FCELB - FuelCell Energy: Another Messy Year Likely Ahead

Summary

- FuelCell Energy releases disappointing Q4 and full-year FY2022 results.

- Both backlog and generation portfolio decreased after the company removed a number of projects for various reasons.

- Aggressive growth investments are likely to result in cash outflows of more than $300 million this year.

- With the one-time benefit from the recent POSCO settlement gone, full year revenue is unlikely to be anywhere close to the current analyst consensus.

- Given the toxic combination of ongoing execution issues, unrealistic growth expectations, and elevated risk of further dilution, investors should continue to avoid the common shares.

Note: I have covered FuelCell Energy ( FCEL , OTCPK:FCELB ) previously, so investors should view this as an update to my earlier articles on the company.

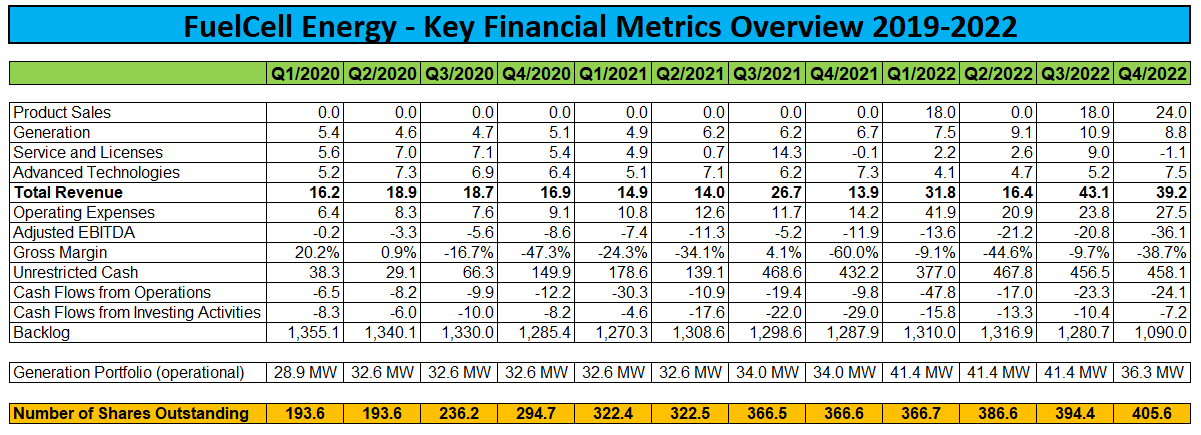

Last month, FuelCell Energy released disappointing fourth quarter and full year FY2022 results as the company's performance continues to suffer from persistent execution issues and the apparent lack of a viable business model.

Adjusted for $60 million in product sales related to a recent settlement agreement with former strategic partner POSCO Holdings ( PKX ), annual revenue remained more or less unchanged from the numbers reported in both FY2020 and FY2021.

{kind=link}

On an annual basis , reported gross margin of negative 22.7% reached a new multi-year low as benefits from the company's first product sales since FY2018 were offset by the requirement to expense construction costs of the Toyota Tri-Generation project in Long Beach after failure to timely secure renewable natural gas ("RNG") supply at favorable prices:

As further background on the costs related to the Toyota project, it was determined in the fourth quarter of fiscal year 2021 that a potential source of RNG at favorable pricing was no longer sufficiently probable for the Toyota project resulting in impairment of the asset. Thus, as the Toyota project is being constructed, only amounts associated with inventory components that can be redeployed for alternative use are being capitalized. The balance of costs incurred (i.e., the approximately $22.1 million associated with the construction costs mentioned above) are being expensed as cost of generation revenues.

FuelCell Energy continues to burn cash at a rapid pace. Free cash flow for the quarter was negative $31.3 million, but proceeds from relentless common shareholder dilution have resulted in the company's cash position remaining rather stable in recent quarters.

