FUBO - fuboTV: Now In Better Shape To Achieve 2025 Cash Flow Goals

2023-11-25 01:37:24 ET

Summary

- fuboTV stock has gained almost 80% this year but is still down over 95% from its 2021 highs.

- After a rigorous evaluation of the prospects for fuboTV, I published a two-part deep dive analysis of the company in July and assigned fuboTV stock a price target of $7.29.

- In this follow-up analysis, I focus on evaluating the recent financial performance of the company to determine whether any changes are necessary for my valuation model for fuboTV.

- Early signs of pricing power and progress on the profitability front suggest that fuboTV is on the right track to achieving its 2025 financial goals.

fuboTV Inc. (FUBO) stock is down more than 95% from its highs of over $60 registered in 2021. This year, however, FUBO stock has gained almost 80% aided by the improving sentiment toward tech stocks. Last July, after a rigorous two-part analysis, I found fuboTV significantly undervalued and assigned FUBO a price target of $7.29. Since then, FUBO has gained 45%, beating the S&P 500's 3% gain handsomely. After digesting Q3 earnings and recent market developments, I am maintaining my fair value estimate for the company and continue to believe fuboTV is grossly mispriced in the market.

Let's get one thing straight before discussing my recent findings. Investing in fuboTV - or even considering that - is only suitable for growth investors with an investment time horizon of at least 5 years. In addition, investors should use position sizing to protect their portfolios from a potential erosion of capital resulting from a potential failure of fuboTV to turn cash-flow positive by 2025. I am forced to strike a cautious note here for a few reasons.

- Since Q4 2022, fuboTV has posted gross profits but margins are still negligible (6% in Q3).

- Content acquisition costs remain elevated and are unlikely to reduce soon, if at all. The company needs to scale a lot more to turn a profit at this rate of content acquisition costs.

- fuboTV is still a long way from generating positive cash flows.

- Ownership dilution is on the cards as the company may tap capital markets to fund growth projects.

If the above risks are too much for you to bear in exchange for potential multibagger returns, FUBO is certainly not for you. As an investor looking for alpha-generating opportunities, I am attracted to the company. In the remainder of this analysis, I will discuss why I continue to find FUBO attractive despite these risks (please read my two-part analysis published in June/July for a deep dive into company fundamentals and the macroeconomic outlook).

Early Signs Of Pricing Power

Investing in small, young companies is inherently challenging because of the difficulty associated with predicting a company's potential to enjoy durable competitive advantages over a long enough period to push the company into profitability. A couple of encouraging developments suggest that fuboTV is on the right track to enjoying pricing power in the streaming market, which is often the first sign of durable competitive advantages.

