FULC - Fulcrum Therapeutics: FSHD Steadily Advancing In Phase 3 Optionality With SCD

2023-05-24 14:15:54 ET

Summary

- Crisis of confidence in prior management (related to full clinical hold in February for FTX-6058 in SCD) led to currently cheap valuation.

- New CEO (appointed mid May) sold prior companies to Pfizer and Sobi.

- Primary endpoint for losmapimod in FSHD of RWS (reachable workspace) has been validated by the FDA, while prospect for effective oral pill in sickle cell disease offers investors significant optionality.

- Key risks include inability to reach agreement with FDA for SCD program (discontinuation) and phase 3 failure in FSHD.

- FULC is a speculative buy. This year we can expect completion of enrollment for FSHD phase 3 trial and regulatory update for SCD.

Shares of small molecule developer Fulcrum Therapeutics ( FULC ) have lost more than 80% of their value since the IPO was priced at $19 in August 2021. Year to date performance is negative 50% after FTX-6058 for sickle cell disease was placed on full clinical hold by the FDA in late February.

Interestingly enough, due to highly promising initial data, the share price hit a high of low-teens to start 2023, allowing the company to raise $125M at $13 per share before the bottom fell out. Crisis of confidence in leadership led to several top officers departing including prior CEO, CFO and Chief Medical Officer.

With new leadership at the helm, including the May 15 appointment of Alex Sapir as CEO (his prior two employers acquired by Pfizer (PFE) and Sobi), I think this left-for-dead rare disease player deserves a second look.

Chart

{kind=link}

FinViz

Figure 1: FULC weekly chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the daily chart above, we can see the share price rocket to the high teens on enthusiasm for updated data in SCD followed by a gap down with news of a full clinical hold by the FDA. After hitting a low of $2.25, a small rebound to mid-$3s has taken place but valuation still remains very depressed. My initial take is that readers interested in this name would do well to establish a partial position before it gets noticed.

Overview

Founded in 2015 with headquarters in Cambridge (89 employees), Fulcrum Therapeutics currently sports an enterprise value of negative ~$100M and Q1 cash position of $297M providing an operational runway into mid-2025.There are ~60M shares outstanding and accumulated deficit to date is $437M.

Fulcrum is focused on developing treatments for genetically defined rare diseases in areas of high unmet medical need, with losmapimod for FSHD (facioscapulohumeral muscular dystrophy) as its lead product candidate. Interestingly, this small molecule program was in-licensed from GSK (GSK) which treated over 3,500 patients across multiple indications (derisking the safety profile). It's worth pointing out that GSK ran studies in other indications (COPD, neuropathic pain, rheumatoid arthritis, etc) but never pursued FSHD or other muscular dystrophies ( 10-K filing ).

The second asset of note is FTX-6058 (hemoglobin or HbF inducer) for the treatment of SCD (sickle cell disease). FTX-6058 is designed to bind to EED and inhibit PRC2 (polycomb repressive complex 2), which per a 10-K filing leads to potent downregulation of key fetal globin repressors and causes an increase in HbF. The key concern here, as I alluded to briefly above, is that approved products in this class of medications (EZH2) have included in their labeling an increased risk of malignancies (the question being whether risk/benefit is optimal to treat this population of patients).

