FCELB - FuelCell Energy: Cash Usage Still High But Upgrading On Improved Refinancing Options

2023-06-08 22:16:08 ET

Summary

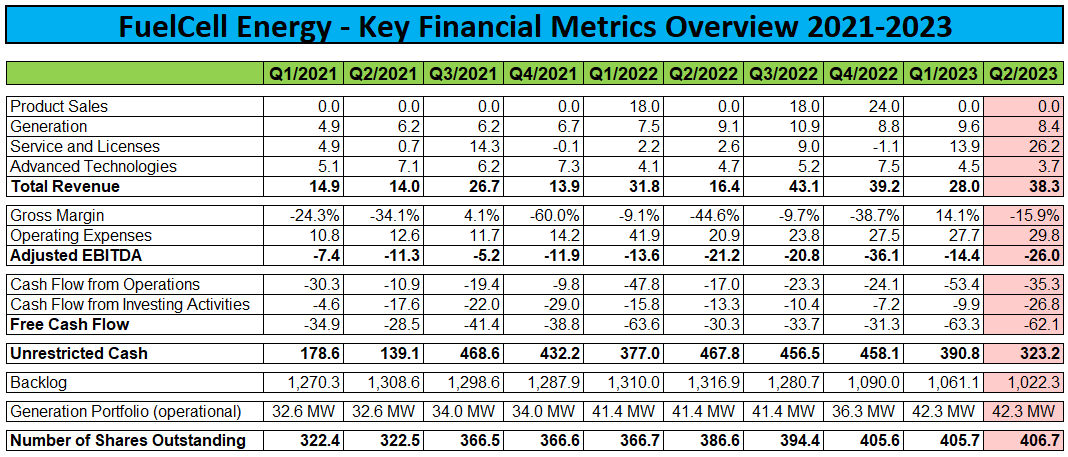

- On Thursday, FuelCell Energy reported another set of disappointing quarterly results. While revenues came in substantially above consensus expectations, margins, profitability and cash flows continued to suffer.

- Negative free cash flow of $62.1 million improved just slightly from the all-time high reached last quarter and resulted in available liquidity.

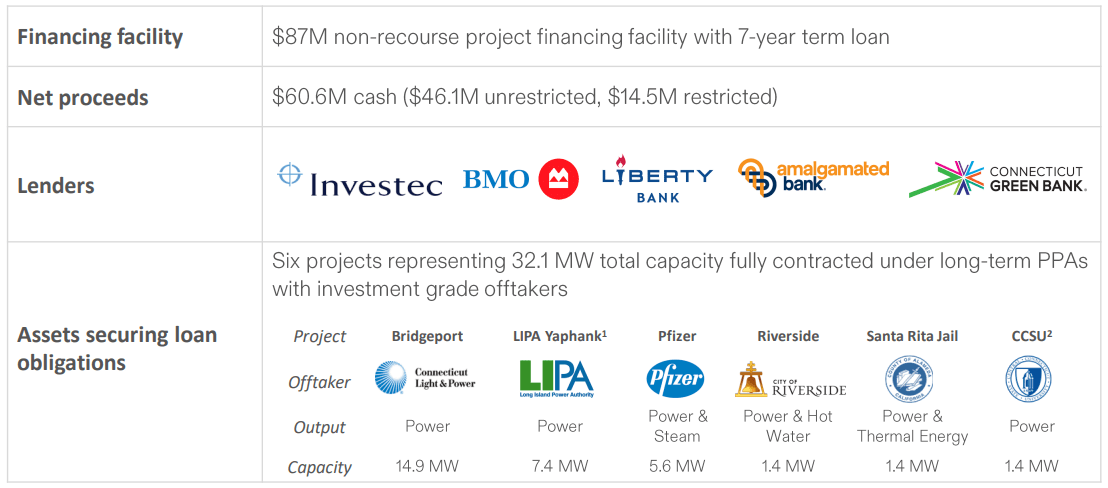

- Subsequent to quarter-end, the company managed to close on $87 million in non-recourse project financing with a consortium of lenders at competitive interest rates for net proceeds of $46.1 million.

- Three new projects are expected to commence commercial operations in the second half of the fiscal year.

- Considering the company's new ability to replenish cash reserves beyond open market sales and with investor risk appetite on the rise again in recent weeks, I am upgrading FuelCell Energy's common shares from "Sell" to "Hold".

Note: I have covered FuelCell Energy ( FCEL ) previously, so investors should view this as an update to my earlier articles on the company.

On Thursday, FuelCell Energy reported another set of disappointing quarterly results. While revenues came in substantially above consensus expectations, margins, profitability and cash flows continued to suffer:

{kind=link}

Regulatory Filings

Please note that reported top line outperformance was mostly a function of analysts' ongoing struggle to accurately model the level of fuel cell module exchanges at existing customer sites on a quarterly basis as these service revenues tend to be lumpy.

