FUBO - fuboTV Continues To Tip The Subscriber Business In Its Favor Ads Helping

2023-11-28 09:00:00 ET

Summary

- fuboTV has shown consistently strong revenue growth, with Q3 revenue growing at 42.8% and subscriber adds exceeding expectations.

- The company has been able to reduce subscriber-related expenses through contract renewals, which has been a major hurdle to profitability.

- fuboTV's advertising business has outperformed the industry, with ad revenue growing at its highest level since Q1 2022.

- With the improved business fundamentals, the stock valuation is still pricing in bankruptcy, leading to a 76% upside potential.

The struggle fuboTV ( FUBO ) has encountered and the legitimate point bears have had over the last two years (or more) has been the ability to leverage the content business it relies on. This leverage has been the crux of whether the overall business can perform profitably and not run out of cash. But, the light at the end of the tunnel began to appear earlier this year as content costs grew slower than revenue. This leverage trend has continued throughout the year. All the while, its high-margin advertising business has stepped up to record levels even in the face of a weaker macro ad environment. Based on my projections and management expectations for these margin trends to continue, the company will have well over $100M in cash when it breaks even in 2025.

There are a few key areas where FUBO's trajectory to profitability is clearly shown, and what I'll focus on:

- Strong revenue growth

- Subscriber-related expense trend

- Advertising revenue strength

- Cash burn and margins

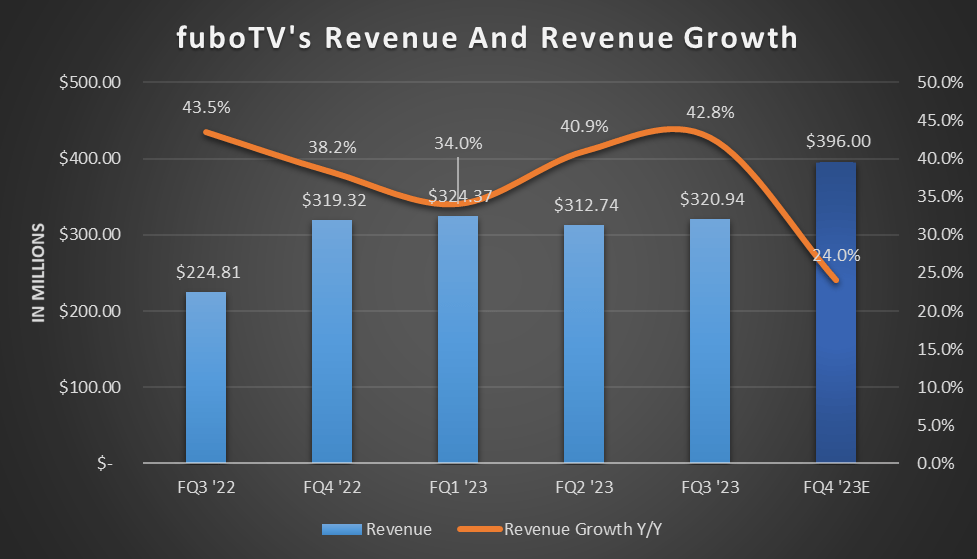

Revenue Growth

If there's one thing bears expected to see weakness in on this journey to 2025, it was revenue growth. And quite frankly, I didn't expect the consistent strength in revenue growth the company has seen over the last five quarters. Yet, the subscriber business is strong, and subscriber adds have been above and beyond expectations.

Specifically, the recent Q3 report's revenue growth rate of 42.8% was almost equal to the same period in 2022 at 43.5%. This is true consistency in the face of what many see as a weak market for consumers - recession fears and all that. But as I've said repeatedly to my subscribers and you, fuboTV is a recession-helped company as many cut the expensive cable cord and move to something they can share with multiple family members while continuing to watch their favorite channels and sports for less each month.

Chart mine, data from FUBO's Shareholder Letters

{kind=link}

Of course, guidance for FQ4 shows a slowdown in growth to one of its lowest levels since being public. However, this is at the midpoint of guidance. The just reported quarter was guided for $282.7M. Outperformance led to it being nearly $40M above that, for a beat of 13.5%. If the momentum were to continue, this kind of beat in Q4 would mean $447.5M, or revenue growth of 40.1%. A more conservative approach of half the beat of Q3 would mean revenue growth of 32.4% - very much in line with the last several quarters.

