FUBO - fuboTV's 0.7X P/S And Improving Profitability Prospects Signal Wonderful Upside

2023-12-27 15:55:47 ET

Summary

- Upon careful consideration of my investment journey, it is evident that fuboTV is one of my worst recommendations and personal investments.

- Despite suffering losses, the company deserves some credit for achieving resilient revenue growth and improving margins.

- The improving top and bottom-line trajectories could signal a major upside from the stock's current, depressed valuation levels.

- Still, the stock's investment case comes with notable risks, as failure to meet near-term profitability goals could lead to harmful dilution.

Investing in fuboTV ( FUBO ) has been a tremulous journey for me, marking it as one of my worst investments. While starting a bullish article with such a candid admission might seem strange, I find it essential to establish context for a clearer understanding.

Reflecting on my previous analyses, I wrote two bullish articles on FUBO: one in May 2021 and one in October 2021 . Sadly, the subsequent performance has been disheartening, with shares witnessing a substantial decline of 86% and 89% since each article's publication, respectively.

Admittedly, the results have been far from favorable, and obviously, I lost a lot of money. However, I view this as a valuable and albeit costly "course" on what happens when you go long on a money-losing company in the face of potential rising interest rates.

Despite experiencing substantial losses, which reached even higher percentages when the stock plummeted below $1.00, I chose to maintain my position in FUBO to observe the unfolding developments. With a staggering decline of over 90%, the prospect of the stock reaching zero no longer weighed heavily on my mind, as a significant portion of my initial investment had already vanished.

Another pivotal factor that influenced my decision to hold onto the stock was the company's resilient performance in expanding its top-line revenue despite facing a deteriorating balance sheet attributed to continuous net losses.

Sure, there were some setbacks in this journey, too, including shutting down a touted revolutionary betting service integrated with FUBO's live sports streams to mitigate losses. That said, the company displayed commendable execution in growing its core streaming service.

