FUPPF - Fuchs: Waiting For The Breakout

2023-10-04 23:26:39 ET

Summary

- Fuchs SE, a German chemical company, has reported solid results for the first half of fiscal 2023, with sales and EBIT increasing by 11.1% year-over-year.

- The company also raised its guidance for free cash flow.

- While management is cautious for the next few quarters, we can be optimistic about solid long-term growth for Fuchs.

- In my opinion, the stock is still undervalued.

To my surprise, I am actually holding several German companies that are - at least in parts - operating in the chemicals industry. Of course, companies like Bayer AG ( BAYZF ) or Henkel AG ( HENKY ) are also operating in other segments as well, but they are also chemical companies. And these companies did not perform great year-to-date, which did hurt my portfolio. Among the companies displayed in the chart, I own every stock aside from Covestro AG ( CVVTF ) (which outperformed).

Among my four holdings, Fuchs SE ( FUPBY ) (formerly known as Fuchs Petrolub) was the best-performing stock. And despite the new name and the underperformance since my last article was published, I remain bullish about Fuchs and will hold on to my "Buy" rating.

2023: High Growth Rates

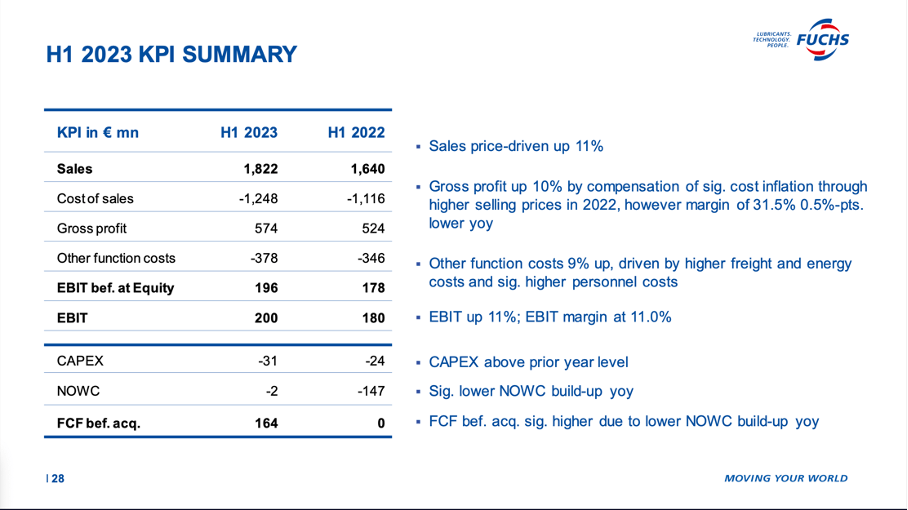

While many other companies in the chemical sector struggle, Fuchs reported solid results for the first half of fiscal 2023. Sales increased 11.1% year-over-year from €1,640 million in H1/22 to €1,822 million in H1/23. And all three regions contributed to growth - especially North and South America increased sales at a high pace. EBIT also increased 11.1% year-over-year from €180 million in the same timeframe last year to €200 million in H1/23. And finally, earnings per ordinary share increased from €0.92 in H1/22 to €1.03 in H1/23 - resulting in 12.0% year-over-year growth.

Fuchs Roadshow Presentation September 2023

{kind=link}

The company could also report free cash flow before acquisitions of €164 million in H1/23 and compare to €0 in free cash flow in the same timeframe last year this is a huge improvement. Of course, free cash flow in H1/22 was rather an outlier.

