FUJIF - Fujifilm's Transformation Is Far From Over

2023-07-14 10:51:11 ET

Summary

- The Japanese corporation is staying true to its “Never Stop” spirit. Soon to be 90, it continues to change shape, all for the better.

- Its innovations have the most potential in healthcare and materials. Healthcare is the leading segment and will keep on taking market share.

- Shareholders will be rewarded for sticking around while FUJIFILM builds moats in healthcare and materials.

In 1934, newly founded FUJIFILM (FUJIY) had been charged with an important state task of creating a domestic capacity to produce photographic and motion-picture films. And in that, it excelled developing technologies for a good part of the last century and accumulating deep expertise in materials and imaging.

Even the demise of the corporation's core film industry in the early 2000s was apparently anticipated , which must be the reason why FUJIFILM was able to pivot, rather successfully, to related businesses: today, in addition to materials and imaging, it is a specialist in healthcare and life sciences.

In fact, FUJIFILM sees its services to pharma companies - as a contract development and manufacturing organization ((CDMO)) - powering major growth in the future and helping enlarge Healthcare division's share of business. FUJIFILM Diosynth Biotechnologies has been spending heavily on production, particularly biomanufacturing facilities for newer biologic drugs .

Diversification, away from film, has been driven by FUJIFILM's competitive strengths - areas where it could apply its existing technology. In 2006, when the corporate makeover was formally initiated, the company began selling cosmetics and supplements. Purposeful merger-and-acquisition activity included Toyama Chemical which marked an entry into pharmaceuticals in 2008. It picked up other businesses through partnerships: decades old Fuji Xerox rebranded just recently as FUJIFILM Business Innovation.

Business Innovation, mostly through office products, generates 29% of revenue in FUJIFILM, just behind Healthcare (32%), the leading segment. These are followed by Materials (24%) and Imaging (14%). Still, healthcare sales, however fruitful, are not what the leadership envisioned; the previous target was to reach ¥1t by 2018. The segment's revenue just broke the ¥900b mark in FY2022.

Annual review

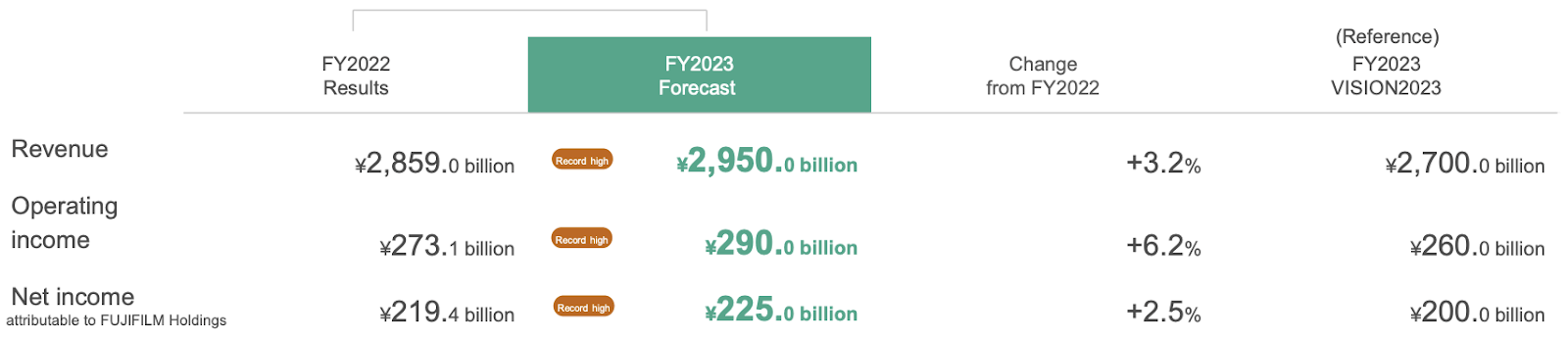

After nearly a decade of flat earnings performance, FUJIFILM appears to be finally livening up. FY2022 was the third consecutive year in which the company achieved increases in revenue, operating income and net income. The results were actually the highest since FY2007 for all three metrics; new highs are expected in FY2023 through low single-digit growth.

