the new rate, the annual payouts should come in at around $57.366 million, which doesn't significantly change what they paid out in this annual report. If we expect the current NII to continue going forward, we'd see a similar distribution coverage of 59%.

On a per-share basis, NII came in at $0.92. This is in line with what we expected when we suggested we'd see NII slip further from the $0.50 in the last semi-annual report. With borrowing costs still climbing, we would anticipate that in the next report, we will see NII take another hit. This is why the increased distribution was a bit surprising that we saw earlier this year.

However, if they added a meaningful amount of leverage back into their portfolio, it could see NII rise - assuming they are buying securities with yields greater than their cost of borrowings and expense ratio. The $1 million they added in leverage between now and our last update is unlikely to be meaningful enough to move the needle.

Due to the sizeable shortfall in distribution coverage, it isn't too surprising to see the fund's distribution tax classification contain return of capital. As they certainly haven't put up gains in the underlying portfolio, this would be considered destructive ROC.

{kind=link}

FTHY's Portfolio

I have covered FTHY quite regularly since the fund launched. And it initially carried a larger portion of its portfolio to senior loans rather than high-yield bonds. However, they have slowly reduced their floating rate exposure and have instead favored bonds. Perhaps this was due to the deleveraging where they were selling off the senior loans as their values held up better relative to the bonds. That being said, the weightings are similar to where they were earlier this year at 80.49% in high yield and 19.48% in senior loans.

FTHY Asset Exposure (First Trust)

The fund's underlying portfolio still also shows a similar weighted average price of $89.59. This compares to the $89.20 on May 15, 2023.

FTHY Portfolio Characteristics (First Trust)

Despite the underlying portfolio moving higher by a touch, the fund's NAV has declined in this period due to the lack of distribution coverage. Meaning they paid out too much, and that has been what reduced the NAV. Since the share price during this time was essentially flat, the reduction in the NAV meant that the NAV per share was moving closer to the share price, and that's what resulted in the fund's discount narrowing slightly. While that's not often what we want to see in CEFs, it is admittedly a fairly short period to look back at.

Given the other factors we've looked at so far, it has indicated that there hasn't been a lot of turnover in the fund since our prior update. This is further reflected by the fact that the fund's credit rating allocations have also remained fairly similar too. The fund continues to carry a fairly material exposure to CCC rated debt at nearly 19% of the portfolio, though that was down slightly from the 20.86% previously. This is an area that's the most speculative, with a high probability of defaults.

FTHY Portfolio Credit Rating (First Trust)

They also tend to favor single B rather than double B, which we see in other junk CEFs. For some context on this, we can go back to HYG. That fund carries around 10.63% of its portfolio in CCC debt or lower. However, its largest weighting is to BB at 51.16% of the portfolio compared to the 36.96% for B rated debt. FTHY has taken a weighting of 26.97% in BB, while B accounts for the largest weighting at 47.41%. This generally means that FTHY is a more speculative and risky portfolio, relatively speaking.

In looking at the top ten, we similarly see that there haven't been significant changes. Again, reflecting that the portfolio has stayed fairly stagnant since our prior update. So not a lot to update in this section.

FTHY Top Ten Holdings (First Trust)

Conclusion

FTHY is a speculative and risky portfolio. The fund has seen its distribution coverage sink while its borrowing costs have risen, but primarily from the result of reducing leverage significantly in the last year. That being said, the fund's large discount provides it some appeal due to its term structure, where the discount should be realized in the future.

For further details see:

FTHY: Discounted High Yield Exposure