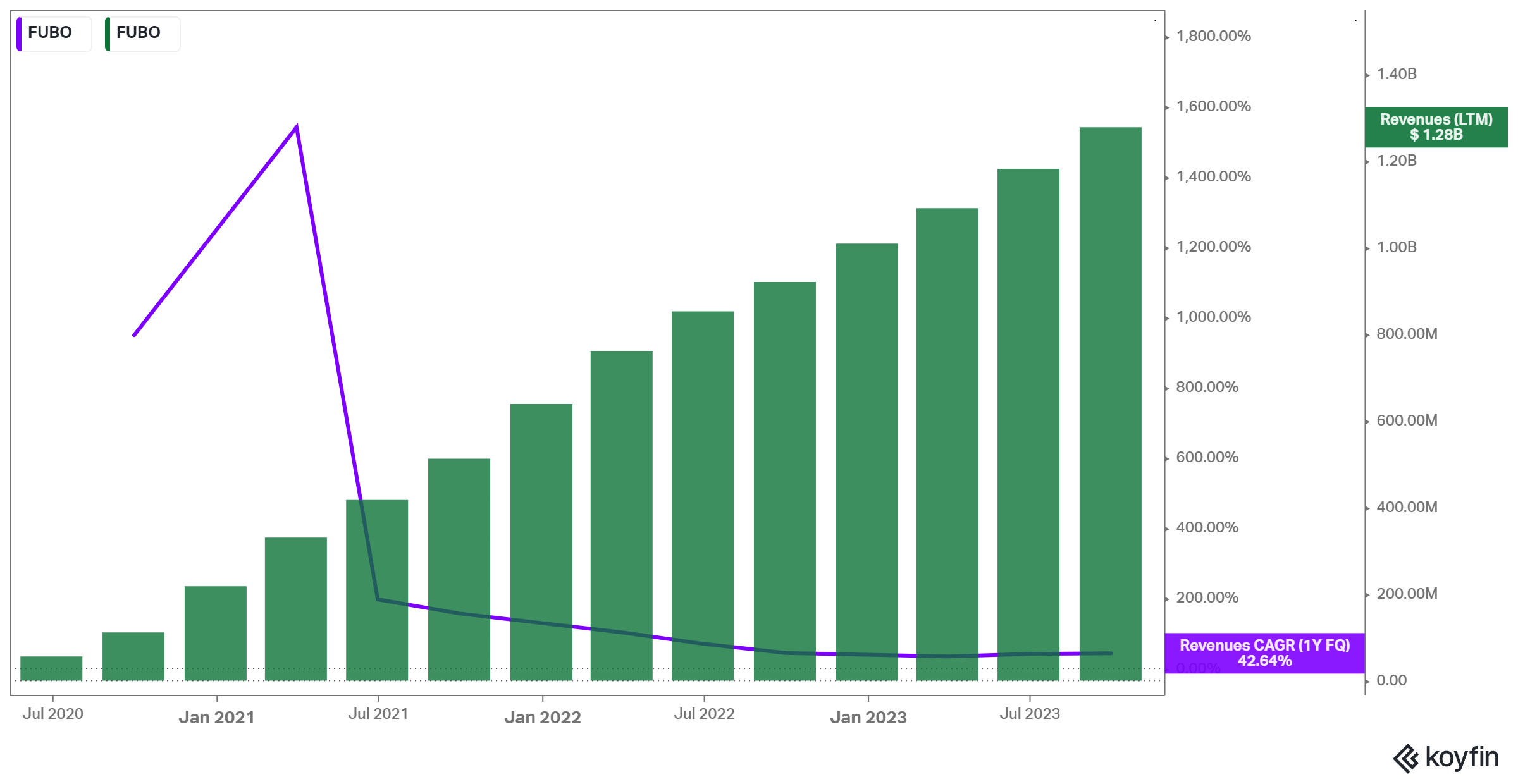

Throughout the steep decline in the stock price, revenue growth remained robust and has, in fact, continued to thrive up to the present day. While revenue growth has decelerated from the triple-digit percentages seen during the days of the pandemic, it remains at very exciting levels.

In the company's most recent Q3 results , FUBO posted revenue growth of 43%, reaching $320.9 million. Impressively, this implies an acceleration compared to Q2's and Q1's revenue growth of 41% and 36%, respectively.

FUBO's Revenue Growth (Koyfin)

{kind=link}

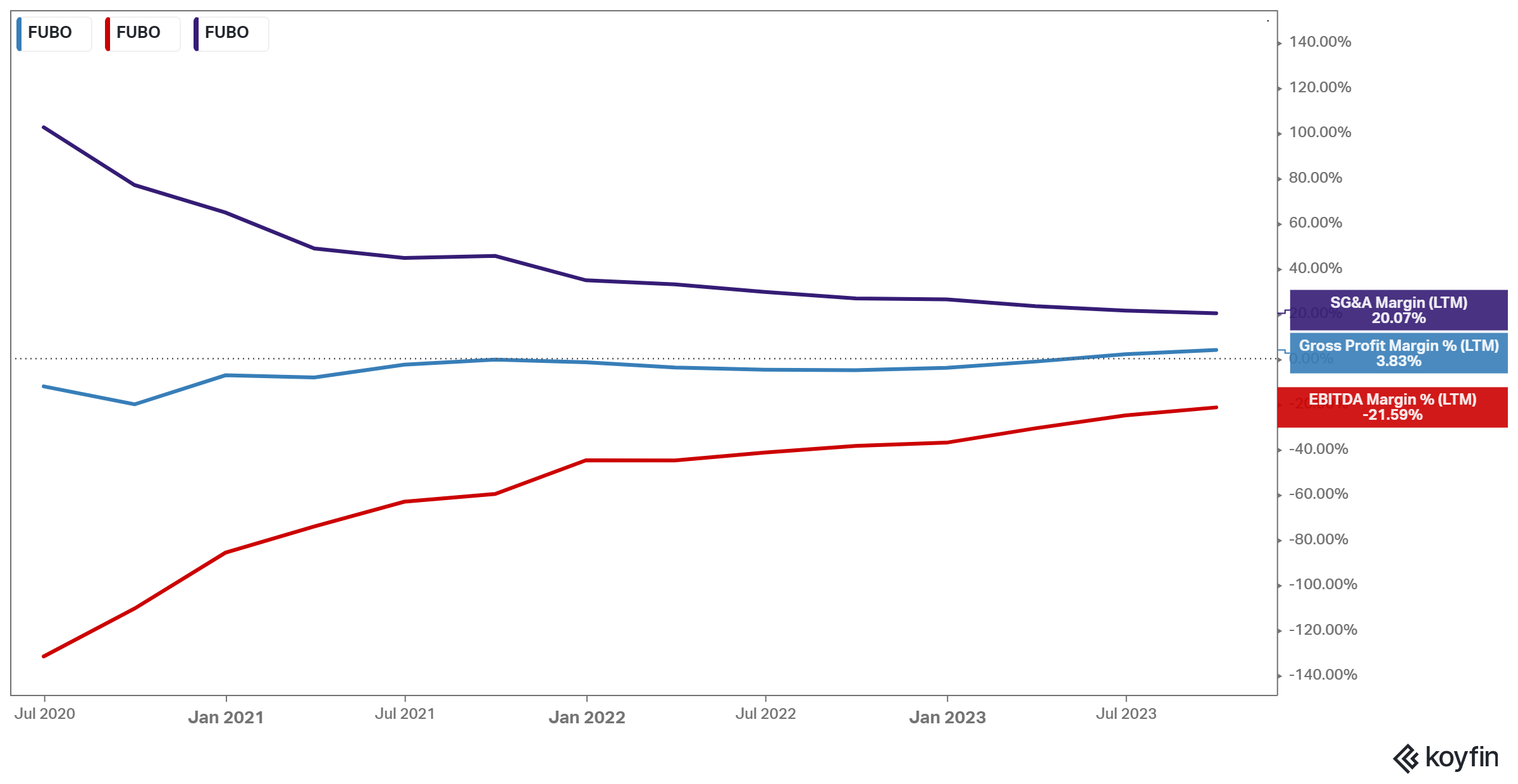

Meanwhile, margins have been on an upward trend due to the ongoing surge in revenues and management's heightened strategic emphasis on FUBO becoming cash flow positive by 2025.

