FULT - Fulton Financial: First Quarter Suggests Headwinds Ahead

2023-04-25 17:39:48 ET

Summary

- Fulton Financial Corporation's first-quarter results fell short of expectations, and the market dynamic points to a difficult time ahead.

- The significant drop in earnings could negatively impact its share price and dividend growth in the coming quarters.

- Fulton's share price decline does not represent a buying opportunity.

Shares of Fulton Financial Corporation ( FULT ) fell after the company reported first-quarter results that fell far short of expectations and were significantly lower than the previous quarter. It appears that the plan to capitalize on the recent share price drop may not work for dip buyers and dividend investors because Fulton's bleak outlook is unlikely to provide support for a price rebound and dividend growth.

Two Big Challenges

Following the failure of several regional banks, the primary challenge for the industry is to maintain deposit levels and lower credit losses. However, this appears challenging because high interest rates may continue to push individuals to invest in money market funds and other instruments. At the same time, higher lending costs and slowing economic growth may increase the risk of higher credit losses.

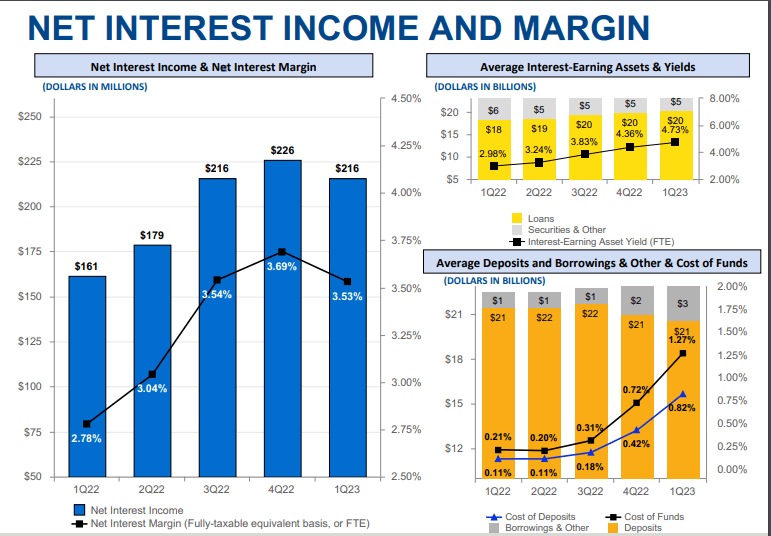

In the case of Fulton, these two negative factors have strongly impacted its earnings potential. The bank reported earnings per share of $0.39 for the first quarter of 2023, a 17.1% decrease from $0.48 per share in the fourth quarter of 2022. The bank blames a shift in the funding mix and higher credit losses for lower earnings. Its total deposits increased by $667 million during the quarter due to the addition of brokerage and other high-cost deposits, but its non-interest-bearing balances decreased by about $600 million. As a result, its total cost of deposits increased by 40 basis points to 82 basis points during the quarter, neutralizing the effect of higher interest rates on lending. Its total net interest income fell by $10.3 million compared to the fourth quarter of 2022, while the net interest margin fell by 16 basis points.

1st-Quarter-Earnings-Presentation (Seeking Alpha)

{kind=link}

In the first quarter, the bank increased the deposit rates for a number of products along with introducing new products, but a looming recession, additional Fed fund rate increases, and weak end markets may force the bank to offer even higher interest rates to entice individuals and institutions. The company projects that by the end of 2023, its total deposit beta will have increased from the current 16% to 32%. A higher deposit beta is a bad sign because it denotes lower margins and higher interest costs.

1st-Quarter-Earnings-Presentation (Seeking Alpha)