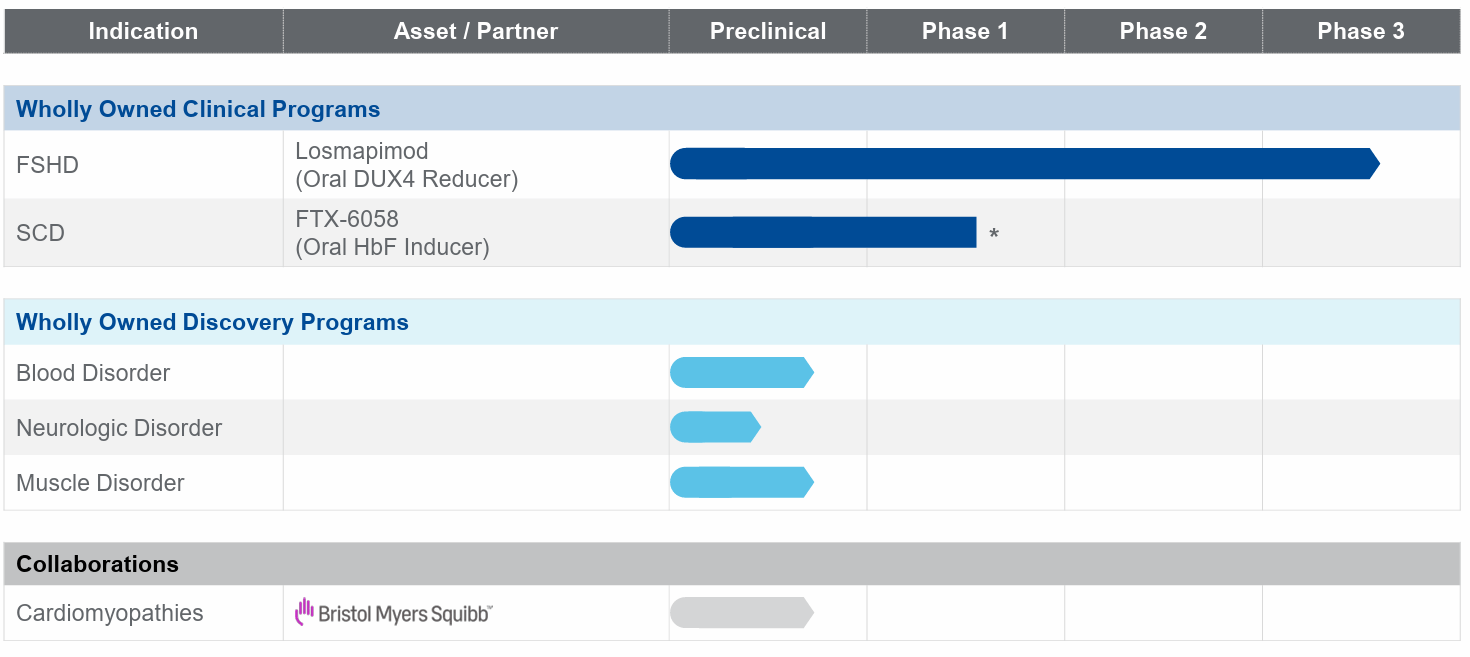

There are additional assets in preclinical across a variety of disease areas, the product of the company's proprietary FulcrumSeek product engine used to find and validate drug targets with potential to modulate gene expression to treat known root causes of such genetically defined diseases ( 10-K filing ).

{kind=link}

Corporate Slides

Figure 2: Pipeline (Source: corporate presentation )

Digging deeper into losmapimod in FSHD, this disease progresses to the point where patients become dependent on wheelchairs and lose ability to perform activities of daily living. Aberrant expression of DUX4 gene is known to be the root cause of the disease, and losmapimod selectively targets p38?/ß (which in turn reduces expression of DUX4 in muscle cells). Such an approach is far from perfect (in the 2030s will likely be replaced by RNAi or gene therapy modalities), but in the meantime should do well in the absence of competition if approved. Estimated patient population is 16,000 to 38,000 in the United States, but even chopping that in a third for the sake of being conservative and utilizing a $200k price tag results in $1B+ peak sales potential.