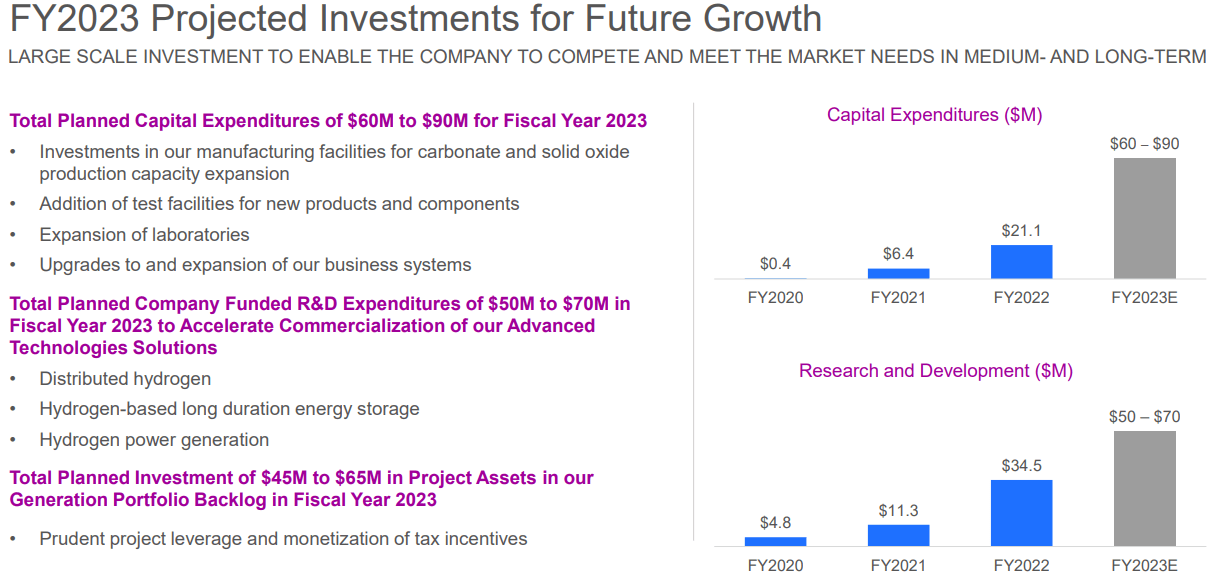

With $458.1 million in unrestricted cash at the end of FY2022 and 76.5 million shares still available for issuance under the company's most recent open market sale agreement, liquidity remains sufficient to fund the company's ambitious growth investments in FY2023:

{kind=link}

That said, with up to $225 million in projected capital expenditures and research and development ("R&D") expenses as well as an estimated $100 million in negative cash flow from operations not related to R&D, investors will likely have to prepare for further dilution this year.

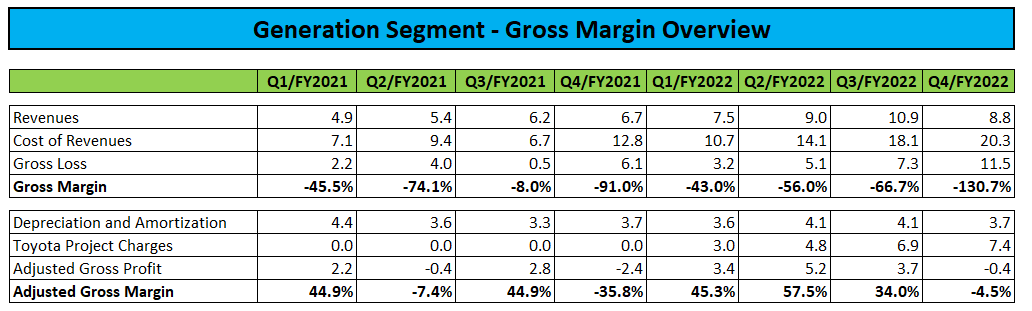

Looking at the company's core generation business, segment performance remains disappointing. Even when adjusted for depreciation, amortization and the above-discussed Toyota project charges, gross margin turned negative again in Q4:

{kind=link}

Generation revenues were down by almost 20% quarter-over-quarter. Clearly, the surprise removal of two projects (UCI Medical Center and Triangle Street) from the active fleet clearly has been a major factor here.

After being poked by analysts on the issue on the conference call , management provided sort of an explanation:

The Triangle Street project is a project here local in Danbury, right down the street from us. (...) Over the past couple of years, that project has evolved to more of an R&D type project where we're using it to essentially test out certain aspects of our platform, that's the high efficiency fuel cell. So, have evolved that from just a generation site where we're taking revenue to more of an R&D project. So it felt appropriate to remove that from our generation backlog.

On the UCI project, that project reached the end of its term. We entered into an agreement with the owner of the project, the UCI Medical Center. They are going through a capital expansion at the UCI Medical Center. So essentially worked out an arrangement where we -- they paid us to essentially remove that asset. Parts of that asset are able to be redeployed in our service fleet.