The company has been conservative this year in its guidance, and I expect nothing less for its football, hockey, and basketball-heavy sports season. With this in mind, I'm pegging revenue growth to come in close to 32% when all is said and done.

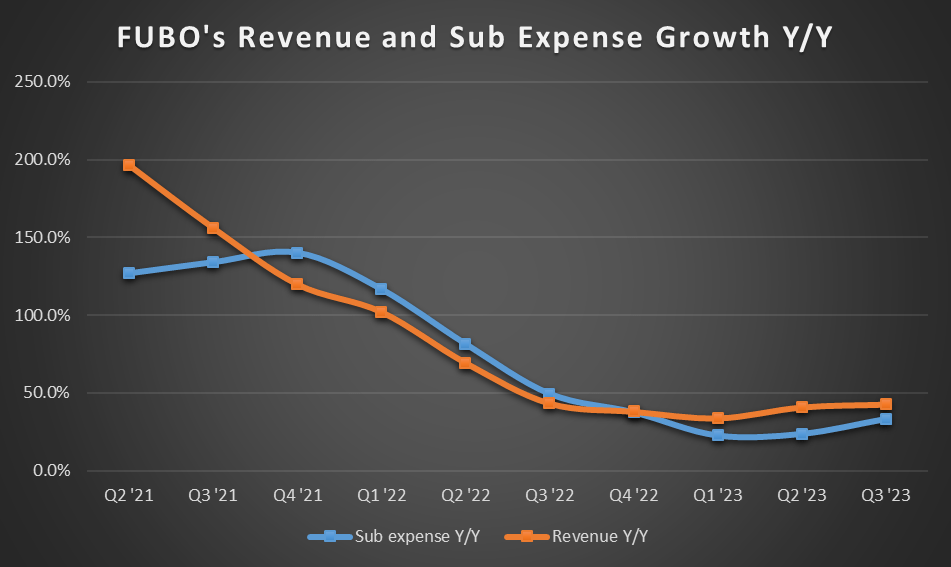

The Big Expense

The subscriber-related expense is where most of the company's costs rest. The biggest hurdle to profitability has been this expense, and until a year ago, this line item was not slowing even as revenue slowed. But, this quarter, the trend of slowing expenses continued from Q1. In Q3, revenue grew 42.8%, while SRE grew 33.4%. This is the direction the company needs to go to reduce cash burn and find breakeven.

However, you'll notice in the below chart the expense's growth rate has trended up since Q1. I've noticed the seasonal trend (while still slower over the last year than revenue) tends to take a step down in Q1 on any given year before generally rising the remainder of the year. Typically, some content contracts roll at the beginning of the year, and while Q3 and Q4 of this year may show some growth acceleration on this expense line, I expect Q1 to begin another set of contracts showing less cost per subscriber.

Chart mine, data from FUBO's Shareholder Letters

{kind=link}

In line with my expectations, management expects this leverage with SRE to continue as subscribers and subscription pricing grow.

As we continue to grow subscribers, optimize our pricing, we expect to see continued leverage on the SRE line , which decreased from 95% to 89% of revenue in Q3 2023 versus the prior-year period.

- John Janedis, CFO, fuboTV's Q3 '23 Earnings Call

Much of this depends on carriage contracts and negotiations, as SRE is the biggest mover for net loss and use of cash. But Gandler expects the trend to continue on that front:

...content costs, which is [a] $1 billion line item. And one of the things that I look at is contribution profit. And if you look back, the last six quarters consecutively, we've seen an expansion of contribution profit. That will continue as we work through our agreements.

