FJTSY - Fujitsu: Service Solutions Surge Challenges In Hardware Sales And Strong Growth From Uvance

2023-11-23 05:48:34 ET

Summary

- Fujitsu's Q2 financial results show strong performance in the Service Solutions segment, driven by increased demand for digital transformation and the success of Fujitsu Uvance.

- The Hardware Solutions segment saw a rebound in sales, but declining sales of network products impacted the segment's overall revenue.

- The Device Solutions segment experienced a decline in sales, while the Ubiquitous Solutions segment saw a slight sales reduction but improved operating margin.

Introduction

Fujitsu Limited (FJTSF), the Japanese multinational IT equipment and services company and one of the world's prominent IT services providers, released its latest financial results about three weeks ago. The company boasts a diverse portfolio of cutting-edge products and a comprehensive range of tech services. For effective oversight of business operations and to maximize cash flow and earnings, management reorganizes the company's business structure or segments from time to time, while setting new revenue and profit margin targets.

Fujitsu Segments (Fujitsu)

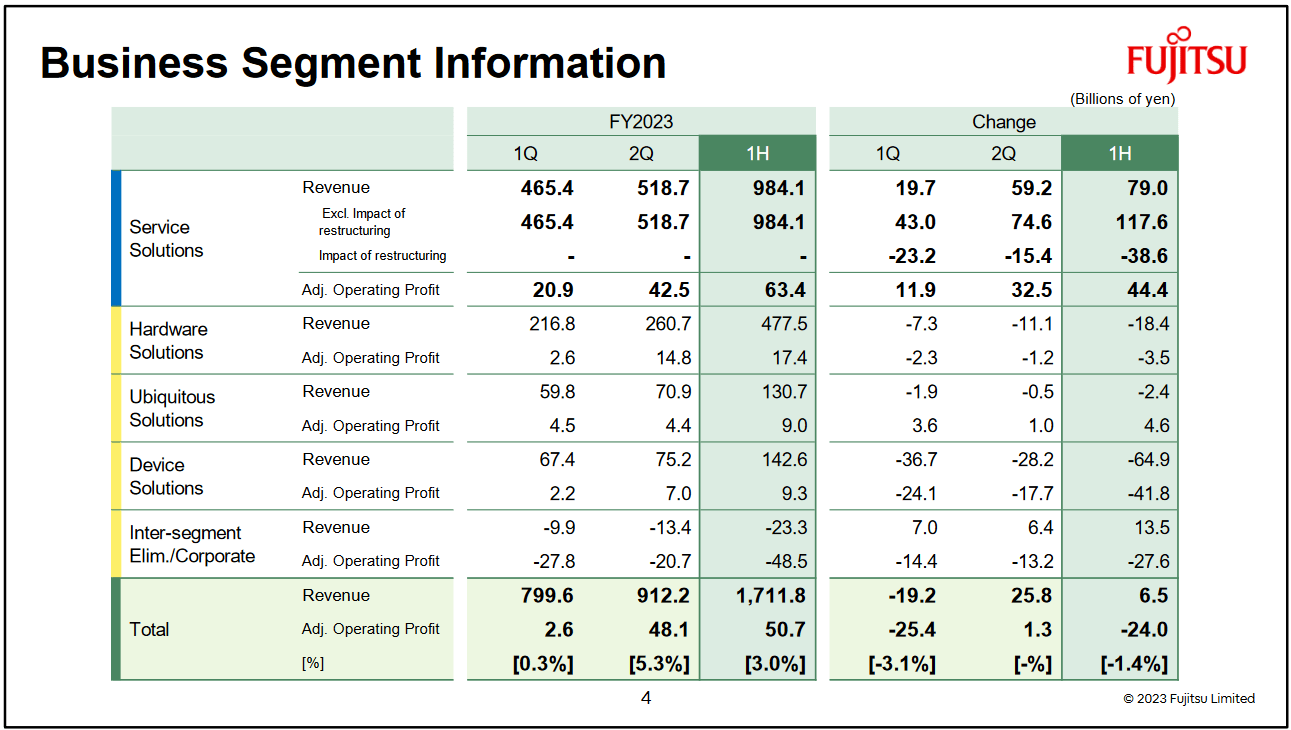

In Q2 this year, Fujitsu introduced some changes to its business segment, including the creation of new sub-segments. The changes to the business segments were made to help the company achieve its medium-term management plan, which includes financial plans. The company's main segments are Service Solutions, Hardware Solutions, Ubiquitous Solutions, and Device Solutions. The Service Solutions segment is currently the company's most important segment in terms of revenue generation.