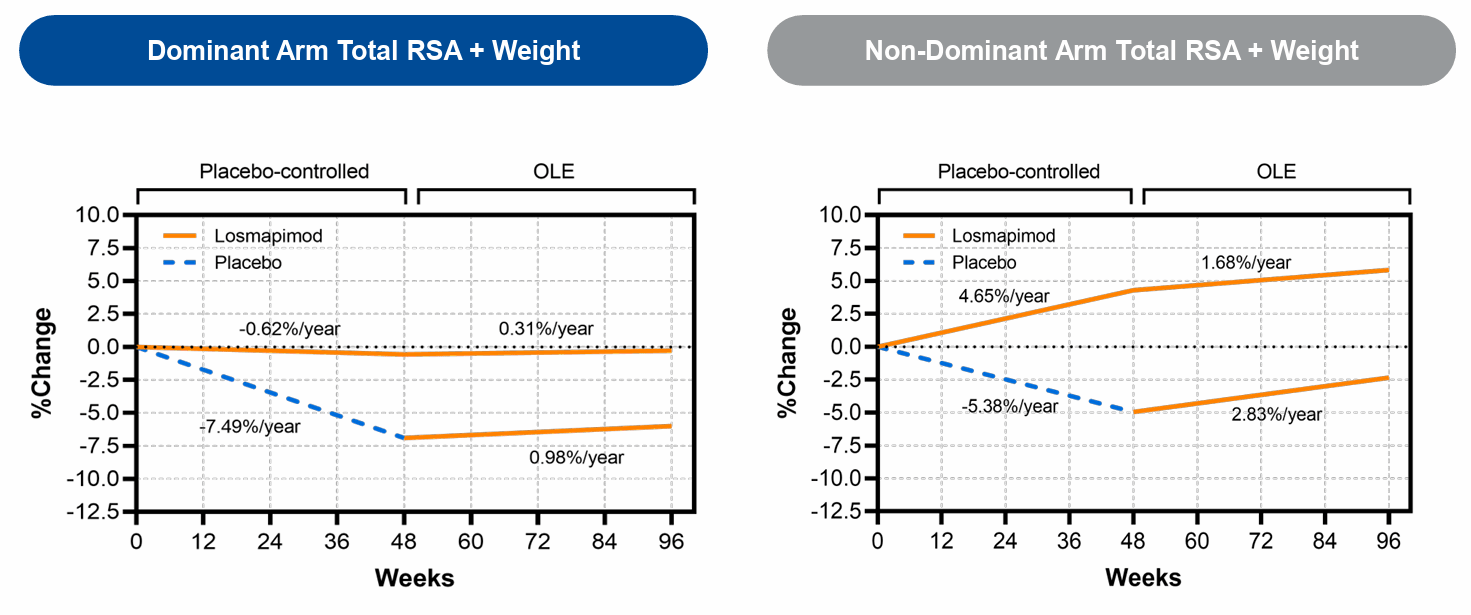

48-week data from the 80-patient phase 2b ReDUX4 study is supportive, with the caveat that primary endpoint was not met. Still, clinically relevant benefits (versus placebo) on multiple measures of muscle health and function as well as patient outcomes warranted moving into phase 3. Slower disease progression, preservation of normal appearing muscles and improved accessible surface area in RWS (reachable workspace) stood out to me (the latter being a key measure of independence).

{kind=link}

Corporate Slides

Figure 3: 96-week open label extension data shows maintenance of treatment effect (Source: corporate presentation)

