SLG - Further Downside For Office REITs Is In Store But Equity Commonwealth Might Be An Exception

2023-06-12 06:51:38 ET

Summary

- Office REITs have seen share prices drop between 14.8% and 28.9% this year due to a lack of demand caused by changes in working conditions.

- Office vacancy rates in the US have worsened, with 65% of the 200 largest areas reporting increases in vacancy rates since 2019.

- Investors should approach the office REIT market cautiously due to the potential for struggling REITs with high debt and difficulty finding tenants.

- But one bright spot is Equity Commonwealth due to its de-risked nature and tremendous financial flexibility.

There have been some rather significant rumblings going on in the market regarding the office space rental industry. With reports indicating significant problems in the space because of a lack of demand that has been caused by a change in working conditions, as well as due to warnings made by top investors and industry experts, shares of most office REITs are down significantly so far this year. This is at a time when the S&P 500 is up over 9% and the NASDAQ has risen over 30%. This may cause some investors to gravitate toward these companies with the hope of picking some up on the cheap. I will not say that some opportunities do not exist. They very likely do. But I do think investors would be wise to approach this situation very cautiously because of what looks like a meaningful paradigm shift.

Rumblings in the market

So far this year, there have been a number of high-profile investors and industry experts who have weighed in and offered rather discouraging opinions regarding the state of the office space leasing market. At the annual shareholders meeting for Berkshire Hathaway ( BRK.A ) ( BRK.B ), for instance, billionaire investor Charlie Munger said that, as leases come due, he expects demand for lease renewals to drop and for more favorable tenant terms to be compelled on property owners because of the massive shift we have seen in recent years to work from home. He even went so far as to say that ‘a hollowing out of the downtowns in the United States and elsewhere in the world’ is slated to occur. His partner, Warren Buffett, was not as harsh in his assessment. But he also worked at the industry with a rather jaundiced view.

Earlier this year, Jamie Dimon, the CEO of JPMorgan Chase ( JPM ), issued a warning about the commercial real estate market. His belief is that souring commercial real estate loans that would be caused by a change in interest rates and a reduction in demand for commercial real estate because of remote working, could threaten some banks moving forward. This comes after a rather difficult couple of months that included some very noteworthy and painful bank failures.