In the previous Technology Solutions segment, the hardware sales and hardware maintenance services that had been a part of the Solutions & Services and International Regions Excluding Japan sub-segments are separated out to create the new Services Solutions segment.

- Fujitsu Press Release

A Look at the Latest Numbers

{kind=link}

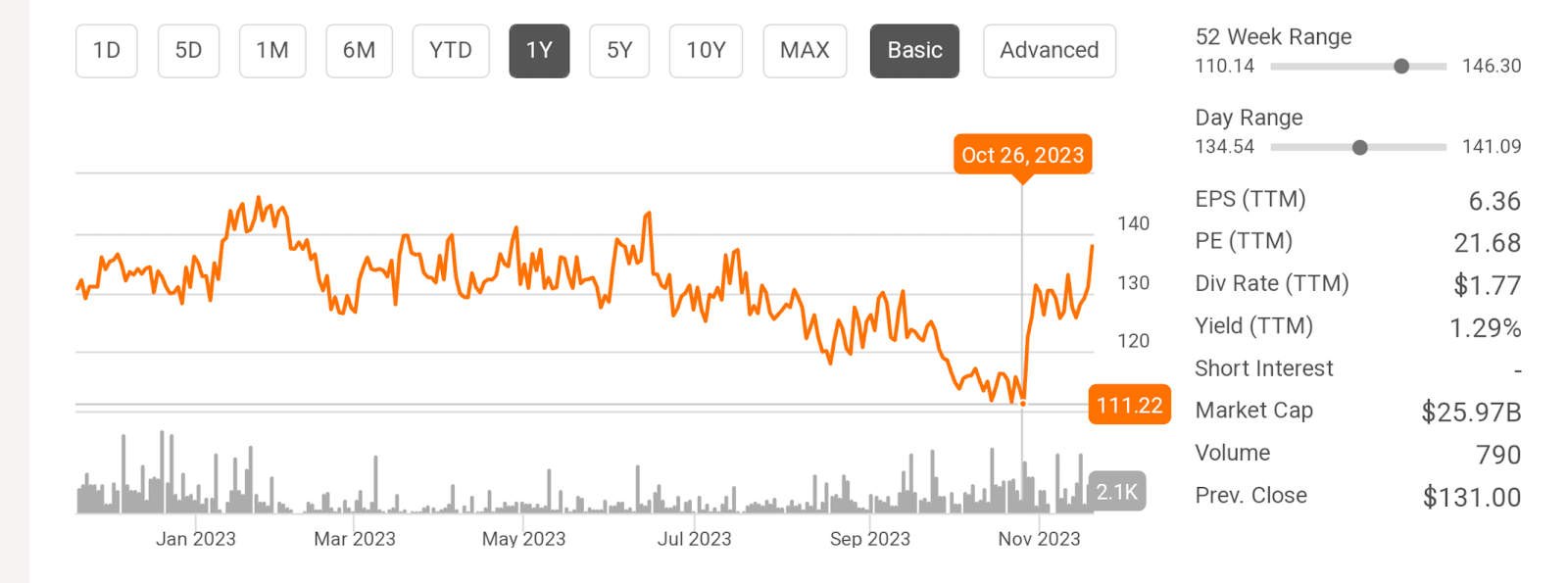

Fujitsu released Q2 FY23 financial results, alongside 1H FY23 consolidated financial results, on October 26. The market reaction was immediately positive. As seen in the chart above, the stock price has rallied about 24% since then. Here are some key highlights from the Q2 earnings call and consolidated financial results.

Service Solutions

{kind=link}

The Service Solutions segment remains the company's strongest and most important segment. The segment recorded revenue of ¥984.1 billion in 1H, which represents a 13.6% increase compared to 1H FY22. The performance in the Service Solution segment was influenced primarily by a robust need for digital transformation ((DX)) and modernization in Japan, especially in the public and healthcare sectors. About 58% or ¥571.1 billion of the total Service Solutions segment revenue for 1H was from the Japan region. International sales also held up well, increasing by about 9% compared to 1H FY22, and accounting for ¥288.4 billion or about 28% of the total 1H revenue in the segment. Revenue from international regions was mainly from Fujitsu's public sector customers in Europe.