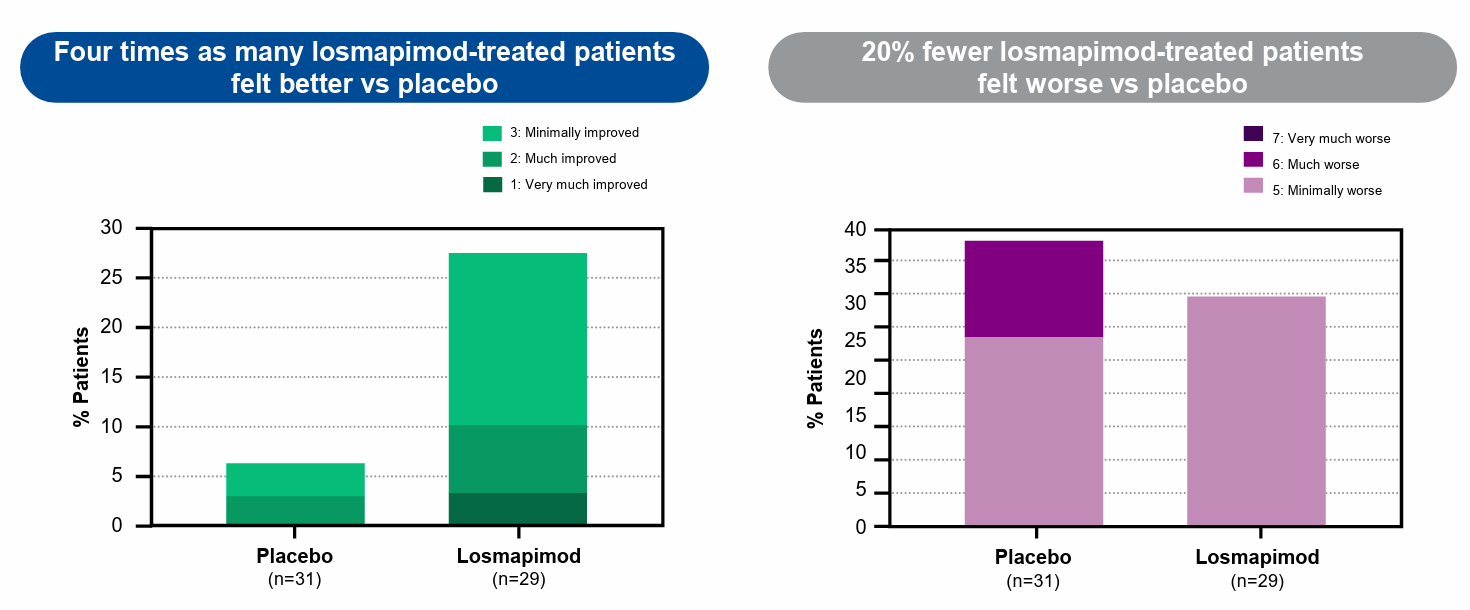

Patients feeling much better on treatment also supports the narrative of a successful launch (if phase 3 hits endpoints and is approved). This is an often overlooked measure that I keep a close eye on in regard to patient perspective, asking why they would want to take a treatment and stay on it (one reason I'm long Blueprint Medicines for Ayvakit launch in iSM).

{kind=link}

Corporate Slides

Figure 4: Patients' global impression of change or PGIC supports "sticky" profile of losmapimod (Source: corporate presentation )

One thing I like about the phase 3 REACH study (started in Q2 2022) is that from a regulatory standpoint there is a degree of derisking as the FDA agreed to using RWS (absolute change from baseline) as the primary endpoint. 230 patients are being randomized to placebo or losmapimod (15mg twice daily) over a 48-week treatment period with data expected in 2024. Secondary endpoints include MFI, PGIC, and Quality of Life in Neurological Disorders of the upper extremity (Neuro QoL UE) per 10-K.

