WMT - Funko: Buyer Beware

2023-10-20 16:56:28 ET

Summary

- Funko, Inc. is a small cap "Busted IPO" that manufactures collectables and has recently experienced insider buying.

- The company has faced management turnover and challenges, but earnings are expected to improve in FY2024.

- Funko may benefit from the popularity of the Barbie phenomenon, but its stock has been volatile and faces challenges in maintaining value.

- A full investment analysis follows in the paragraphs below.

Beware of the people who observe everything, yet don't speak anything .”? Nitya Prakash.

Today, we look at a small cap "Busted IPO" with some recent insider buying in its stock. The company has had its share of management turnover and other challenges recently. Earnings are expected to turn around in FY2024 and the company may benefit from the Barbie phenomenon. An analysis follows below.

{kind=link}

Company Overview:

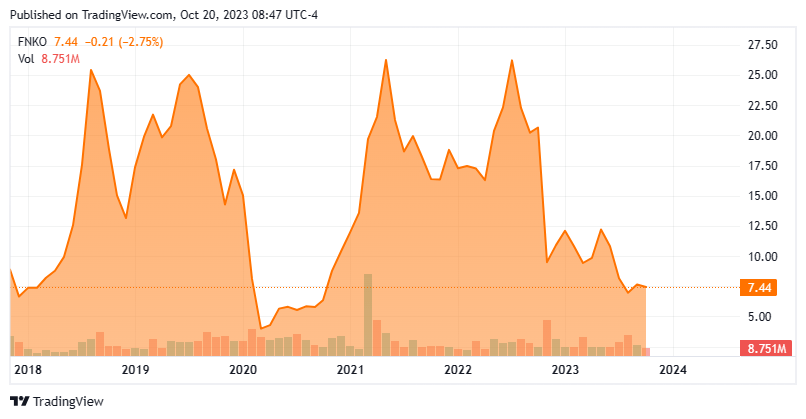

Funko, Inc. ( FNKO ) is an Everett, Washington based pop culture concern, focused on the manufacture of collectables, consisting of vinyl figures, bobbleheads, action toys, board games, non-fungible tokens, accessories, and other knick-knacks that are sold to enthusiasts and collectors. Known for its Pop! figurines, the company boasts over 1,000 licenses from more than 250 content providers. Funko was formed in 1998 and went public in 2017, raising net proceeds of $117.3 million at $12 a share in an IPO known as the worst of the 21st century, with its stock closing the first day of trading at $7.07 a share, down 41%. Shares have been volatile throughout the company's history as a public company and after the stock's recent sell-off have made a round trip and sport an approximate market capitalization of $385 million.

Operating Model

The company enters into licensing agreements with many franchises to create products mimicking popular characters from said franchises. Disney ( DIS ) , which includes Lucasfilm and Marvel, is by far the company’s largest licensor, accounting for 44% of its FY22 net sales. Under many of these agreements, the licensor owns the intellectual property rights, which means that upon license termination, Funko can no longer sell its products. Furthermore, the deals are generally limited to specific properties, product categories, and territories. In return for the license, the company pays its licensors a royalty on its product sales, which has averaged ~16% from FY20-FY22.

Product Lines

Funko’s core product line includes Pop! Vinyl, which are figures with large squarish heads, tiny bodies, and large, circular black eyes, modeled after Japanese caricatures known as Chibi. For example, a Pop! Captain Hook figure sells on its website for $12 – most items sell for $15 or less. This core series also includes newer collectible brands such as Soda, Vinyl Gold, and Popsies. Want a 5-inch Bo Jackson Vinyl Gold (a less caricatured) figurine? $12. These Core Collectables accounted for FY22 net sales of $998.4 million, or 76% of Funko’s total top line.

The company also owns Loungefly, which is a line of collectable mini-bags, backpacks, wallets, and purses that feature popular characters, such as Hello Kitty and Disney princesses. These are more expensive. Want a Michael Myers Glow Mask Cosplay Mini Backpack? $80. Sales of Loungefly accounted for FY22 net sales of $253.0 million, or 19% of Funko’s total.

The balance (Other) includes toys, games, as well as emerging brands and was responsible for 5% of the company’s top line.

According to a 2022 investor presentation, the average age of a Funko customer is 36 years with sales breakdown approximately 36% to the collector, 33% to the enthusiast, and 31% to the occasional buyer. The U.S. market is responsible for ~73% of net sales.

Operational and Stock Price Performance and Recent Struggles

The company believes that its broad portfolio of licenses will provide study revenue and insulate it from boom or bust trends that pervade individual collectibles. Instead, this approach has led to inventory issues.

After its brutal debut, shares of FNKO climbed to an all-time high of $31.12 in September 2018, plunged to a pandemic-induced low of $3.12, and then started to rebound as federal assistance flowed into the economy. During this peak-to-trough and rebound in its stock, Funko’s operational performance was relatively consistent. Adj. EBITDA as a percentage of revenue ranged between 15% and 17% (with the understandable exception of FY20 (12%)) during FY17-FY21, while revenue doubled to $1.03 billion.