As for our outlook for the second half, the level of our backlog of orders in Japan, including orders for fiscal 2024, is 12% higher than last year's level, so we believe the revenue trend in the second half will also be solid. Our profit target for Service Solutions is quite high, but we believe that we can fully achieve it.

- Q2 FY23 Earnings Call

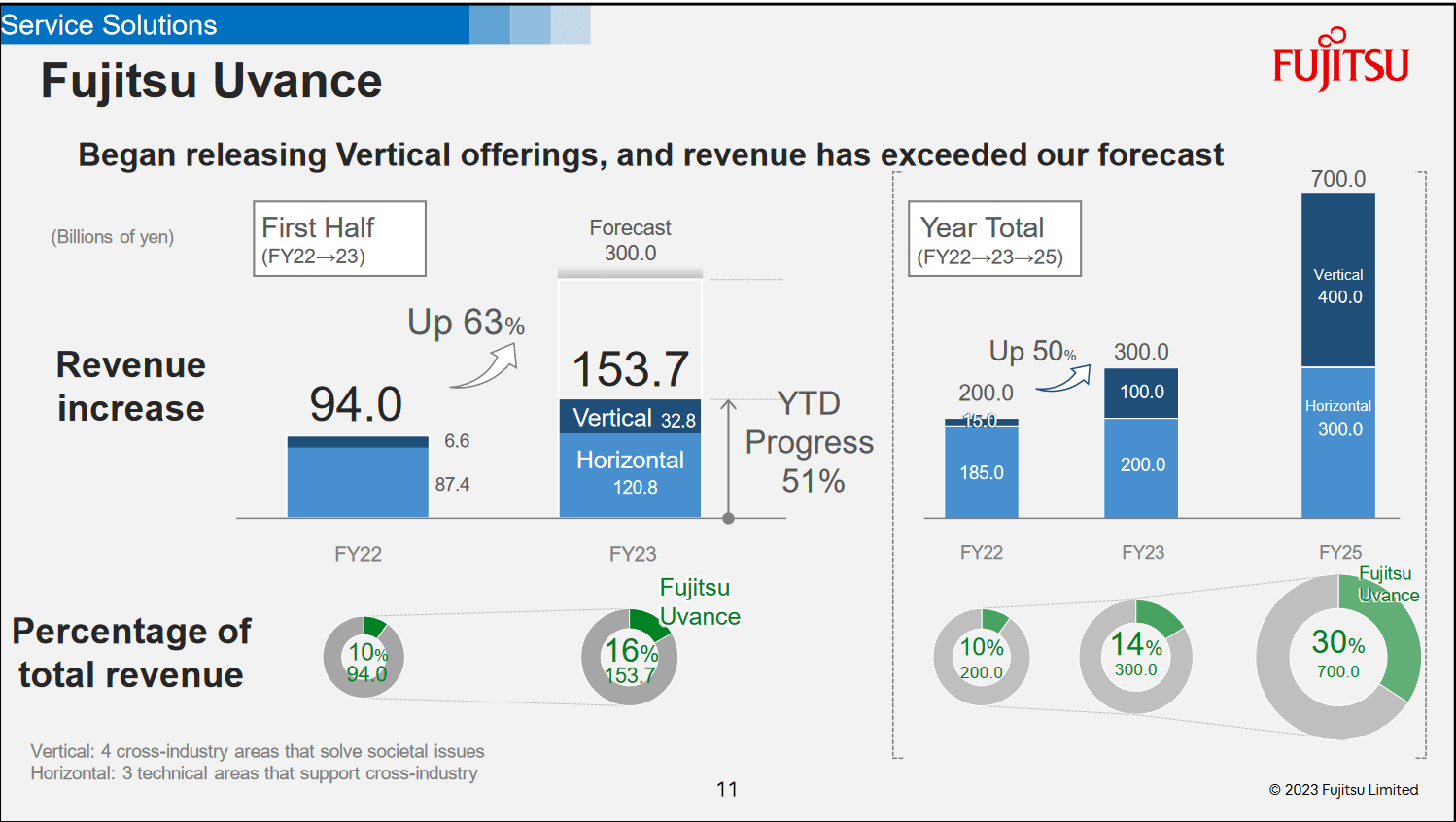

In September, Fujitsu became Japan's inaugural RISE with SAP (SAP) premium partner. Through the premium partnership, Fujitsu will be offering (through the arm of the company called Fujitsu Uvance) all-round cloud solutions and infrastructure, including cloud enterprise resource planning (ERP) solutions to support sustainable enterprise transformation in Japan. There has been a proactive stance by the Japanese government in supporting digital transformation as the country is said to surprisingly lag in digital transformation. Fujitsu is actively organizing itself to effectively seize the business opportunity presented. Fujitsu is fairly optimistic about future demands and growth in its Services Solutions segment. I believe that with the launch of RISE with SAP, there will be further enhancements to sales the company makes through Fujitsu Uvance, and the Service Solution segment will remain strong and be a continuous growth driver for the company's consolidated top line. Fujitsu Uvance was launched in 2021 as the company's business brand that will focus on providing both vertical and horizontal technology solutions to enterprises. In 1H FY23, Fujitsu Uvance saw a 63% increase in revenue. Fujitsu Uvance has become an important brand in the Services Solutions segment.

{kind=link}

Fujitsu Uvance is already beating growth expectations. From a ¥94 billion revenue in FY22 to ¥153 billion in 1H FY23. It is expected to generate ¥300 billion in revenue by the end of FY23. The vertical technology offerings of the Fujitsu Uvance brand are growing impressively so far. In FY22, revenue from the vertical offerings made up 7.5% of the brand's total revenue. In 1H this fiscal year, vertical offerings account for about 21% of the total revenue generated from Fujitsu Uvance. Forecast for FY25 shows that the brand is expected to generate up to ¥700 billion in revenue, of which vertical offerings will account for over 50%.

Enterprises are adopting vertical cloud solutions and it is an in-demand market right now. RISE with SAP offers vertical cloud solutions and services. This aligns with the burgeoning trend and presents a strategic opportunity for Fujitsu Uvance to capitalize on the demand for such solutions. I anticipate this to bolster the Service Solutions segment's top-line performance.

Breakdown by Quater (2Q FY2023 Consolidated Financial Results)