As you can see in the graph below, economies of scale have started to kick in in recent quarters as FUBO's subscriber base has been increasing, resulting in gross margins turning positive. SG&A expenses as a percentage of total revenue have also declined over time.

FUBO's Gross, EBITDA, and SG&A margins (Koyfin)

{kind=link}

Despite FUBO's strong revenue growth and improving margins, the stock has remained depressed. Sure, shares have more than tripled from their sub-$1 levels. However, from a valuation point of view, FUBO continues to trade at overly attractive levels. While the stock has somewhat recovered from trading at a P/S of 0.2X during last March/April, shares still trade at a rather depressed P/S of just 0.7X.

In my view, this valuation multiple translates to very strong upside potential if we assume FUBO meets its cash-flow-positive goal by 2025 - especially given that FUBO is expected to keep posting notable revenue growth in the coming years.

As you can see, even with Wall Street forecasting significant deceleration in revenue growth in fiscal 2024 and fiscal 20254, FUBO is still expected to achieve revenue growth of about 20% and 17% each year, respectively.

FUBO's P/S Multiples (Seeking Alpha)

{kind=link}

Assuming the company achieves a modest free cash flow margin of 5% in fiscal 2025, as per management's plan to be cash flow positive by that time, this implies a free cash flow of $95 million. In that scenario, the stock trades today at just about 10X its FY2025 free cash flow.

While there is some forward-looking uncertainty attached to this scenario (and any other scenario in which you apply your own free cash flow margin projection), this is a highly attractive multiple for a company operating in a niche space and growing revenues at very exciting rates.

It's also worth noting that FUBO's valuation does not necessarily need to be compressed in the context of what appears to be a very crowded SVOD market.

The streaming landscape is fiercely competitive, with industry titans like Netflix ( NFLX ), Disney ( DIS ), Amazon ( AMZN ), and AT&T ( T ) vying for market dominance. Consequently, the growth of these giants' streaming platforms has significantly decelerated. A case in point is Disney+, which has experienced a decline in subscribers in recent quarters. In sharp contrast, FUBO continues to exhibit robust growth, underscoring its strategic advantage within the industry by prioritizing live sports.

In this context (i.e., FUBO evolving into a market leader in live sports streaming), we could see the stock attracting a much more prominent multiple, resulting in shares delivering exciting returns both from the underlying revenue growth and the possibility of a multiple expansion.

What's The Catch?

FUBO's sub-1X Price-to-Sales (P/S) ratio holds the promise of substantial returns, contingent upon the company achieving profitability in the near future. One could posit that, at this valuation, the stock might emerge as an appealing acquisition target for a major player seeking to capitalize on operational synergies, cost reductions, and the absorption of FUBO's high-value subscriber base, especially considering its industry-leading Average Revenue Per User (ARPU) of $83.50.

However, an investment in FUBO comes with a caveat. Simply put, if FUBO depletes its existing cash reserves before achieving positive cash flow, the prospect of securing additional funding could pose a serious threat to the stock's performance.

For context, FUBO ended Q3 with cash and equivalents of $259.9 million. The company also achieved a $40 million year-over-year improvement in free cash flow, which landed at a negative $29.5 million compared to a negative $69.5 million last year.

Observing the positive trajectory of FUBO's free cash flow margin, it seems the company possesses sufficient resources to sustain its operations until it attains positive free cash flow, thereby achieving its cash flow-positive goal without resorting to additional fundraising. The current negative free cash flow run rate affords the company several quarters of financial flexibility during this transitional phase.

Nevertheless, the inherent risk lies in unforeseen circumstances, such as unexpected spikes in expenses or adverse events that may lead to unanticipated cash outflows. If FUBO finds itself needing additional capital soon, the potential consequences could be severe.

The company's less-than-robust financial position may dissuade creditors from offering favorable lending terms, leaving FUBO with the alternative of issuing more stock to raise funds. Yet, given the current depressed valuation of the stock, such a move would result in instant and destructive dilution.

For instance, raising $150 million could translate to approximately a 15% dilution at the current stock levels. Since investors have already weathered significant dilution since the stock's IPO, this scenario might erode confidence in FUBO, contributing to further downward pressure on its stock price.

For further details see:

fuboTV's 0.7X P/S And Improving Profitability Prospects Signal Wonderful Upside