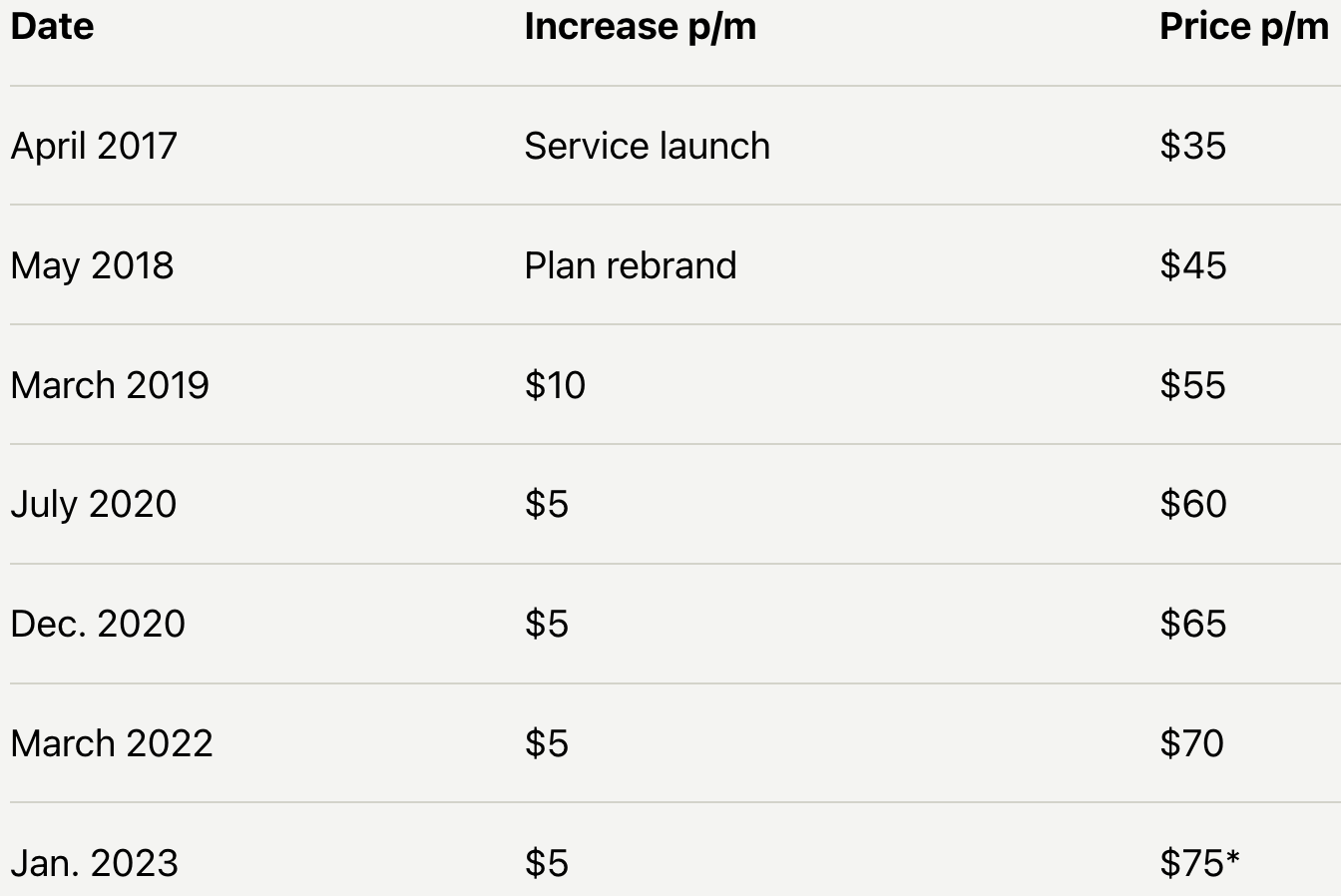

fuboTV raised the prices of its Pro plan - the cheapest subscription option - from $69 to $75 last January. When fuboTV gained popularity in 2017, the cheapest plan was priced at $35. As illustrated below, the company, since then, has hiked the price of the cheapest plan by a considerable amount.