- David Gandler, CEO, fuboTV's Q3 '23 Earnings Call Q&A

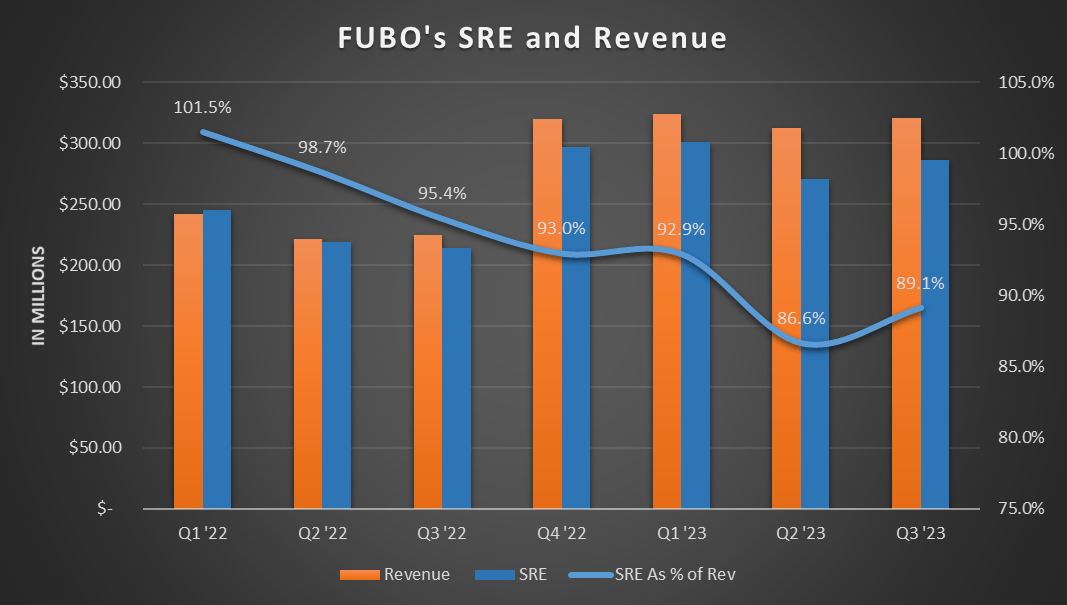

Another way to look at the improvement for SRE is based on its margin relative to revenue. This perspective's trend is more easily seen below and shows the overall trend is improving even if there are slight rises along the way. This also more easily tracks the improvements to content agreements and how renewals are helping.

Chart mine, data from FUBO's Shareholder Letters

{kind=link}

This is the trend needed to reach its 2025 breakeven goal. And so long as revenue grows faster than SRE, this leverage trend will continue.

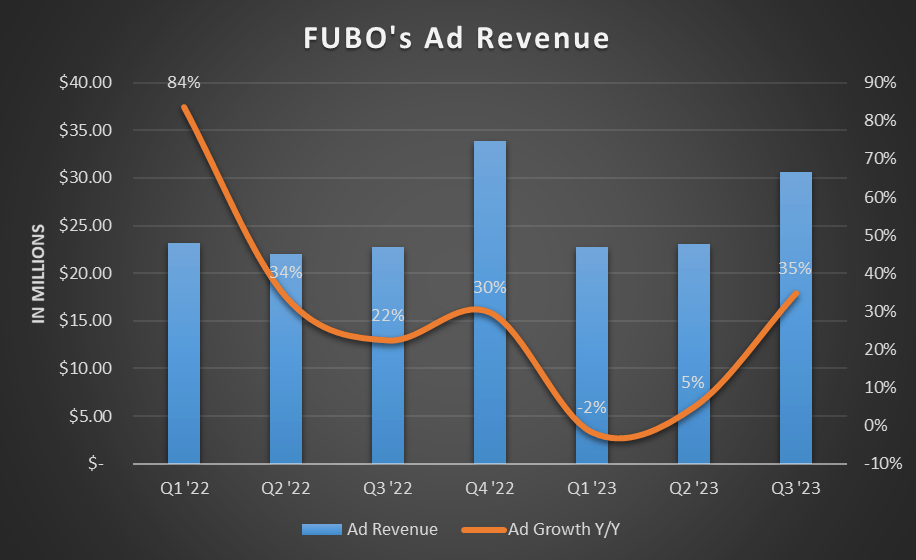

Ads Are A Bright Spot

It's no secret advertising is a touch-and-go industry right now. While Meta Platforms ( META ) is seeing growth return nicely, Google ( GOOG )( GOOGL ) and Snap ( SNAP ) are still either flatlining or barely getting off the ground from 2022. I attribute the current winners in advertising to their efforts in AI. FUBO not only has efforts in AI underway for advertising and other initiatives, but its ability to target viewers and do so well has granted it promising results in the vMVPD industry.

The company's ad revenue business picked up momentum during the quarter and grew at its highest level since Q1 '22.

Chart mine, data from FUBO's Shareholder Letters

{kind=link}

Management expects ad momentum to continue in Q4.

We noted on our last earnings call that we expected the ad market would experience an acceleration in the back half of 2023, and are pleased that trends are moving favorably in that direction.