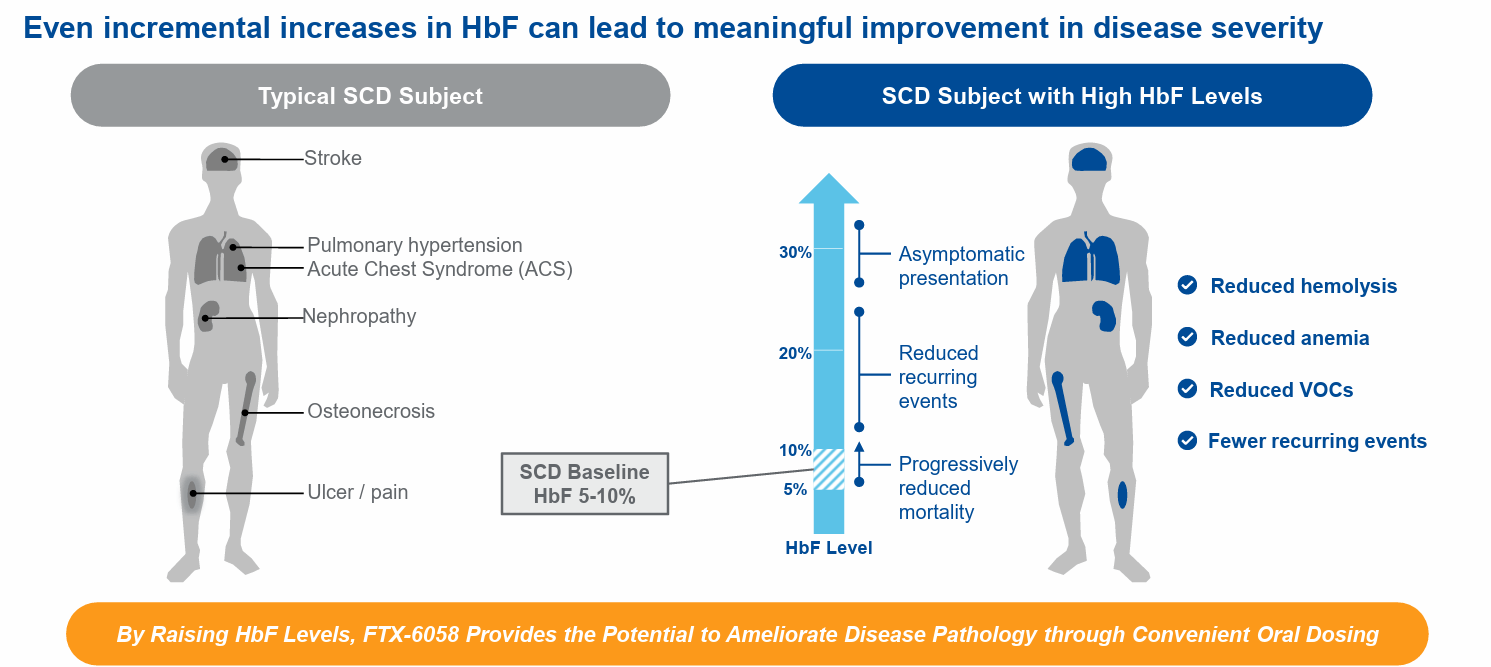

Moving on to FTX-6058 in SCD, market potential here is outsized with prevalence of 100,000 patients in the US and 50,000 in EU. Approved drugs manage and reduce VOC (vaso-occlusive crises) due to which patients end up in the hospital. Global Blood Therapeutics was bought out by Pfizer for $5.4B in August last year to gain control of voxelotor and earlier-stage SCD candidate in the pipeline. Hydroxyurea is considered to be standard of care to reduce frequency of painful crisis and reduce need for blood transfusions (10-K filing).

Phase 1b data for FTX-6058 was announced in January 2023 with no additional patients being enrolled due to full clinical hold. The plan had been to file IND separately for beta thalassemia, but this was withdrawn as Fulcrum works with the FDA to get the hold lifted in the near term (I still lack clarity here on if and when this will happen). Preclinical data showed that treatment with FTX-6058 increased HbF levels to 30% of total hemoglobin (essentially curative effect). No wonder the market got excited about this one including key healthcare hedge funds at the beginning of 2023, as such an approach would have a drastically different set of risks than a more exotic modality like gene therapy where long-term effects are still unknown.

{kind=link}

Corporate Slides

Figure 5: Higher HbF levels result in reduced symptoms in the 20% range, with 30%+ representing curative potential (Source: corporate presentation)