Not surprisingly, on the conference call management projected a lower level of module exchanges for the remainder of the fiscal year. As a result, I would expect analyst estimates for the second half of FY2023 to come down somewhat but considering the level of outperformance in Q2, full year revenue expectations of $135.8 million remain achievable.

Negative free cash flow of $62.1 million improved just slightly from the all-time high reached last quarter and resulted in unrestricted cash and short-term investments declining by approximately 17% quarter-over-quarter to $323.2 million.

During the quarter, FuelCell Energy sold approximately 0.9 million newly issued shares into the open market for gross proceeds of $2.9 million. As of April 30, 2023, approximately 75.6 million shares remained available for issuance under the company's Open Market Sale Agreement with a number of investment banks.

Subsequent to quarter-end, the company managed to close on $87 million in non-recourse project financing with a consortium of lenders at competitive interest rates:

{kind=link}

Company Presentation

After deducting funds utilized for the refinancing of existing project-related debt and $14.5 million required to fund performance reserves, the transaction increased FuelCell Energy's available liquidity by $46.1 million.

Quite frankly, I wasn't expecting the company to refinance the majority of the existing generation portfolio at favorable conditions anytime soon, if ever.

In fact, the facility was oversubscribed due to strong lender interest as disclosed by management on the conference call.

Suffice to say, the transaction bodes very well for the company's ability to refinance projects scheduled to come online over the next couple of quarters like the much-touted Toyota Tri-Generation project at the port of Long Beach, California and two projects in Derby, Connecticut.

Please note that the company recently managed to secure the renewable natural gas ("RNG") supply required by the project terms but this doesn't change the fact that management's failure to sign a RNG supply contract in a timely manner has resulted in the requirement to expense the majority of the project investments, rather than capitalizing them as explained in the company's quarterly report on Form 10-Q:

It was determined in the fourth quarter of fiscal year 2021 that a potential source of renewable natural gas (“RNG”) at favorable pricing was no longer sufficiently probable and that market pricing for RNG had significantly increased, resulting in the determination that the carrying value of the project asset was no longer recoverable. (...)

As this project is being constructed, only inventory components that can be redeployed for alternative use are being capitalized. The balance of costs incurred are being expensed as generation cost of revenues.

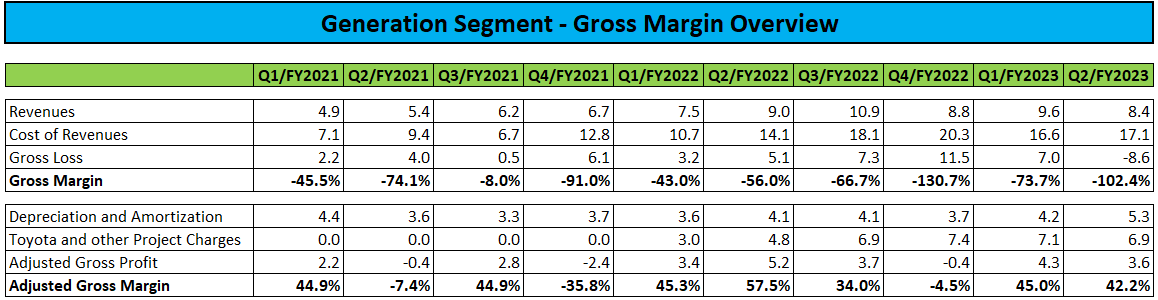

Not surprisingly, the issue has been a major drag on generation margins for some time already with $33.7 million in expenses related to the Toyota project having been recorded since Q1/FY2022:

{kind=link}

Regulatory Filings

FuelCell Energy's less-than-stellar project execution became evident again in the second quarter with the company required to recognize a $2.4 million impairment " of a project asset due to an anticipated power purchase agreement that was not awarded " without management providing specific details on the impacted project, even after being poked by an analyst on the issue during the questions-and-answers session of the conference call:

(...) So as we look at generation yes, we did have one impairment which came through generation related to an old development asset that the company chose not to move forward with.

As we think about generation margins going forward, one thing that has been coming through the P&L which has been a drag on generation margins as we've been expensing capital costs related to the Toyota project, I believe there's about 4.5 million coming through this quarter. Certainly, as Toyota comes online those costs will mitigate. What we target for our generation portfolio is EBITDA in the 40% to 50% range. So when you do the math and you essentially back out the charges for Toyota impairments as well as depreciation, we're in that range this quarter and for the fiscal year.

In absence of new project awards, FuelCell Energy's backlog is likely to fall below $1 billion next quarter with long-term generation backlog representing more than 90% of contracted revenues. Please note that the company's backlog will be recognized over a period of up to 20 years.

Company Presentation

In combination, FuelCell Energy's service and generation backlog had a weighted average term of approximately 17 years at quarter end.