- David Gandler, CEO, fuboTV's Q3 '23 Earnings Call

However, it expects Q4 ad growth to moderate from Q3 but be above Q2's growth rate:

...October came in a little bit lighter than what we saw for the third quarter in any specific month. And so, if I give you sort of some guardrails, I would say if 2Q grew at -- I think it was around 5%, 3Q was 34%, call it, 4Q probably looks somewhat closer to 2Q than 3Q.

- John Janedis, CFO, fuboTV's Q3 '23 Earnings Call Q&A

Considering Q4 '22's political climate and 30% growth comp, coming in at even 10% growth is quite strong in this still weak ad market. It'd ultimately mean advertising will grow to $37.24M against tough comparables and become a record quarter for ad revenue. It would also keep the 9.5% ad revenue makeup intact at the midpoint of Q4's revenue guide.

Show Me The Money

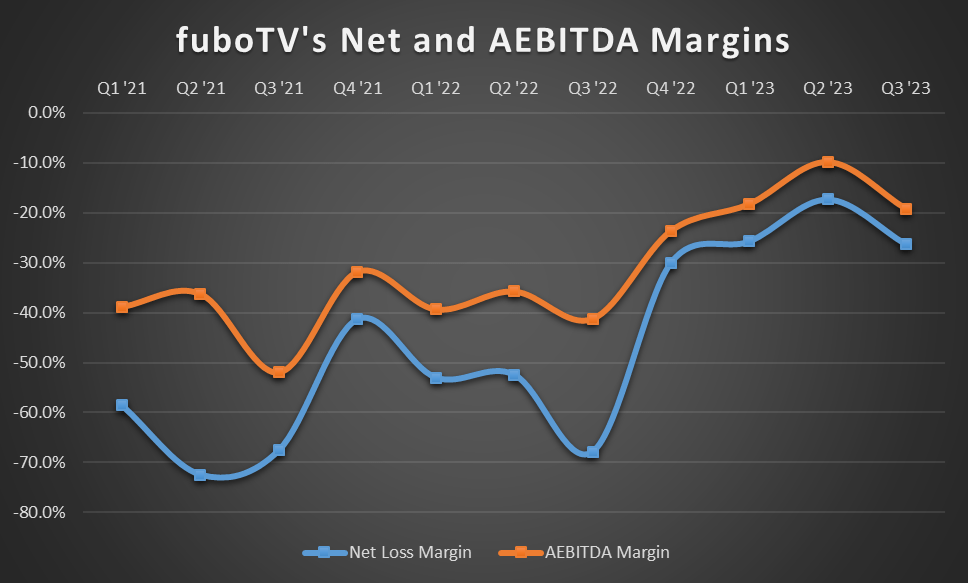

Finally, we arrive at the bottom line numbers and how they have trended over the last several quarters. This is the culmination of the preceding sections, which have detailed the business performance.

High revenue growth combined with shrinking SRE costs show continued improvement in net and AEBITDA margins. Q4 should provide a high point for the year in terms of margin and get the company the closest to breakeven it has been. It's also best to view the below on a year-over-year basis rather than a quarter-to-quarter basis, which your eyes may initially wander toward.

Chart mine, data from FUBO's Shareholder Letters

{kind=link}

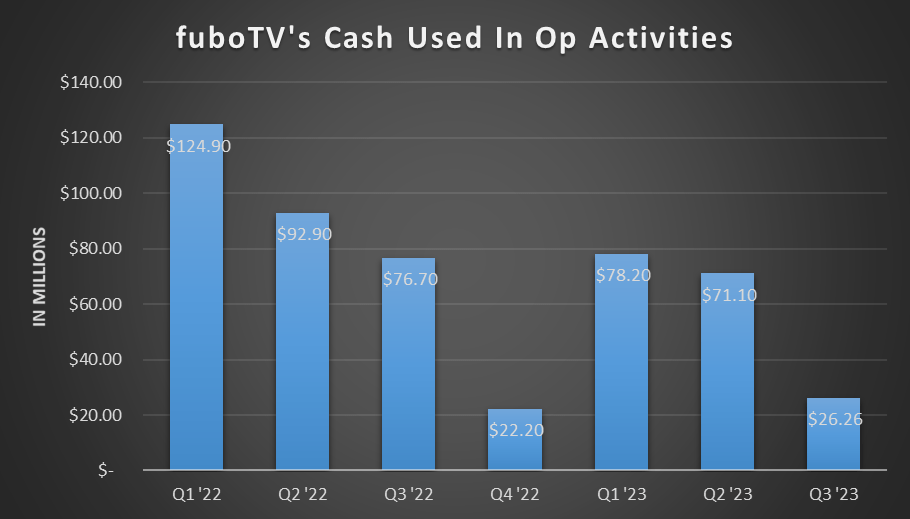

Of course, shrinking loss margins are important, but it comes down to dollar bills, how much is being used, and how much remains to continue operating.

