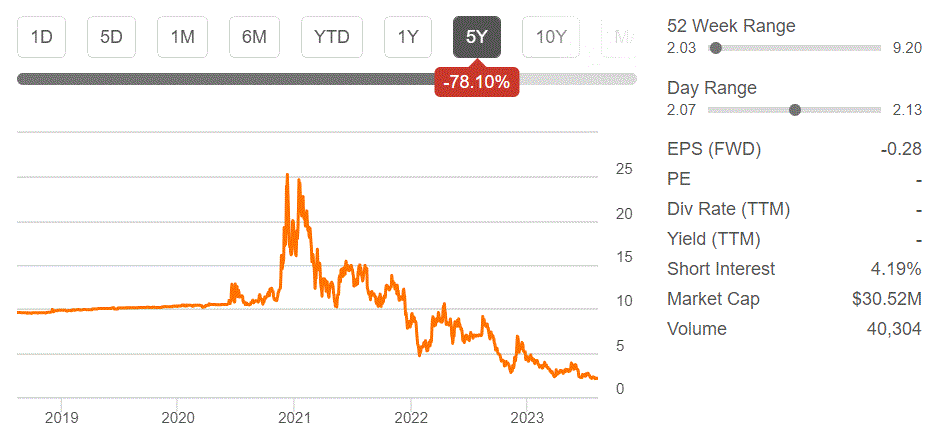

HTOOW - Fusion Fuel Green: Buying The Steep Selloff But Cautiously (Rating Upgrade)

2023-08-16 09:14:39 ET

Summary

- EU must aggressively pursue green energy due to strained Russia-EU trade relationship.

- Fusion Fuel is a startup producing solar-powered hydrolysis units, with its low unit costs potentially allowing for a broader market, beyond large-scale producers.

- Fusion Fuel recorded revenues of 582,000 euros and aims to earn 25 million euros this year, with potential for exponential growth.

Investment thesis: With the Russia-EU business and trade relationship seemingly ruptured for good, the EU now has no choice but to aggressively pursue a path of green energy production and utilization, which it can rely on as a domestic source of energy. One of the greatest tasks is to counteract the unreliable aspect of renewable sources of energy such as wind & solar. While giant grid batteries and other solutions provide at most hours or a few days of backup, the need is for variations in power output that can last for weeks or even months, which is where green hydrogen comes into the equation. For this reason, Fusion Fuel (HTOO) is a very interesting potential investment opportunity.

It is a startup that produces solar-powered hydrolysis units. While many other companies are getting into this emerging potentially crucial industry in Europe and the world, Fusion Fuel has several advantages from an investor's point of view, including the fact that it does not carry legacy baggage, like the likes of Shell, which is a leading contender to dominate the green hydrogen industry in Europe. Some drawbacks include the emergence of the nuclear-power-derived hydrogen industry, as well as the potential failure of Fusion Fuel's yet-to-be-proven technology to compete with peers. While the decline in its stock price relative to my average buying price is significantly lower, I am opting to only increase my position in this stock slightly to improve my average buy-in price, rather than increasing my exposure significantly to what remains a high-risk, high-potential return investment opportunity, with a very intriguing big-picture story behind it.

Fusion Fuel finally starts bringing in revenues, but still a long way to profitability.

For the first quarter of this year, Fusion Fuel recorded an operating loss of just under 7.4 million euros. It is a significant improvement on the previous quarter when it lost 18.7 million euros. The highlight of the quarter is not so much the narrowing loss, but rather the fact that it achieved 582,000 euros in revenues from the sale of 62 of its HEVO units. In its 2022 annual report , Fusion Fuel estimated that it will earn 25 million euros in revenues, with 5.7 million euros in equipment sales having been already contracted by the end of last year. The start of revenue inflows is encouraging, even if there might be some further disappointment along the way.

Other newsworthy developments include yet another grant, this one in support of a hydrogen supply project that will be built in 2024, to fulfill the demand for 112 tonnes of green hydrogen per year for a Spanish company. The grant is for 3.3 million euros. These grants have been instrumental in keeping Fusion Fuel from greatly increasing its share issuance, or taking on debt. For the first quarter of the year, the number of shares outstanding increased to 14.5 million, from 13.8 million at the end of last year. There is stock dilution going on, but it is limited by the continued inflow of grants.