{kind=link}

{kind=link}

This meant that FUJIFILM was able to reach the targets set for FY2023 in VISION2023 ahead of time. (For perspective, the goals set by the earlier VISION2019 had not been met.) These record results are reflective of the management's more recent - under CEO Teiichi Goto - growth-oriented strategy, in already strong businesses like Electronic Materials as well as newer businesses with high potential like CDMO.

| Strategy | Segment | Area |

|---|---|---|

| Revenue | ||

| 21,534m | ||

| 30,713m | ||

| 4,730m | ||

| 6,642m | ||

| Operating margin | ||

| 9.55% | ||

| 9.41% | ||

| 9.20% | ||

| 19.51% | ||

| Cash from operations | ||

| 1,585m | ||

| 2,006m | ||

| 0.1m | ||

| 741.8m | ||

| Earnings per share | ||

| 4.12 | ||

| 1.80 | ||

| 0.94 | ||

| 0.85 |

Source: Company reports, Seeking Alpha

Canon's size is mainly explained by its dominance in printing which is almost three times bigger than FUJIFILM's Business Innovation. But this segment is also the most competitive, so the margins earned here are lower than in other businesses. The most profitable segments for all four companies are Imaging and Healthcare.

| Revenue (US$ b), 2022 |

| FUJIFILM |

| Canon |

| Nikon |

| Olympus |

| Imaging |

| 3.01 |

| 5.90 |

| 1.70 |

| - |

| Business Innovation |

| 6.16 |

| 16.63 |

| - |

| - |

| Healthcare |

| 6.75 |

| 3.77 |

| 0.73 |

| 6.39 |

| Materials |

| 5.10 |

| 2.42 |

| 2.21 |

| - |

Source: Company reports, Seeking Alpha

Naturally then, Olympus has an edge on margins; however, just size wise, FUJIFILM's healthcare unit is still larger. Like Olympus , FUJIFILM is aspiring to gain a proper foothold in the medical field. In contrast, both Canon and Nikon have a broader vision for the future, spreading resources across their product portfolios more or less evenly.

| Imaging | ||||

|---|---|---|---|---|

| 17.8% | ||||

| 15.7% | ||||

| 18.2% | ||||

| - | ||||

| Business Innovation | ||||

| 8.2% | ||||

| 9.3% | ||||

| - | ||||

| - | ||||

| Healthcare | ||||

| 11% | ||||

| 6% | ||||

| 11.5% | ||||

| 24% | ||||

| Materials | ||||

| 9.7% | ||||

| 17.6% | ||||

| 14% | ||||

| - | ||||

| Operating margin, 2022 | FUJIFILM | Canon | Nikon | Olympus |

Source: Company reports, Seeking Alpha

The main reason why FUJIFILM stands out is its intense focus on growth; meanwhile, the competitors are either reducing or sustaining their capital and R&D expenditure. Investments in healthcare are aimed at earning the company a dominant position in the space. The plan, although long-term in nature, looks likely to succeed. And that should give a boost to FUJIFILM's earning power.

| R&D and Capex (US$ m) |

| FUJIFILM |

| Canon |

| Nikon |

| Olympus |

| 2019 |

| 2,252 |

| 4,731 |

| 753 |

| 351.3 |

| 2020 |

| 2,277 |

| 4,232 |

| 683 |

| 349.1 |

| 2021 |

| 2,271 |

| 4,036 |

| 639 |

| 342.5 |

| 2022 |

| 3,642 |

| 3,772 |

| 683 |

| 358.3 |

Source: Company reports, Seeking Alpha

Valuation

FUJIFILM (TSE:4901) boasts an equity structure that maximizes shareholder value. It has one the lowest numbers of shares outstanding among TSE-listed peers which allows it to offer investors comparatively high earnings per share. The stock has also provided a high total return of over 150% for the past ten years (5 year: 97%).

FUJIFILM's valuation has historically varied within a small range. At 15.6x, P/E is almost at the same level as before the pandemic; it briefly passed 18x in September 2021. Within the industry, the stock is below Olympus (20x) but slightly above Canon (14.6x) and Nikon (14.1x). The analyst consensus puts the 12-month price forecast at ¥9.92k, about 20% over ¥8.21k per share as of 13 July.

Conclusion

It has been almost two decades since FUJIFILM began its corporate transformation. Its success ran counter to the failure of other big names in the film industry and belied the stereotype of an unwieldy Japanese corporation. Relying on its suite of fine technologies, FUJIFILM has opened itself up for critical tie-ups in order to capture the opportunities of inventive co-creation. Although risks of potential economic weakness and currency volatility remain constant, its latest growth-minded strategy focusing on Healthcare and Advanced Materials is promising. Shareholders, as long-time beneficiaries of reliable returns, will surely benefit.

For further details see:

Fujifilm's Transformation Is Far From Over