What the data says

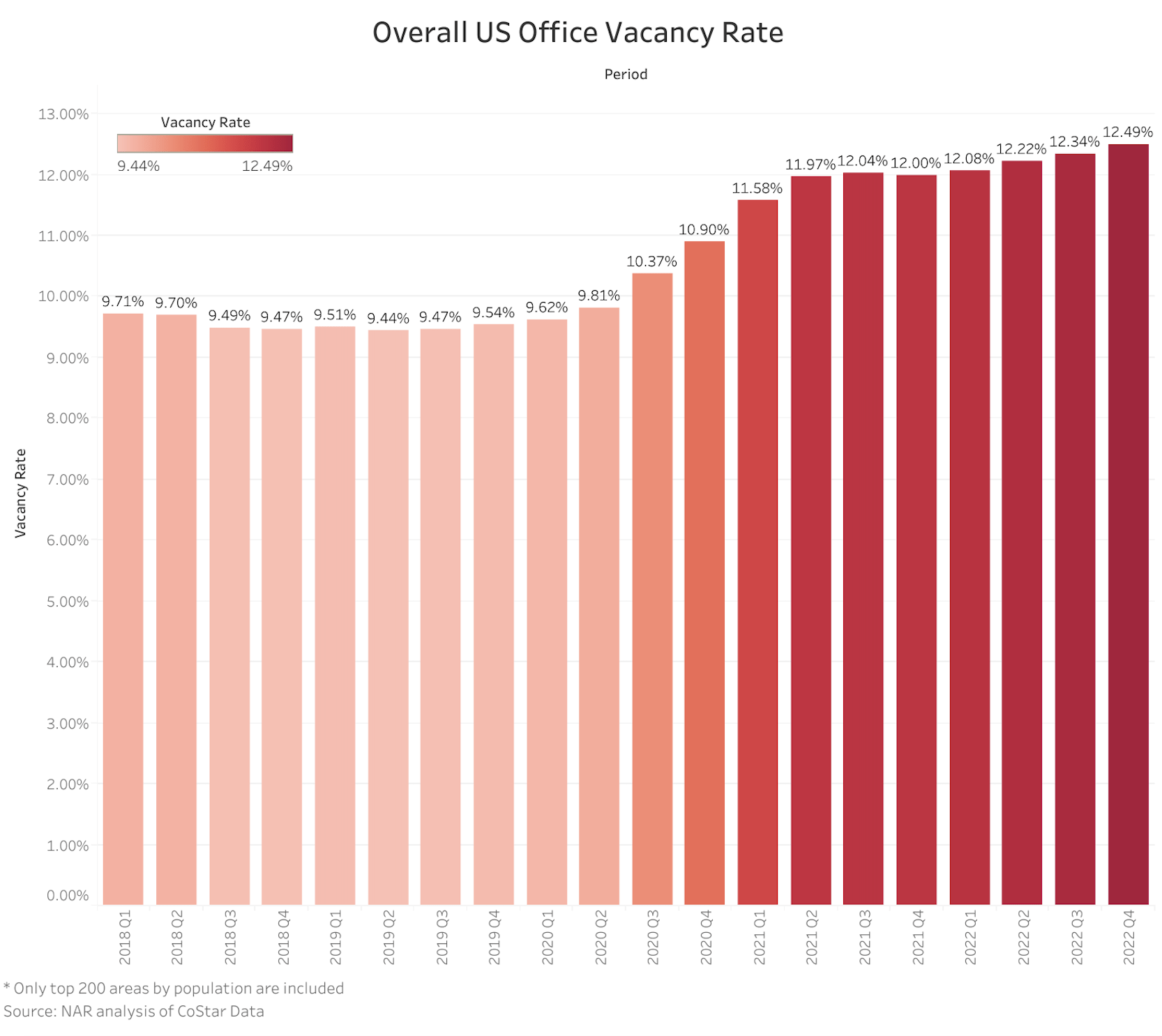

As an investor, what matters to me most is not necessarily what other people are saying. It is important, especially when those people know more than I do. But what's even more important is what the data says. And unfortunately, the data does seem to align quite well with these experts. Consider the overall office vacancy rate currently in the US. From 2018 through the second quarter of 2020, the vacancy rate remained pretty much range bound between a low point of 9.44% and a high point of 9.81%. In the third quarter of 2022, office vacancy rates popped up to 10.37%. This number continued to worsen, eventually hitting 12.49% in the final quarter of 2022.