{kind=link}

If Fusion Fuel will indeed achieve 25 million euros in revenues this year, it will more or less be equal to its current market cap. Given hydrogen production projects coming online as well as continued sales, its revenues have the potential to increase exponentially beyond this year. Green hydrogen subsidies alone through the European Hydrogen Bank project would amount to about 450,000 euros/year for the 112 tonnes of hydrogen that were recently contracted for in Spain, as I already mentioned. Then there will be the price charged to the customer, which will add to the revenues it will earn. It should be noted that the subsidy also increases the odds of profitability, while it limits potential losses.

Perhaps one of the most important effects that the green hydrogen production subsidies will have on Fusion Fuel is that it can potentially greatly increase demand for its solar-powered hydrolysis units. It is a potentially relatively small capital investment that relatively small enterprises and even individuals can contemplate investing in purchasing, with income more or less guaranteed to flow, assuming that the subsidy will remain in place for the foreseeable future. The low cost per unit may be one of the greatest competitive advantages that Fusion Fuel has over many of its peers because it broadens the potential market for its products.

If Fusion Fuel's equipment proves to be up to the challenge in terms of quality/price, its sales can grow exponentially for the foreseeable future. Looking at its market cap of about $30 million, versus the potential sales growth that is possible, that can reach the $ billion + level/year potentially within a few years, the potential for significant stock price appreciation, thus returns on investment is very tempting.

Investment implications:

Given the emerging need for the European power grid to manage the growing share of intermittent power sources, while the continent strives to completely cease using fossil fuels for energy, Fusion Fuel is arguably part of an emerging green hydrogen industry that is still in its infancy, with huge demand potential. In my personal view, based on history, when countries like Germany saw double-digit shortfalls in renewable energy output for a whole year, the future of Europe's green-powered economy involves roughly 20% of all the wind & solar power that is generated having to be transformed into green hydrogen that can be stored and used whenever renewable power production will fall short.

{kind=link}

Assuming that eventually about three-quarters of Europe's electricity generation will come from wind & solar, which will have to include about 20% of it coming from green hydrogen , we are looking at about 13 million tonnes of hydrogen being needed every year to keep the grid stable. The revenues that the green hydrogen industry in Europe can earn from the above-mentioned subsidy of 4 euro/kilogram of green hydrogen alone, amounts to about 52 billion euros. This calculation does not include the potential increase in electricity demand as EV sales growth continues to be robust, as well as other factors, including green hydrogen hypothetically replacing natural gas-derived hydrogen in the EU economy for other uses. We should also keep in mind that global hydrogen demand is likely to also increase substantially.

One factor that might negatively impact green hydrogen production from wind & solar is the fact that the EU recently decided to arrive at a compromise in terms of how nuclear power-derived hydrogen is classified. I covered this particular issue in a previous article I wrote on Fusion Fuel this year. I continue to think that this may be one of the greatest potential impediments to the likes of Fusion Fuel capturing market share in the future. Several countries in the EU as well as abroad may take advantage of the EU decision to produce green hydrogen using nuclear power, which can then be sold on the EU market.

Given how far Fusion Fuel's stock price has gone down in the past year, I found it somewhat tempting to add to my already-existing position but only did so on a relatively modest scale. While its move into a revenue-generating company, which will hopefully be followed by it becoming a profitable company is going slower than investors would like to see, the fundamentals behind it still seem to be solid. There are of course still several potential pitfalls along the way which could derail this startup, which make me somewhat cautious in buying more, rather than just riding it out on my existing position, which at this point is down about 50%. I may decide to buy some more shares to bring down my average buy-in price, but I intend to keep my exposure to this stock limited, given that it remains a highly speculative startup, with a still very uncertain future.

For further details see:

Fusion Fuel Green: Buying The Steep Selloff, But Cautiously (Rating Upgrade)