AZUL - Fundamentals Do Not Justify Azul's Discount To Gol

2023-11-29 14:42:05 ET

Summary

- Azul's margins have benefited from jet fuel prices decreasing 30% YoY in Brazil. However, this trend reverted in 3Q23.

- The company has been moderately successful in recapitalizing via issuing equity at premiums and renegotiating debt and leases. Some terms are yet to be disclosed.

- I do not find Azul attractive for long-term buyers, however, the company presents a significant valuation discount to its competitor Gol, despite no fundamental reasons to back it.

Azul ( AZUL ) is one of the two Brazilian pure-play domestic airlines, with Gol ( GOL ) and LATAM ( LTMAY ).

I have covered Azul a few times already ( January 2023 , August 2022 , December 2021 ). Generally, my take has been negative, given the difficulties of running an airline profitably and the company's high leverage.

In this article, I review the recent developments affecting Azul, particularly the increase in margins caused by fuel prices decreasing in 2023 and the renegotiation of a portion of their debt and lease payments.

Besides this, I bring to your attention what I believe is an interesting mispricing in the market: Gol trades at larger valuations than Azul in both market cap and EV terms; however, Gol seems to be in a similar or worse position than Azul across several business metrics. The two stocks move very close despite their fundamental business divergence.

I do not like long/short strategies and, therefore, would not buy Azul and short Gol. However, this information might be helpful for a reader more interested in that strategy. For an investor looking to have exposure to the Brazilian airline market, Azul is a better vehicle than Gol.

Recent profitability increase

Azul has increased its profitability significantly in 2023. This has been due to an expansion of margins coupled with increased business.

For 3Q23 , the company revenues grew 13% YoY, but the operating margin expanded 10 percentage points, meaning operating profits grew 130%.

There have been three forces behind this recovery.

First, the recovery in Brazilian domestic air traffic, back to pre-pandemic levels.

Second, jet fuel prices, controlled by the public-private giant Petrobras ( PBR ), were down close to 30% YoY as of 3Q23. Despite flown kilometers growing 11% YoY, fuel costs decreased by 30% for Azul.

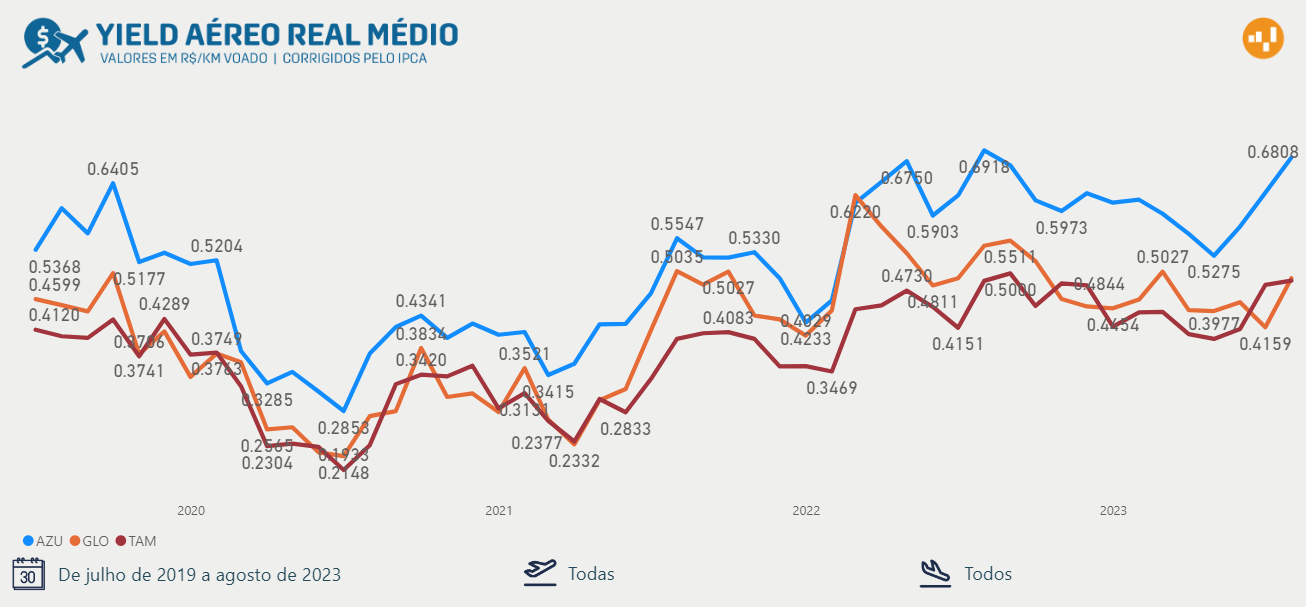

Third, Azul resisted the urge to decrease the cost of its tickets compared to its competitors Gol and LATAM, as shown in the chart below by ANAC.

Average real yield (BRL per kilometer flown) for AZUL, GOL and LATAM (ANAC)

{kind=link}

Unfortunately, Petrobras announced in September an increase of 21% in the cost of jet fuel , followed by another 5% in October. With this, the cost of jet fuel is only 12% lower in 4Q23 than it was during 4Q22.

This will probably affect Azul's margins unless it continues increasing the price per kilometer flown. In my opinion, this is difficult, given the already large gap between Azul and its competitors.

Recapitalization

Azul's has an equity deficit of $4 billion, and faces debts and lease maturities of more than $5 billion, albeit concentrated by the end of this decade.