Exhibit 1: fuboTV Pro plan price hikes

{kind=link}

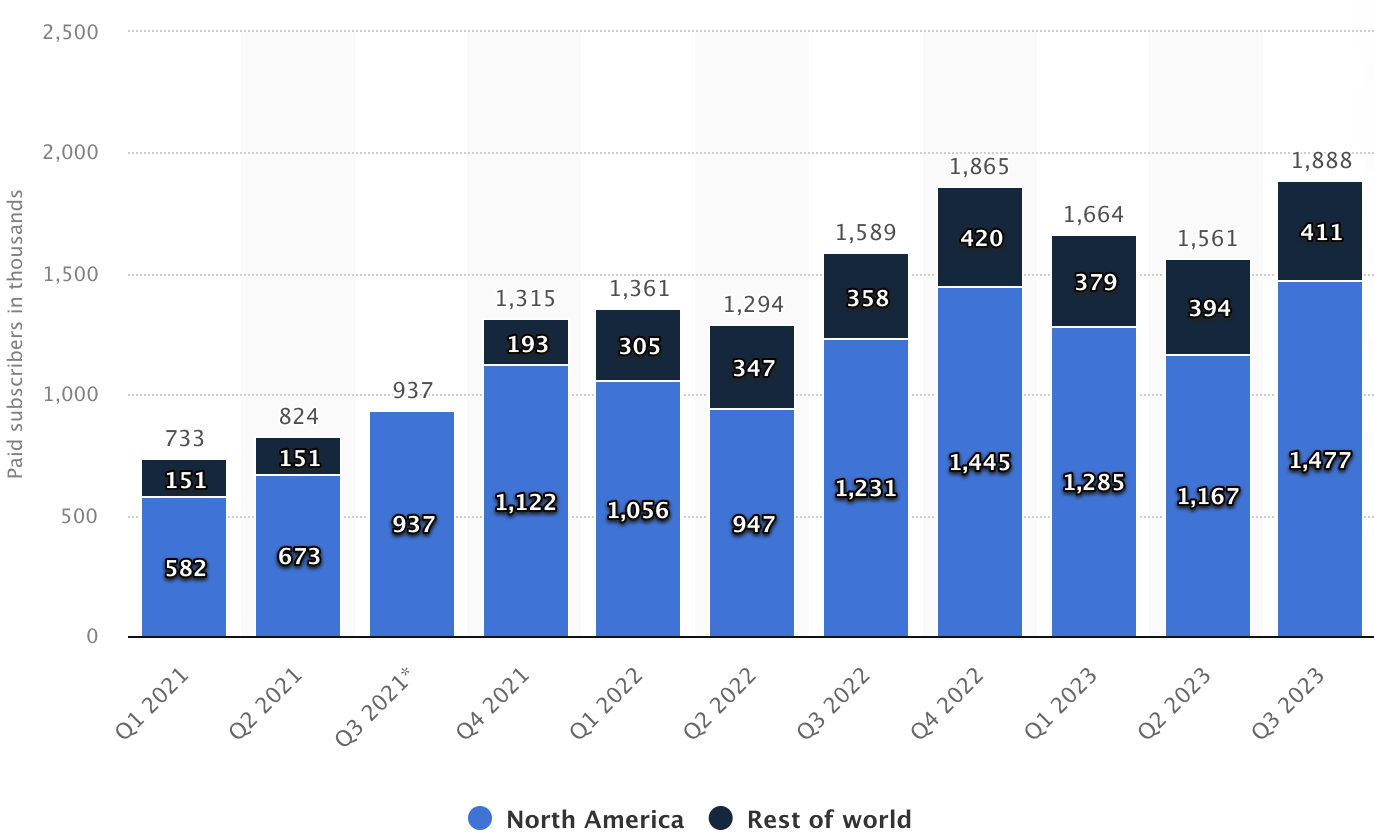

I am more interested in the price hike announced by the company earlier this year at a time when consumers were beginning to feel the wrath of rising interest rates and inflation. As illustrated below, fuboTV's subscriber growth in North America and internationally has picked up since the first quarter of 2023 after the price hikes were announced. The company ended Q3 with 1.477 million North American subscribers compared to 1.29 million in Q1. In my opinion, this is a clear sign that fuboTV's value proposition is appealing enough to lure cord-cutters.

Exhibit 2: fuboTV global paid subscribers by quarter

{kind=link}

It is too early to claim that fuboTV will enjoy durable competitive advantages. Still, I am encouraged by the company's continued ability to attract and retain users in a tricky environment.

Progress On The Profitability Front

fuboTV management has guided for positive cash flows in 2025, just two years down the line. When the company initially talked about this target, I was not entirely sure about its ability to achieve this. Today, after digesting the company's recent financial performance, I feel this target is very much within the company's reach. As a reminder to my new followers, I look for companies that can generate positive net profits in the long term - not just adjusted EBITDA. However, generating positive cash flows is often the first major milestone for a young company looking to break through to profitability. Positive cash flows also strengthen a company's liquidity profile, which is another important consideration for small-cap stock investors.

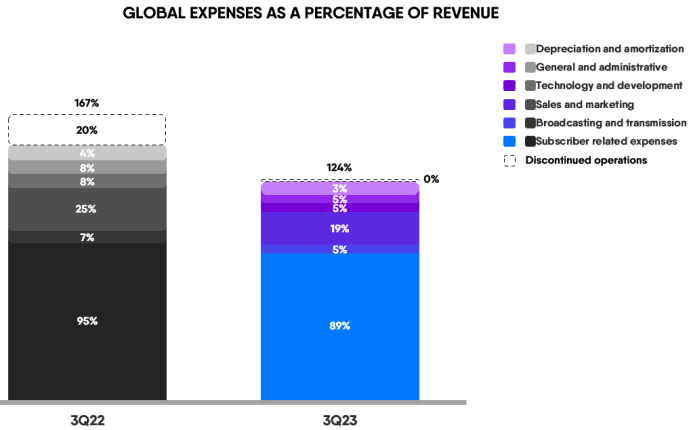

In Q3, subscriber-related expenses, which account for content acquisition costs, declined to 89% of revenue from 95% a year ago. While content costs are still sky-high, this gives an early indication of how fuboTV can inch toward profitability with sufficient scale. Recently executed price hikes certainly helped the company in Q3 alongside efforts by the management to manage costs better in a competitive environment.

Exhibit 3: fuboTV Q3 expenses as a percentage of revenue

{kind=link}

There was an improvement in the bottom line and other non-GAAP financial metrics too. The company reported a net loss of $84.4 million for the third quarter, down 20% from a loss of $106 million in Q3 2022. Cost management played a massive role in this improvement. In Q3, revenue grew 43% YoY while operating expenses grew at a slower pace of 23%, enabling fuboTV's net loss margin to improve by more than 20 percentage points. The adjusted EBITDA margin improved by over 17% percentage points as well.

With subscribers growing at a stellar pace (20% in North America and 15% in the rest of the world in Q3), revenue benefiting from recent price hikes, and the company's cost reduction strategies delivering the desired results, I believe fuboTV is now in better shape than it was a few quarters ago to reach its cash-flow profitability target by 2025.

Takeaway

fuboTV, as I highlighted in my previous articles, enjoys a long runway to grow aided by favorable macroeconomic trends for the global streaming sector. In this follow-up analysis to my deep dive article series on the company, I found that fuboTV is headed in the right direction to achieving its 2025 cash flow targets. However, I am not making any adjustments to my fair value estimate for the company as I prefer to patiently wait a few quarters to see if fuboTV's perceived pricing power will hold its strength amid the increasing competition in the sports streaming sector.

For further details see:

fuboTV: Now In Better Shape To Achieve 2025 Cash Flow Goals