Guidance

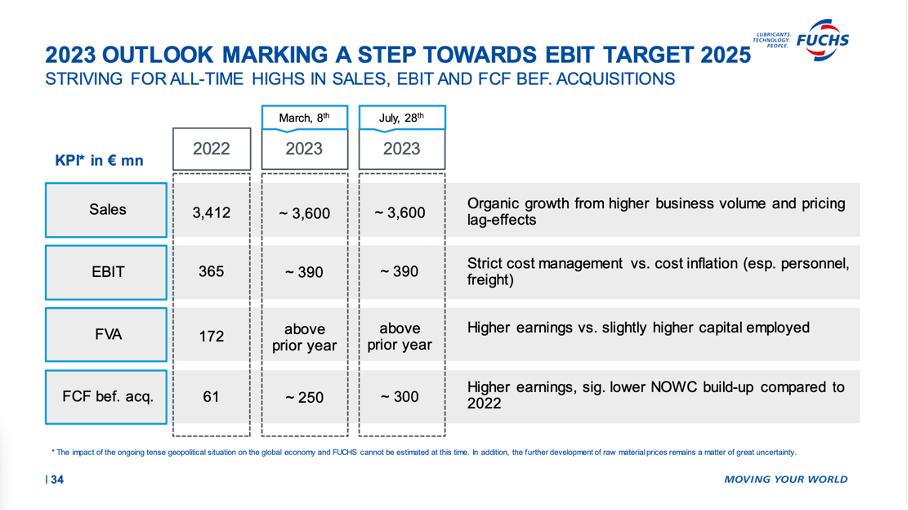

Aside from reporting great first half results, Fuchs also reiterated its previous guidance (for most metrics). Sales for the full year are expected to be around €3.6 billion and EBIT is expected to be around €390 million. And compared to a previous guidance for free cash flow was actually raised. Instead of €250 million according to the previous guidance, Fuchs is now expecting free cash flow before acquisitions to be around €300 million.

Fuchs Roadshow Presentation September 2023

{kind=link}

During the last earnings call, management commented several times on the guidance and was asked by analysts several times for more details. Management pointed out that these numbers are probably in contrast to most other chemical companies - especially in the German-speaking area. And Fuchs is admitting it is being cautious with its guidance for the full year, but on the other hand management is confident it does not have to lower the guidance in the coming months. When asked why guidance for EBIT was so low, CFO Isabelle Adelt answered :

Although, the current environment, as I said, in the US, but in Asia as well, is obviously a little difficult to navigate. We saw varying demands. A lot of other companies issue profit warnings. This is why we decided to stay on the cautious side to make sure to cater for all of those risks. Although, of course, guidance around 390 does not mean that we will not do all that is in our power to exceed this number and that a number in the ballpark of 400 could be achievable.

Management is especially cautious as the current environment in many regions around the world is "difficult to navigate and to read". And while volumes for Fuchs are very stable, management is seeing hints that the customers getting more cautious.

China

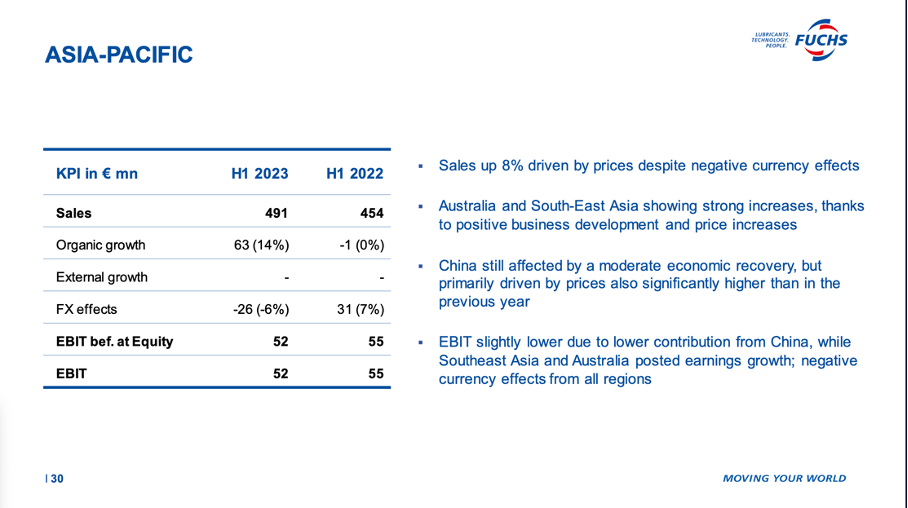

And one region that is especially difficult to navigate is China. When looking at the results in the first half of 2023, sales increased 8% from €454 million in the same period last year to €491 million while organic growth was 14% and offset by negative currency effects. However, management was disappointed as they were expecting even higher sales in the beginning.

Fuchs Roadshow Presentation September 2023

{kind=link}

During the last earnings call, management also commented on the rather high levels of uncertainty in China:

Well, if you look at how the economy in China is developing, growth rates are not yet or not there where we used to see them before COVID. So economy is still relatively slow. There's a lot of uncertainty in the market. The demand from the industry is not as strong as it used to be before COVID. And we only see a slow recovery, especially due to the fact that a lot of export business in China is not there yet.

And while management is rather cautious for the next few quarters, they seem to be optimistic over the long run that China will contribute to growth. The sales team was quite successful in getting new accounts while existing customers were ordering with a low volume. During the earnings call, management stated:

Although, our team in China was very successful in gaining new accounts, getting access to new customers in the market. So we were able to compensate for most of the volume growth that did not come from the existing accounts yet. So I think this is very good news, because once the economy starts to pick up again, we have the old-face business with Chinese as well as Western customers, and we already have the new business in our books with the customers we now on boarded to make sure that we can at least meet our expectations.