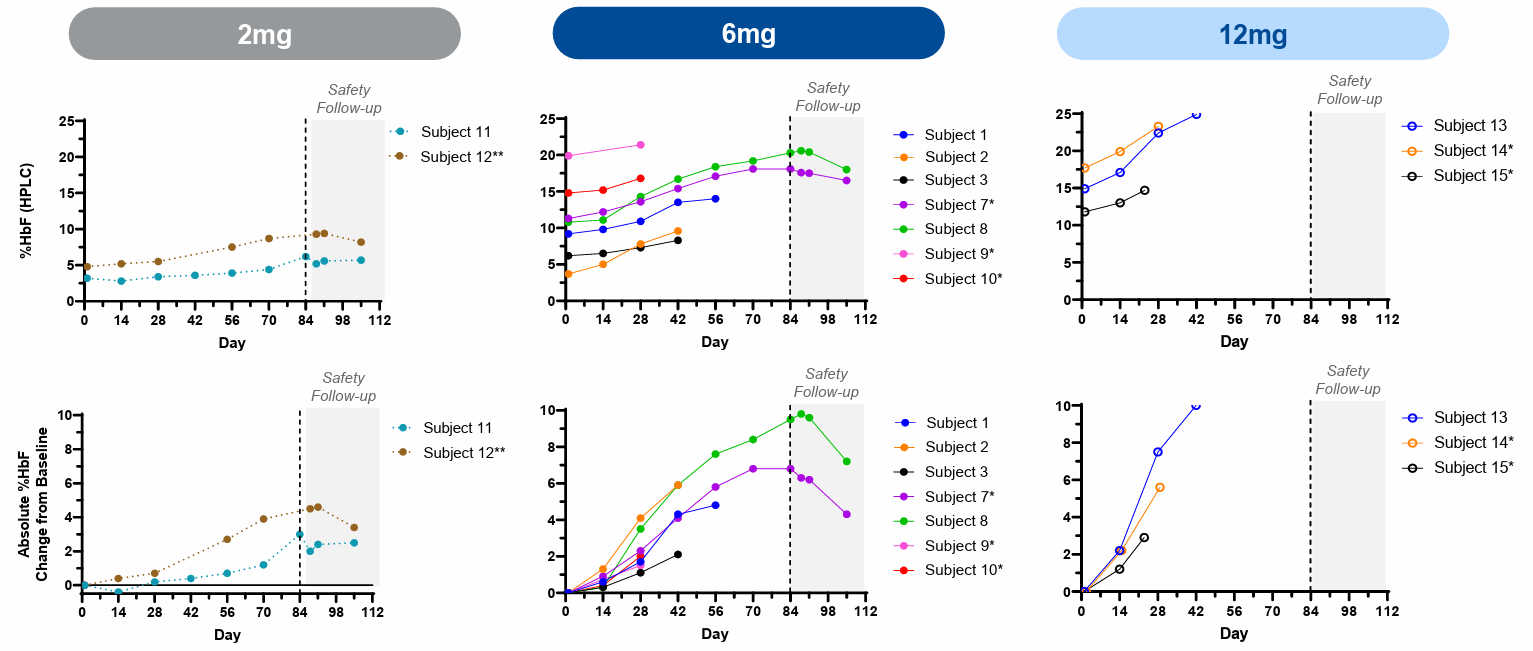

In humans, 6mg cohort data (10 patients) showed up to 9.5% absolute HbF increases from baseline with no difference in response for patients on or off background hydroxyurea (standard of care). Three patients in 12 mg cohort (prior to clinical hold) showed up to 10% absolute HbF increases from baseline after 42 days. I consider it a green flag that we can easily see a dose-dependent effect (along with beneficial impact on red cell distribution, decrease in bilirubin reflective of less hemolysis and reductions in reticulocytes indicative of healthier bone marrow function).

{kind=link}

Corporate Slides

Figure 6: Dose dependent increase in HbF (Source: corporate presentation)

Side effect profile to date has been relatively benign with 14 treatment emergent adverse events (TEAEs) reported to date of which two (headache, lip numbness) were deemed possibly related to study drug and non-serious. Acute chest syndrome (serious event) was considered not to be related to FTX-6058. In the 10-K filing, the company notes that they "are not certain when we will be able to resume the phase 1b trial, if at all." So, the worst case scenario is that they do not come to agreement with the FDA on risk/benefit profile and this program gets nixed.

Other Information

For Q1 2023, the company reported cash and equivalents of $297M comparing favorably to net loss of $25M (operational runway into mid 2025). G&A expenses rose slightly to $11.5M, while research and development costs decreased to $16.7M. The company reiterated that the phase 3 REACH trial in FSHD will complete enrollment 2H 23 ( clinical trials gov website shows October 2024 primary completion date).

On the conference call , more clarity was provided on clinical hold for FTX-6058 (related to preclinical data submitted in April, October and December of last year as well as nonclinical and clinical evidence of hematologic malignancies observed with other PRC2 inhibitors). FDA wants Fulcrum to further define the population or benefit of treatment with an emphasis on how it outweighs potential risk (the "good" news is that the hold is not related to any findings from the phase 1b study). Language sounds like the company is not giving up and remains convinced that FTX-6058 offers favorable risk/benefit (whether they can convince the FDA remains to be seen). On Q&A, prior interim CEO Robert Gould highlighted two outstanding issues including reversibility of gene expression changes (preclinical, non-toxicology studies are underway and it's a matter of waiting for results to discuss with the FDA, so this could take some time). To that last point, an analyst asks if this is a 2024 event and Gould was unable to provide clarity other than noting that current guidance is for rapid resolution of that timeline.

Another topic of central importance is defining patient populations that can most benefit from the elevation of HbF they're seeing (seems like FDA is pushing for a higher risk population than was being evaluated previously). Management contends that gene and cell therapies have their own unique challenges including potential safety risks as well. A related question is whether the 10% absolute induction bar for HbF is still relevant in a higher risk population and interim Chief Medical Officer Iain Fraser states they don't see themselves as going up against gene therapy and gene editing - getting patients into the 20% to 30% range is associated with clinical benefit for either genetic or pharmacological approaches and closer to 30% is associated with functional cure (sounds like they could move up potentially beyond the 12mg dose to achieve maximal benefit).

As for competition in FSHD, I'm aware that Arrowhead Pharmaceuticals ( ARWR ) has a promising preclinical candidate that could get partnered in the near term (RNAi has yet to make inroads in muscle). Avidity Biosciences ( RNA ) has an AOC (antibody oligonucleotide conjugate) program in phase 1, but serious adverse event (essentially a stroke) has already been observed in a DM1 patient treated with AOC1001 and this could be platform-related. I think that FSHD could be primed for a gene therapy approach, but this would not replace losmapimod until the 2030s, in my opinion.

As for institutional investors of note , Adage Capital Partners recently increased its position to over 5% of the company and RA Capital owns an ~18% stake. RTW Investments owns ~9% of the company and Suvretta Capital Management increased its stake to 5.1M shares. However, insider sales over the past year do not inspire confidence. I do see that RA Capital's recent purchases were in the $5 to $13 range (significantly underwater on its position).