While the company used $6M more in cash in Q2 than I had modeled, it used nearly $19M less than I modeled for Q3.

Chart mine, data from FUBO's Shareholder Letters

{kind=link}

Due to this, my model into 2025 has the company with just over $100M left in cash by the time it reaches breakeven.

| In Millions |

| Q1 '23A |

| Q2 '23A |

| Q3 '23A |

| Q4 '23 |

| Q1 '24 |

| Q2 '24 |

| Q3 '24 |

| Q4 '24 |

| Q1 '25 |

| Q2 '25 |

| Q3 '25 |

| Q4 '25 |

| Cash Used In Op Act. |

| $ 78.20 |

| $ 71.10 |

| $ 26.26 |

| $ 10.00 |

| $ 45.00 |

| $ 30.00 |

| $ 18.00 |

| $ 2.00 |

| $ 25.00 |

| $ 10.00 |

| $ - |

| $ (8.00) |

| Cash Remaining |

| $ 259.94 |

| $ 249.94 |

| $ 204.94 |

| $ 174.94 |

| $ 156.94 |

| $ 154.94 |

| $ 129.94 |

| $ 119.94 |

| $ 119.94 |

| $ 127.94 |

(A number shown in () means cash provided by operating activities)

The potential for the company to execute ahead of schedule is growing as the company used less cash this quarter than I anticipated, by 40%. Combined with the continued bullish outlook for SRE and raised guidance, the company doesn't have a cash problem over the next five quarters.

The conclusion, therefore, is the company does have a defined path, and it's not even the most bullish scenario with tons of outperformance. Even in this mildly bullish scenario, the company has a cushion of cash to make it to 2025. Based on the current run rate, the company could use $20M more per quarter beyond my model in 2024 and still get to mid-2025 with cash left.

Why Does All This Matter?

It'd be one thing if the stock was trading at some highly expected valuation level and didn't coincide with the risk still present. But it's an entirely different risk-reward setup when the stock trades for less than 1x price-to-sales. This valuation makes sense if the company was indeed headed for total cash burn and nearing a restructuring. However, with a buffer of over $100M in cash remaining by mid-2025, the company isn't at risk of going bankrupt like it was just a year ago.

From a fundamental perspective, the stock should trade at least a 1x price-to-sales, even if just on a trailing basis, with a path to cash remaining on hand by breakeven. This equates to a stock price of $4.36, or 38% upside. And this is just a starting point. If it's based on a forward basis, a 1x price-to-sales lands at $5.54, or 76% upside.

Should the company show signs of printing breakeven in 2024 or early 2025, the stock would easily exceed a 1x valuation. $6.00-$7.00 wouldn't be out of the question and would only mean a 1.08-1.26 price-to-sales multiple.

From a chart perspective, sentiment appears to have consolidated off the lows and may be headed exactly for the $6-$7 range per share "coincidentally." In either case, a fundamental and chart setup is in place for FUBO to double over the next two to three quarters.

There's No Issue With Cash With The Goal In Sight

With its improving subscriber numbers and pricing power leading to greater than expected revenue, its yearly improving content costs, and remarkable ad recovery, the business is ahead of where both bulls and bears expected it to be just a few quarters ago. Because of this, the cash burn situation is now not in a dire position. In fact, in my model, the company has a buffer heading into and through 2025.

But the stock's valuation is still pricing in a dire bankruptcy situation, far below one time sales. As long as the progress made in the business and its leverage continue on the same arc, the stock's fundamental picture grows further disconnected from its stock price, creating a skewed risk-reward situation. The skewed situation has already begun based on the valuation and the conservative fourth quarter guidance.

fuboTV is on the road to greater returns, and the company's initiatives to create features and functionality will continue to attract subscribers cutting the expensive cable cord to something made for the modern sports viewer and fan. And as subscribers add up, carriage costs and contract renewals have more favorable terms for the company, and lead to the business leverage position the company has sought for several years.

For further details see:

fuboTV Continues To Tip The Subscriber Business In Its Favor, Ads Helping