Long-term Growth

And over the long run, Fuchs should be able to grow at a solid pace and offset short-term fluctuations or headwinds. In an article published in December 2022, I already wrote about the growth potential Fuchs has for the next few years (and probably decades):

The shift from ICE to EV is not really a threat for the business - the world shifting from private transportation to public transportation would be a threat as it would reduce the number of cars and the number of new cars sold. Or if people were suddenly using their existing cars less. But estimates are not really projecting less cars in 2040 - instead the number is expected to increase. In the United States the number of annual sold cars is expected to increase from 15 million in 2021 to 15.8 million in 2040. In Europe the number is expected to increase from 13 million to 16 million and in China expectations are 35 million sold cars in 2040 (compared to 21 million in 2021).

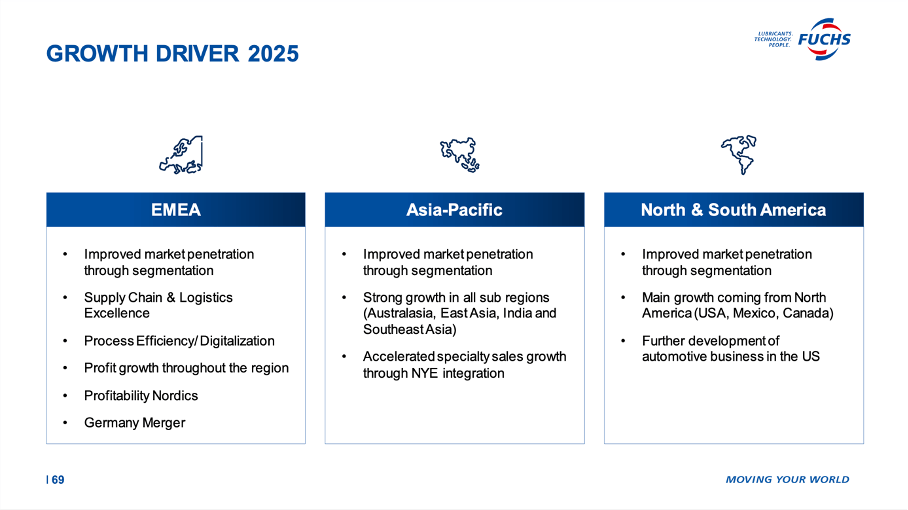

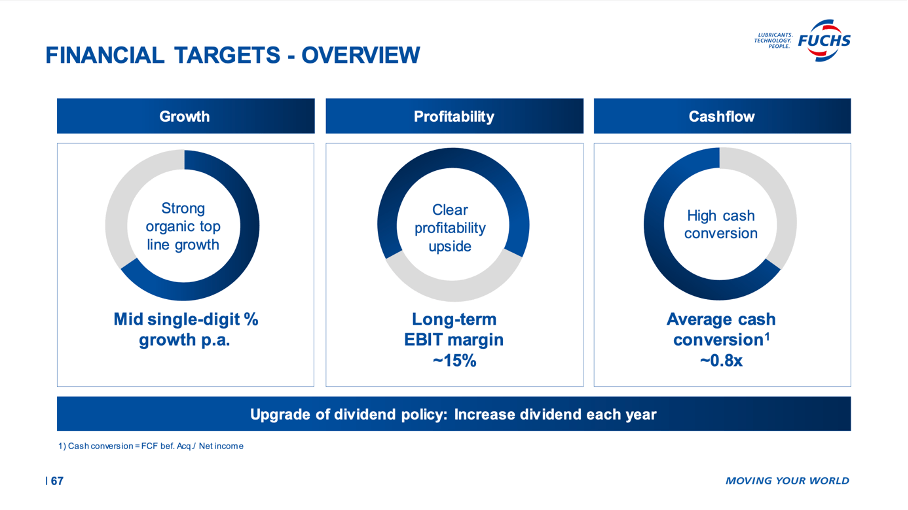

And the company is identifying several growth drivers in the different regions for the next few years.

Fuchs Roadshow Presentation September 2023

{kind=link}

In total, Fuchs is expecting top line to grow in the mid-single digits due to strong organic growth. Additionally, EBIT margin is also expected to improve and free cash flow conversion rate should climb as high as 80%.