{kind=link}

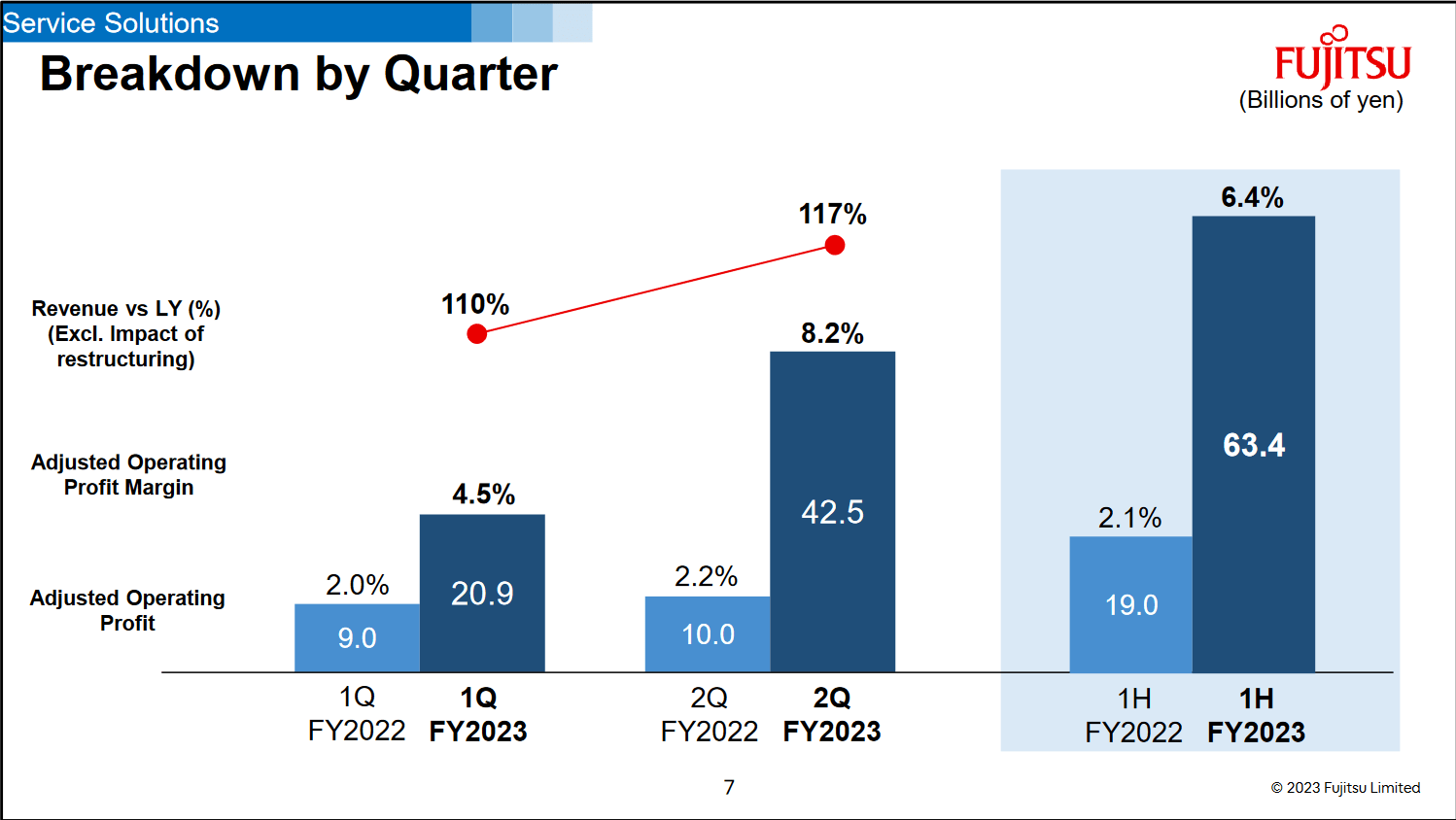

A quarterly breakdown of sales and profit margins for the Service Solutions segment shows an impressive performance in non-GAAP operating profit and operating profit margin alongside the top line. Note how adjusted operating profit and margin recorded a higher increase than the percentage increase in revenue between Q1 and Q2 FY23. While the Service Solutions revenue increased by 10.4% (from ¥464.4 billion in Q1 to ¥518.7 in Q2), operating profit improved by about 103% (from ¥20.9 billion in Q1 to ¥42.5 in Q2). In my view, what this signifies for Fujitsu is a noteworthy enhancement in the operational efficiency and profitability of the Service Solutions segment. The fact that the