National Association of Realtors

{kind=link}

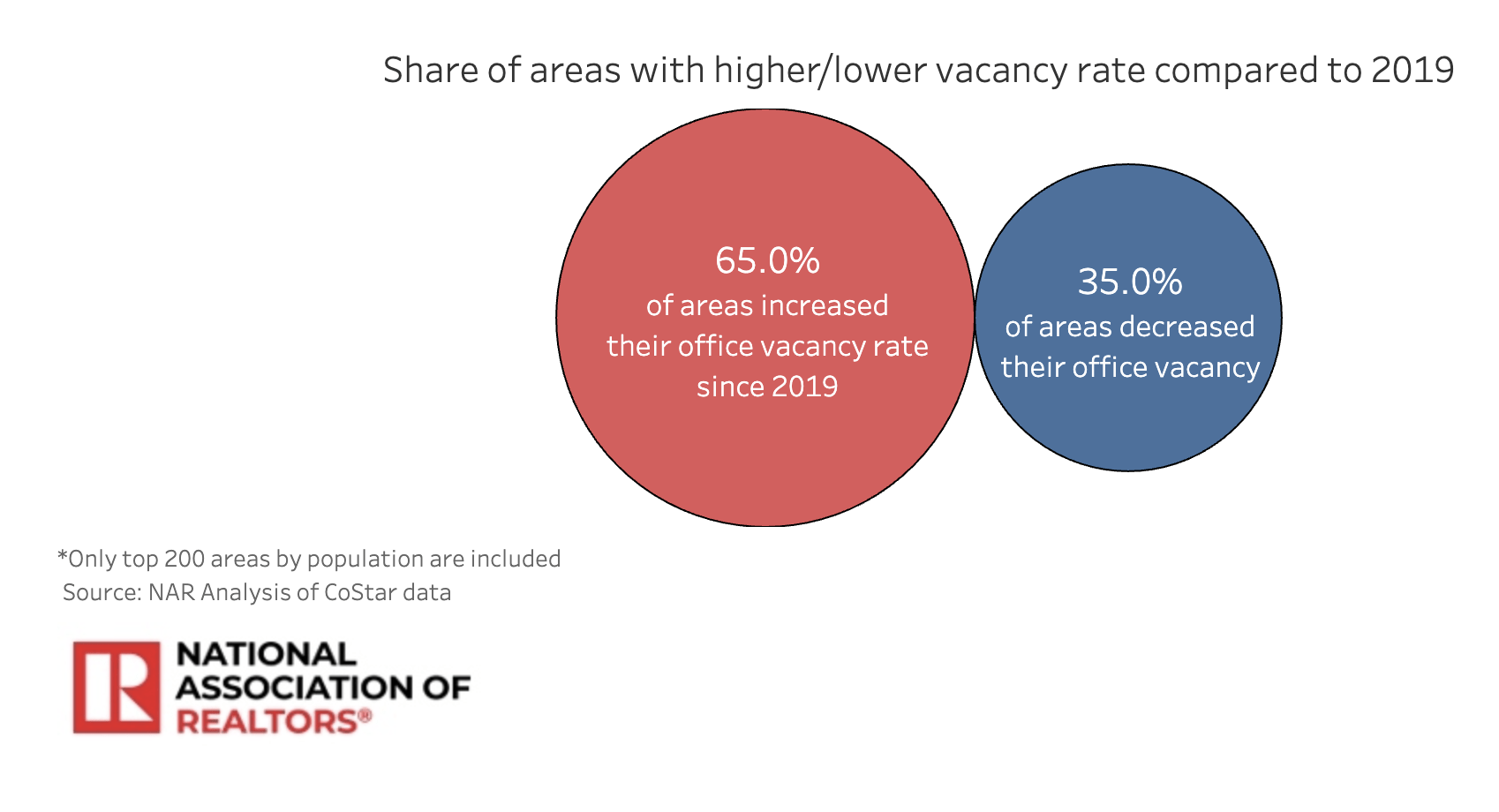

When you dig deeper into the data, you start to find that, while most areas have been hit, some have been hit harder than others. Since 2019, 65% of the 200 largest areas, by population, reported increases in their office vacancy rates. This compares to 35% that saw improvements. To better understand the data, I decided to look at the data through the lens of the 10 cities that have been hit the hardest . These are the 10 cities that have the overall highest vacancy rates as of the most recent data provided. At the very top of the list, you can see Austin, Texas. It has a vacancy rate of 22%. A close second is Houston, Texas, at 21.5%. Outside of the Lone Star State, the worst is Denver, Colorado, with a vacancy rate of 19.9%. Other areas of pain include Atlanta, Georgia, San Francisco, California, Brooklyn, New York, and others.

National Association of Realtors

{kind=link}

It is imperative that I point out that, as bad as this data is, the actual picture facing the office space market is far worse. Because of the multi-year contracts that tenants sign, you only see how much of the office space is not being leased, not how much is actually empty. According to multiple reports , the shift to remote work from an office work has resulted in approximately half of all office space in the roughly $20 trillion US commercial real estate market being empty as of this year. This is after many companies started demanding that workers show up either full time or part time into the office as opposed to working entirely from home like they did during the pandemic.

Author - CommercialEdge

REITs are already feeling the pain

Unfortunately for investors, REITs that have a tremendous amount of focus on the ownership and leasing out of office properties have been hit hard. As part of my research for this article, I decided to focus on nine REITs that have significant exposure to office properties. I used a specific set of criteria in choosing these firms. For starters, I only focused on REITs that were either primarily or exclusively focused on office properties. Second, I decided only to look at those that had market capitalizations of $500 million or more. And finally, I decided to leave out from the analysis REITs that derive a large portion of their revenue from the government. This is because I view the government as less likely to move away from leasing commercial property.