{kind=link}

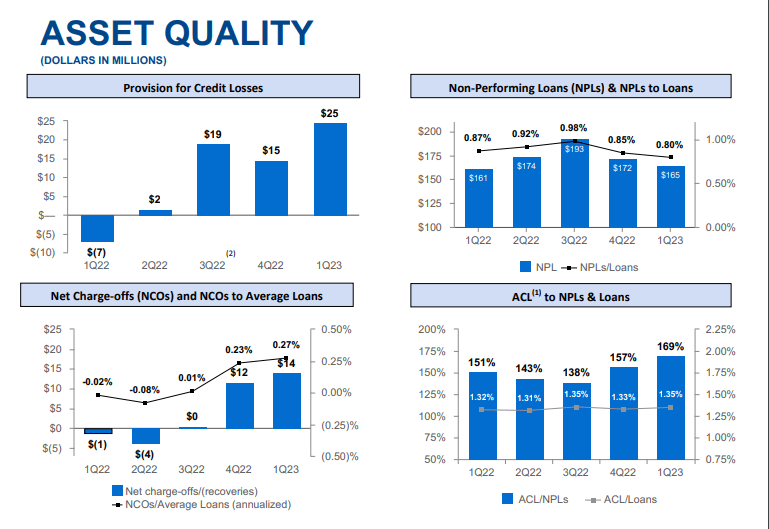

Another factor contributing to earnings declines is a significantly higher provision for credit losses. The company reported $25 million in credit losses in the first quarter of 2023, up from $15 million in the previous quarter. Fulton is not alone in having a deteriorating financial situation. A large number of regional banks , including Bank OZK ( OZK ) and Western Alliance Bancorporation (WAL), increased their credit loss provisions significantly in comparison to the fourth quarter of 2022. This trend is likely to continue in the coming quarters as regional banks, including Fulton, focus on customers in the hard-hit technology and real estate sectors. In the first quarter release, Fulton anticipated a provision for credit losses above $70 million for 2023.

1st-Quarter-Earnings-Presentation (Seeking Alpha)

{kind=link}

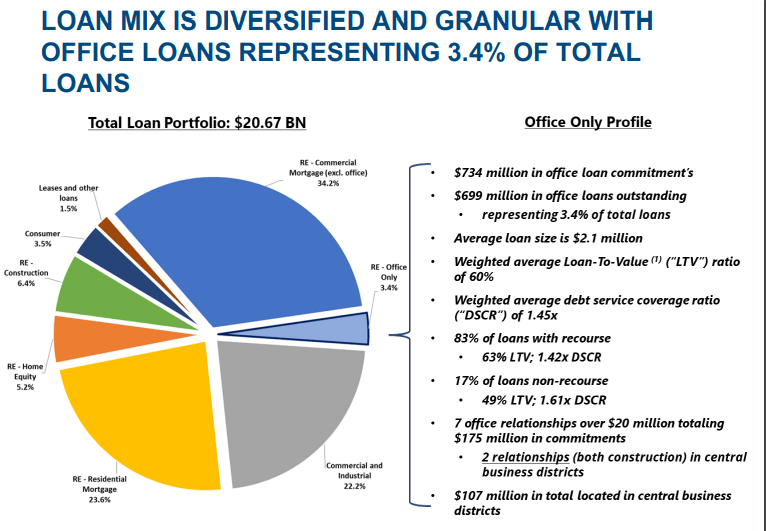

Fulton's loan portfolio is solely focused on the troubled real estate sector. In my opinion, the fundamentals of the real estate sector will deteriorate further in the coming quarters. Aside from higher borrowing costs and an impending recession, other factors have also contributed to the real estate sector's weakening fundamentals. For example, according to Moody's report , the rise in work-from-home opportunities is causing office tower revenue to decline to the point of default. At present, about 3.4% of Fulton's total portfolio is made up of office lending. Furthermore, the high supply of new homes continues to have an impact on apartment rental rates. According to RealPage data , the largest influx of brand-new houses in nearly 40 years will enter the market in 2023.

Wall Street analysts revised their earnings projections for Fulton after the first-quarter results. According to Seeking Alpha data , eight analysts have reduced their earnings projections for the bank, giving the company a C quant grade on earnings revisions. Fulton is expected to earn around $1.67 per share in 2023, a significant decrease from its 2022 median earnings of $1.79 per share. Analysts predict that earnings will fall to $1.65 per share in 2024. These estimates could fall even further if the US economy enters a severe recession and credit conditions worsen in the coming quarters.