adjusted operating profit and margin increased at a higher rate than the revenue suggests that the company has managed its costs effectively or introduced measures to improve profitability. In the earnings call, Fujitsu management attributes this operating profit uptick to "improvements in service delivery methods, which has enhanced the profit margin."

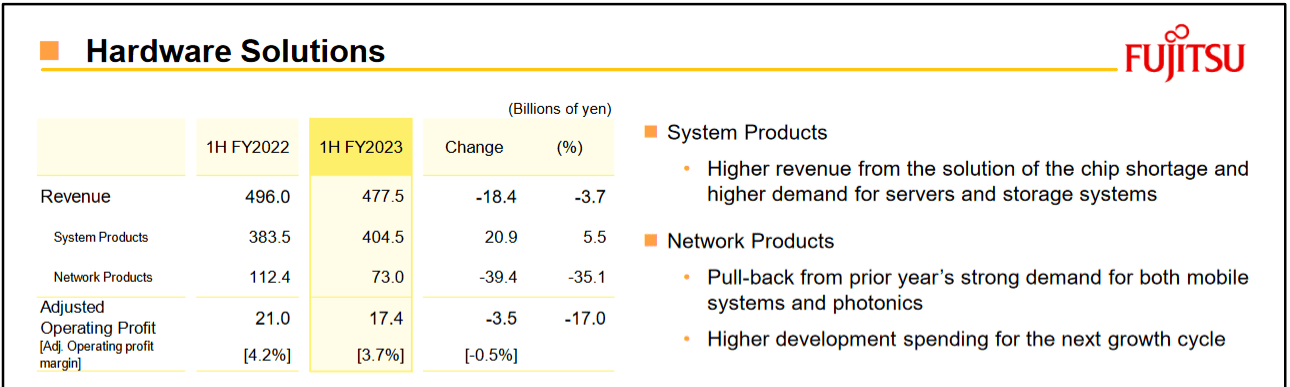

Hardware Solution

Hardware Solutions (2Q FY2023 Consolidated Financial Results)

{kind=link}

The Hardware Solutions segment recorded solid performance in Q2 because chip supply has improved and supply chain bottlenecks have improved lately, unlike in 2022, when companies faced procurement delays for components owing to the global chip shortage .