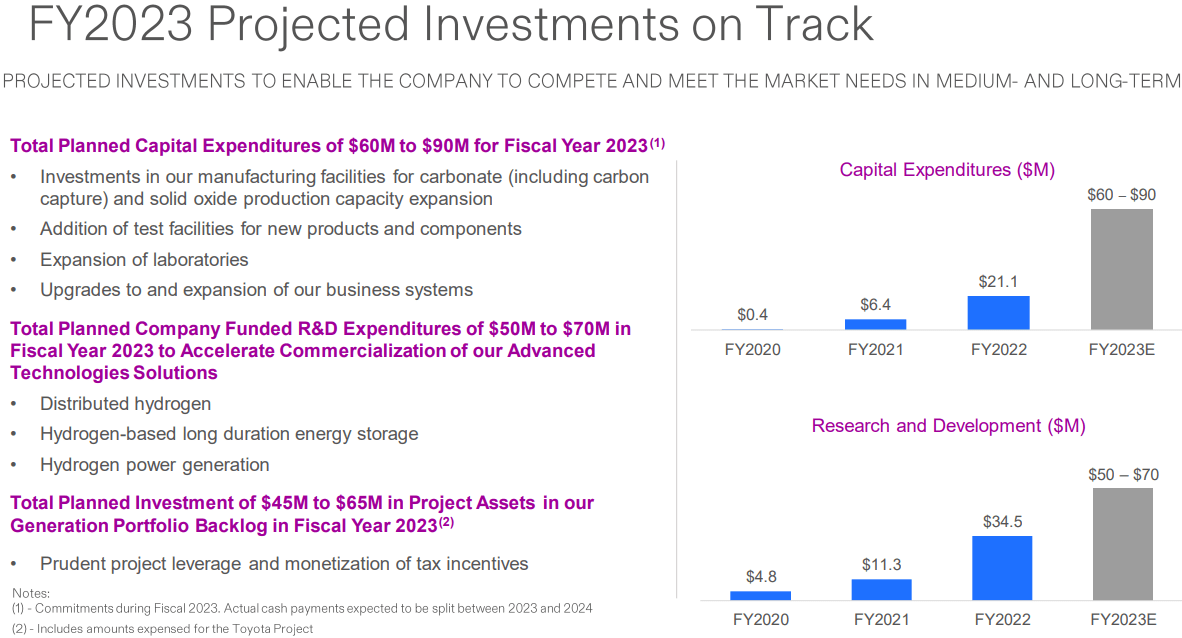

On the conference call, management reiterated expectations for capital expenditures, research and development expenses as well as investments in project assets for the fiscal year:

{kind=link}

Company Presentation

For the first half of FY2023, the company has reported capital expenditures of $16.9 million and investments in project assets of $19.8 million, thus leaving up to $120 million for the second half.

In combination with losses from operating activities, I would estimate negative free cash flow for the fiscal year of between $300 million and $350 million.

That said, considering the above-discussed project financing and plenty of availability under the company's Open Market Sale Agreement, I do not expect FuelCell Energy to run into renewed liquidity issues anytime soon, particularly not with an aggregate 19.1 MW in generation assets expected to commence commercial operations in the second half of the fiscal year.

At this point, I would estimate the company to raise at least $50 million in net proceeds from a refinancing of these projects in the first half of FY2024.

While management again touted potential benefits from last year's Inflation Reduction Act ("IRA"), investors should not expect any near-term revenue impact from potential IRA incentives as market participants are still waiting for additional guidance from the Treasury Department and the Internal Revenue Service.

In addition, product sales are likely to remain limited this fiscal year due to Korea Fuel Cell having abstained from ordering additional modules and the company still being in the process of rebuilding its Korean sales channel.

Bottom Line

FuelCell Energy reported another less-than-stellar quarter with a large top line beat more than offset by ongoing margin and profitability issues and cash burn hovering near all-time highs.

In addition, the company has committed to aggressive growth investments which in combination with anticipated losses from operations might result in negative free cash flow of up to $350 million this year.

As a result, investors better prepare for further utilization of open market share sales as a means to replenish the company's dwindling cash reserves.

That said, the recent $87 million non-recourse project financing was a positive surprise which bodes very well for the company's efforts to refinance projects scheduled to come online in the second half of the fiscal year at decent terms in the not-too-distant future.

Considering the company's new ability to replenish cash reserves beyond open market sales and with investor risk appetite on the rise again in recent weeks, I am upgrading FuelCell Energy's common shares from " Sell " to " Hold ".

Investors looking for a somewhat less risky investment in FuelCell Energy should consider taking a position in the company's Series B Preferred Shares ( OTCPK:FCELB ) which trade around 40% of face value despite ranking senior to common stock and paying a rather safe and juicy 12.5% cash dividend on an annualized basis.

For further details see:

FuelCell Energy: Cash Usage Still High, But Upgrading On Improved Refinancing Options