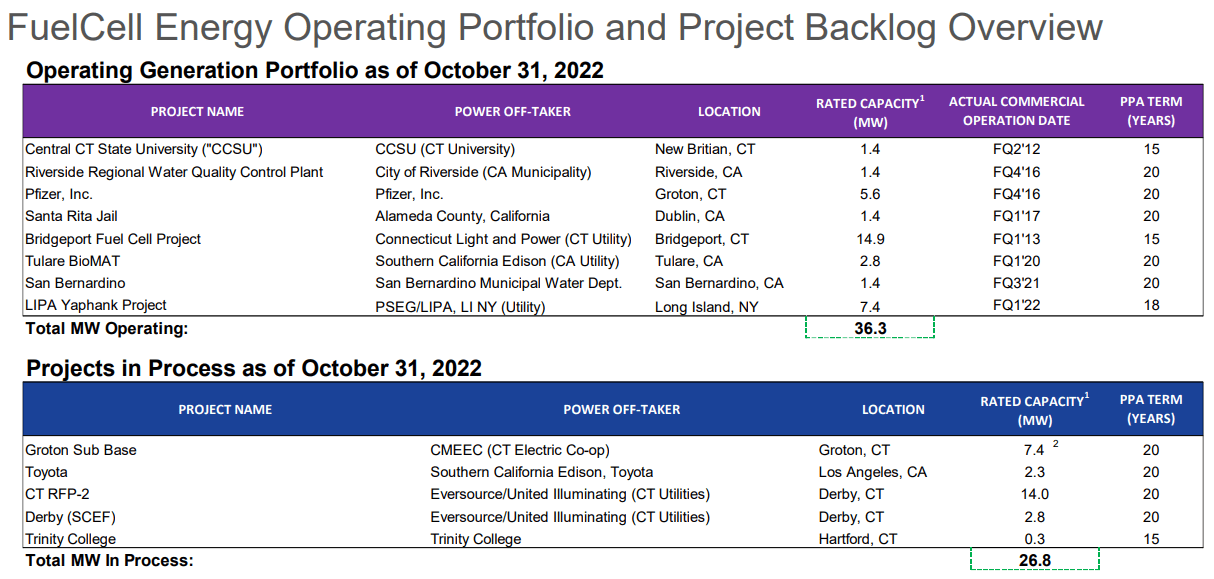

As a result, the rated capacity of the company's generation portfolio declined from 41.4 MW at the beginning of the fiscal year to 36.3 MW at the end of October:

{kind=link}

In addition, FuelCell Energy also removed two projects in Hartford, Connecticut with an aggregate rated capacity of 8.4 MW from the "In Process" portfolio:

So as we looked at Hartford, there's a couple of factors that we evaluated in terms of our decision around that program. One is, as we looked at the PPA and the timing of the PPA, the questions around interconnection and timing became a risk factor in terms of interconnection being able to be done in times to comply with the PPA. It's a project where we had exposure to gas prices. And as we looked at when we originally did this agreement to now, there's been a pretty significant shift in gas prices. And so as we looked at our ability to manage the gas price risk and that exposure, the risk around interconnection, we made a decision that right now this program didn't make sense for us to continue to move forward.

Please note that in addition to the above-discussed Toyota facility, two projects with an aggregate rated capacity of 16.8 MW in Derby, Connecticut also remain subject to fuel sourcing risk.

Mostly as a result of the company no longer pursuing the Hartford projects, backlog has been taking a $200 million hit:

Company Presentation

On a more positive note, after years of delays the company finally commenced commercial operations for its 7.4 MW project on the U.S. Navy Submarine Base in Groton, Connecticut. That said, ongoing problems have resulted in a reduced output of 6 MW which the company hopes to address over the next twelve months. Not surprisingly, the plant's reduced capacity has resulted in FuelCell Energy incurring a substantial one-time penalty and ongoing performance guarantee fees (emphasis added by author):

On December 16, 2022, the Company declared and, per the terms of the Amended and Restated Power Purchase Agreement between the Company and Connecticut Municipal Electric Energy Cooperative ("CMEEC") entered into on that date (the "Amended and Restated PPA"), CMEEC agreed that the platform at the U.S. Navy Submarine Base in Groton, CT (the "Groton Project") is commercially operational at 6 MW. As of December 16, 2022, the Groton Project will be reported as a part of the Company's operating generation portfolio. The Amended and Restated PPA allows the Company to operate the plant at a reduced output of approximately 6 MW while a Technical Improvement Plan ("TIP") is implemented over the next year with the goal of bringing the platform to its rated capacity of 7.4 MW by December 31, 2023. In conjunction with entering into the Amended and Restated PPA, the Navy also provided its authorization to proceed with commercial operations at 6 MW. The Company paid CMEEC an amendment fee of $1.225 million and will incur performance guarantee fees under the Amended and Restated PPA as a result of operating at an output below 7.4 MW during implementation of the TIP. Although the Company believes it will successfully implement the TIP within approximately one year and bring the plant up to its nominal output of 7.4 MW, no assurance can be provided that such work will be successful. In the event that the plant does not reach an output of 7.4 MW by December 31, 2023, the Amended and Restated PPA will continue in effect, and the Company will be subject to ongoing performance guarantee fees as set forth in the Amended and Restated PPA.

In addition, the company and a subsidiary of Exxon Mobil (XOM) extended their joint development agreement for carbon capture technology to August 31, 2023 to provide more time to collect data and allow for development of a second generation fuel cell module prototype as well as " studying the manufacturing scale-up and cost reduction of a commercial Generation 2 Technology fuel cell carbon capture facility ".