To recapitalize, the company renegotiated in the third quarter part of its deferred lease payments (for an undisclosed amount so far) in exchange for a $375 million note payable in 2030 with a 7.5% coupon (yield including discount undisclosed) plus $570 million in Azul shares at BRL 36 per share. This is almost a 100% premium to the price at which Azul shares traded for most of 2023 (between 15 and 20 reais per share).

Further, the company issued $800 million in bonds maturing in 2028 at close to a 12% coupon.

These terms are much better than Gol's recent recapitalization financed by the Abra Group, where it exchanged notes paying less than 10% coupon for notes paying 18%, on top of that, issuing 100% warrants without any premium on the strike (BRL 5.8 strike versus Gol shares trading close to BRL 6 for most of the year).

Azul has not yet released all of the details of this recapitalization. Specifically, it has not released a lease maturity schedule.

The unjustifiable discount to Gol

Both in terms of market cap and EV, Azul trades at a lower price than Gol. This has been this way since Azul went public in 2018.

Further, the stock prices of both companies trade in almost lockstep.

To me, this seems unjustifiable, given that in every one of the business measures considered, Azul defeats Gol, and increasingly so.

Both companies have similar levels of cash and debts plus capital leases.

Azul has had higher margins, which are less cyclical and has recently matched Gol's revenues.

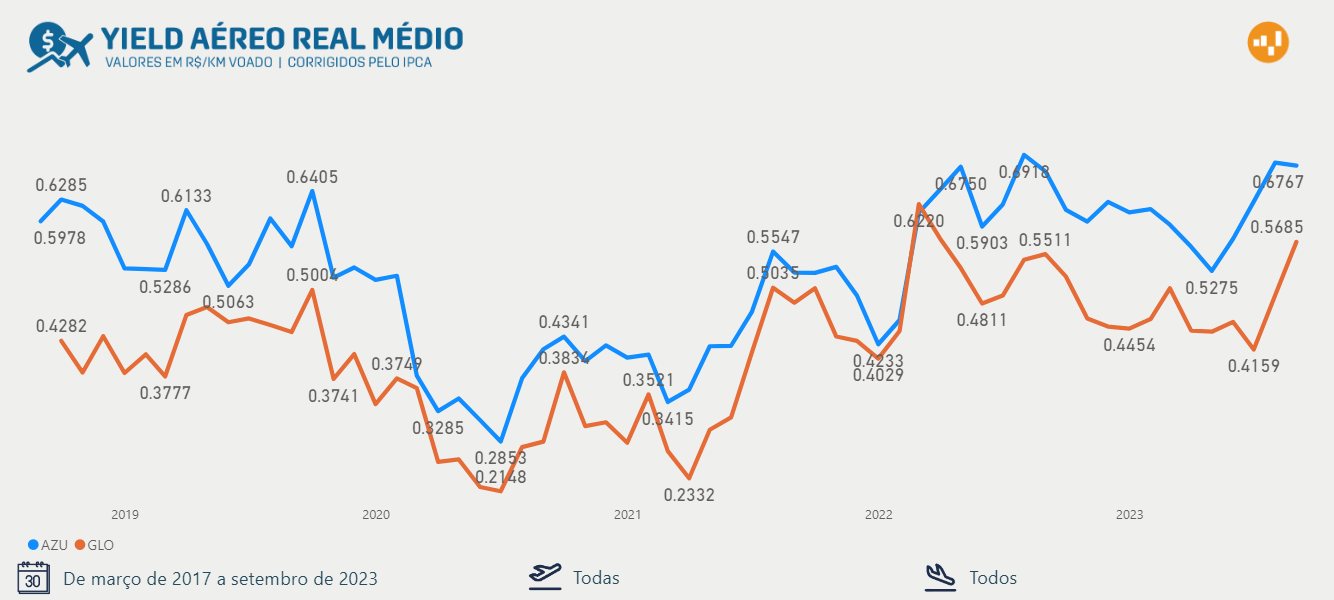

Azul has historically commanded a premium yield price per kilometer flown, as shown in the chart below by ANAC.

Cost per kilometer flown, in BRL, for Brazilian domestic flights, by airline (AZUL, GOL) (ANAC)

{kind=link}

Finally, I believe Azul has a better aircraft strategy for a country as sparsely populated as Brazil. Azul has a diversified aircraft base, including Cessnas, ATRs, Embraers E2s, and Airbus widebody, whereas Gol concentrates on the Boeing 737 alone.

Although concentration on a single model provides cost advantages, the diversity of Azul's models allows it to cover routes with different traffic densities with the scale that makes sense for each route.

Conclusion

I continue to believe that neither Azul nor Gol are suitable investments at these prices and in their current capital situation. However, Azul makes more sense than Gol, given its discount to the latter and better operations.

The decrease in fuel prices has benefited both companies but has now begun to revert. I believe price competition will push these companies' margins lower. Azul commands a premium on the market that might help it weather it better.

Both companies are still heavily leveraged, but while Azul managed to sell its stock at premiums to traded prices and replace lease payments with average-yielding debt, Gol diluted its shareholders and issued expensive debt.

I believe, eventually, one of them is going to get massively recapitalized via almost complete dilution to current shareholders or will be allowed to leave the market. Given the Brazilian government's interest in keeping air ticket prices low, I am inclined toward the first option.

For further details see:

Fundamentals Do Not Justify Azul's Discount To Gol