Investment Analysis

Fulton's Share Price (Seeking Alpha)

{kind=link}

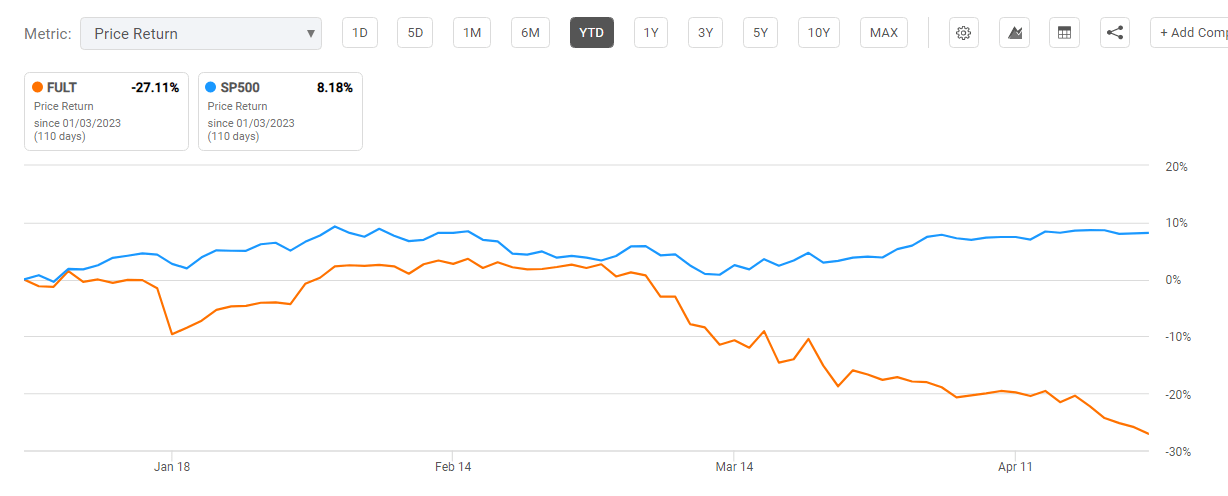

Buying when others are scared is one of the best strategies, but it is risky and requires a thorough understanding of future trends. Investors cannot achieve their objective of generating impressive returns in the short to medium term by purchasing a stock with weak fundamentals. Fulton's stock has lost more than 27% of its value since the beginning of the year. In the short- to mid-term, there is little chance of a solid recovery for Fulton's stock because price drivers like income and earnings growth are likely to worsen in the coming quarters. The overall market dynamics also do not look promising given the possibility of a recession, tight monetary policy, and high inflation.

{kind=link}

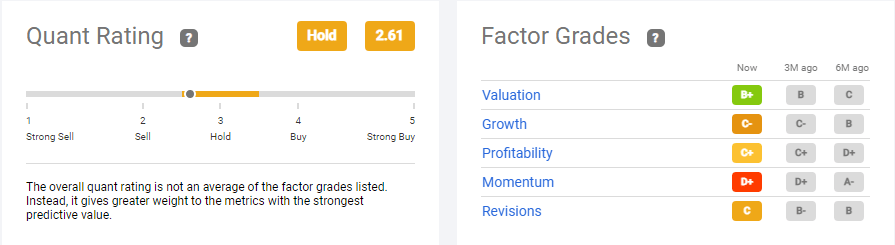

Despite the recent price drop, quant ratings also suggest that it may be prudent to avoid buying Fulton's stock. The bank received a hold rating with a quant score of 2.61. Aside from valuations, the majority of its key quantitative factors indicate a downward trend. A low score on earnings, growth, and momentum indicates slim chances for a swift turnaround.

On the other hand, Fulton is regarded as a good stock for dividend portfolios due to its high dividend yield and 32-year dividend payment streak. Although its dividends remain secure, a dividend increase in 2023 appears unlikely due to a significant drop in earnings. The company's dividend payout ratio already exceeded 50% of earnings in the first quarter of 2023, which is significantly higher than the sector median and its 5-year average of less than 50% of earnings. The bank earned an F quant grade on dividend safety and a D on growth, which is not encouraging when considering a dividend stock for a recessionary year.

In Conclusion

Fulton Financial Corporation does not seem to be a reliable stock for dividend portfolios or dip buyers. Its future fundamentals appear bleak, with declining low-cost deposits, tightening lending markets, and struggling end markets. Investors looking to capitalize on the share price collapse of regional banks may consider other opportunities with high quant grades, such as LCNB Corp. (LCNB) and Peoples Bancorp Inc. (PEBO).

For further details see:

Fulton Financial: First Quarter Suggests Headwinds Ahead