As for relevant leadership experience, with the lineup currently being refreshed it's encouraging that recently-appointed CEO Alex Sapir served prior as CEO of ReViral (sold to Pfizer for up to $525M) and same role at Dova Pharmaceuticals (acquired by Sobi in $915M deal). High turnover in 2022 (multiple CSOs, CMO, VP Finance, President R&D, CEO role) not to mention after the clinical hold debacle is a red flag to my eyes.

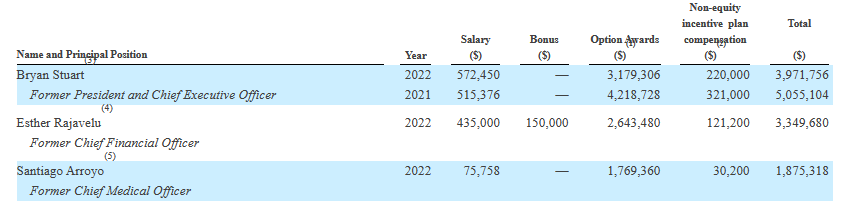

Moving on to executive compensation, cash portion of salary for former CEO Bryan Stuart is reasonable (in the range of similar companies I've covered) but the level of options awards appears outsized.

{kind=link}

Proxy Filing

Figure 7: Executive compensation table (Source: proxy filing )

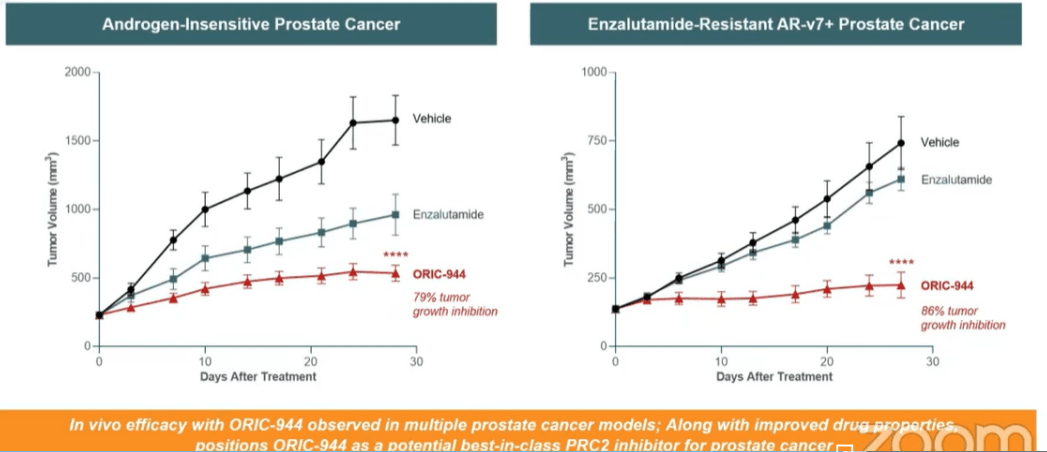

Moving onto useful nuggets from members of the ROTY community, back in February it was pointed out that ORIC Pharmaceuticals ( ORIC ) has its own PRC2 inhibitor (global rights licensed from Mirati Therapeutics) in development initially for prostate cancer. Preclinical data showed greater potency than enzalutamide and initial data update from phase 1b study is expected 2H 23. If especially promising, perhaps Fulcrum could receive a sympathy bump in valuation as well. Similarly, if Fulcrum's FTX-6058 gets back on track in the clinic in SCD, ORIC stands to benefit (could out-license this indication for significant economics while retaining rights in oncology).

{kind=link}

ORIC Corporate Slides

Figure 8: Strong single agent activity observed for ORIC-944, significantly better than blockbuster drug enzalutamide (Source: Wainwright presentation )

Delving further into the cancer risk that concerned the FDA, see tazmetostat approval document from the FDA which cites "known serious risk of acute myeloid leukemia, myelodysplastic syndrome, T lymphoblastic lymphoma, and other secondary malignancies." For further context, as for adverse events it was noted that second primary malignancy was the most common reason for treatment discontinuation (2% of patients). Keep in mind however that targeting PRC2 could carry specific advantages over EZH2 including overcoming resistance mutations.