That all changed near the end of FY22. Coming out of a largely successful campaign in FY21, management initially forecasted FY22 non-GAAP EPS of $1.83 a share and Adj. EBITDA margin of ~14.6% on net sales of $1.26 billion, based on range midpoints. It then raised those estimates twice – after Funko’s Q1 2022 and Q2 2022 financial reports. Then in November 2022, the company posted Q3 2022 non-GAAP earnings of $0.28 a share, which missed consensus by $0.22 a share as inventory management issues were blamed. After raising its outlook twice in the prior two quarters, the company lowered its FY22 forecast from a range midpoint of $1.94 to $0.90, while lowering Adj. EBITDA margins from 14.6% to “high single digits.” This stunning reversal in outlook so late in the year destroyed management’s credibility. Having achieved a post-pandemic high of $27.79 in August 2022, shares of FNKO were taken out behind the woodshed and shot, losing 59% of their value in the subsequent trading session, closing at $7.92.

That report facilitated the ousters of the CEO and CFO, of whom the former was replaced by a prior CEO. Also, 258 jobs were eliminated. The CFO position was filled by ex- Walmart ( WMT ) executive Steve Nave in March 2023. He also assumed the newly created role of COO. Shortly after the close of Q1 2023, Funko approved an inventory reduction plan that entailed the destruction of $30.1 million of property. Management’s first crack at FY23 was Adj. EBITDA of $62.5 million on revenue of $1.36 billion (versus Adj. EBITDA of $97.4 million on revenue of $1.32 billion in FY22). Then in July 2023, the newly installed CEO stepped down and an interim CEO was hired.

Q2 2023 Financials & Revised Outlook

With that tumult as a backdrop, Funko reported financials on August 3, 2023, posting a Q2 2023 loss of $0.43 a share (non-GAAP) and Adj. EBITDA of negative $7.6 million on revenue of $240.0 million versus a gain of $0.26 per share (non-GAAP) and Adj. EBITDA of positive $31.8 million on revenue of $315.7 million in Q2 2022. Gross margin, which spent most of past six years in the mid-to-upper 30s, was 29.2% in Q2 2023 versus 32.7% in the prior year period. Average net sales per active property (756 in total) decreased 23%.

Management stated that it would cut back the number of product types (e.g., keychains) it sells to reduce the complexity of its business, laying off an additional 180 employees in the process. The new team was also compelled to reduce its FY23 Adj. EBITDA forecast from (a briefly revised higher) $70 million to $25 million on revenue of $1.09 billion, based on range midpoints.

Already down on the exit of the "old new" CEO, shares of FNKO fell 14% to $6.37 in the subsequent trading session before hitting a post-pandemic low of $5.27 on August 16, 2023.

Balance Sheet & Analyst Expectations:

With a disastrous twelve months on the income statement , the balance sheet has been negatively impacted, reflecting cash of $36.8 million and debt of $305.0 million, up from $245.8 million at YE22. Based on its FY23 outlook for Adj. EBITDA, net leverage is a concerning 10.7. Inventories are down $59.1 million since YE22 to $187.3 million, but accounts receivable are down $30.5 million while accounts payable are up $15.7 million. In short, not a very encouraging picture.

Prior to the credibility “ bomb ” being dropped (as one analyst described it at the November 2022 conference call), eight Street prognosticators covered Funko with five buy or outperform ratings and three holds with a mean price target of around $30. Since second quarter earnings posted, five analyst firms including JP Morgan and Goldman Sachs and Stifel Nicolaus have reissued Hold/Sell ratings on the stock with price targets proffered between $5.00 and $10.50 a share. D.A. Davidson seems to be the lone optimist on the stock maintaining a Buy rating and $9.50 price target.

On average, the Street expects Funko to lose $0.88 a share on net sales of $1.09 billion in FY23, followed by a gain of $0.37 a share on net sales of $1.16 billion in FY24. That said, given the events of the past ten months, the Street’s forecasts (as well as management’s) are toothless.

CFO Steve Nave used the selloff after the 2Q23 financial update as a buying opportunity, initiating a position by purchasing 55,500 shares at an average price of $5.45 on August 17, 2023. Beneficial owner Working Capital Advisors has used the post earnings report period to accumulate more than 1.5 million shares, cost-averaging while upping its ownership interest to north of seven million shares, just over 15% of outstanding float.

Verdict:

With approximately one-third of its sales to the occasional buyer, there must be something en vogue to keep the needle moving at the top of the income statement, and Barbie may be it. The stock has rallied significantly off the August 2023 low, aided by news that Funko introduced products related to the movie beginning in July, including Pop figures of Barbie and Ken rollerblading for $29.90. That could give the company and its stock a bit of a jolt as the iconic brand becomes a Pop. The quandary is that every time one of its products has a chance to be valuable – like Barbie and Ken Pops – Funko feels the pressure to produce more to generate revenue for shareholders, making it less attractive to collectors.

That predicament is really beside the point. Unless the company can reinvent itself, the outlook is not bright with Pops! trending towards becoming this generation’s Beanie Babies. Based on its own FY23 revenue projection, the decline in their popularity has begun and a " collector" will be able to pick up one (and possibly a share of FNKO) at a yard sale for $0.50 in a few years. Just like baseball cards in FY21, these collectables have seen their peak as disposable income becomes much dearer absent any new unprecedented federal assistance. With apologies to the CFO and beneficial owner, avoid Funko.

Beware the honest, ... they will hurt you just to feel clean .”? Kieron Gillen.

For further details see:

Funko: Buyer Beware