Fuchs Roadshow Presentation September 2023

{kind=link}

Intrinsic Value Calculation

In my last article, I calculated an intrinsic value of €45 for Fuchs Petrolub and I still think the fair value for the stock should be somewhere in this price area. But let's use a few different calculations using the DCF model to provide more information on the intrinsic value of Fuchs at this point. The basis for our calculation is 135.0 million outstanding shares on June 30, 2023, and - as always - a 10% discount rate as this is the minimum annual return I would like to see.

In a very simple calculation, we can just use the expected free cash flow for fiscal 2023 (€300 million) as basis and assume about 5% annual growth in the years to come. Fuchs' long-term target is mid-single digit revenue growth (see slide above) and therefore 5% annual growth for FCF seems realistic. When calculating with these assumptions we get an intrinsic value of €44.44 for Fuchs Petrolub.

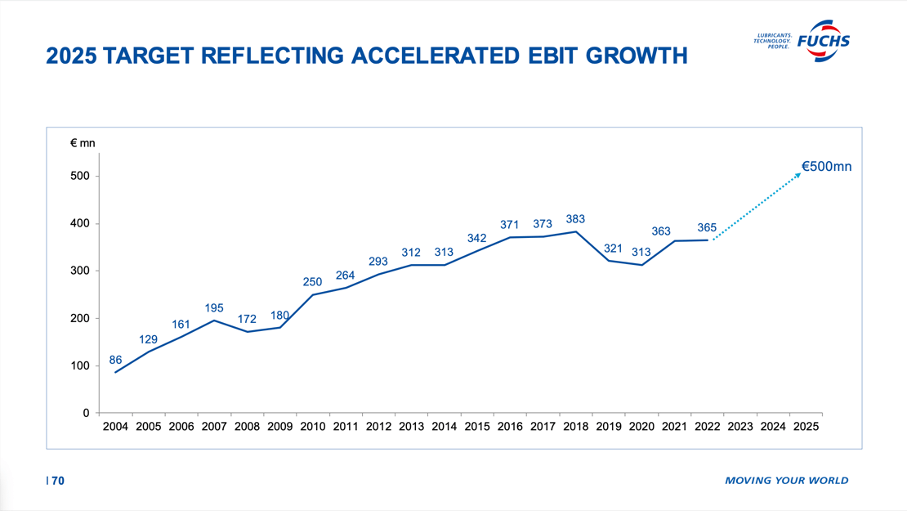

However, what is not reflected in this calculation is the company's goal to improve EBIT margin to 15% again. Now the margin is around 11%. When Fuchs can keep free cash flow conversions stable (in this case conversion between EBIT and free cash flow) we should also expect a much higher free cash flow than calculated above.

And in my opinion, 5% growth is also a rather a cautious growth assumption as Fuchs should be able to grow at a higher pace. In the last ten years, the numbers reported by Fuchs do not support higher growth assumptions: While revenue increased 6.49% in the last ten years, operating income increased only with a CAGR of 2.60% and earnings per share increased with a CAGR of 2.58%. However, when looking at previous years and longer timeframes, Fuchs could grow at a much higher pace. And in the last few years, Fuchs had high investments (capital expenditures) and high expenses. But as the situation is normalizing again, we can expect much higher growth rates in the next few years for the bottom line.

Fuchs Roadshow Presentation September 2023

{kind=link}

In my opinion, we could also assume 6% growth for the years to come and due to the wide economic moat, we can also assume 6% growth till perpetuity. When calculating with these assumptions we get an intrinsic value of $55.56 for Fuchs and the stock is clearly undervalued.

Looking At The Chart

When looking at the chart, Fuchs is still "fighting" with its resistance line I already pointed out in my last article. Depending on how accurately we are drawing the line and also depending on what chart we are using - normal or logarithmic - we get different lines, the stock is already slightly above the resistance level or still below it.

Fuchs SE: Weekly Chart (TradingView)

{kind=link}

And aside from this resistance level marked by the declining trendline (white), the stock is also caught in a sideway range (marked in yellow) between €28.50 and €32 and the 200-week moving average (red line) is also a resistance for the stock. But when the stock manages to break out of its sideway range - and therefore to overcome the other two resistance levels - we can be optimistic that the stock will climb higher with €40 being the next potential target.

Conclusion

In my opinion, Fuchs is still undervalued and a good buy. Of course, we are faced with the risk of the stock bouncing off the current resistance level (200-week moving average, declining trendline) and if this happens one might buy at the completely wrong time. But as long-term investors we should not care so much about short-term fluctuations. Nevertheless, one can wait before buying if Fuchs is either declining again (and creating another buying opportunity) or if the stock is breaking out of its current range.

For further details see:

Fuchs: Waiting For The Breakout