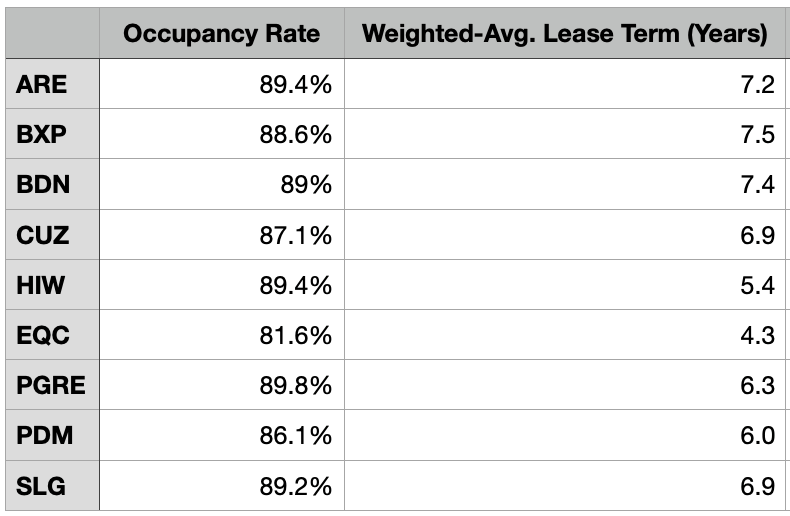

What I found can aptly be described as a bloodbath. Even while the general market is up materially this year, these nine REITs have seen their share prices drop by between 14.8% and 28%. This is in spite of the fact that they all have fairly high occupancy rates and a decent amount of time left on current leases. The worst of the group, for instance, has an occupancy rate of 81.6% and 4.3 years for the weighted average lease term remaining. The best of the group, meanwhile, has an occupancy rate of 89.8%, with 6.3 years remaining. In terms of the weighted average lease term, the highest on the list is 7.5 years.