Sales in this segment have seen a rebound due to increasing demands for servers and storage systems. However, the total sales in the Hardware Solutions segment were impacted by declining sales of network products. Network products saw declining sales compared to the same period in FY22, and the management attributes this to "weakened demand for mobile systems and photonics network products in Japan and North America." Hardware Solutions segment revenue decreased by ¥18.4 billion or 3.7% compared to 1H FY22. Systems products saw increased sales from ¥383.5 billion in 1H FY22 to ¥404.5 billion in 1H FY23. Network products declined by a whopping 35.1%; hence, the consolidated revenue for the segment is impacted. The trend of poor sales of network products is expected to continue in 2H FY23 and guidance for the segment shows a lower revenue for FY23 compared to FY22. The operating profit margin for the Hardware Solutions segment is expected to drop by about 12% for FY23, according to management's guidance.

Other Segments

Performance in the other segments was not very encouraging. The Device Solutions segment saw decreased sales. Revenue for the segment was ¥142.6 billion, which is a 31.3% decline compared to 1H FY22.

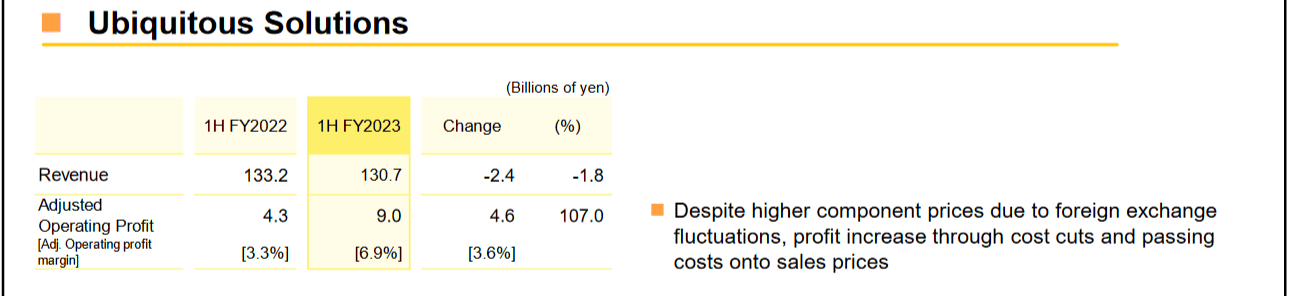

Ubiquitous Solutions (2Q FY2023 Consolidated Financial Results)

{kind=link}

The Ubiquitous Solutions segment (focused on the manufacture of smartphones and PCs through Shimane Fujitsu) saw a slight 1.8% reduction in sales. The operating margin was, however, impressive. Effective cost cuts on the production line have improved the margin of this segment.