Just recently, FuelCell Energy secured the first order for its new solid oxide fuel cell which can operate on a variety of fuels, including hydrogen, natural gas, and renewable biogas.

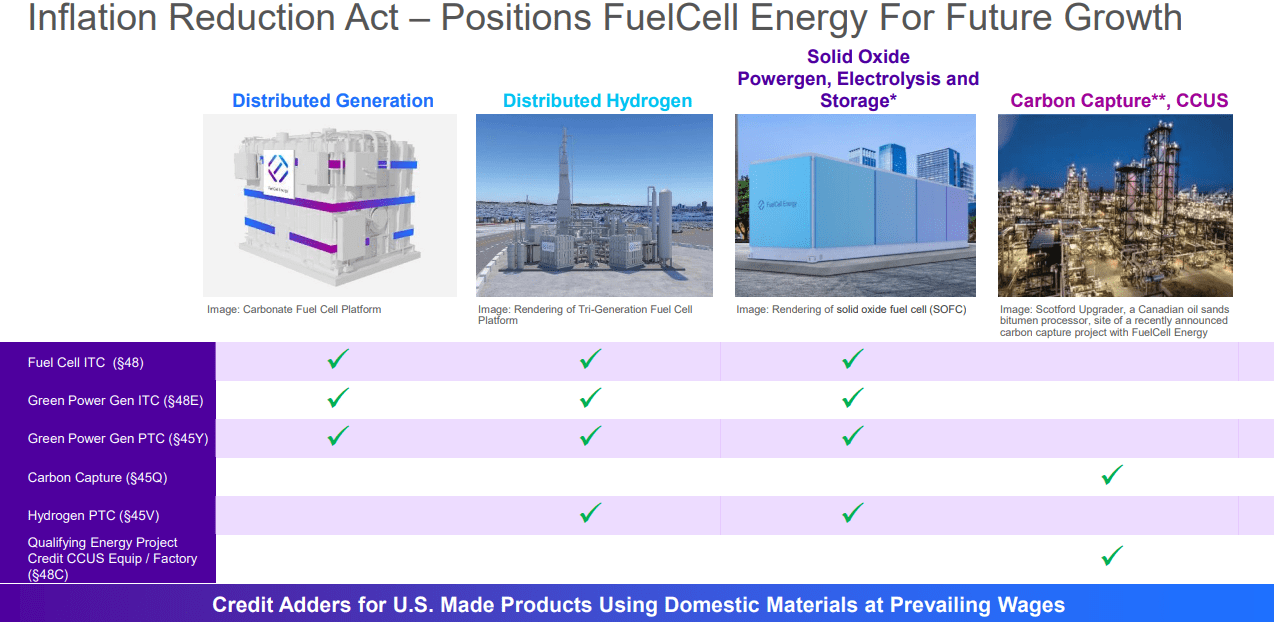

On the conference call, management projected higher service revenues for FY2023 due to a higher number of scheduled module exchanges at customer sites and touted potential benefits from last year's Inflation Reduction Act ("IRA"):

{kind=link}

That said, investors should not impact any near-term revenue impact from potential IRA incentives as market participants still wait for additional guidance from the Treasury Department and the Internal Revenue Service.

In FY2023, product sales are likely to remain limited as the company is still in the process of rebuilding its Korean sales channel.

Even with anticipated improvements in the company's service and generation segments, FuelCell Energy's FY2023 revenue is unlikely to come anywhere close to the $129 million analyst consensus. In fact, I would expect the number to end up well below $100 million. Consequently, analysts might be required to adjust their models over the course of the year with further price target reductions potentially in the cards.

Bottom Line

After a disappointing FY2022, FuelCell Energy has committed to aggressive growth investments which in combination with anticipated losses from operations might result in negative free cash flow of more than $300 million this year.

As a result, investors better prepare for further, aggressive utilization of open market share sales as a means to replenish the company's cash reserves.

With the one-time benefit from last year's POSCO Energy settlement gone, FY2023 revenues are unlikely to come anywhere close to the $129 million analyst consensus.

Given the toxic combination of ongoing execution issues, unrealistic growth expectations and elevated risk of further dilution, investors should continue to avoid the common shares.

Despite these issues, the company continues to trade at a massive premium to its closest and much larger competitor, Bloom Energy ( BE ).

Investors looking for a somewhat less risky investment in FuelCell Energy should avoid the common shares and consider taking a position in the company's Series B preferred shares ( OTCPK:FCELB ) which trade around 51% of face value despite ranking senior to common stock and paying a rather juicy 9.8% cash dividend on an annual basis.

For further details see:

FuelCell Energy: Another Messy Year Likely Ahead