{kind=link}

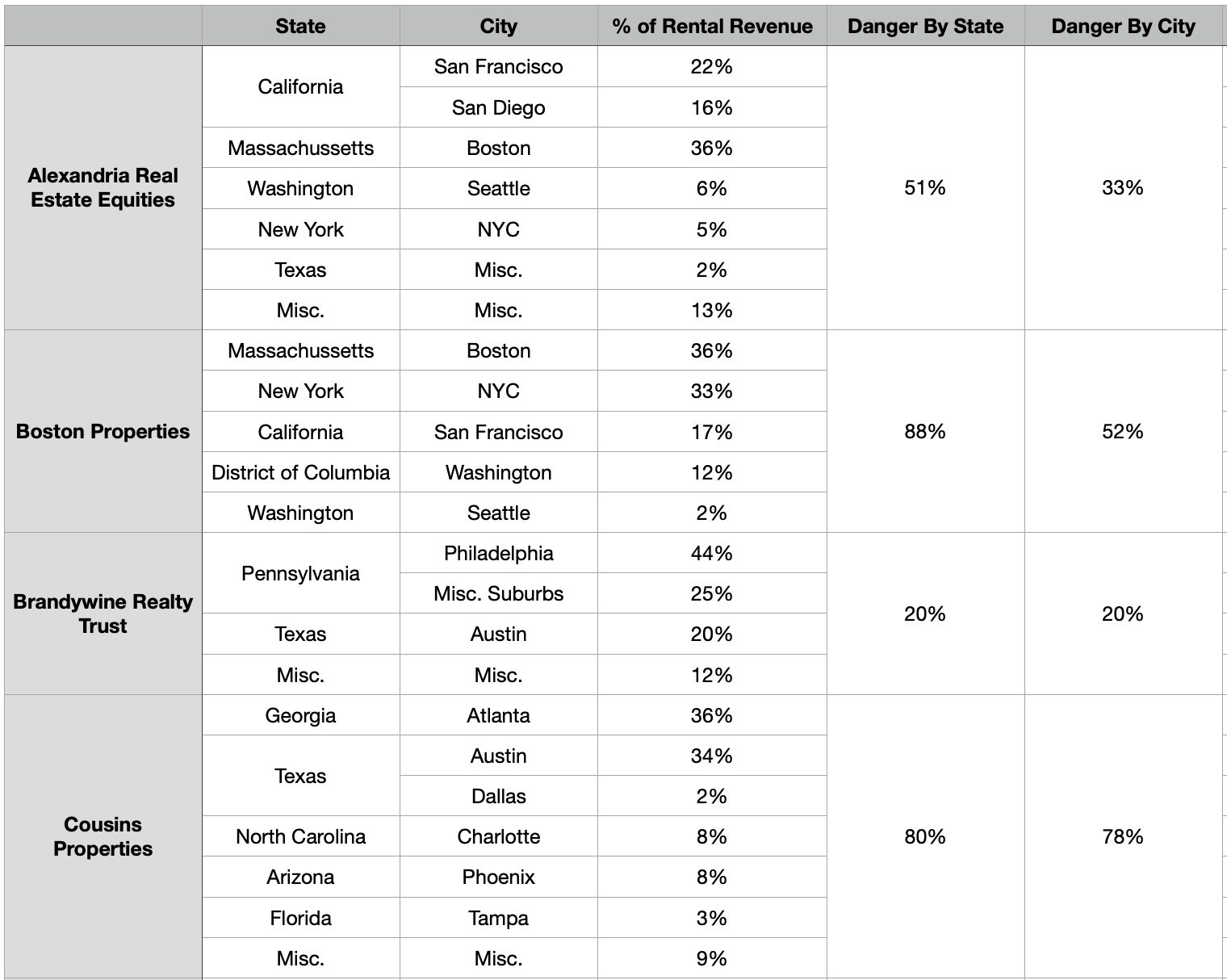

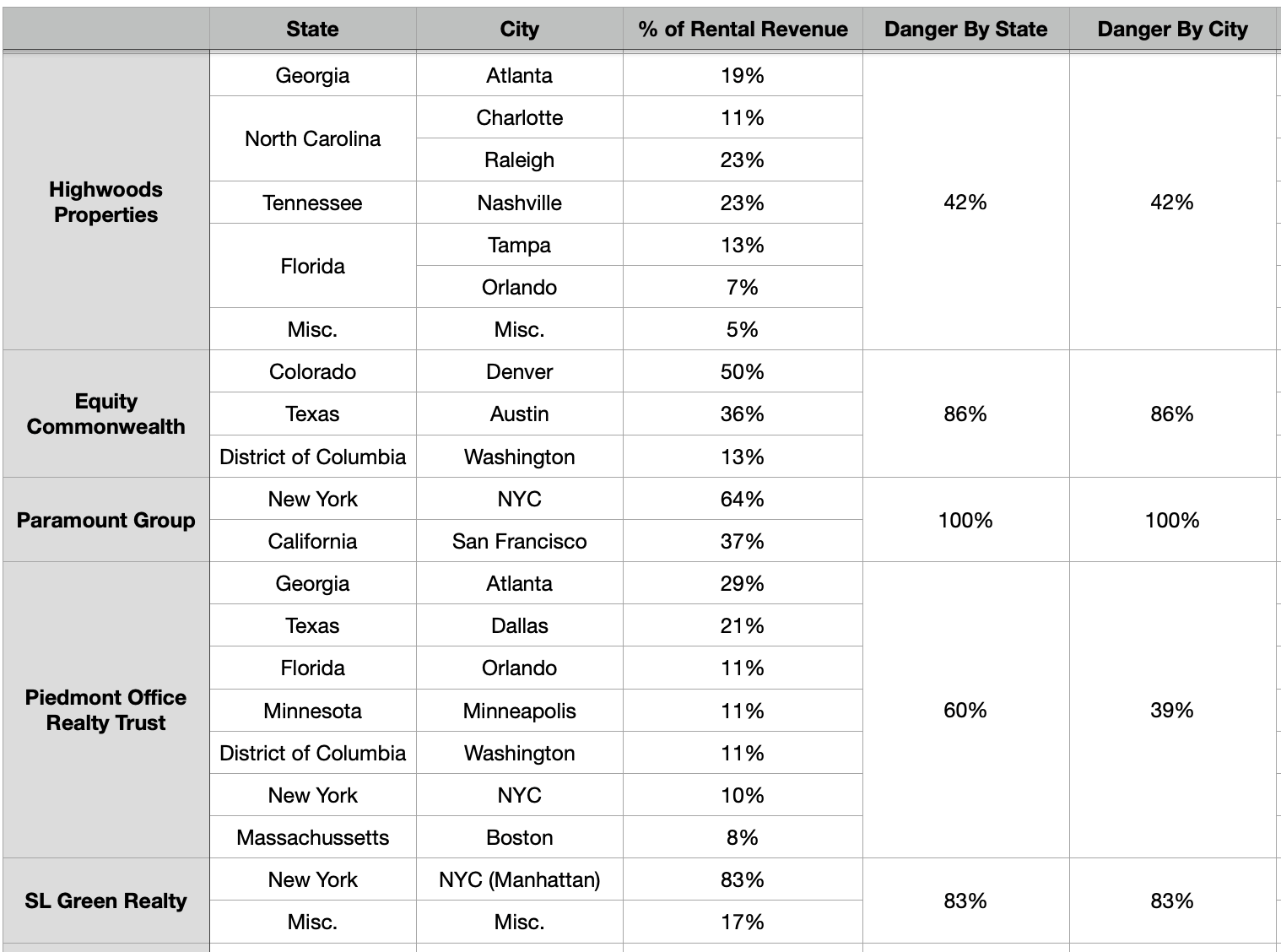

To see what kind of exposure they each might have to the markets that have been most impacted, I broke out their rental revenue by the specific markets in question. As an example, Alexandria Real Estate Equities ( ARE ) derives about 51% of its rental revenue from states that have a top ten city listed in them. And it arrives 33% of its rental revenue from one of the worst 10 cities listed. It's important to note that the numbers that I show are based on public filings and are limited to some degree. For instance, some of the REITs don't specify which cities or states they get some of their rental revenue from. So the numbers that I provide here should be viewed as the lowest amount of exposure that these companies have.

{kind=link}

Given these restrictions, it looks as though the REIT that is in the best shape from an exposure perspective is Brandywine Realty Trust ( BDN ). From what I can tell, only 20% of its revenue comes from states and cities that are in the top ten worst for vacancy rates. It also has one of the highest occupancy rates at 89%, with the second highest weighted average lease term on the list at 7.4 years. The REIT that has the greatest exposure is Paramount Group ( PGRE ), with 100% of its rental revenue coming from problem cities and states.

{kind=link}

A great prospect to consider right now

Of the nine office-oriented REITs that I analyzed, one that struck me as particularly interesting that could offer some nice upside is one that you might least expect. This would be Equity Commonwealth ( EQC ). The reason why I say that this may be a surprise is because, of all the companies analyzed in this piece, it looks to be the riskiest at first glance. Its occupancy rate of 81.6% is the lowest in the group and the 4.3 years for the weighted-average lease term is also the lowest. To make matters worse, 86% of its annual rent revenue comes from the problem areas that I identified already. Add on top of this the fact that it is the second-best performer of the group, with shares falling only 16.6% so far this year, and you might be shocked that I'm not taking a very bearish stance on the business.

This is where deeper analysis of any company besides just the surface level data is important. The fact of the matter is that Equity Commonwealth is very much unlike any of its peers. Over the past nine years or so, management has been working to sell off most of the company’s assets. During this time, they succeeded in selling off 164 properties and three land parcels. The properties in question totaled 44.3 million square feet. These sales brought in $6.9 billion worth of cash, plus $704.8 million worth of stock in another REIT called Select Income REIT. Today, the company has only four properties in its portfolio that work out to 1.5 million square feet of space.