Cash Flow and Valuation

{kind=link}

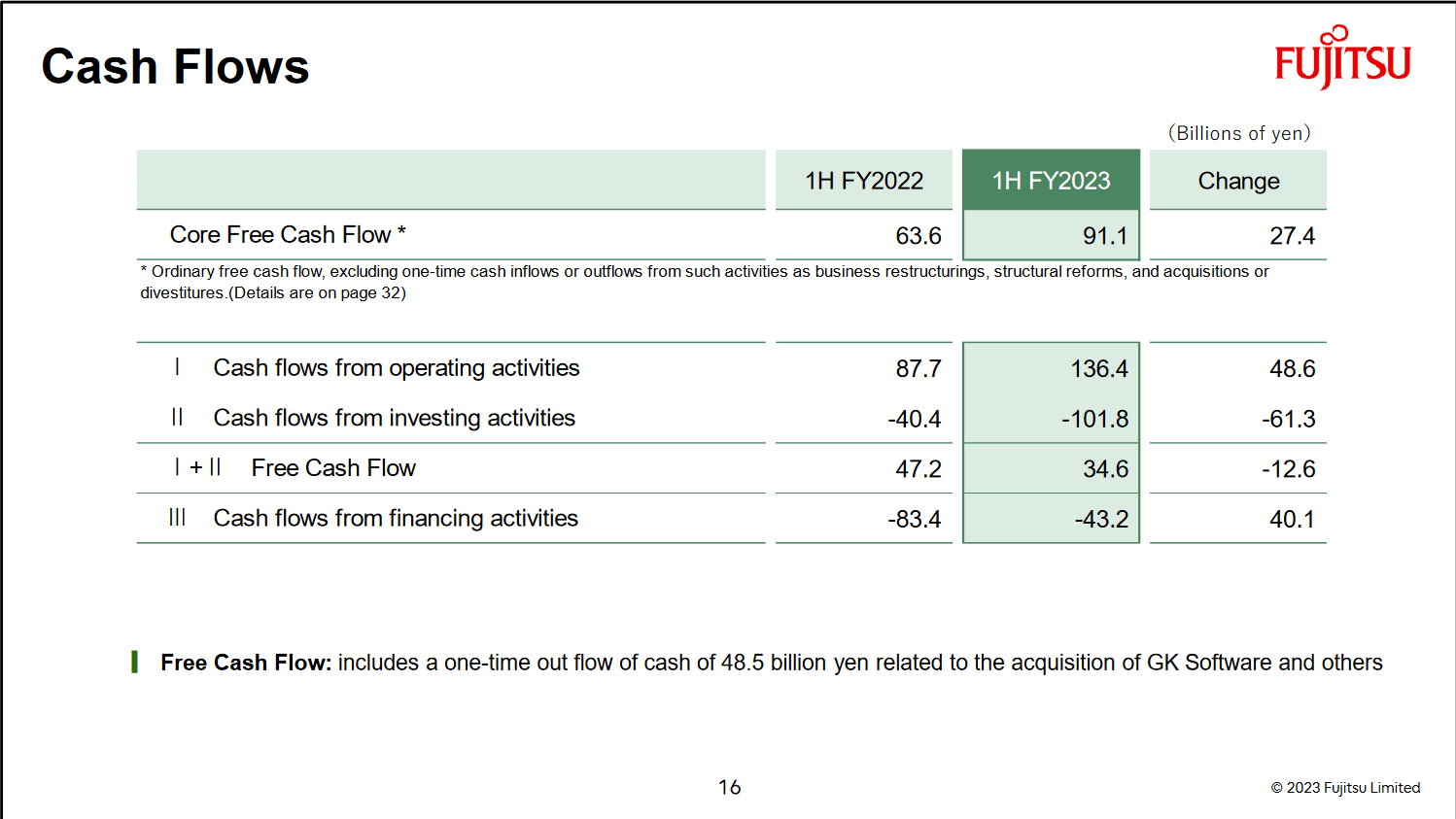

Cash from operating activities improved by ¥48.6 billion in 1H over the same period last fiscal year. Core free cash flow went up ¥27.4 billion, reaching $91.1 billion in 1H. This bodes well for Fujitsu and reflects the adept management of CapEx. With this ample amount of free cash flow, Fujitsu can strategically invest in Fujitsu Uvance's growth opportunities, and continue its occasional share buybacks which enhance shareholder value.

The strong top line makes Fujitsu's P/S ((TTM)) and EV/Sales ((TTM)) much lower than the IT sector median metrics, indicating undervaluation in terms of revenue. P/S ((TTM)) and EV/Sales ((TTM)) both have a value of 1.06x and are both about 60% lower than the sector median metrics. A 21.85x P/E GAAP ((TTM)), which is 14% lower than the sector median P/E, suggests that the stock is relatively inexpensive based on its current earnings. An EV/EBITDA ((TTM)) multiple of 9.97x, which is about 34% lower than the sector median value of 15.17x, shows that Fujitsu is doing pretty well in terms of operating performance and profitability in comparison to peers in the IT sector and is somewhat undervalued in this regard.

Takeaway

In summary, Fujitsu's Q2 financial results underscore the company's financial resilience and strategic prowess in a dynamic market. The Service Solutions segment remains a powerhouse, driven by increased demand for DX and the impressive performance of Fujitsu Uvance. I am optimistic about the prospects for Fujitsu Uvance, as global demand for vertical cloud technology continues to rise. I expect improvements in the sales and earnings for the Hardware Solutions and the Device Solutions segments. Operational improvements in all segments of the company will be strong catalysts for Fujitsu. For now, I think it is worth a "hold," while monitoring sales and operational improvements in all the segments of the company.

For further details see:

Fujitsu: Service Solutions Surge, Challenges In Hardware Sales, And Strong Growth From Uvance