As for IP, losmapimod appears to have a lengthy runway with patent covering use for treatment of FSHD expiring in 2038. Additional provisional or pending applications are expected to expire between 2038 to 2043. On the con side, keep in mind that composition of matter (licensed from GSK) has expired. For FTX-6058, two issued US patents directed to composition of matter are expected to expire in 2040 (per 10-K).

As for other useful nuggets from the 10-K filing (you should always scan these because investors may not get the complete picture from press releases), GSK agreement for losmapimod was inked in 2019 and resulted in issuance of 12.5M Series B preferred stock at that time (GSK still owns 1.7M common shares I believe). Fulcrum remains on the hook for up to $37.5M in development and regulatory milestone payments as well as royalties in mid-single to low double-digit range. MyoKardia drug discovery agreement was inked in July 2020 for which Fulcrum could receive up to $298M in milestone payments plus mid-single to low double-digit royalties on sales of net products resulting from collaboration. As a caveat, Fulcrum has no manufacturing facilities (lack of internal control and relying on contract manufacturing organizations could result in supply bottlenecks or disruptions).

Final Thoughts

To conclude, with negative $100M enterprise valuation, I think that pessimism is excessive and it would take very little to move the needle here. Losmapimod in FSHD, while far from a cure and leaving much to be desired, would still represent a significant advance for this sizeable patient population for which nothing is approved. From regulatory standpoint, the phase 3 study seems somewhat derisked given FDA's green light for the RWS (reachable workspace) endpoint. As for FTX-6058 in SCD, the prospect of an oral pill that provides a shot at functional cure or at least high enough HbF levels to substantially reduce symptoms would seem quite valuable to my eyes. The risk here again is on the regulatory side (if the FDA allows them to move forward) and clinical (if malignancy risk is a real issue or overblown).

For readers who are interested in the story and have done their due diligence, FULC is a Speculative Buy at current levels. Given the speculative nature of the company, I remind readers that a lower portfolio weighting is warranted. As an example, if one owns 3% portfolio weighting and the stock triples or more with clearing of FDA hold or further data updates (or phase 3 win for FSHD), the benefit to the portfolio is substantial. Conversely, from a risk perspective, it the stock ends up being a zero (FTX-6058 is DOA and phase 3 FSHD study fails), the overall fallout to the portfolio would be limited to a manageable level.

While dilution in the near term is not a concern given the strong balance sheet, key risks include the FDA not lifting the clinical hold for FTX-6058 and deciding that risk/benefit profile of the drug candidate is not appropriate in SCD. Similarly, phase 3 FSHD study could fail primary endpoint or even if it barely achieves the desired result, overall data package could be less than compelling which could result in a failed (or subpar) launch effort. Competition in FHSD is highly likely to overtake losmapimod in the long term whether from an RNAi, gene therapy or other modality (though the good news is these are quite a few years behind in the clinic. Roche's R07204239 (anti myostatin antibody) also is in phase 2.

As for ROTY's clinical stage portfolio, I continue to weigh risk/reward profile of the company for potential inclusion at some point in the near to medium term. Playing devil's advocate, it might be too speculative for us as I typically require a high degree of derisking and often prefer a more validated drug discovery platform (capable of generating additional high-value assets to move into the clinic).

Author's Note: I greatly appreciate you taking the time to read my work and hope you found it useful. While I post research on many companies that interest me, in ROTY (clinical stage) and Core Biotech (commercial stage) portfolios I own just 15 or fewer names in order to focus on stories that are highest conviction for me.

Disclaimer: Commentary presented is NOT individualized investment advice. Opinions offered here are NOT personalized recommendations. Readers are expected to do their own due diligence or consult an investment professional if needed prior to making trades. Strategies discussed should not be mistaken for recommendations, and past performance may not be indicative of future results. Although I do my best to present factual research, I do not in any way guarantee the accuracy of the information I post. I reserve the right to make investment decisions on behalf of myself and affiliates regarding any security without notification except where it is required by law. Keep in mind that any opinion or position disclosed on this platform is subject to change at any moment as the thesis evolves. Investing in common stock can result in partial or total loss of capital. In other words, readers are expected to form their own trading plan, do their own research and take responsibility for their own actions. If they are not able or willing to do so, better to buy index funds or find a thoroughly vetted fee-only financial advisor to handle your account.

For further details see:

Fulcrum Therapeutics: FSHD Steadily Advancing In Phase 3, Optionality With SCD