{kind=link}

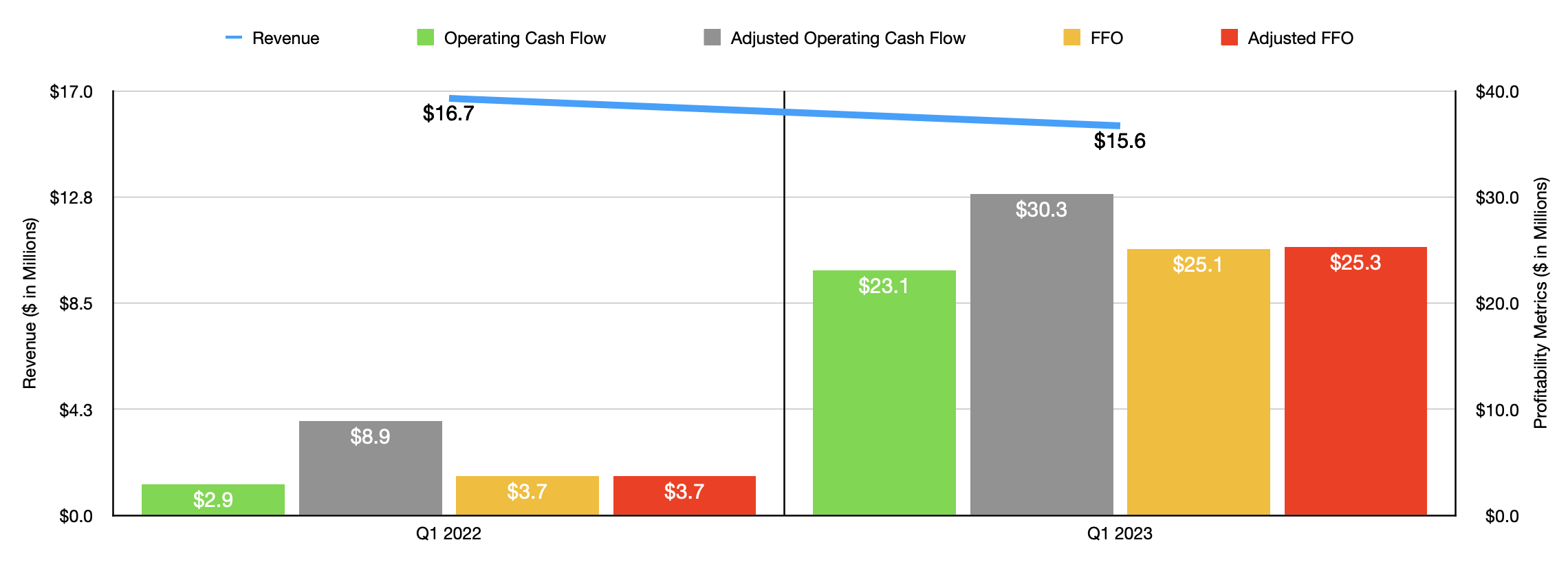

The great thing about Equity Commonwealth is that management decided to keep most of the cash on the firm's balance sheet. As of the end of the most recent quarter, the company had $2.13 billion worth of cash, cash equivalents, and investments. It also had no debt. Much of its financial performance is based on the returns that cash brings in. Consider the most recent quarter. During that time, revenue for the company came in at only $15.6 million. And yet, operating cash flow was $23.1 million. If we adjust for changes in working capital, it was $30.3 million. FFO, or funds from operations, totaled $25.1 million, while the adjusted figure for this came in at $25.3 million. This massive amount of profitability that translates to cash flow margins that are well in excess of 100% was thanks in large part to a $26.8 million increase in interest and other income that the company generated during that time. With high interest rates, the firm should benefit from the investment of its capital.

This is also exciting for a couple of other reasons. First, there's the fact that the book value of equity of the company, which again is largely cash, stands at $2.37 billion. That's actually higher than the $2.29 billion market capitalization of the firm. Second, there's the fact that this provides the company with a tremendous amount of capital to serve as fuel for growth when it decides to deploy it. If we do see a true collapse in the office niche of real estate, this could allow the company to get some rather fantastic deals once the space shows signs of stabilizing, if that ever occurs. Or it could give the company the opportunity to invest the capital in other real estate that could diversify it and put the company in a new direction entirely. Of course, having such a large cash balance also increases the risk of management perhaps doing something suboptimal. But that's not necessarily the worst risk for investors to take.

Takeaway

Based on the data provided, I would make the case that, right now, the office REIT market is incredibly dangerous. Those who are bullish regarding the space may accurately point out that the lease terms of the companies I cited still indicate that they have years before significant pain develops. And during that time, we might see a continued shift back to working from the office. I don't think that this is terribly likely. And if this shift does not materialize, you could end up with REITs that are struggling to get tenants and that, in most cases, are saddled with debt. When you consider how many different types of REITs are on the market today, I see no reason to be focused on this rather troubled market niche. After all, the primary objective of investing in REITs is to capture stability, steady growth, and attractive income that builds up value over an extended period of time. By focusing on a market segment that has a lot working against it, investors are taking on a rather significant amount of risk that they don't have to.

Having said that, one bright spot at this time does seem to be Equity Commonwealth. The company's surplus of cash, its low trading value relative to its book value, and its inherent flexibility all make it a compelling prospect at the present moment. I would make the case that it likely offers the best prospects for investors at this time and I have decided to rate it a 'strong buy' for now.

For further details see:

Further Downside For Office REITs Is In Store, But Equity Commonwealth Might Be An Exception